BC

BCParticipant

Master

Hi Grahal

Sound right, all I can do now is compare live result again, but no deal on yesterday and today.

Your Strat is very good Bin!

I tried 3 or 4 times to minus 7 hours from all your times (UTC +8) to get to my time (GMT +1 / UTC +1) but I’m sure due to my ‘finger trouble’ I got big overall loss.

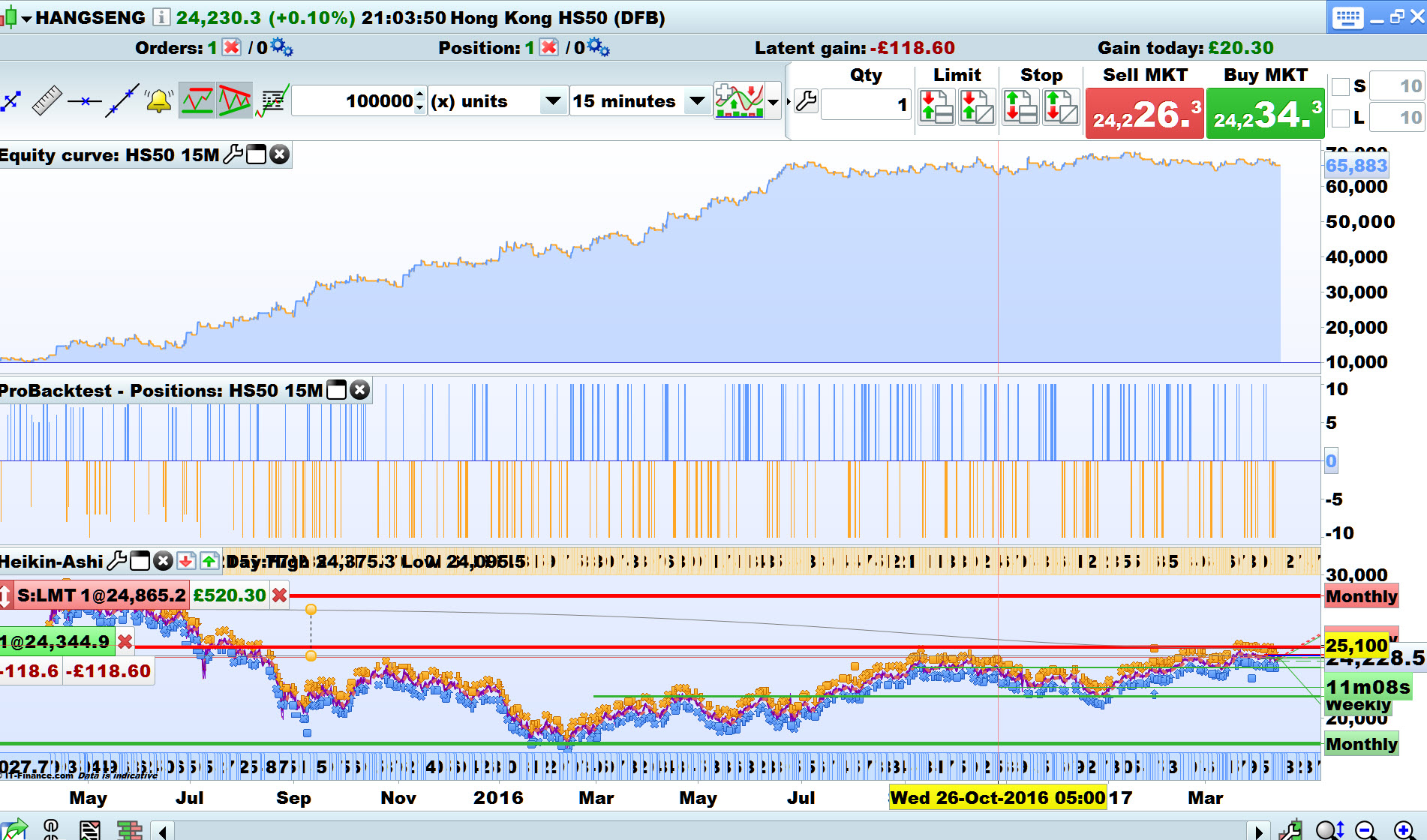

So I changed my Platform to UTC +8 and now it works great, results attached.

