Good Day

We can use this thread to further discuss possible enhancements on the Combined Supertrend EURUSD 4Hr strategy posted in the Library:

https://www.prorealcode.com/prorealtime-trading-strategies/combined-supertrend-eurusd-4hr/

Hi @Juanan71 please might you share the changes you made to Juanj code?

Juanj code is well good, your changes make the equity curve look sooo good, you will understand we are interested in, and want to learn from, the coding details!?

Did it take you long?

Thank You

GraHal

Is no good..other backtest bug…does not work on real

@juanan71 it be good to share your version of the code anyway, others may spot the problem and then we all good to go!?

Or was it that you did not have the tick by tick box checked??

Cheers

GraHal

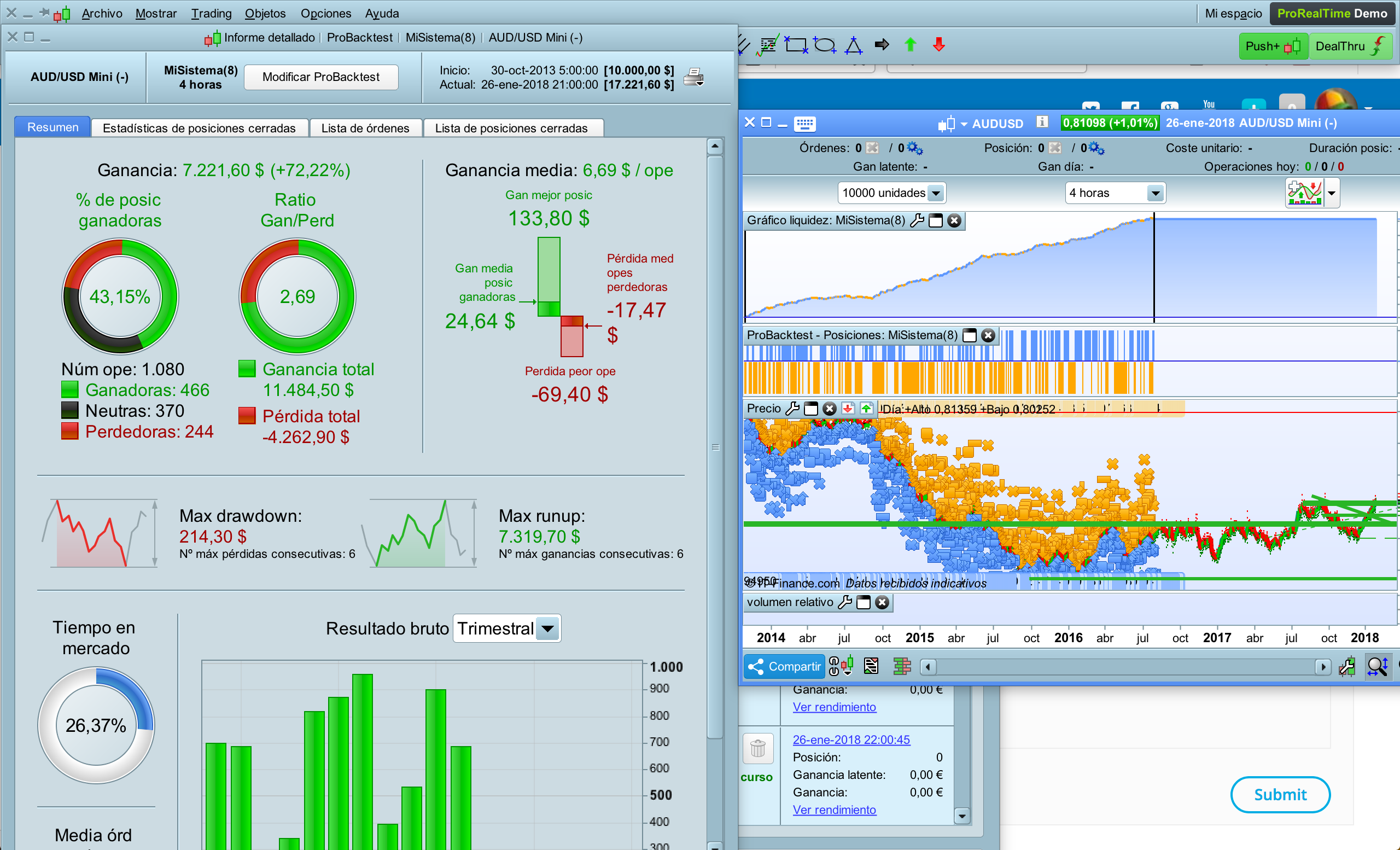

Problem is backtest does not work like demo mode in real time.Backtest make many neutral trades in 0 but really in demo mode is not like that…these trades close at stop loss ..never in be and i dont know why

