CA

CAParticipant

New

Hello!

I have been working on a new strategy for catching trends and I have come up with a code. What I have been doing is optimizing the code for having a specific set of parameters for each currency pair.

So far in the BT I have gotten good results with some pairs E.G. AUD/JPY.

After I get the best variables for the pair I improve the strategy with an optimzed trainling stop.

I will just leave the code here for the AUD/JPY example. Please just let me know what you think:

SHORT = 10

LONG = 38

PERIODOADX = 16

PERIODOSDECRUCE =20

PERIODODECRUCE2 = 50

// Longs

Condition1 = ADX[PERIODOADX] CROSSES OVER PERIODOSDECRUCE

Condition2 = ExponentialAverage[SHORT](Close) > ExponentialAverage[LONG](Close) AND LOW[1] > ExponentialAverage[SHORT](Close)

Condition3 = ExponentialAverage[SHORT](Close) < ExponentialAverage[LONG](Close) AND HIGH[1] < ExponentialAverage[SHORT](Close)

IF NOT LongOnMarket AND Condition1 AND Condition2 THEN

BUY 1 CONTRACTS AT MARKET

ENDIF

// Exit longs

If LongOnMarket AND ADX[PERIODOADX] >= PERIODODECRUCE2 then

allowtrailing = 1

else

allowtrailing = 0

endif

if allowtrailing then

SET STOP pTRAILING TRAILINGn

endif

If LongOnMarket AND (ExponentialAverage[SHORT](Close) CROSSES UNDER ExponentialAverage[LONG](Close)OR ADX[PERIODOADX] < PERIODOSDECRUCE) THEN

SELL AT MARKET

ENDIF

// Shorts

IF NOT ShortOnMarket AND Condition1 AND Condition3 THEN

SELLSHORT 1 CONTRACTS AT MARKET

ENDIF

// Exit shorts

IF ShortOnMarket AND ADX[PERIODOADX] >= PERIODODECRUCE2 then

allowtrailing = 1

else

allowtrailing = 0

endif

if allowtrailing then

SET STOP pTRAILING TRAILINGn

endif

IF ShortOnMarket AND (ExponentialAverage[SHORT](Close) CROSSES OVER ExponentialAverage[LONG](Close) OR ADX[PERIODOADX] < PERIODOSDECRUCE) THEN

EXITSHORT AT MARKET

ENDIF

SET STOP LOSS 150// Stops

What Timeframe is above code optimised for please?

What value are you using for TRAILINGn ?

