BC

BCParticipant

Master

I found this strategy via below link and use my limited knowledge translate to PRT robot, please kindly try, comment and feel free modify to fit for your need.

http://www.tradingstrategyguides.com/big-three-trading-str

// Big Three Trading Strategy

// Original Idea from: http://www.tradingstrategyguides.com/big-three-trading-strategy/

// Market: DAX 30

// Time Frame: 1 Hour

// Time Zone: Any

// Spread: 2.9

// Version : V 2.0

defparam preloadbars = 3000

defparam cumulateorders =false //true //false

//// Core Indicator Parameter Setting ////

// Moving Average Setting (Original: 20, 40, 80)

Fast = 20 //

Medium = 40 //

Slow = 80 //

// Look Back Bar (Original: N/A)

CP = 3 // 1-20

//// Optional Function Switch ( 1 = Enable 0 = Disable ) ////

FixedMinMaxStopLoss = 1

TargetProfit = 1

TimeExit = 1

MFETrailing = 1

MoneyManagement = 0

//// Optional Function and Parameter Setting ////

// 1) Fixed Min Max Stop Loss Setting

If FixedMinMaxStopLoss = 1 then

//Long

MaxLong = 80 // 40-100 (90) 80

MinLong = 30 // 5-30 (30) 30

//Short

MaxShort = 60 // 40-100 (50) 60

MinShort = 5 // 5-30 (10) 5

Endif

// 2) Take Profit Setting

If TargetProfit = 1 then

//Long

TakeProfitLongRate = 2.5 // 1-5

//Short

TakeProfitShortRate = 2.5 // 1-5

Endif

// 3) Time Exit Setting

If TimeExit = 1 then

//Long

ONCE maxCandlesLongWithProfit = 78 // 12-120 (72)

ONCE maxCandlesLongWithoutProfit = 66 // 12-72 (72)

//Short

ONCE maxCandlesShortWithProfit = 60 // 12-96 (60)

ONCE maxCandlesShortWithoutProfit = 54 // 12-48 (48)

Endif

// 4) MFE Step Setting

If MFETrailing = 1 then

//Long

MFELongStep = 1.5 // 2-12 2

//Short

MFEShortStep = 1 // 2-12 9

Endif

// 5) Money Management

If MoneyManagement = 1 then

LongRisk = 5 //% 1-5

ShortRisk = 3 //% 1-5

CloseBalanceMaxDrop = 50 //% 30-60

Capital = 2000 //$

Equity = Capital + StrategyProfit

LongMaxRisk = Round(Equity*LongRisk/100)

ShortMaxRisk = Round(Equity*ShortRisk/100)

//Max Contract

MaxLongContract = 500 // 50-100 (1000)

MaxShortContract = 100 // 10-50 (200)

//Check system account balance

If equity<QuickLevel then

Quit

Endif

RecordHighest = MAX(RecordHighest,Equity)

QuickLevel = RecordHighest*((100-CloseBalanceMaxDrop)/100)

Endif

// Core indicator

//Big Three MA

FMA = Average[Fast](close) //green coloured(0,255,0)

MMA = Average[Medium](close)//blue coloured(0,0,255)

SMA = Average[Slow](close)//red coloured(255,0,0)

// Entry Rules

//Buy Signal

B1 = low > SMA and low>MMA and low>FMA

B2 = high >= highest[CP](high)

BC = B1 and B2

//Buy Candle

BC1 = Close[1] < Close[2]

BC2 = Close > Close[1]

BC3 = Close > Open

BCandle = BC1 and BC2 and BC3

//Sell Signal

S1 = high < FMA and high<MMA and high<SMA

S2 = low <= lowest[CP](low)

SC = S1 and S2

//Sell Caandle

SC1 = Close[1] > Close[2]

SC2 = Close < Close[1]

SC3 = Close < Open

SCandle = SC1 and SC2 and SC3

// Exit Rules

LongExit = Close crosses under SMA

ShortExit = Close crosses over SMA

//Long Entry

If BC and BCandle then

BuyPrice = Close

If FixedMinMaxStopLoss = 1 then

StopLossLong = MIN(MaxLong,MAX(MinLong,(BuyPrice - SMA)))