Just i’ve added the trailing stop made for Nicolas time ago but this trailing is aplyed at the close of candle and no follow the price…problem…when sl or trailing step is in the same candle backtest can not calculate and return very good results but are not reals.

Code of trailing is this but i dont know how integrate it because does not work properly…try this…copy and paste this code at final of any system you have and check resuts in 2h,4h,1h… you will see are amazing but no real

128 line to final add to any other code

Defparam cumulateorders = false

possize = 1

//////////////////////////////////////////////////////////////

//Andrew Abraham Trend Trader

//Posted by @Nicolas in PRC Library

/////////////////////////////////////////////////////////////

Length = 21

Multiplier = 3

avrTR = weightedaverage[Length](AverageTrueRange[1](close))

highestC = highest[Length](high)

lowestC = lowest[Length](low)

hiLimit = highestC[1]-(avrTR[1]*Multiplier)

lolimit = lowestC[1]+(avrTR[1]*Multiplier)

if(close > hiLimit AND close > loLimit) THEN

ret = hiLimit

ELSIF (close < loLimit AND close < hiLimit) THEN

ret = loLimit

ELSE

ret = ret[1]

ENDIF

/////////////////////////////////////////////////////////////

//Simplified supertrend (without volatility component ATR)

//Posted by @verdi55 in PRC Library

/////////////////////////////////////////////////////////////

ONCE direction = 1

ONCE STlongold = 0

ONCE STshortold = 1000000000000

factor = 0.005

indicator1 = medianprice

indicator3 = close

indicator2 = indicator3 * factor

STlong = indicator1 - indicator2

STshort = indicator1 + indicator2

If direction = 1 and STlong < STlongold then

STlong = STlongold

endif

If direction = -1 and STshort > STshortold then

STshort = STshortold

endif

If direction = 1 and indicator3 < STlong then

direction = -1

endif

If direction = -1 and indicator3 > STshort then

direction = 1

endif

STlongold = STlong

STshortold = STshort

If direction = 1 then

ST = STlong

else

ST = STshort

endif

/////////////////////////////////////////////////////////////

//PRC_adaptive SuperTrend (r-square method) | indicator

//Posted by @Nicolas in PRC Library

/////////////////////////////////////////////////////////////

Period = 10

mult = 2

Data = customclose

SumX = 0

SumXX = 0

SumXY = 0

SumYY = 0

SumY = 0

if barindex>Period then

// adaptive r-squared periods

for k=0 to period-1 do

tprice = Data[k]

SumX = SumX+(k+1)

SumXX = SumXX+((k+1)*(k+1))

SumXY = SumXY+((k+1)*tprice)

SumYY = SumYY+(tprice*tprice)

SumY = SumY+tprice

next

Q1 = SumXY - SumX*SumY/period

Q2 = SumXX - SumX*SumX/period

Q3 = SumYY - SumY*SumY/period

iRsq=((Q1*Q1)/(Q2*Q3))

avg = supertrend[mult,round(Period+Period*(iRsq-0.25))]

EndIf

//////////////////////////////////////////////////////////////////

OriginalST = Supertrend[3,5]

/////////////////////////////////////////////////////////////////

margin = 7*pointsize

If countofposition = 0 and abs(ret[1]-ST[1]) > margin and abs(ret-ST) > margin Then

If close > ret and close > ST and close > avg Then

Buy possize contract at market

ElsIf close < ret and close < ST and close < avg Then

Sellshort possize contract at market

EndIf

ElsIf longonmarket and ((abs(ret[1]-ST[1]) < margin and abs(ret-ST) < margin) or ((close < ret and close < ST and close < avg and close < OriginalST) and (close[1] < ret[1] and close[1] < ST[1] and close[1] < avg[1] and close[1] < OriginalST[1]))) Then

