Is the 100 limitation the same in v11? Am I correct in thinking you have the free Daily version of v11?

Sorry GraHal – I missed your questions due to my own ramblings and musings! I have been doing my testing on a combination of v11 and v10.3 and my latest tests were all on v10.3. The v11 EOD has 5 day weeks where the v10.3 via IG has 6 day weeks so I have tended to stick with that on the last few tests just to keep some continuity. Also I struggle to use meaningful spreads in v11 EOD on DJI because it only allows one decimal point and seems to have different pricing /pipsize. So that is a long way of saying that yes perhaps I would be better off testing on v11 in some ways but in other ways not.

Here is another example of SEB’s in action. This time I went back to having a strategy for every day of the week so that it was easier to produce an equity curve in Excel.

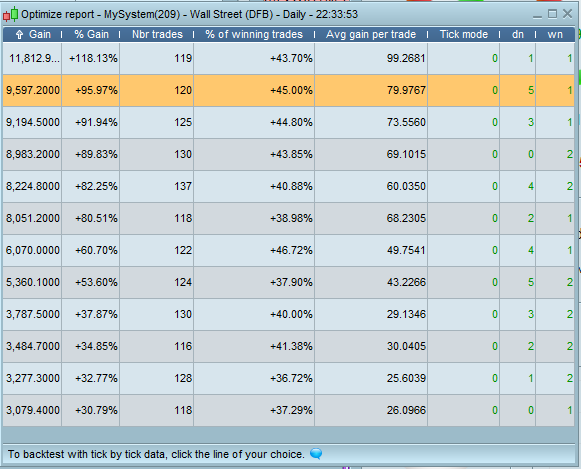

This time the strategy takes an average of RSI and Stochastic and and uses that to decide to open a position and to decide when to close a position. The normal back test only presented results for 88 trades and my SEB test showed that there were a potential 122 trades so it only tested just over 72% of trades. The SEBS test managed to test on 117 trades and so tested just under 96%.

Here is the very simple code:

//optimise with dn from -1 to 5

defparam cumulateorders = false

p = 19

k = 13

p2 = 17

if opendate > 19950101 then

stoch = stochastic[p,k]

myrsi = rsi[p2]

avg = average[(p+p2)/4]((stoch+myrsi)/2)

if dn = -1 or opendayofweek = dn then

if avg > avg[1] and avg[1] < avg[2] and avg[1] < 50 then

trades = trades + 1

buy 1 contract at market

endif

endif

if onmarket and avg < avg[1] and avg[1] > avg[2] and avg[1] > 50 then

sell at market

endif

endif

graph trades

Here are the results (normal back test top and SEBS test bottom):

Gain

Trades

%Winning

Avg. gain

2,405.94

88

73.86%

27.34

3,364.70

117

71.46%

28.76

So that was pretty close – slightly lower win rate% but slightly higher average gain and obviously because we took more trades by running five strategies we made a lot more money – almost 40% more! The average time per trade in the market was just over 25 days for the normal back test and just over 26 for the SEB test so pretty similar. Unfortunately this strategy did not provide many trades even using SEB’s to allow us to test as many trades as possible so we must still be wary of it – but at least it passed the SEB test with flying colours so perhaps it is still worthy of further testing and consideration.

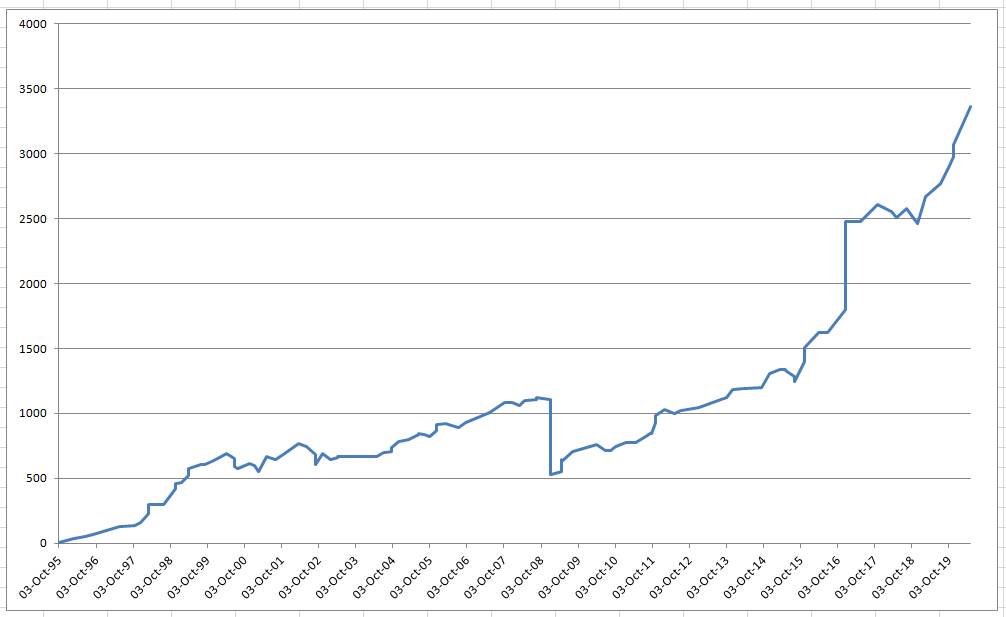

Attached is the Excel equity curve for it and also the normal back test curve. Both took a bit of a dip in the 2008 crash but performance apart from then has been pretty solid.