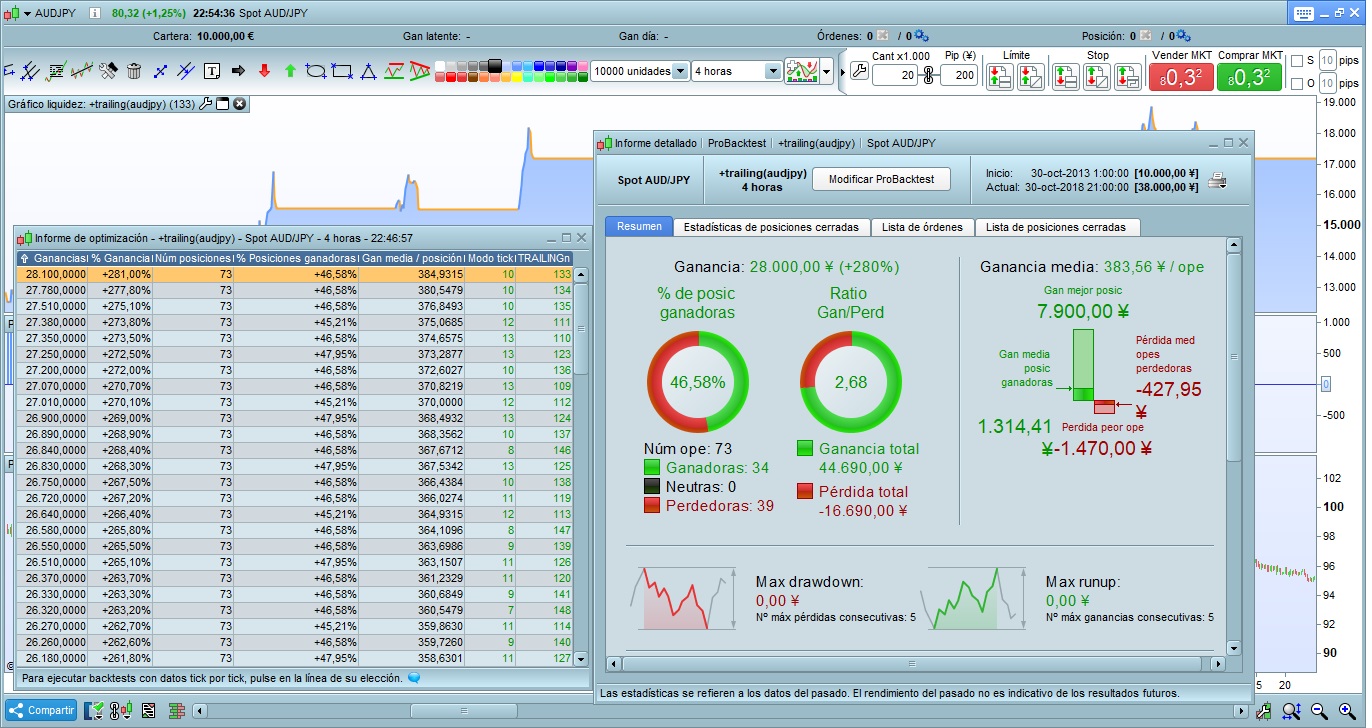

Please can you post your equity curve and Performance results?

I’ve optimised TRAILINGn on every TF from 1 Min to 1 Day (on AUD/JPY).

CAParticipant

New

Oh right! Sorry misses that “detail” . Only for 4H. It attempt to be a swing system.

CAParticipant

New

And for the rest of the questions I am replying from my phone so when I get to my pc I’ll pos the rest

CAParticipant

New

So here is what you asked for GraHal.

I used 4H time frame. 10000 units for optimization of the initial code (without the trailing stop – if you want I can post it too) and for the optimization of the trailing stop.