When I get the GMT+1 times correct, I’ll post the code on here so others can test and we can compare Trades.

GraHal

Eric

EricParticipant

Master

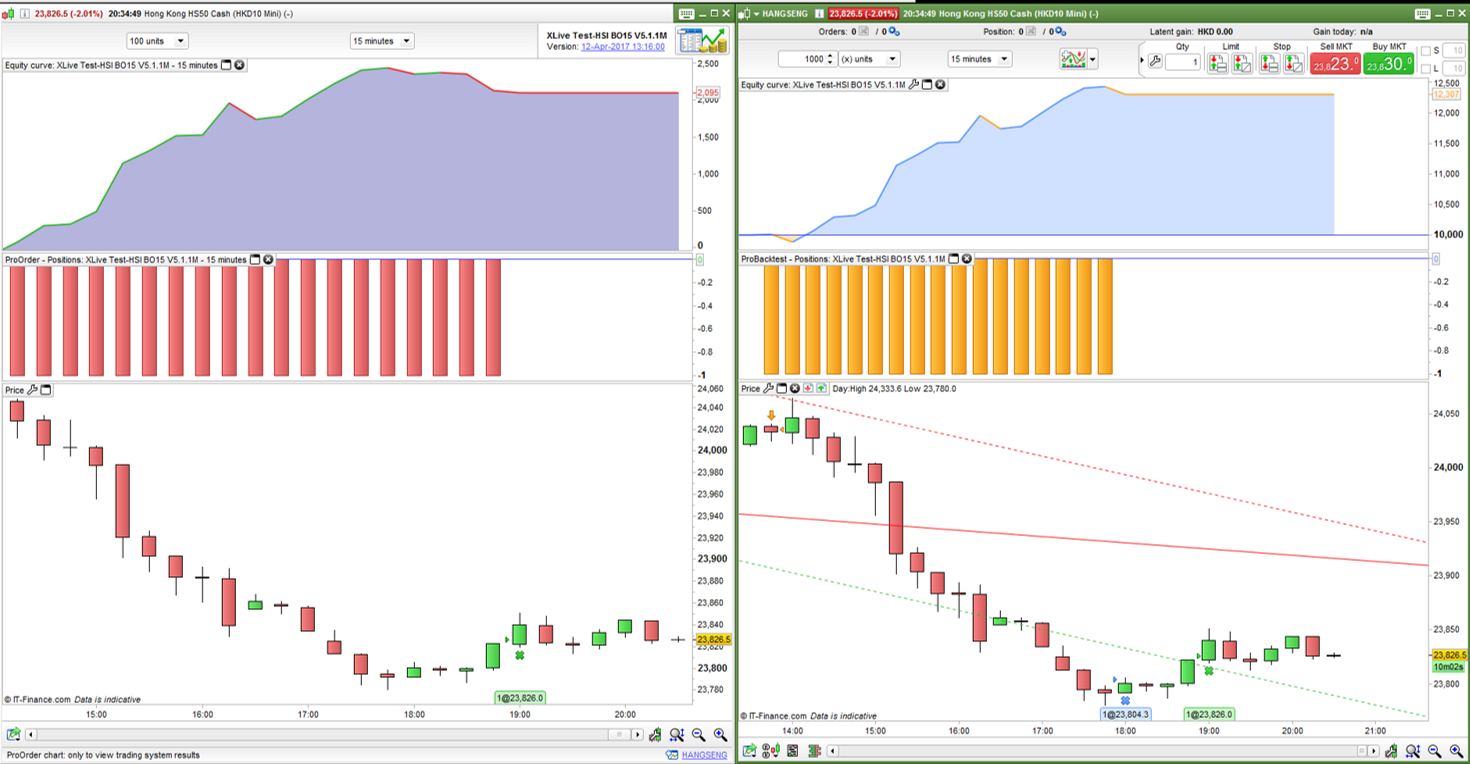

I dont know why this strategy perform different live versus backtest

But generally speaking about this “spread” thing

When dealing with IG CFD/SB you have a midprice (that price we see on the charts and if nothing has changed lately also used in backtesting)

and then you have the spread we can call it bid and ask, if the spread are 12 points and the midprice is 1000 then the bid is 994 and ask 1006

when trading live with stop and limit you can get filled on a stoporder even if the midprice not touch the stop and to get filled on the limitorder the midprice must be 6 points higher then the limit

The problem is if the bid touch the stop and the midprice dont and if midprice touch the limit but not the ask

this problem is bigger with bigger spread (and many trades with small win/loss), if trading dax with 0,5 on each side you probably get filled on every trade

If i am wrong about this please enlighten me

(when using markets order this is not a problem, only stops and limits)

EricParticipant

Master

When thinking about it why not use one version in live and a version with spread added (in the code) in backtesting then the result would be similar?

when dealing with large spread and stop/limit

BCParticipant

Master

Hi Eric

Yes, that’s what I think (Wish I am wrong instead of PRT bugs).

I already start live (no spread built in, with little bit amend) 2 days ago, but no trade trigger due to market situtation.

