Hello,

I am working in a system based in divergences, it can be used with several indicators (RSI, MACD…), markets and timeframes. Its numbers are not spectacular but it looks quite reliable to me. Anyway, still proving it in demo and I will post it here in the future . But what I want to to talk about here is that I noticed in backtesting is that this system and others, even with a long wining system, is quite common to start the firsts months/weeks/days loosing money. Does it happen to you also? Why you think is that?

Hi TF

Yes … start the firsts months/weeks/days loosing money … does seem to happen to me also, but I think it may ‘stick in one’s mind’ due seeing an overall healthy gain in Backtest and then being disappointed that a System shows an instant loss? 🙂

I guess the ‘acid test’ is … is the System exceeding its parameters observed in BT … in particular Drawdown? But of course many of don’t / didn’t even get the DD figure populated in BT to compare to Live!? (Delete java cache fixed the no show DD figure for me yesterday anyway!) .

Just a few thoughts anyway

GraHal

Thanks GraHal for your response,

I had a similar idea. Even the best system only have the wining ratio to prevail for sure in the long run, so at the begining is more or less a flipcoin. But even having in mind that it looks to me too usual the bad beginnings, but maybe it´s just a problem of false expectations as you suggest. Have you noticed the same effect in real?

Yes I have noticed the same effect in real / Live and it scares me so I’ve gone back to manual trading! 🙂

If I look at a System Live trading and it takes a position and I think, for example … “I’d never go Long there” … and the System then loses, naturally I think … told you so! :). So then I stop the System!

I guess I need a System that trades as I manual trade, but I’m not a ‘skilful coder’ and so can’t do. Having spent over 18 months trying to get a good System (Demo tested close to 1,000 Systems!) I feel like I am giving up!

One of the main reasons that I am demoralised is the useless ‘System Trade Test Window ‘… it’s not possible to sort results by Highest Gain, Lowest Drawdown etc etc etc … so how is one expected to decide analytically which System to go forward with in Live Trading??

Yes you can click on each individual System and make notes / take screen shots of Gain and DD etc etc … but who wants to do all that faffing admin stuff … I wanna make money! haha

You’ve got me started now … I have commented vociferously on above on this site, but as usual we are kept in the dark (by PRT Platform provider) as to when / if anything is due to improve re above issues.

GraHal

I can understand your frustration. What´s the max time you have tried any system in live? Al least by backtesting results, e.g. bad beginings, looks like a question of trust, constancy and deep pockets. My idea is that, no matter how promising the backtesting is, there is too much risk only with a system. But maybe diversifying with several systems, or markets, timeframes… I can lower the risk, or maybe just loose more. What do you think?

Ha … we think similar … I tried the ‘numbers game’ in Demo … got 76 systems running, I was aiming for 100 then IG throttled back to a max of 50 so I then got 50 going on SB and 50 on CFD. Also my wife has an account so same on hers … so that’s 200 Systems running in all! :). My logic was that I hope it was going to be swings and roundabouts / law of averages … but it wasn’t! 😉

Some Systems were straight copy off here, some off here and tweaked by me, some my own work, many the same System, but optimised for different markets covering Forex, Index and Commodities … NOTHING WORKED CONSISTENTLY! hahahhaha

The I tried a more ‘Quality Approach’ and selected the best (by Gain and DD etc) out of the near 1,000 Systems I have tried over 18 months … better but still a consistent reduction in equity although slower than the ‘numbers game’.