Something odd here? Attached is what I get! 🙂

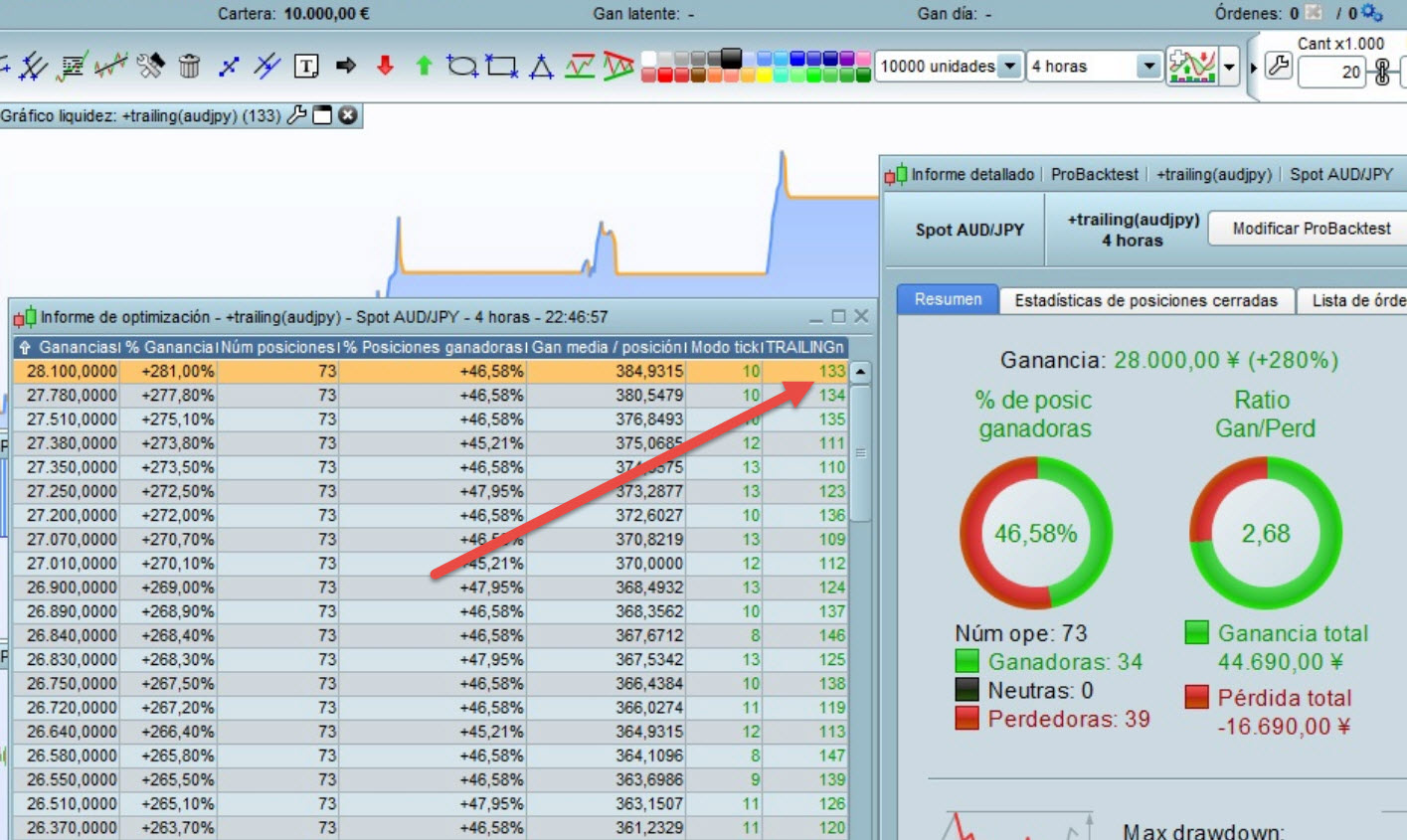

Am I reading that correct … you are buying 1,000 Contracts on AUDJPY??

I’ll have to collect my thoughts as I see you show performance results for Spot AUD/JPY??

Anybody reading this got any comments??

CAParticipant

New

I only buy 1 contact per operation. Could you show me the code you are using. It is quite wierd!!

Leo

LeoParticipant

Veteran

Hi CA,

What I think is that you start your journey of automatic trading like me ( or most of us)

first: to much variables means overfitting which means the code only works in the past but not in the future

second: test it 100000 bars (it means at much data as possible)

third: walk forward test, if it works in the walk forward test, then you have a nice code.

Kind Regards

I only buy 1 contact per operation.

So why does this say 1000 as the Lot size then (see red arrow on attached)?

Or has sleep done me no good or even my coffee is not working this morning?? 🙂

Could you show me the code you are using. It is quite wierd!!

I am using testing your code with TRAILINGn at value 133 as you show in your screen shot of optimised results.

Are you sure you have the tick by tick box selected??

We need to get to the bottom of this, I hate oddities like this, but I am driven to investigate!!!! hahahha

This is the code / your code I am using

SHORT = 10

LONG = 38

PERIODOADX = 16

PERIODOSDECRUCE =20

PERIODODECRUCE2 = 50

// Longs

Condition1 = ADX[PERIODOADX] CROSSES OVER PERIODOSDECRUCE

Condition2 = ExponentialAverage[SHORT](Close) > ExponentialAverage[LONG](Close) AND LOW[1] > ExponentialAverage[SHORT](Close)

Condition3 = ExponentialAverage[SHORT](Close) < ExponentialAverage[LONG](Close) AND HIGH[1] < ExponentialAverage[SHORT](Close)

IF NOT LongOnMarket AND Condition1 AND Condition2 THEN

BUY 1 CONTRACTS AT MARKET

ENDIF

// Exit longs

If LongOnMarket AND ADX[PERIODOADX] >= PERIODODECRUCE2 then

allowtrailing = 1

else

allowtrailing = 0

endif

if allowtrailing then

SET STOP pTRAILING 133

endif

If LongOnMarket AND (ExponentialAverage[SHORT](Close) CROSSES UNDER ExponentialAverage[LONG](Close)OR ADX[PERIODOADX] < PERIODOSDECRUCE) THEN

SELL AT MARKET

ENDIF

// Shorts

IF NOT ShortOnMarket AND Condition1 AND Condition3 THEN

SELLSHORT 1 CONTRACTS AT MARKET

ENDIF

// Exit shorts

IF ShortOnMarket AND ADX[PERIODOADX] >= PERIODODECRUCE2 then

allowtrailing = 1

else

allowtrailing = 0

endif

if allowtrailing then

SET STOP pTRAILING 133

endif

IF ShortOnMarket AND (ExponentialAverage[SHORT](Close) CROSSES OVER ExponentialAverage[LONG](Close) OR ADX[PERIODOADX] < PERIODOSDECRUCE) THEN