//Market: Hong Kong HS50 Cash (HKD10 Mini)

//Time Zone: UTC+8:00

//Time Frame: 15 mins

//Please manual stop the system on Hong Kong public hoilday.

//Remark: Offical HSI future night trade start from 2013-04-08, 17:00-23:00, amended on 2014-11-03, 17:15-23:45

// code-parameter

DEFPARAM FlatAfter = 234500 //234500

// window high/low calculation

ONCE StartTime = 90000//91500

ONCE EndTime = 93000//100000

// trading window

ONCE BuyTime = EndTime

ONCE SellTime = 234500 //234500

//Money management

ONCE PositionSize = 1

ONCE Capital = 10000

ONCE Risk = 5

ONCE MaxD = 50 // Quit system if highest close account balance drop over xx%

equity = Capital + StrategyProfit

maxrisk = round(equity*(Risk/100))

//Check system account balance

if equity<QuitLevel then

quit

endif

recordhighest = MAX(recordhighest,equity)

QuitLevel = recordhighest*((100-MaxD)/100)

//MA Filter

FMA=Average[80](close)

SMA=Average[200](close)

// calculate breakout box high/low and sl/tp

IF Time >= StartTime AND Time <= EndTime THEN

IF TIME = StartTime THEN

DailyHigh = High

DailyLow = Low

ENDIF

IF High > DailyHigh THEN

DailyHigh = High

ENDIF

IF Low < DailyLow THEN

DailyLow = Low

ENDIF

sl = min(120,(max(30,((DailyHigh - DailyLow)))))

tp = sl*4

PositionSize = min(10,(max(1,abs(round((maxrisk/sl)/PointValue)*pipsize))))

TradeCounterLong = 0

TradeCounterShort = 0

ENDIF

//Define the best trading day and time and avoid trading at lunch & teakbreak high spread period, please manual stop system on Hong Kong public hoilday.

