@ manel : what is the meaning of green trades in excel ?

Hi – there is no meaning, it’s just to separate each set of actions belonging to a specific trade (ie buy, sell, pending orders, trailing stops etc) from each other. Just to make it easier to look at visually. Each block of white or green contains orders that belong to just one fully closed trade (buy and sell).

It is possible that v10.3 is still not able to perform the trailing stop correctly. Maybe the solution, although less beneficial is to put a normal stop and take profit as in the original robot.

To the left what happened in v2, with trailing stop 5, to the right the backtest of v2 with stop 5 and take 10. the money curve is very similar, it is possible that in the backtest or in real the trailing stop does not work correctly .

I will never use pro real time again. None of you should either. We get fooled to use strategies that doesnt work. Dont waste more time or money on software that doesnt work.

I think we need to probably wait for the guys at PRT to iron out some bugs in 10.3 backtest engine as I think there are a few more issues than those just relating to trailing stops. For eg.

1)I cannot backtest beyond 30/11/15 – today as if I pre-load 15,000 units as it comes up with the “could not be analyzed with tick by tick data because this data was not available at this time” error and returns only results for the month of Nov. This could have made sense within the maximum 500 bars limit mentioned earlier BUT – However I can test tick by tick from 28/09/15 to 10/05/16 which is a much longer period of almost 50,000 units without getting that error message. Therefore suggesting that there is some corrupt/unavailable data set in later months and/or another problem or that the earlier period does not even use/have tick by tick data in the PRT software but is incorrectly telling us that it does.