Sell at market

ElsIf shortonmarket and ((abs(ret[1]-ST[1]) < margin and abs(ret-ST) < margin) or ((close > ret and close > ST and close > avg and close > OriginalST) and (close[1] < ret[1] and close[1] < ST[1] and close[1] > avg[1] and close[1] < OriginalST[1]))) Then

Exitshort at market

EndIf

SL = 20//15//20 // Initial SL

TP = 0//30

TSL = 1 // Use TSL?

TrailingDistance =5// 20//20//20 // Distance from close to TSL

TrailingStep =5// 20//20//3 // Pips locked at start of TSL

//************************************************************************

IF TSL = 1 THEN

//reset the stoploss value

IF NOT ONMARKET THEN

newSL = 0

CAND = 0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL = 0 AND CLOSE - TRADEPRICE(1) >= TrailingDistance*PipSize THEN

newSL = TRADEPRICE(1) + TrailingStep*PipSize

ENDIF

//next moves

CAND = BarIndex - TradeIndex

IF newSL > 0 AND CLOSE[1] >= HIGHEST[CAND](CLOSE) THEN

newSL = CLOSE[1] - TrailingDistance*PipSize

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL = 0 AND TRADEPRICE(1) - CLOSE[1] >= TrailingDistance*PipSize THEN

newSL = TRADEPRICE(1) - TrailingStep*PipSize

ENDIF

//next moves

CAND = BarIndex - TradeIndex

IF newSL > 0 AND CLOSE[1] <= LOWEST[CAND](CLOSE) THEN

newSL = CLOSE[1] + TrailingDistance*PipSize

ENDIF

ENDIF

//stop order to exit the positions

IF newSL > 0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

SET STOP pLOSS SL

set target pprofit tp

ENDIF

@Juanan71 thanks for sharing.

