CN

CNParticipant

Senior

What might the reason be for the sudden loss in momentum?

What might the reason be for the sudden loss in momentum?

At a guess the take profit and stop loss levels just happen to fit the period that it was developed on better than the period since then. This is always a problem with TP and SL levels they are very easy to curve fit to past data. The general theory of the strategy is good but the difference between profits and loss will always come down to how the market is currently moving in relation to these TP and SL fixed levels.

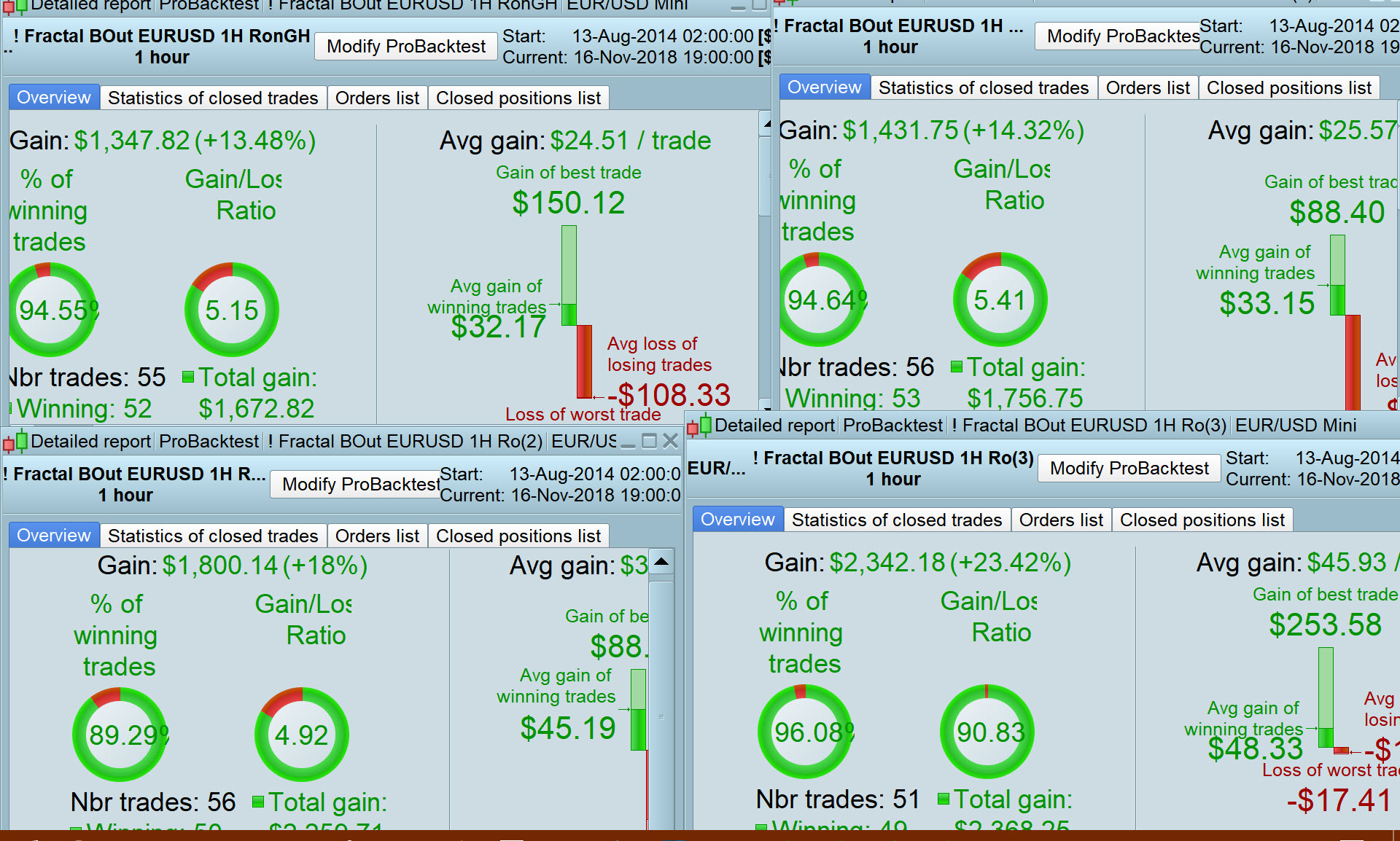

IMO, this is a great strategy with nice potential, OOS speaks for itself.

IMO, this is a great strategy with nice potential, OOS speaks for itself.

I don’t disagree – I just think it is difficult to get excited about the OOS 18.2 pips profit over six trades in one year and 90% of that profit came from just two trades. The lack of any losing trades is exciting though.

It will be interesting to see how this one continues with further real life forward testing.

Can anybody see why I am getting the Rejects for the reason shown (red arrow) on the code below please?

Why is the code trying to take a limit position at a price that is clearly not obtainable (blue arrow)?

And then – in the same second, 100012 code tried to take a stop position at a realistic price as expected ( black arrow).

Version below may include changes I have made.

Hope that makes sense?

