Hello ! 🙂

Here is a strategy that takes only one position per day. On the DJ in h1 at the opening.

This is my version of a classic strategy that I am trying to improve.

It is very simple: we take position once a day in the direction of the trend. Trend confirmed by the MACD and an MA100 at the time of opening.

We exit postion with the ATR trailing stop (code on prorealcode) :

// Période

p = 14

// Average True Range X

ATRx = AverageTrueRange[p](close) * 1.5

// ATRts = ATR Trailing Stop

// Inversion de tendance

IF close crosses over ATRts THEN

ATRts = close - ATRx

ELSIF close crosses under ATRts THEN

ATRts = close + ATRx

ENDIF

// Cacul de l'ATRts lors de la même tendance

IF close > ATRts THEN

ATRnew = close - ATRx

IF ATRnew > ATRts THEN

ATRts = ATRnew

ENDIF

ELSIF close < ATRts THEN

ATRnew = close + ATRx

IF ATRnew < ATRts THEN

ATRts = ATRnew

ENDIF

ENDIF

return ATRts as "ATR Trailing Stop"

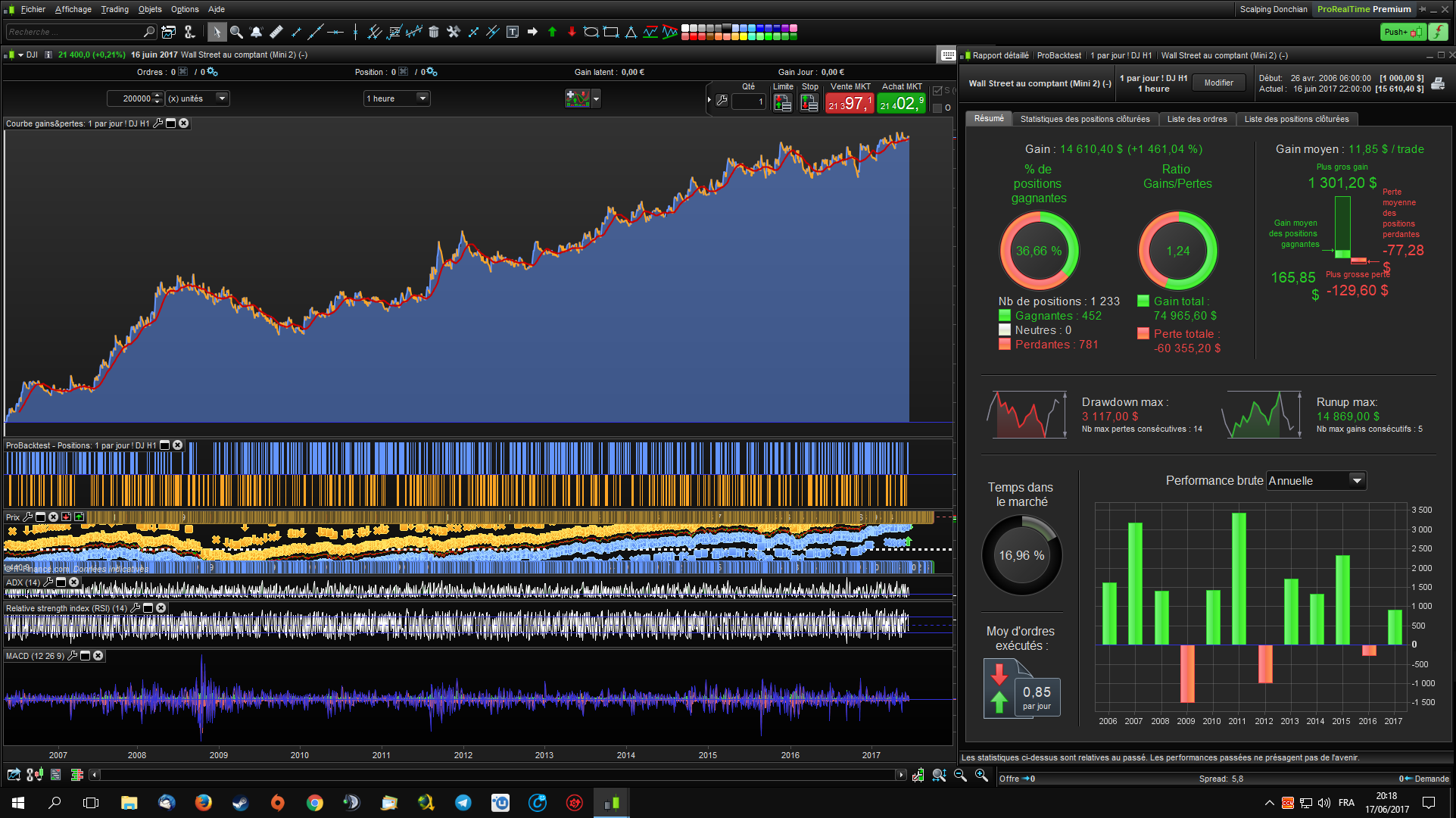

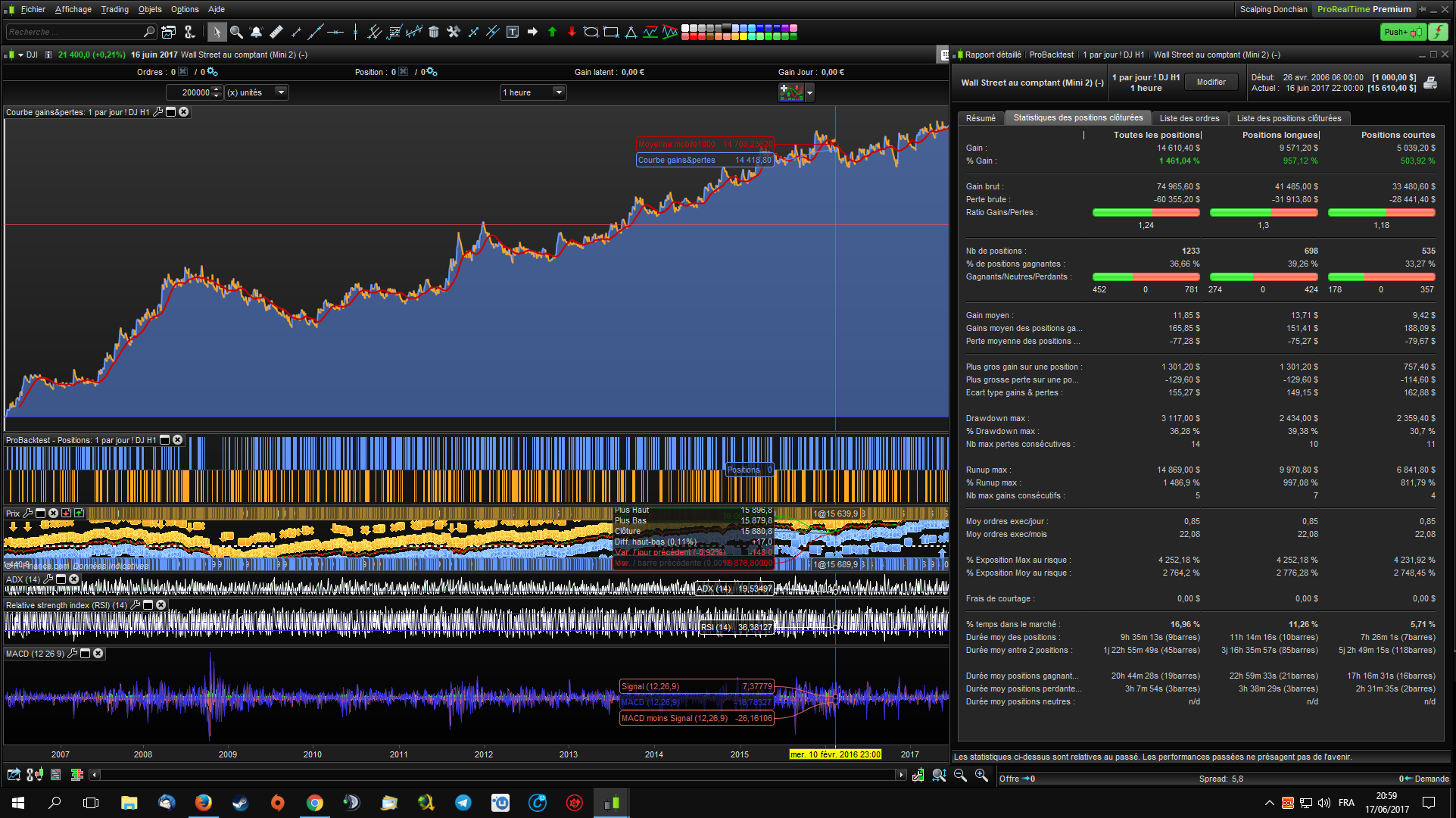

I did not over-optimize it. I code it on 50 000 unit and i test on 200 000 unit. The Spread of 1.8 is included. Starting capital 1000 usd.