Else

StopLossLong = BuyPrice - SMA

Endif

If TargetProfit = 1 then

TakeProfitLong = StopLossLong * TakeProfitLongRate

TakeProfit = TakeProfitLong

Endif

If MoneyManagement = 1 then

PositionSizeLong = min(MaxLongContract,(max(1,abs(round((LongMaxRisk/StopLossLong)/PointValue)*pipsize))))

BUY PositionSizeLong CONTRACT AT MARKET

Else

BUY 1 CONTRACT AT MARKET

Endif

Endif

//Long Exit

If LongonMarket and LongExit then

sell at market

Endif

//short entry

If SC and SCandle then

SellPrice = Close

If FixedMinMaxStopLoss = 1 then

StopLossShort = MIN(MaxShort,MAX(MinShort,(SMA - SellPrice)))

Else

StopLossShort = SMA - SellPrice

Endif

If TargetProfit = 1 then

TakeProfitShort = StopLossShort * TakeProfitShortRate

TakeProfit = TakeProfitShort

Endif

If MoneyManagement = 1 then

PositionSizeShort = min(MaxShortContract,(max(1,abs(round((ShortMaxRisk/StopLossShort)/PointValue)*pipsize))))

SELLSHORT PositionSizeShort CONTRACT AT MARKET

Else

SELLSHORT 1 CONTRACT AT MARKET

Endif

Endif

//Short Exit

If ShortonMarket and ShortExit then

exitshort at market

Endif

// Time Exit

If TimeExit = 1 then

If LongonMarket then

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

elsif ShortonMarket then

posProfit = (((positionprice - close) * pointvalue) * countofposition) / pipsize

Endif

m1 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithoutProfit

// take profit after max candles

IF LONGONMARKET AND (m1 OR m3) THEN

sell at market

endif

IF SHORTONMARKET AND (m2 OR m4) THEN

exitshort at market

endif

Endif

//MFE Trailing stop

If MFETrailing = 1 then

MFELong = (TakeProfitLong/MFELongStep)

MFEShort = (TakeProfitShort/MFEShortStep)

If not onmarket then

MAXPRICE = 0

MINPRICE = close

priceexit = 0

Endif

If longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

If MAXPRICE-tradeprice(1)>=MFELong*pointsize then

priceexit = MAXPRICE-MFELong*pointsize

Endif

Endif

If shortonmarket then

MINPRICE = MIN(MINPRICE,close)