//Long

LOK1=currentdayofweek=1 and ((time>=091500 and time<120000) or (time>=130000 and time<160000) or (time>=171500 and time<230000))

LOK2=currentdayofweek=2 and ((time>=091500 and time<120000) or (time>=130000 and time<160000) or (time>=171500 and time<230000))

LOK3=currentdayofweek=3 and ((time>=091500 and time<120000) or (time>=130000 and time<160000) or (time>=171500 and time<230000))

LOK5=currentdayofweek=5 and ((time>=130000 and time<160000) or (time>=171500 and time<230000))

//Short

SOK1=currentdayofweek=1 and ((time>=091500 and time<120000) or (time>=130000 and time<160000) or (time>=171500 and time<230000))

SOK2=currentdayofweek=2 and ((time>=130000 and time<160000) or (time>=171500 and time<230000))

SOK4=currentdayofweek=4 and ((time>=091500 and time<120000) or (time>=171500 and time<230000))

SOK5=currentdayofweek=5 and ((time>=091500 and time<120000) or (time>=130000 and time<160000) or (time>=171500 and time<230000))

// Position management

IF Time >= BuyTime AND Time <= SellTime THEN

//Long Entry

IF Not LONGONMARKET and (LOK1 or LOK2 or LOK3 or LOK5) and close>DailyHigh and FMA>SMA and TradeCounterLong=0 THEN

BUY PositionSize CONTRACT AT MARKET

TradeCounterLong = TradeCounterLong + 1

ENDIF

//Short Entry

IF Not SHORTONMARKET and (SOK1 OR SOK2 OR SOK4 OR SOK5) and close<DailyLow and FMA<SMA AND TradeCounterShort=0 THEN

SELLSHORT PositionSize CONTRACT AT MARKET

TradeCounterShort = TradeCounterShort + 1

ENDIF

// trailing stop function

ONCE trailingStepLong = 0.08// in %

ONCE trailingStepShort = 0.08 // in %

trailingStartLongInPoints = max(30,(TP/5))

trailingStartShortInPoints = max(30,(TP/4))

trailingStepLongInPoints = max(10,(tradeprice(1) * trailingStepLong / 100))

trailingStepShortInPoints = max(10,(tradeprice(1) * trailingStepShort / 100))

// reset the stoploss value

IF NOT ONMARKET THEN

newSL = 0

ENDIF

// manage long positions

IF LONGONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND close - tradeprice(1) >= trailingStartLongInPoints * pipsize THEN

newSL = tradeprice(1) + trailingStepLongInPoints * pipsize

ENDIF

// next moves

IF newSL > 0 AND close - newSL >= trailingStepLongInPoints * pipsize THEN

newSL = newSL + trailingStepLongInPoints * pipsize

ENDIF

ENDIF

// manage short positions

IF SHORTONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND tradeprice(1) - close >= trailingStartShortInPoints * pipsize THEN

newSL = tradeprice(1) - trailingStepShortInPoints * pipsize

ENDIF

// next moves

IF newSL > 0 AND newSL - close >= trailingStepShortInPoints * pipsize THEN

newSL = newSL - trailingStepShortInPoints * pipsize

ENDIF

ENDIF

// stop order to exit the positions

IF newSL > 0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

// close positions

IF Time = SellTime THEN

IF LONGONMARKET THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND Time = SellTime THEN

EXITSHORT AT MARKET

ENDIF

ENDIF

// stops and targets

SET STOP pLOSS sl

SET TARGET pPROFIT tp

ENDIF

Hi!

@Grahal, Did you manage to translate it to CET? Ive tried a couple of times to but have the same problem.

Do you know why @Nicolas?

@Henrik ah I thought it was me! No I’ve not done it again since, forgot sorry and been out over Easter holiday.

I had 4 attempts to change all the times (to UTC+1) and was more deliberate and careful each successive time, I even used find & replace and none of my attempts worked / produced good results.

Weird … only thing I can think of is that not all Bins times are UTC +8?

What you reckon @Bin … is every time used in your code set to UTC + 8 please?

Thanks

GraHal

I tried also to change the code for +1GMT, even change all Asian market to +8GMT but nothing worked.

cheers Kasper

Worked good for me if I changed my whole Platform time to UTC +8 (see my results here #31949).