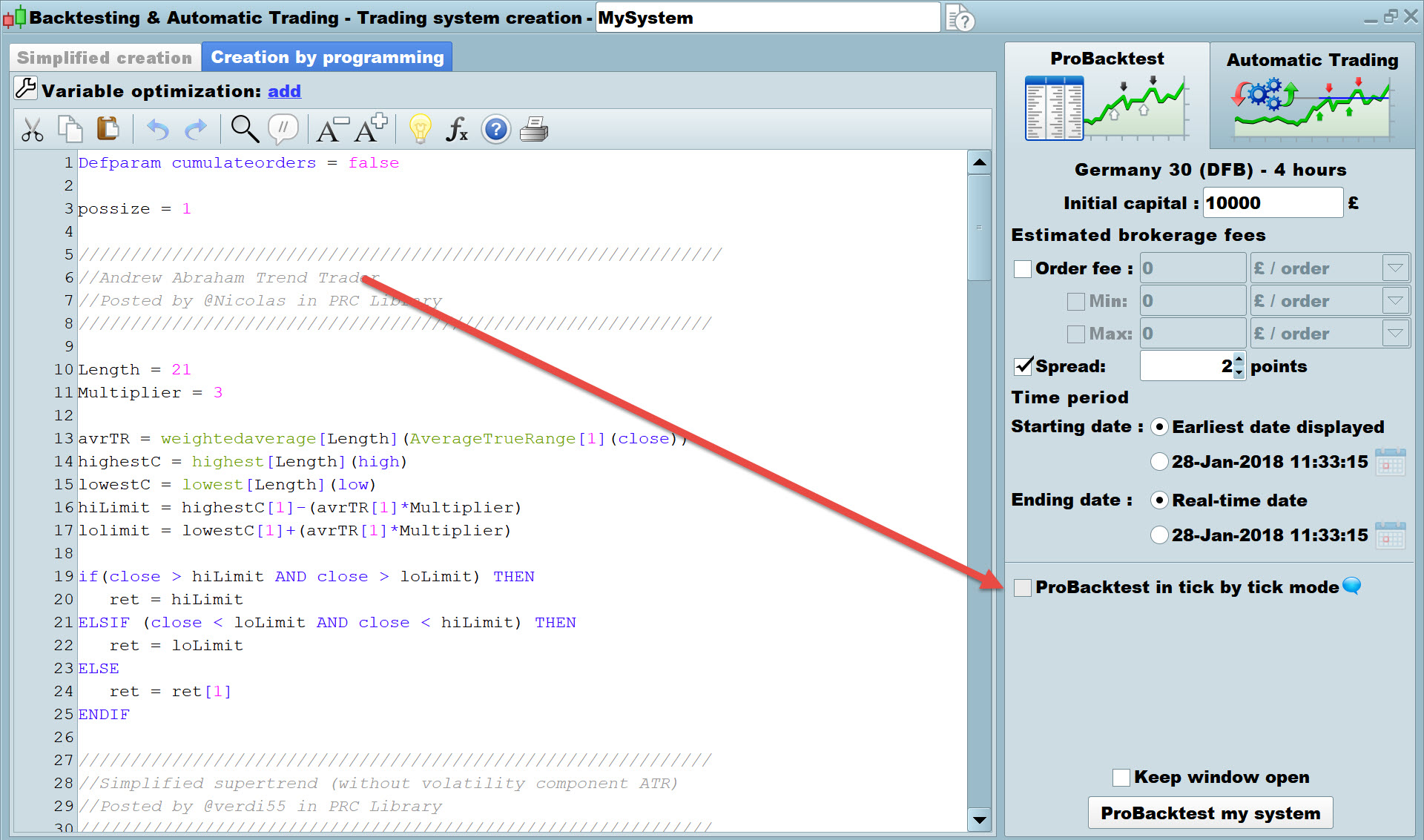

Your problem … Backtest make many neutral trades in 0 … is due to the tick by tick box not being checked during backtesting. See attached image.

To make backtest work like real trading it has to be in tick by tick mode … because that is what happens in real trading.

If you want more information then search for zero bars on this site. Or, as it is quite boring, save yourself time and just accept the explanation above 🙂 (0 bars / zero bars is called other names also on here, but it’s so long since I’ve looked at this I’ve forgotten the other names! 🙂 )

Cheers

GraHal

So you mean should make backtest ithout tick by tick? my english is not so good…and really the good resuts was without tick by tick in this case?

No it has to be with tick by tick selected to work as near as possible to Live Trading.