If tradeprice(1)-MINPRICE>=MFEShort*pointsize then

priceexit = MINPRICE+MFEShort*pointsize

Endif

Endif

If onmarket and priceexit>0 then

EXITSHORT AT priceexit STOP

SELL AT priceexit STOP

Endif

Endif

// Stop Loss

if LongonMarket then

SET STOP LOSS StopLossLong

endif

if ShortonMarket then

SET STOP LOSS StopLossShort

endif

// Target Profit

If TargetProfit = 1 then

SET TARGET PROFIT TakeProfit

Endif

//graph BuyPrice

//graph SellPrice

//graph StopLossLong

//graph StopLossShort

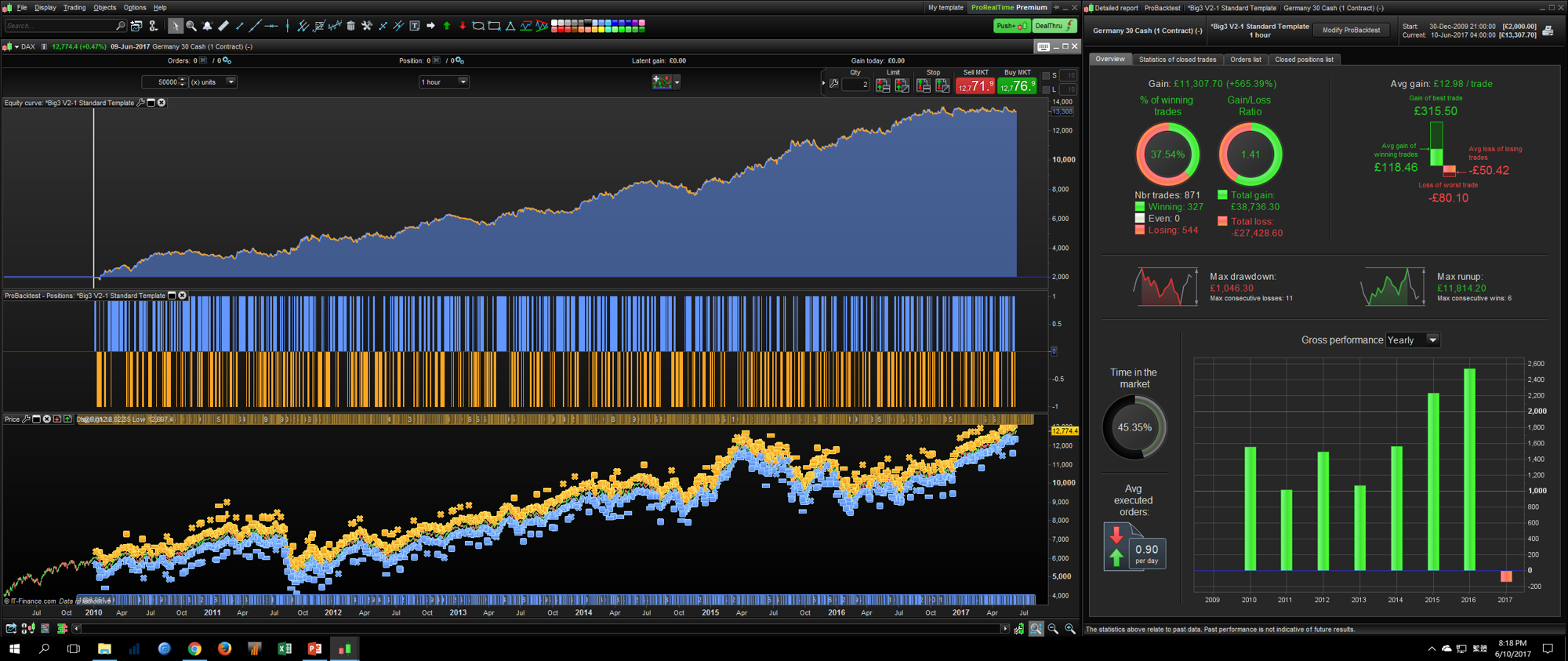

interesting strategy but seems pretty flat the last months? Hows your trading been with this? running in demo/live?

BCParticipant

Master

No, I don’t trade with this robot.

Aw okay, well, it seems pretty flat for now. But it has been relatively stable up until this point, so might as well add to demo and see where it goes 🙂