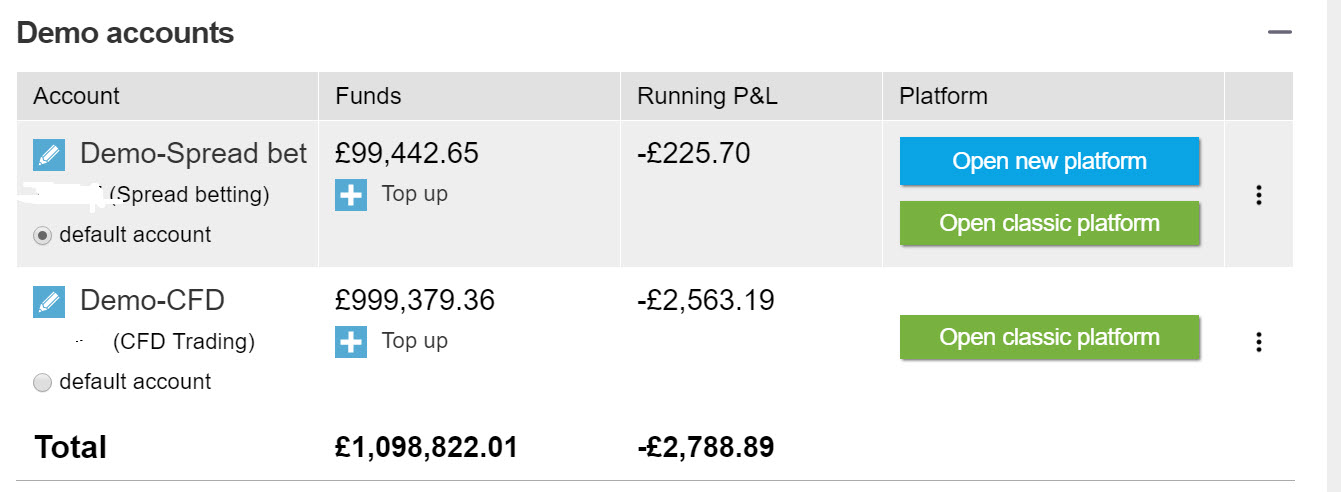

Latest is that about 10 days ago I stopped all the Systems that showed a Loss > £100. Each time I have a new initiative I make my Demo Accounts up a round figure … 10,000 , 100,000 etc so I can easily see if Losing or gaining from thereon. I’ll check later and report back.

Not good is it??

I manual trade higher highs, lower lows, Elliott Waves and Fib retracements in the main, but there is precious little on here re Systems following such strategies? If anybody can point me to any that work please let me know?

Re Max time Live / Real Trade for a System … around 2 weeks! Yes I know, I don’t give them enough time … but hey I want to sleep at night!

When you consider I mainly trade the 1 Minute TF with Entries and Exits made on the 6 second TF then 2 weeks is a lifetime!!! hahahahah

GraHal

PS Just had a great Short run on the DAX and have now made back losses on the last few Systems I ran Live!

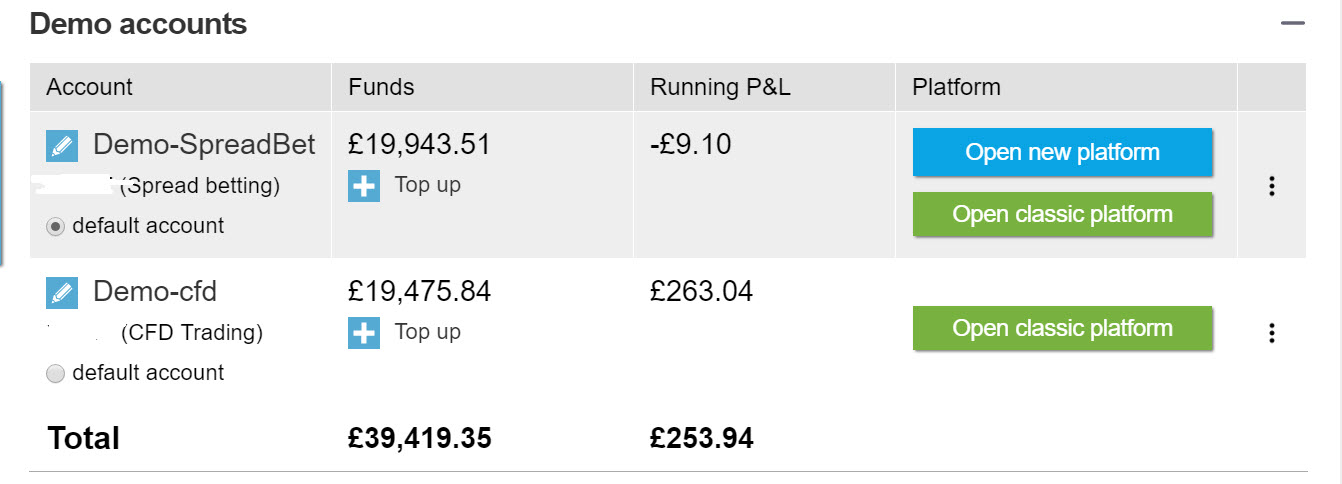

Further to above re ‘Best of Best’ System I’ve Demo Traded in the last 2 weeks… see attached.