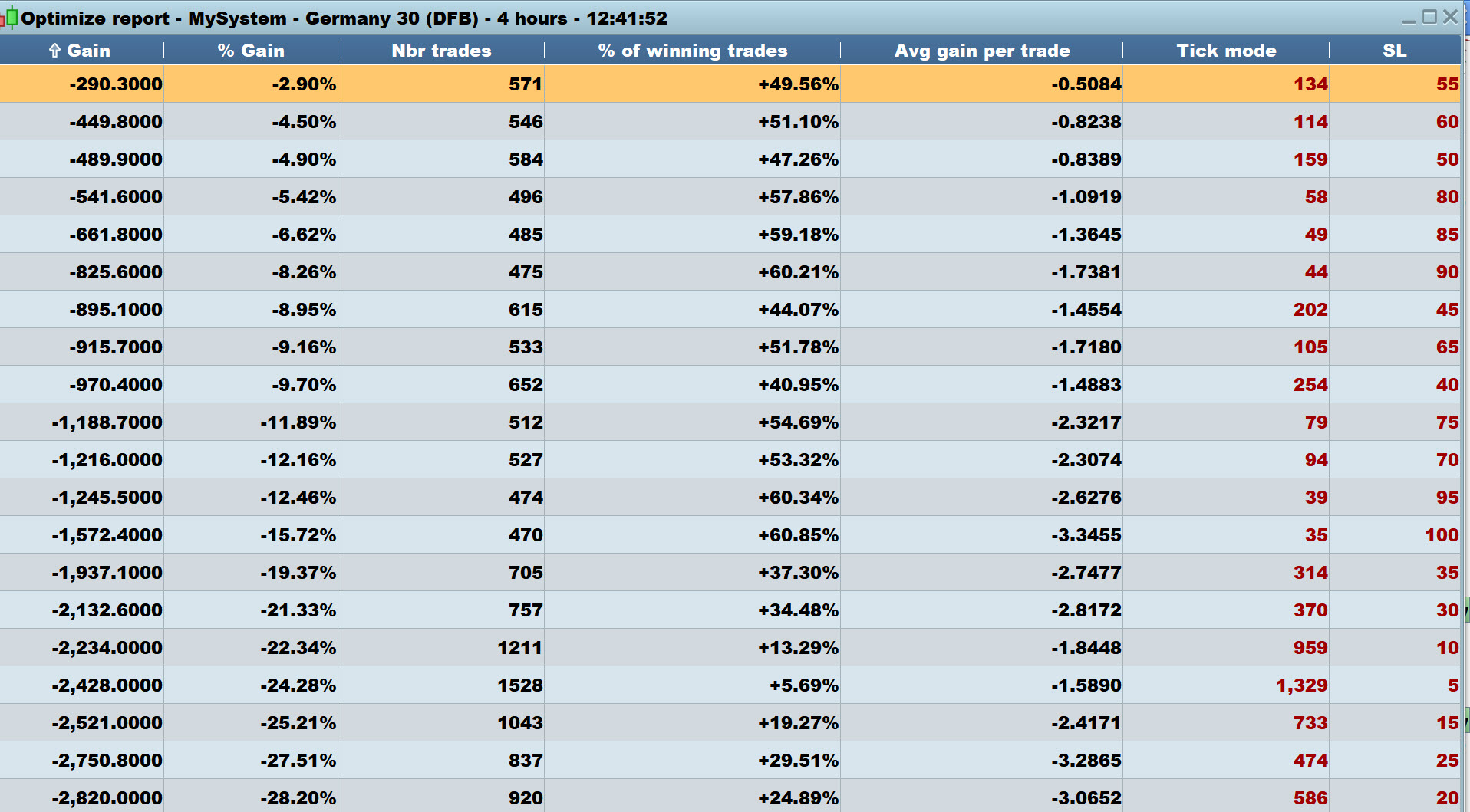

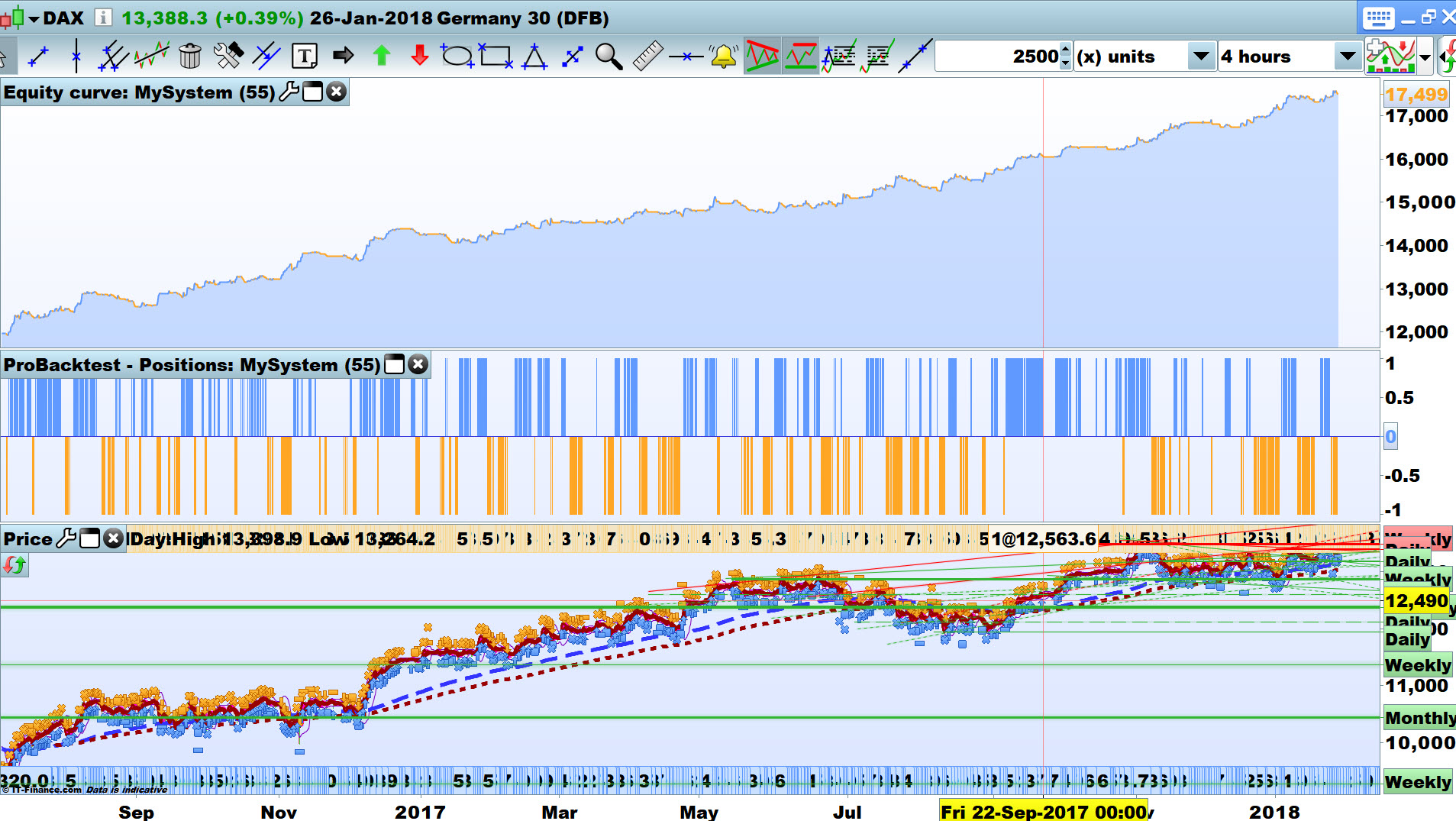

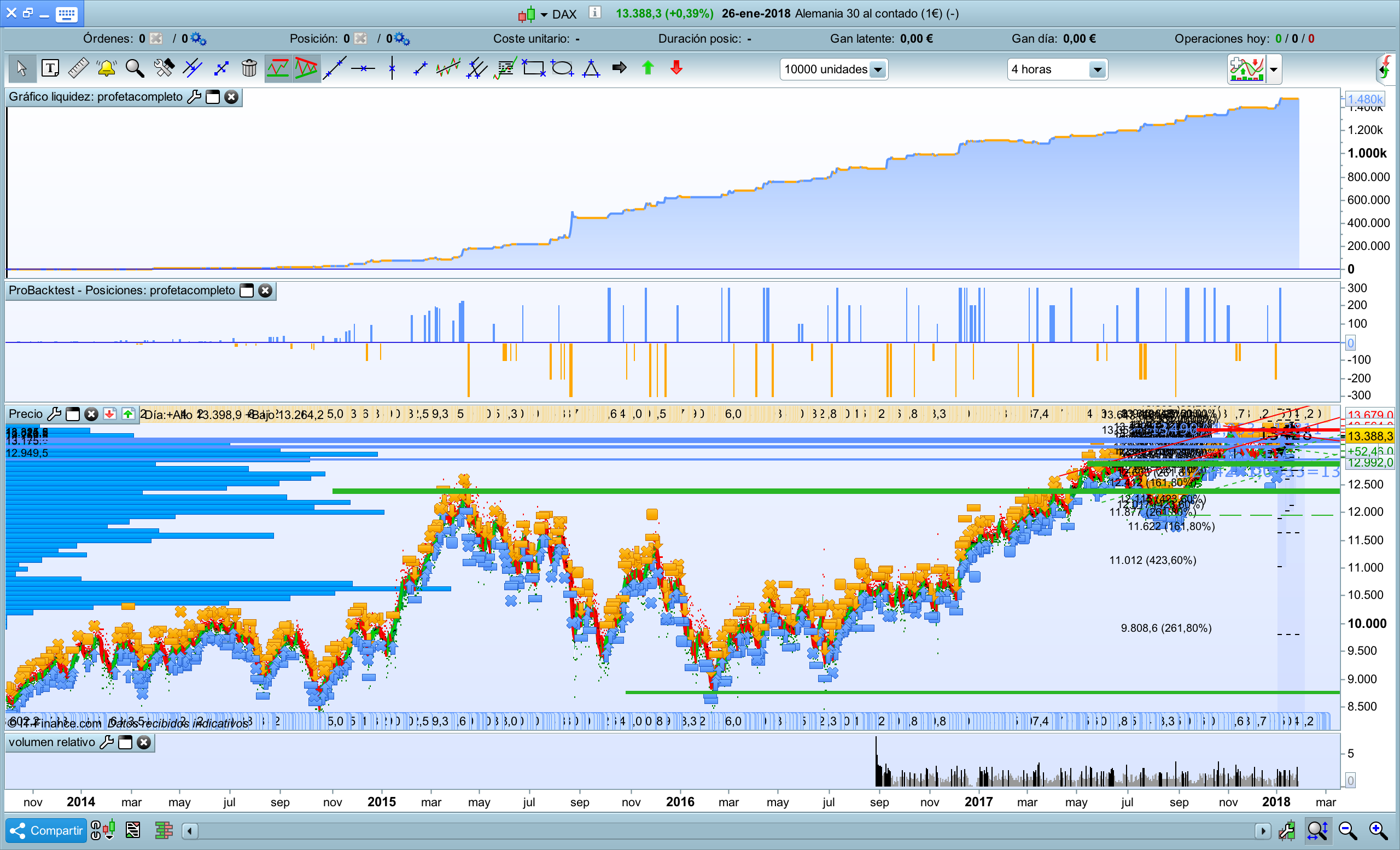

Also, I think your setting of TP = 0 in your code is why there’s massive difference between the optimised results table (shows bad) and the equity curve (shows good!) … even with tick by tick selected. See attached.

I will continue to think on this while I have a shave! Often have brainwaves while shaving / cleaning teeth and away from the screen! 🙂