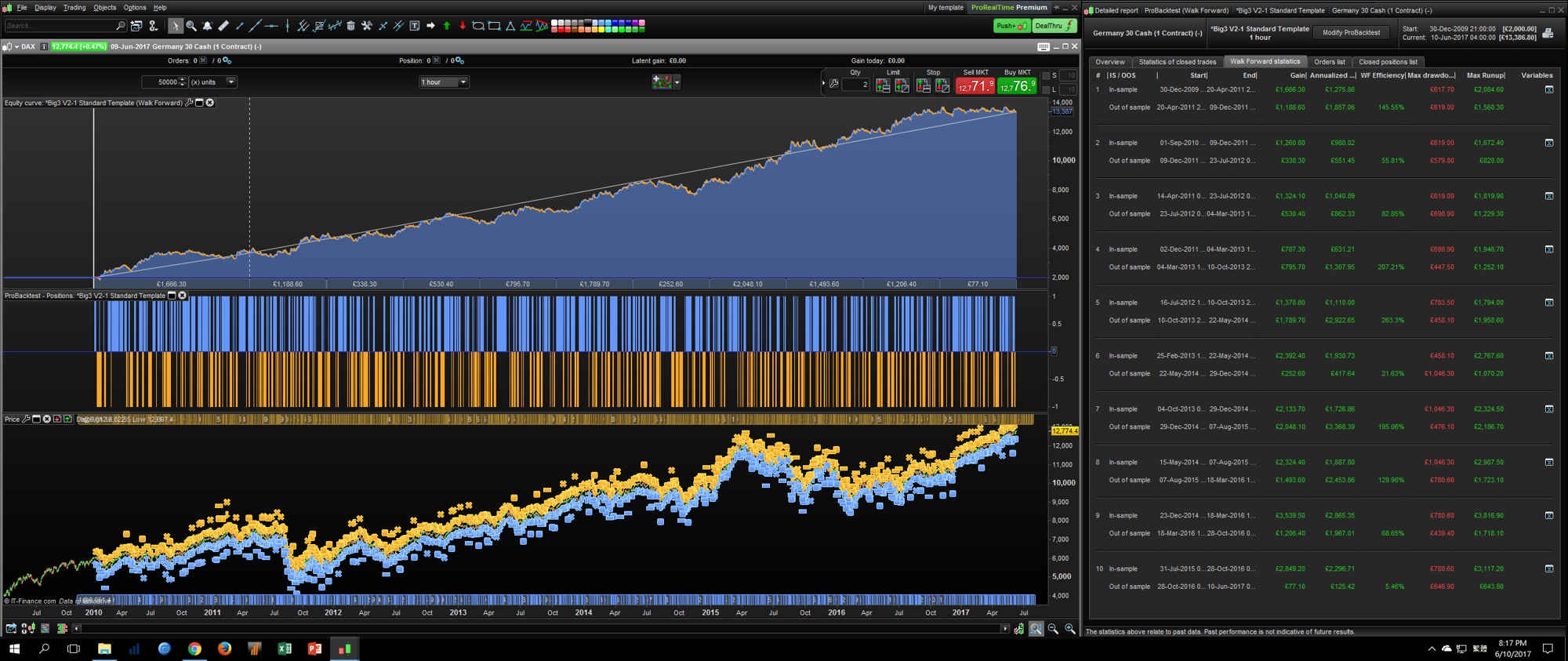

Thank you Bin, nice one. In order to get the complete view of it, what are the variables optimized? Did you try WFA on any other instrument?

This one could probably be a part of the library, can I post it there for you?

BCParticipant

Master

Mainly on CP and test with DAX, I try HS but no good result.

It’s my pleasure to post at library. THX.

Thank you Bin for the strategy. I like the neat and modular approach to your coding and hope you don’t mind me cutting and pasting so that I may use some of it in future ideas of my own!

As for being flat for the last few months…. it is a trend following strategy and markets haven’t really known which way to go recently with all the political turmoil so it is not really surprising to me that a trend reliant strategy has gone a bit flat.

Great work – thanks.

BCParticipant

Master

Hi Nicolas

Please kindly post this latest version to library with detailed remark which variables were optimized and their unit. THX.

// Big Three Trading Strategy

// Original Idea from: http://www.tradingstrategyguides.com/big-three-trading-strategy/

// Market: DAX 30

// Time Frame: 1 Hour

// Time Zone: Any

// Spread: 2.9

// Version : 2.8

// Revised on 2017-11-14

Defparam preloadbars = 3000

Defparam cumulateorders =false //true //false

//// Optional Function Switch ( 1 = Enable 0 = Disable ) ////

FixedMinMaxStopLoss = 1 // Optional Function 1

TargetProfit = 1 // Optional Function 2

TimeExit = 1 // Optional Function 3

MFETrailing = 1 // Optional Function 4

MoneyManagement = 0 // Optional Function 5

//// Core Indicator Parameter Setting ////

// Moving Average Setting (Original: 20, 40, 80)

Fast = 20 // Not Optimize

Medium = 40 // Not Optimize

Slow = 80 // Not Optimize

// Look Back Bar (Original: N/A)

CP = 3 // Variables Optimized

//// Optional Function ////

// 1) Fixed Min Max Stop Loss Setting

If FixedMinMaxStopLoss then

//Long

MaxLong = 80 // by points, Variables Optimized

MinLong = 30 // by points, Variables Optimized

//Short

MaxShort = 60 // by points, Variables Optimized

MinShort = 5 // by points, Variables Optimized

Endif

// 2) Take Profit Setting

If TargetProfit then

//Long

TakeProfitLongRate = 2.6 // by %, Variables Optimized

//Short

TakeProfitShortRate = 2.5 // by %, Variables Optimized

Endif

// 3) Time Exit Setting

If TimeExit then

//Long

ONCE maxCandlesLongWithProfit = 78 // by bar, Variables Optimized

ONCE maxCandlesLongWithoutProfit = 66 // by bar, Variables Optimized

//Short

ONCE maxCandlesShortWithProfit = 60 // by bar, Variables Optimized

ONCE maxCandlesShortWithoutProfit = 54 // by bar, Variables Optimized

Endif

// 4) MFE Step Setting

If MFETrailing then

//Long

MFELongStep = 1.5 // by %, Variables Optimized

//Short

MFEShortStep = 1 // by %, Variables Optimized

Endif

// 5) Money Management

If MoneyManagement then

LongRisk = 5 // by %, Variables Optimized

ShortRisk = 3 // by %, Variables Optimized

CloseBalanceMaxDrop = 50 // by %, Personal preference

Capital = 3000 // by $

Equity = Capital + StrategyProfit

LongMaxRisk = Round(Equity*LongRisk/100)