190 ish Systems had been running in Demo for between 2 months and 6 months. I then stopped all Systems making Loss > £100 and ended up with just Profit makers and small Loss makers < £100 (about 4 or 5) … this called ‘Best of Best’ but maybe it should be ‘Best of the Worst’?? 🙁

I then rounded up my equity balance (to 10k, 100k etc) .. attached are the results since 6 Mar 17.

GraHal

Very funy and helpfull messages, thanks GraHal for sharing your experience…. My name is TempusFugit and I am a tradercolic loser Jajaja

Seriously, I had the same idea but the key is in the detail. I mean that most of the systems in this web or wherever are loosers, if you just gather a lot of them more or less ramdomly, most of them will be loosers and you will loose the more you use. You only need a few or even one versatil system, than can be use in different similar markets (forex, index…) or different setups or different timeframes. I consider only one system too uncertain, no mather how good is it, but with diferent setups/markets/timefrimes probably the uncertain is diluted more. I am working on one system that I consider very versatil just with this idea, to use it in different markets/setups/timeframes. If the system is right I consider the risk lower.

By the way, your recent win in short-DAX was with 4h-Pathfinder? I am using it in Demo also, it´s the only system in this web that I have found consistent so far.

No my DAX short win today was me manual trading, but yes I agree the 4H Pathfinder Systems are good.

You may be interested in this Pathfinder Trades Log that I host on my Google drive …

https://docs.google.com/spreadsheets/d/1BkjhSK32r1MD0eMnWSHG3cJH7hETYIEl5mXtee2WMjE/edit?usp=sharing

I look forward to seeing your ‘Divergence System’ if you ever want to share on here.

Regards

GraHal

Interesting thread guys. Just my two cents: believe in diversification, portfolios and risk management, have a deeper look at correlation between strategies and instruments, that’s where is the key of “success”, or rather should I say the path that will take you on the very thin line between the very good and the very bad. I’m used to say that automatic trading is 100 times more difficult than manual trading.. sad but true 🙂

automatic trading is 100 times more difficult than manual trading … Wow and that’s the Master saying it … he who can code anything! What chance have us young grasshoppers got! 🙂

But we just may get there with help from O Wise One!

Thank You for this Site and Your continuing Help Nicolas

GraHal

I should have said “automatic trading needs 100 times more work than manual trading”.. but that’s almost the same 🙂

Nicolas’s point about correlation is spot on and cannot be emphasised enough. It is absolutely crucial that we can understand that diversification only works – until it doesn’t. This was the single biggest factor in the cause of the financial crisis, in that firms did not fully appreciate the correlation between markets and at the same time the historic correlation models all broke down making the whole situation even worse. I can verify this from experience having lived through it 🙂

At present I try and download into Excel the returns of the strategies and work out the overlaps and correlations of the overall portfolio. It’s painful because the data is all in text format with currency signs etc etc so I have to reformat into numbers first. I wish that PRT would format the fields as numbers, it would be sooooo much easier 🙂 Actually, that reminds me, I will add this to the suggestion thread.

GraHal,

Thanks for the link to the Pathfinder Log. I will contribute with my demo operations. Actually, it seems to work but not sure how, I just know it´s about breaks and seasonality, isn´t it? I think breaks it´s just to easy, many systems work with that… and fail. Do you think is seasonality the key? Because it wouldn´t make me very confident about it. For me seasonality it´s just a better overoptimization. What do you think Oz Wizard (Nicolas)?

And yes, the sentence “automatic trading is 100 times more difficult than manual trading” is really scary, Oz. And what do you mean with ” correlation between strategies and instruments”? To use different strategies with different instruments?

Strategies that reason about seasonality are a full-fledged school in the trading world, such as trend follwing, mean reversion, pair trading, … For Pathfinder, seasonality is only salt and pepper influencing its money management (sorry if I’m wrong ..?).

Basically high correlation between instruments means that they move in the same way, such as many world index for instance, so it’s not a good idea to trade the same way 2 high correlated instruments, because when you loose on one of them, you loose also on the over one. And it’s the same about strategies equity curves.. 2 trend following systems that work the same way: gain and loss during the same period.. are also correlated, so your risk is not well diversified.