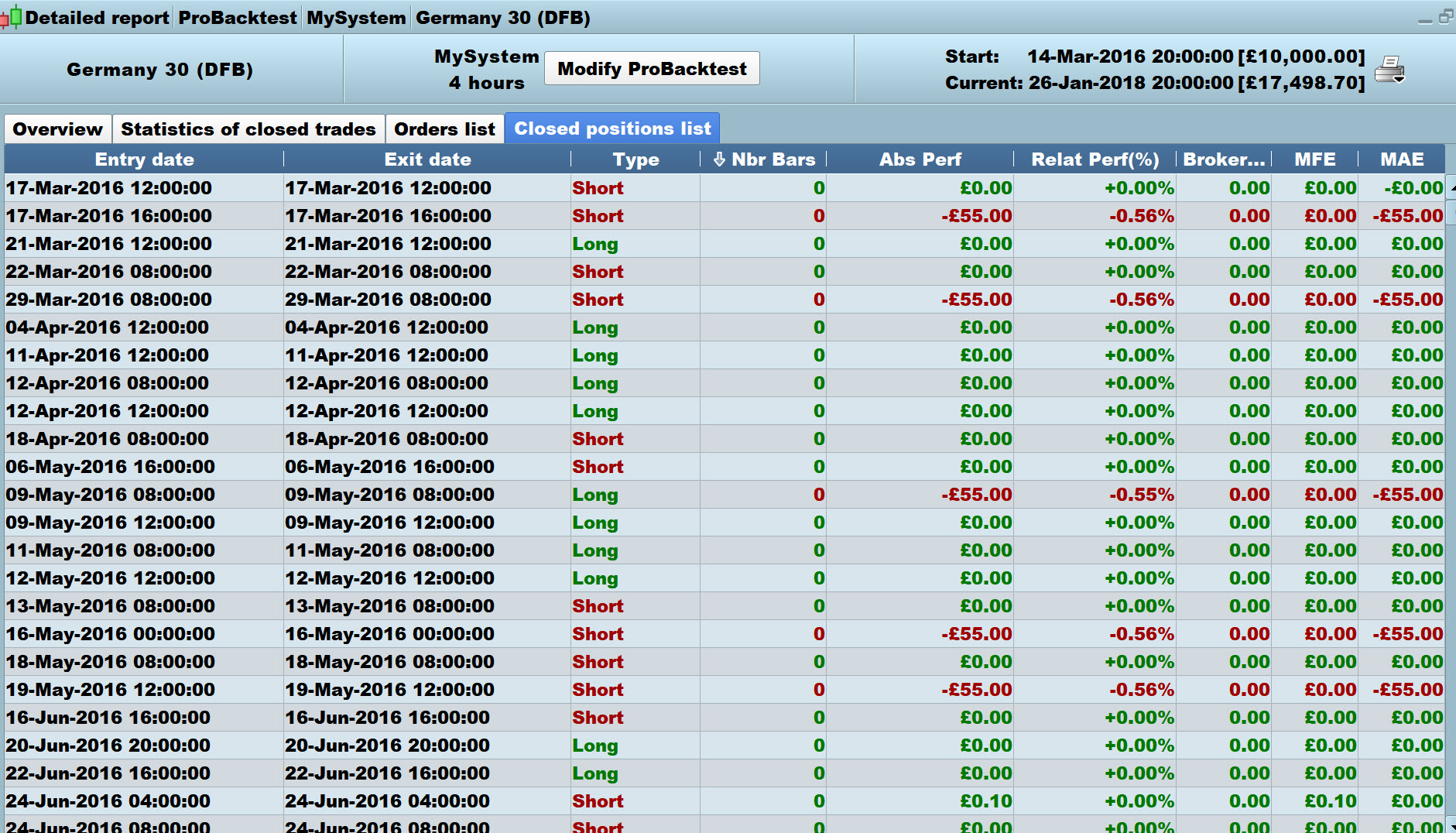

I haven’t studied / understood your code, but when there is a zero bar / 0 bar then on the equity curve it is showing as 0 profit but in reality it has been a SL value loss (in my case attached SL = £55 loss!

But the odd thing is … some 0 bars / zero bars do show as -£55 loss (see attached) so still some thinking to do! 🙂

I went over a few trades bar by bar on a 1 min TF and the anomaly (see line above) doesn’t seem to be related to whether a profit is hit before the -55 loss or vice versa.

Any comments anyone??

GraHal

Often have brainwaves while shaving / cleaning teeth and away from the screen!

I should try it.

You should – I have my best ideas in the shower. I am sometimes in there for far too long though!

I still dont know whats exactly the problem….my idea is keep these neutral trades because are important….If can not be neutral maybe loss 1 or 2 points but if i have more winning trades it will be good..any idea for make this neutral trades if price turn back? i mean if price go up for later go down…be sure will not arrive to sl but if price goes down at the beggining of the trade is no problem if arrives to sl…

If you have a good strategy and a good entry system winning the most times and keeping neutral others….we’ll have a good system i think but

if i’m working on a system and after a hard job tested with tic by tic and results are so good but no real…why work? maybe you’ll found other prt bug and all your job is lost again

Often have brainwaves while shaving / cleaning teeth and away from the screen!

I should try it.

Vonasi wrote

You should – I have my best ideas in the shower. I am sometimes in there for far too long though!

Maybe Nicolas means he should try just getting away from the screen !!?? 🙂 🙂

Por ejemplo este sistema…de que me sirve trabajar en él si resuta que luego no va a hacer lo que debe hacer…quién me dice que cualquier otro que haga no pasará lo mismo y seguira fallando una y otra cosa???…no me fio para nada ya de los backtest ni del propio prorealtime…creo que tiene muchas cosas que pulir y arreglar.

Me siento decepcionado

@Juanan71 logically the value TP = 0 (your code above line 129 & line 175) is corrupting all the figures. Why have a Take Profit / TP at 0??

Best you read up on the 0 bars / zero bars issue (search on this site) as maybe this is the only way to appreciate what is happening?

Also you have the settings below on Nicolas Trailing Stop. These are not realistic as a trailing distance of 5 would get hit all the time?? The minimum on Dax is 6 points anyway and price retraces 6 points (in a few seconds) at almost every move up / down > 10 to 12 points.

TrailingDistance =5// 20//20//20 // Distance from close to TSL

TrailingStep =5// 20//20//3 // Pips locked at start of TSL

GraHal