Is the 100 limitation the same in v11?

I just did a quick test on my v11 EOD and I’m afraid the 100 limit is still there.

I’m looking forward to shift my portfolio to a daily timeframe and this topic will be an obligatory stop on the way.

If i understood well this is the methodology: i create my daily strategy and i run a classic RT to see if it’s acceptable. Then i use the following code to understand how the system would work in every day of the month.

startdate = 19950101

if opendate >= startdate then

tradeon = 0

if (dn = 0) or (day = dn) then

tradeon = 1

endif

After this i can’t understand how we can operatively shift those results into live trading. Once i got 31 results how i can live trade them? Should i run 31 different systems? Also, why you don’t use tick by tick mode?

You could either run 31 strategies or just start a strategy every day that only opens trades tomorrow. If it doesn’t open a trade tomorrow because conditions are not met then delete it and set a new strategy to run for the new tomorrow. Alternatively set 6 strategies running, one for each trading day of the week then once a week set a new strategy running for any days of a week that still have a trade open. This way you will never miss a single trade because you are already on the market.

You can simply add:

dn = 1 //Change from 0 to 5 for Sunday to Friday

tradeon = 0

if opendayofweek = dn then

tradeon = 1

endif

Then use TRADEON as a condition for entry.

I do use tick by tick mode if the strategy I’m testing has any way to exit mid candle with pending orders or stop and target orders. If the strategy only decides whether to close a trade or not at the end of a candle then I don’t need tick by tick.

I guess that preparing the trading week with 5/6 strategies is the best idea.

Anyway thanks as always for the help, that was very clear and helpful 🙂 Are you using this “methodology” in live trading for your daily/weekly strategies? How it’s going?

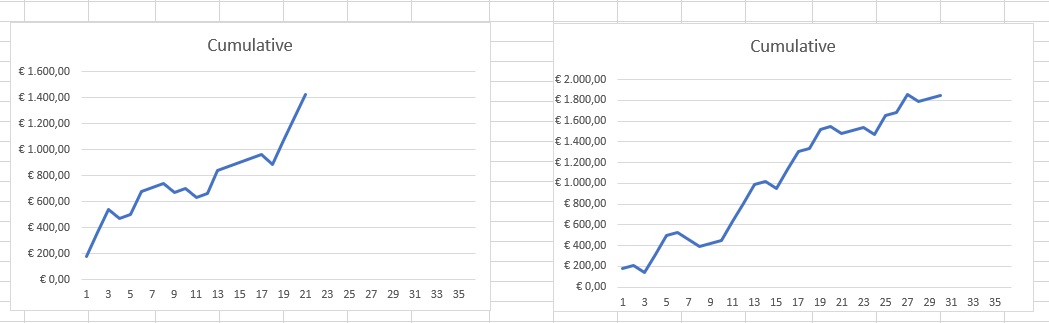

Here’s a first test on a stupid and not Robustness Tested system. On the left we have the classic backtest results, and on the right we have the same system splitted for every day of the week.

+45% positions

+29% gain

SEB testing for me is just a much better robustness test than my VRT because the VRT just used the idea of shaking up and randomising the bars we traded on and then giving us some sort of monte carlo results for us to analyse whereas SEB testing shows us almost 100% of all possible trades if not 100% of all trades. The downside to SEB testing is that due to the need to use something like Excel to analyse the results it is really only practical on daily,weekly or monthly strategies.

I would absolutely love it if PRT added a tool that just added together the results of every possible trade on every bar and gave us statistics and an equity curve of those results. It would be a very powerful tool and much more powerful than our current back tests that miss trades because we are already on the market with a position and so fool us into thinking a strategy is good when in fact it is just curve fitted luck.

Your test of 45% more trades giving 29% more gain is a good example of a strategy that looked better in a standard back test than reality might actual give us. The good thing is that it was still profitable even if not quite as good as it first appeared. Our expectations of its potential have at least been brought a little back down to earth.

At the moment I don’t have any live strategies running because I am out sailing around Greece for the summer with limited gigabytes and not so much time for looking at screens due to the demands of navigation and swimming off the back of the boat and firing up the BBQ whilst sinking a glass of cold wine! It is not all beer and skittles though as I have spent the last few days sweating like a pig in 35C whilst fixing the anchor windlass!

At least you can take an immediate dip in the water when the sweat is excessive, have a good sail 🙂

Hello.