This is very odd, we need to find the reason?

I know it sounds daft, but please Bin say what time it is where you are and post the time on a message here. Whoever sees your post as soon as you post it then check what your clock is showing and post here?

GraHal

BCParticipant

Master

Hi Grahal

Yes, I think change whole platform time to UTC+8:00 before backtest or start live is the only choice. Just like Reiner Hang Seng PF, I try to many many setting to fit for UTC+8:00 but failed. Finally I change whole platform time to UTC+1:00 and then start the system. (May be the issue of summer and winter time? )

Hi Bin and Grahal!

I need CET time for my other strategies, so i need to figure something out here.

@BIN are you shore you have +8 setting on hs chart?

I ran original code with CET times and got a simular result but not the same, See lower test on picture on erlier post.

Regards

Henrik

BCParticipant

Master

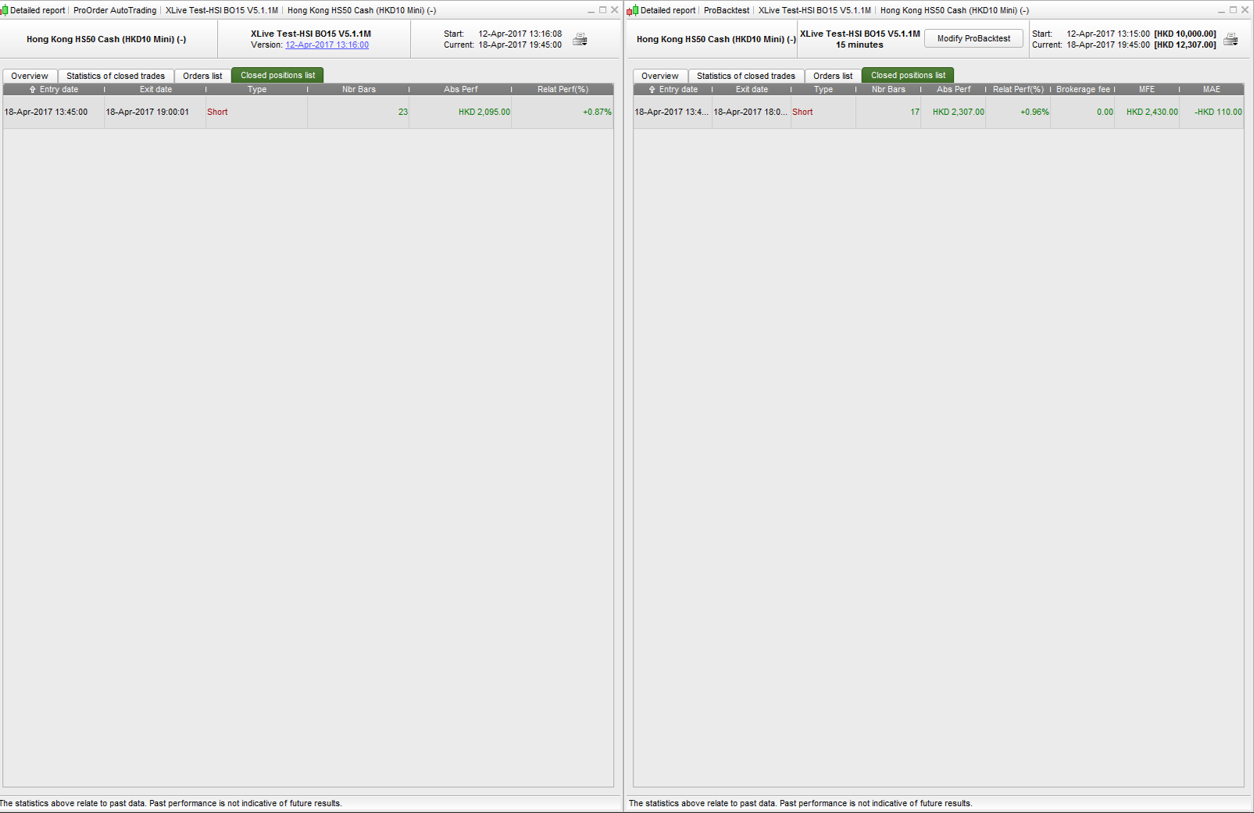

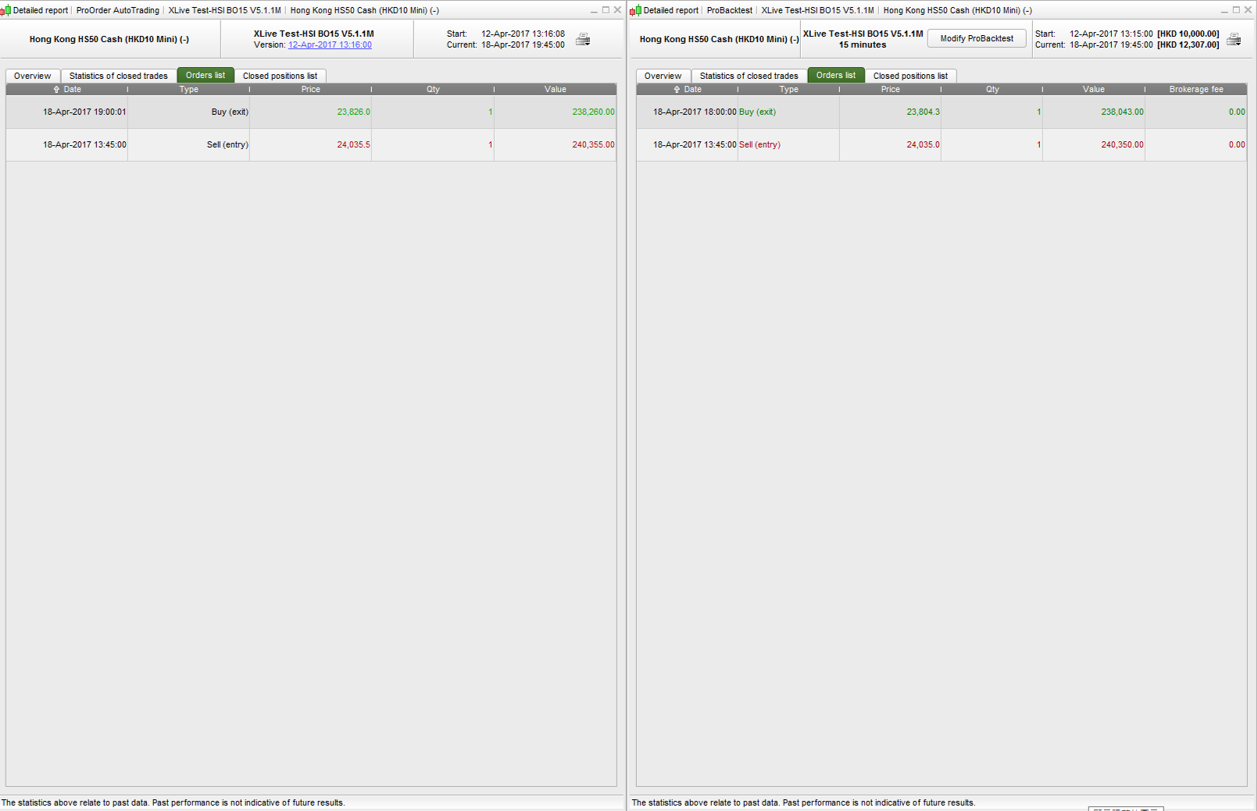

No luck, live and back test result still different on no [spread] version.

Live exit on 19:00 but back test exit on 18:00.

@Bin when next you post, please type on this Page the time that the clock on your computer is shwoing when you press Submit below.

Thank You

GraHal