EXITSHORT AT MARKET

ENDIF

SET STOP LOSS 150// Stops

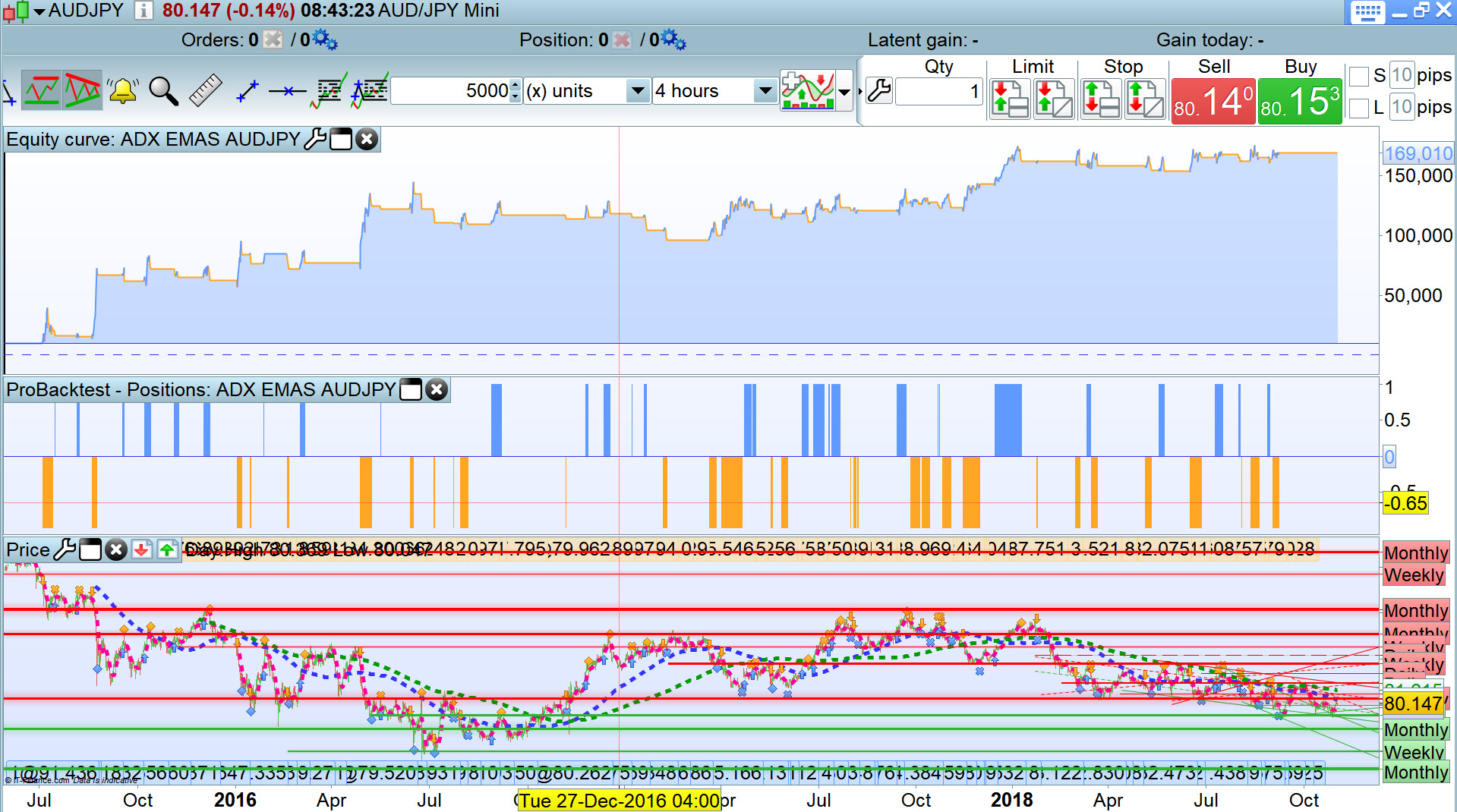

HAHAHA … I can get positive results if I backtest only over 5,000 bars!

As Leo says I think your variables are over-optimised over too short a backtest period?

HAHAHAHHAHAHAHAHHAHAHAHAHAH

It’s all my error!!!!!!!!!!! I’m glad I am driven to investigate!!!!!!!!!!!!!

I had my capital set at 10,000 (as always) but for this test, starting capital needs increasing by at least a factor of 10 to account for GBP to Yen exchange rate!

I get same / similar to you now you!!!!!!!!!!

A useful lesson learnt (for me!!!!!!!)

Results attached over 100k bars

Well done @CA

(Apologies for my doubts!)

CAParticipant

New

Thank you Leo. I have actually tested it in walk forward an it still work! I’ll upload late the results.

CAParticipant

New

Thank you GraHal! So for you it worked! So your opinion is that (at last in theory) it is a good code? I’ll start FT next week as I am still woking out on which par it work and optimizing vales. Later I will post the inicial code from where I start optimiza tío, which, as I said to Leo, have even worked under walk forward optimization.

Any way happy you get to solve what was affecting the code! 🙂

Be aware that SET STOP PTRAILING will certainly not act the same way in live as in backtest, due to the minimal stop level that it is used as the step of stoploss moving. You should use one of the trailing code you’ll find around in the website.