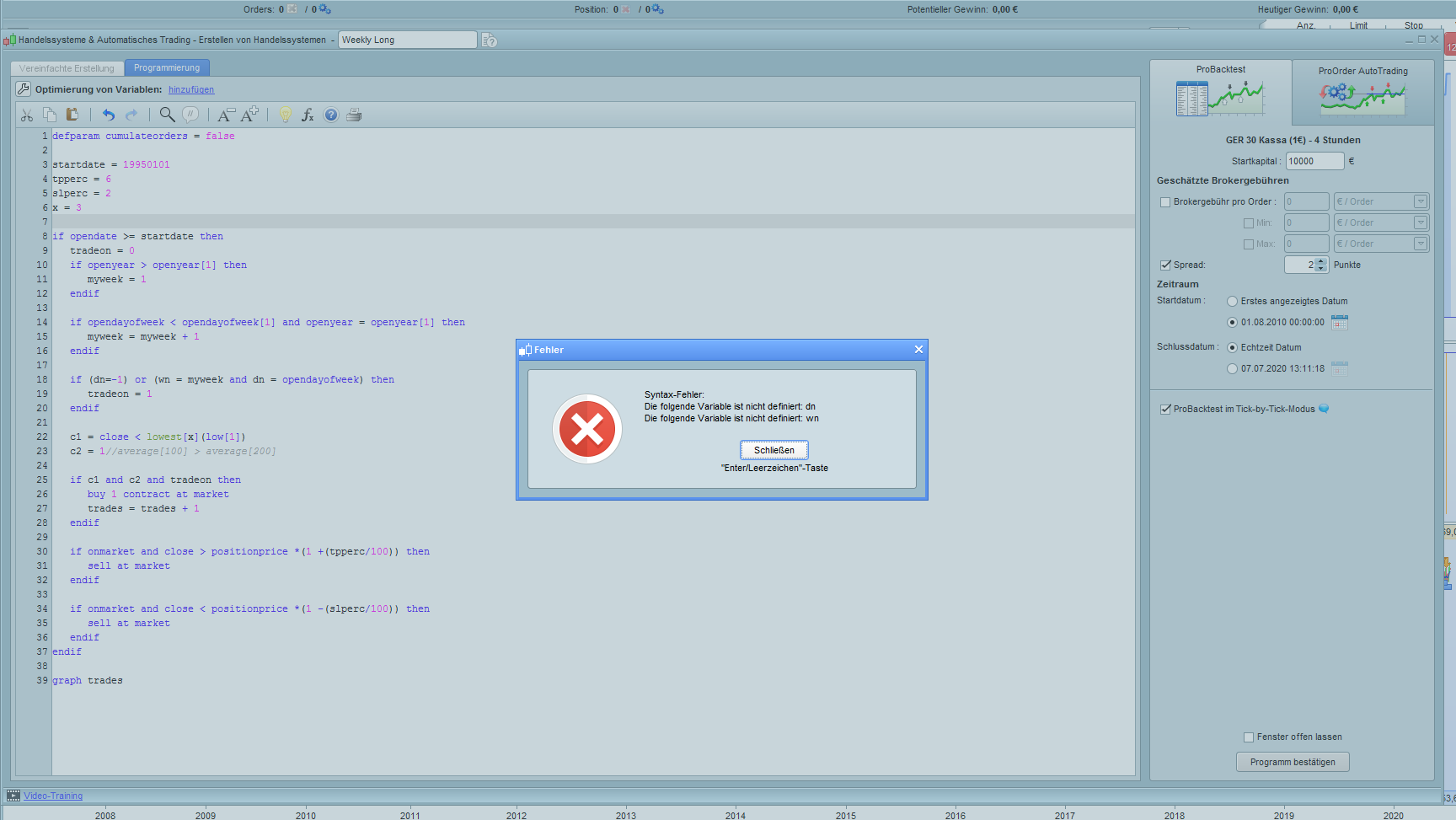

If I copy and paste the code above i got an error message

dn wn not defined

see attached

‘dn’ and ‘wn’ are the variables that you set or optimise to open trades on certain days of certain weeks.

dn = day number (0 to 5)

wn = week number (1 to 53)

Setting dn to -1 carries out a normal back test to use for comparison.

I’ve had a daily strategy on forward test now for a couple of month with five identical strategies running – one for each day of the week – but I noticed that some trades are still open for over a week meaning that I missed possible trades. The ideal solution to this is that I have 53 strategies running (one for every possible week in the year) but IG won’t let me do this in demo so I adjusted the code to at least let me have one strategy for each day in even numbered weeks and one for each day in odd numbered weeks. So 12 possible entry days and a trade will only be missed when a trade is open for over two weeks.

Here is the SEB code:

dn = 1 //0 to 5 for each day of the week

wn = 1 //1 or 2 for odd or even weeks

once thisweek = 1

if opendayofweek < opendayofweek[1] then

if thisweek = 1 then

thisweek = 2

else

thisweek = 1

endif

endif

if opendayofweek = dn and thisweek = wn then

(buy code here)

endif

(exit code here)

The attached images show the results of the 12 strategies running the same code but just trading on different days in odd and even weeks. There are also images for the most profitable and least profitable equity curves plus one for what a normal back test result would show us. Lots of robustness information there!