ShortMaxRisk = Round(Equity*ShortRisk/100)

//Max Contract

MaxLongContract = 500 // by contract, Variables Optimized

MaxShortContract = 100 // by contract, Variables Optimized

//Check system account balance

If equity<QuitLevel then

Quit

Endif

RecordHighest = MAX(RecordHighest,Equity)

QuitLevel = RecordHighest*((100-CloseBalanceMaxDrop)/100)

Endif

// Core indicator

//Big Three MA

FMA = Average[Fast](close) //green coloured(0,255,0)

MMA = Average[Medium](close) //blue coloured(0,0,255)

SMA = Average[Slow](close) //red coloured(255,0,0)

// Entry Rules

//Buy Signal

B1 = low > SMA and low>MMA and low>FMA

B2 = high >= highest[CP](high)

BC = B1 and B2

//Buy Candle

BC1 = Close[1] < Close[2]

BC2 = Close > Close[1]

BC3 = Close > Open

BCandle = BC1 and BC2 and BC3

//Sell Signal

S1 = high < FMA and high<MMA and high<SMA

S2 = low <= lowest[CP](low)

SC = S1 and S2

//Sell Candle

SC1 = Close[1] > Close[2]

SC2 = Close < Close[1]

SC3 = Close < Open

SCandle = SC1 and SC2 and SC3

// Exit Rules

LongExit = Close crosses under SMA

ShortExit = Close crosses over SMA

//Long Entry

If Not LongonMarket and BC and BCandle then

BuyPrice = Close

If FixedMinMaxStopLoss then

StopLossLong = MIN(MaxLong,MAX(MinLong,(BuyPrice - SMA)))

Else

StopLossLong = BuyPrice - SMA

Endif

If TargetProfit then

TakeProfitLong = StopLossLong * TakeProfitLongRate

TP = TakeProfitLong

Endif

SL = StopLossLong

If MoneyManagement then

PositionSizeLong = min(MaxLongContract,(max(2,abs(round((LongMaxRisk/StopLossLong)/PointValue)*pipsize))))

BUY PositionSizeLong CONTRACT AT MARKET

Else

BUY 2 CONTRACT AT MARKET

Endif

Endif

//Long Exit

If LongonMarket and LongExit then

sell at market

Endif

//short entry

If Not ShortonMarket and SC and SCandle then

SellPrice = Close

If FixedMinMaxStopLoss then

StopLossShort = MIN(MaxShort,MAX(MinShort,(SMA - SellPrice)))

Else

StopLossShort = SMA - SellPrice

Endif

If TargetProfit then

TakeProfitShort = StopLossShort * TakeProfitShortRate

TP = TakeProfitShort

Endif

SL = StopLossShort

If MoneyManagement then

PositionSizeShort = min(MaxShortContract,(max(2,abs(round((ShortMaxRisk/StopLossShort)/PointValue)*pipsize))))

SELLSHORT PositionSizeShort CONTRACT AT MARKET

Else

SELLSHORT 2 CONTRACT AT MARKET

Endif

Endif

//Short Exit

If ShortonMarket and ShortExit then

exitshort at market

Endif

// Time Exit

If TimeExit then

If LongonMarket then

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

elsif ShortonMarket then

posProfit = (((positionprice - close) * pointvalue) * countofposition) / pipsize

Endif

m1 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithoutProfit

// take profit after max candles

IF LONGONMARKET AND (m1 OR m3) THEN

sell at market

endif

IF SHORTONMARKET AND (m2 OR m4) THEN

exitshort at market

endif

Endif

//MFE Trailing stop

If MFETrailing then

MFELong = (TakeProfitLong/MFELongStep)

MFEShort = (TakeProfitShort/MFEShortStep)

If not onmarket then

MAXPRICE = 0

MINPRICE = close

priceexit = 0

Endif

If longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

If MAXPRICE-tradeprice(1)>=MFELong*pointsize then

priceexit = MAXPRICE-MFELong*pointsize

Endif

Endif

If shortonmarket then

MINPRICE = MIN(MINPRICE,close)