The problem is that there are sometimes long series of losses.

Any ideas to reduce the drawdown or to improve the strategy will be appreciated 🙂

TheAccountant

PS : Google translation is my new friends now 🙂 🙂 🙂

// Définition des paramètres du code

DEFPARAM CumulateOrders = False // Cumul des positions désactivé

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position avant l'heure spécifiée

noEntryBeforeTime = 145000

timeEnterBefore = time >= noEntryBeforeTime

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position après l'heure spécifiée

noEntryAfterTime = 151000

timeEnterAfter = time < noEntryAfterTime

// Empêche le système de placer de nouveaux ordres sur les jours de la semaine spécifiés

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

// Conditions pour ouvrir une position acheteuse

indicator1 = Average[100](close)

c1 = (close > indicator1)

indicator2 = MACD[12,26,9](close)

c2 = (indicator2 > 0)

IF (c1 AND c2) AND timeEnterBefore AND timeEnterAfter AND not daysForbiddenEntry THEN

BUY 1 CONTRACT AT MARKET

ENDIF

// Conditions pour fermer une position acheteuse

indicator3 = CALL "ATR trailling Stop"

c3 = (close CROSSES UNDER indicator3)

IF c3 THEN

SELL AT MARKET

ENDIF

// Conditions pour ouvrir une position en vente à découvert

indicator4 = Average[100](close)

c4 = (close < indicator4)

indicator5 = MACD[12,26,9](close)

c5 = (indicator5 < 0)

IF (c4 AND c5) AND timeEnterBefore AND timeEnterAfter AND not daysForbiddenEntry THEN

SELLSHORT 1 CONTRACT AT MARKET

ENDIF

// Conditions pour fermer une position en vente à découvert

indicator6 = CALL "ATR trailling Stop"

c6 = (close CROSSES OVER indicator6)

IF c6 THEN

EXITSHORT AT MARKET

ENDIF

// Stops et objectifs

SET STOP pLOSS 50

Hi Accountant,

Thanks so much for your reply!!!! I will take a look to your system, although I am afraid I am not going to be able to test it for more than 100.000 units, since PRT does not allow more than that.

I can see you have a very narrow timeframe: 14:50-15:10h, so I cannot apply to my system. I operate in M15 from 09:00 to 14:00 and the average time for an operation is 30-60 min, so after that time another one is open. I am browsing the different forums and getting new ideas, but in any case, I do appreciate your help.

As I said, I will review your code and if I see any room for improvement, I will let you know.

Very best,

Juan

P.S.- Good luck with Google translation. I am living in Germany and I can’t live without it ;))))))))

hello !

For now the positions taken directly on the demo account are exactly the same as the backtest !

Good news TheAccountant!

Did you try to test the slope of the 100SMA and/or the MACD one to trigger your orders?

I do not understand what you mean ? I use the 100sma and the MACD. ( une ptite trad en french de “the slope” ? 🙂 ou une ptite explication de ce que tu veux dire en french ? )

Slope means “pente” in French or the “direction” of the curve to be precise 🙂

ok thank ! 🙂

I do not know how to do that. I can put price above or below but according to the Slope I do not know

You can compute a simple slope just by comparing if the current period value of the indicator is superior or inferior to the previous one:

sma100=average[100]

bullish=sma100>sma100[1]

Or you can also add a filter to know the current slope is bullish since 10 bars for example:

sma100=average[100]

bullish=sma100>sma100[1]

longtermbullish=summation[10](bullish)=10

Ok thank you Nicolas. I tested both ways and it’s not better for the drawdown.

I also tried to add a 50sma (sma 50> sma100 for buy) and replaced ATR trailing stop by a simple trailing stop : It’s a little better for the winnings but still with a big drawdown 🙁

You can also use the same slope condition with your MACD.