Thank You in Advance

//-------------------------------------------------------------------------

// Main code : ! Fractal BOut EURUSD 1H RonGH

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

// Main code : ! Fractal BOut EURUSD 1H RonGH

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

// Main code : ! Fractal BOut EURUSD 1H RonGH

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

// Main code : ! Fractal BOut EURUSD 1H RonGH

//-------------------------------------------------------------------------

//https://www.prorealcode.com/topic/fractal-breakout-intraday-strategy-eurusd-1h/page/20/

//Ronny #48560

//EURUSD(DFB) - IG MARKET

// TIME FRAME 1H

// PROBACKTEST TICK by TICK

// SPREAD 0.9 PIP

// ALE - KASPER - VONASI

DEFPARAM CumulateOrders = false

CP = 101 //Fractal Period

RSINum = 2

Ave = 7 //AverageTrueRange Period

TGLMult = 0.6 //ATR multipier for TGL

STPMult = 1.8 //ATR multiplier for StopLoss

AddOn = 1.1 //Added to STPMult for TakeProfit

RSIHighLevel = 80

RSILowLevel = 100 - RSIHighLevel

//KASPER CODE OF REINVESTMENT

Reinvest=0 //change

if reinvest then

Capital = 5000

Risk = 1//0.1//in % pr position

StopLoss = AverageTrueRange[Ave] * STPMult

TakeProfit = AverageTrueRange[Ave] * STPMult + AddOn

REM Calculate contracts

equity = Capital + StrategyProfit

maxrisk = (equity*(Risk/100))

MAXpositionsize=Capital

MINpositionsize=1

Positionsize= MAX(MINpositionsize,MIN(MAXpositionsize,abs(((maxrisk/StopLoss)))))

else

Positionsize=2

TakeProfit = 40 //change

StopLoss = 50 //change

Endif

///BILL WILLIAM FRACTAL INDICATOR

if Close[cp] >= highest[2*cp+1](Close) then

LH = 1

else

LH = 0

endif

if Close[cp] <= lowest[2*cp+1](Close) then

LL = -1

else

LL = 0

endif

if LH = 1 then

HIL = Close[cp]

endif

if LL = -1 then

LOL = Close[cp]

endif

//CumulativeRSI2

RSI2 = (SUMMATION[RSINum](RSI[RSINum](Close)))/RSINum

RSILow = RSI2 < RSILowLevel

RSIHigh = RSI2 > RSIHighLevel

//LONG and SHORT CONDITIONS

if (time >=100000 and time < 230000) then

C1 = (close CROSSES OVER HIL)

D1 = (close CROSSES UNDER LOL)

IF c1 and NOT ShortOnMarket and RSIHigh THEN

PositionMultiple = (RSI2/100) + 1//Increase PositionSize depending on CumRSI2 level

PositionSize = (PositionSize/((RSIHighLevel/100)+1)) * PositionMultiple

PositionSize = Round(PositionSize * 100)

PositionSize = PositionSize / 100

BUY positionsize CONTRACT AT MARKET

ENDIF

IF D1 and NOT LongOnMarket and RSILow THEN

PositionMultiple = ((100-RSI2)/100) + 1//Increase PositionSize depending on CumRSI2 level

PositionSize = (PositionSize/((RSIHighLevel/100)+1)) * PositionMultiple

PositionSize = Round(PositionSize * 100)

PositionSize = PositionSize / 100

SELLSHORT positionsize CONTRACT AT MARKET

ENDIF

ENDIF

//TRAILING STOP

TGL = AverageTrueRange[Ave] * TGLMult

TGS = TGL

if not onmarket then

MAXPRICE = 0

MINPRICE = close

PriceExit = 0

ENDIF

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

if MAXPRICE-tradeprice(1)>=TGL*pointsize then

PriceExit = MAXPRICE-TGL*pointsize

ENDIF

ENDIF

if shortonmarket then

MINPRICE = MIN(MINPRICE,close)

if tradeprice(1)-MINPRICE>=TGS*pointsize then

PriceExit = MINPRICE+TGS*pointsize

ENDIF

ENDIF

if onmarket and PriceExit>0 then

EXITSHORT AT PriceExit STOP

SELL AT PriceExit STOP

ENDIF

set target profit TakeProfit

set stop ploss stoploss

Related to limited risk account I guess. Stoploss can’t be too far related to the margin required..

Stoploss can’t be too far related to the margin required..

This is why I am confused … isn’t the StopLoss = 50 at Line 50 and used in Line 124 (set stop ploss stoploss)?

Also it is Limit Orders (not Stops) that are being rejected as being too far from price.

You need to add a p

set target pprofit TakeProfit\

@GraHal TGL is 0, because it’s a price and does not need to be converted using POINTSIZE. Replace those lines with:

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

if MAXPRICE-tradeprice(1)>=TGL then//*pointsize then

PriceExit = MAXPRICE-TGL//*pointsize

ENDIF

ENDIF

if shortonmarket then

MINPRICE = MIN(MINPRICE,close)

if tradeprice(1)-MINPRICE>=TGS then//*pointsize then

PriceExit = MINPRICE+TGS//*pointsize

ENDIF

ENDIF

This will affect performance a bit.

You don’t need to add a P, since those values are differences in price, not in Pips,

Hello Guys, how can I find the last updated code from Ale? There are a lot of posts… Grazie / Thanks Giuseppe

You don’t need to add a P, since those values are differences in price, not in Pips,

You are right, but it doesn’t matter if the instrument has a pipsize = 1, and this is the case for DAX.

Nicolas, this is EurUsd, not DAX.

Indeed lines 49-50 should have * POINTSIZE before the comment, so their values match lines 38-39 which are in price (probably Francesco78 referred to lines 49-50). So GraHal will have to choose one of the two ways and use PROFIT/LOSS with/without P accordingly.

Thanks guys

hahahah I’ve tried 4 combinations of your suggestions and results just get better and better! 🙂

Now to start thinking what is really happening and interpreting your suggestions?

Results seem too good to be true?