If tradeprice(1)-MINPRICE>=MFEShort*pointsize then

priceexit = MINPRICE+MFEShort*pointsize

Endif

Endif

If onmarket and priceexit>0 then

EXITSHORT AT priceexit STOP

SELL AT priceexit STOP

Endif

Endif

// Stop Loss a

SET STOP LOSS SL

// Target Profit

If TargetProfit then

SET TARGET PROFIT TP

Endif

//graph BuyPrice

//graph SellPrice

//graph StopLossLong

//graph StopLossShort

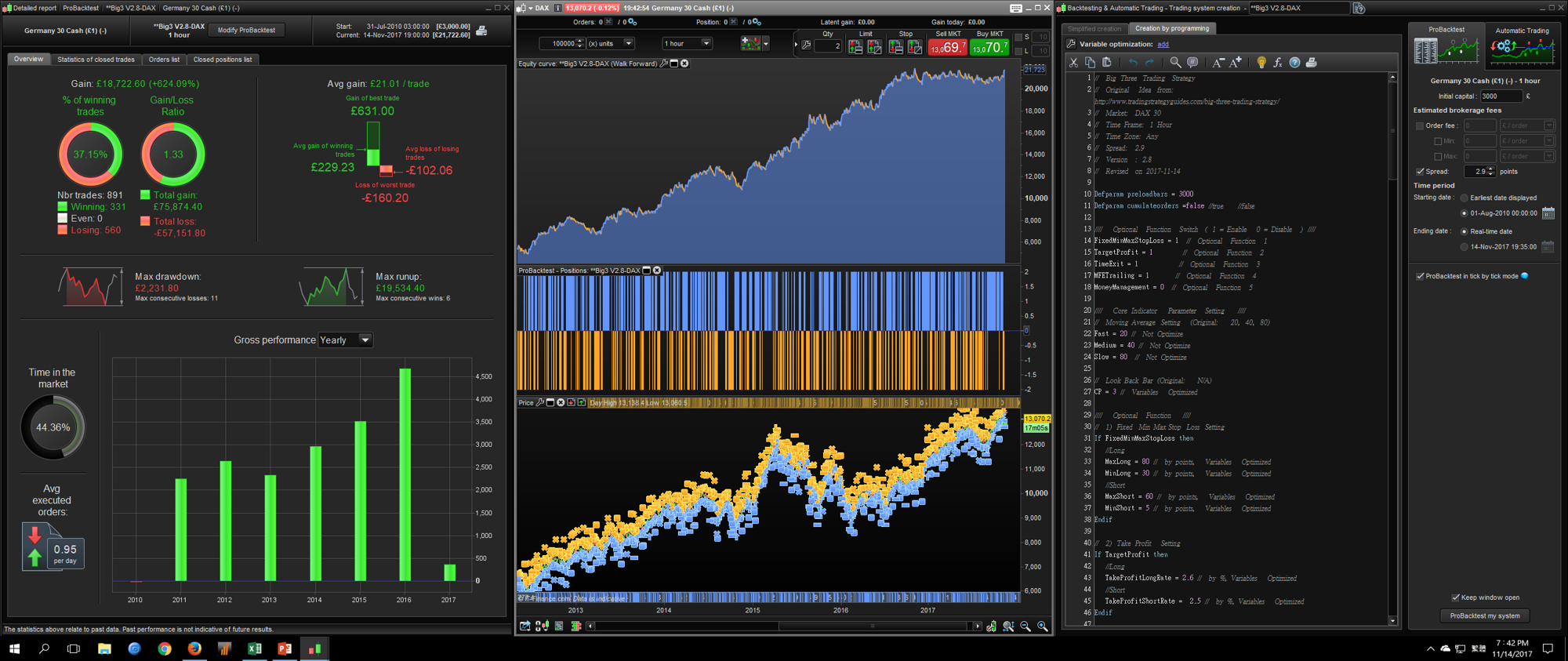

I downloaded the itf of v2 and notice that tick by tick data is not selected. Results are terrible once tick by tick data is used!

BCParticipant

Master

Hi Vonasi

Tick by tick back test screen shot attached. I don’t suggest play this robot with real money, just for study purpose. THX.