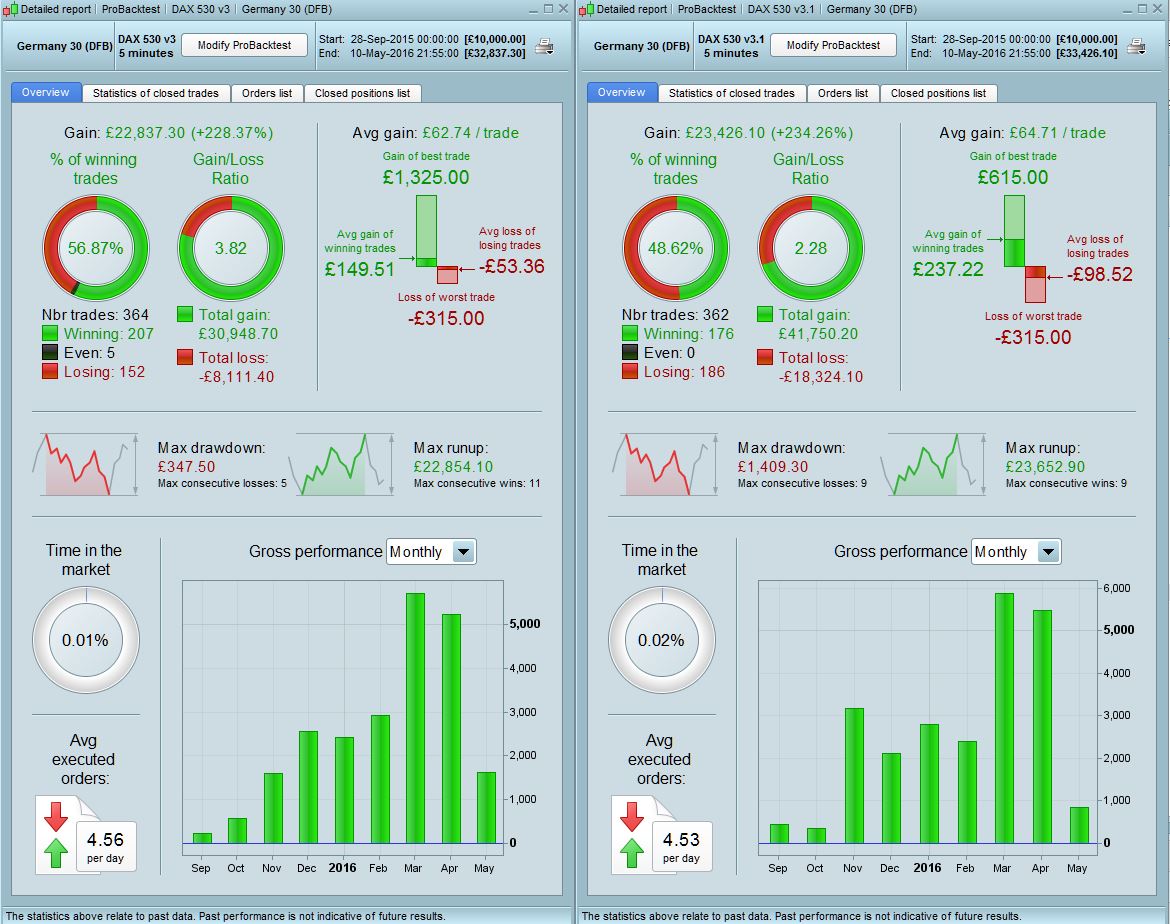

2) In the backtest results the average time in winning positions is 0s and losing positions is less than 10s which as we know from live results cannot be true as positions are held for longer than this.

3) The MFE and MAE calculations in the closed positions list are also incorrect as the positions always either go straight to immediate profit or immediate loss (without any temporary movement in-between) which in reality never occurs of course.

2) and 3) could be inter-related.

But this throws up the whole question of whether even the tick by tick backtesting calculations themselves are reliable which at the moment it has to be said, they aren’t. So we should treat any results with extreme caution until they resolve this issue. I’m sure they are working on it.

Raul – I agree with your findings. Attached is v2 backtest. Left is with a trailing stop of 5 and the right is sl 5 and tp of 10pts. The results overall are remarkably similar (even if there are a few individual variances) which I find difficult to believe, seems too coincidental. Therefore I don’t have much faith even in the stop loss/take profit method either at this time for reasons mentioned earlier due tick by tick testing problems. Something definitely is not right it seems.

personnally i will continue , i want to test v1 v2 v3 during at least 30 days maybe more , two months . i want to compare the equity curve real with the backtest .

When i say compare it is not i want the same results exactly , it seems impossible , i look for the same shape same design .

The whole backtest engine seems crappy. Seems like none of the calculations are done correctly. I just cancelled my subscription and will never trust them again.

I would suggest that PRT need to be directly advised of whatever you think is a problem? I doubt they are working on anything re v 10.3 as they extensively beta tested it for months by VIP users and are releasing to brokers on a gradual basis?

You have a good methodical approach and have got to grips with several issues Manel … how about you advise PRT via your Platform provider (better still if this be PRT Direct?)?

Eric

EricParticipant

Master

to be honest, i dont think “scalping” (with small stops) is the best way of using automated trading with prorealtime

better to focus on swing trading?

and why is everybody trading DAX when there is thousands of other thing to choose from?

i don t understand .

@ all

why are you not happy , because the system is loosing or because the system seems to have in live same results than backtest ?

I just wrote to the PRT team who has wrote this part of the new version, I hope to get news by tomorrow about the different issues.

Do someone tried to remove the SET STOP TRAILING and replaced it with my own trailing codes from the blog please? I’d like to see if we have the same problem of weird exit prices.. I think we should start from here to see if it’s not this instruction that has a different behaviour between the backtest engine and how the IG server deal with it.

Grahal – Actually you make a good point, there would been a lot of UAT testing conducted before the live release of 10.3 so you would have thought that these issues would have been tested and ironed out. I am with IG so I will send a report via PRT charts and hopefully it gets to PRT directly. I will post any updates if I get them here.

The problem we have as users is that we do not have access to more than 200,000 units of tick by tick data which is only around 5 days worth of data so we are unable to verify any backtesting calculations that occurred in any previous weeks or months manually to see if there is a problem. We have to assume that PRT got it correct. Only PRT have access to the underlying data.

I think there are two main issues – The calculations/formulae are obviously not being performed correctly in some cases as explained above and that the backtesting engine is not interpreting the ticks properly/does not have access to the ticks. These are not in itself difficult issues for the software guys to solve so hopefully we will get some resolution soon.