We are all multimillionaires…

Try this : I just added my famous exponential growth routine.

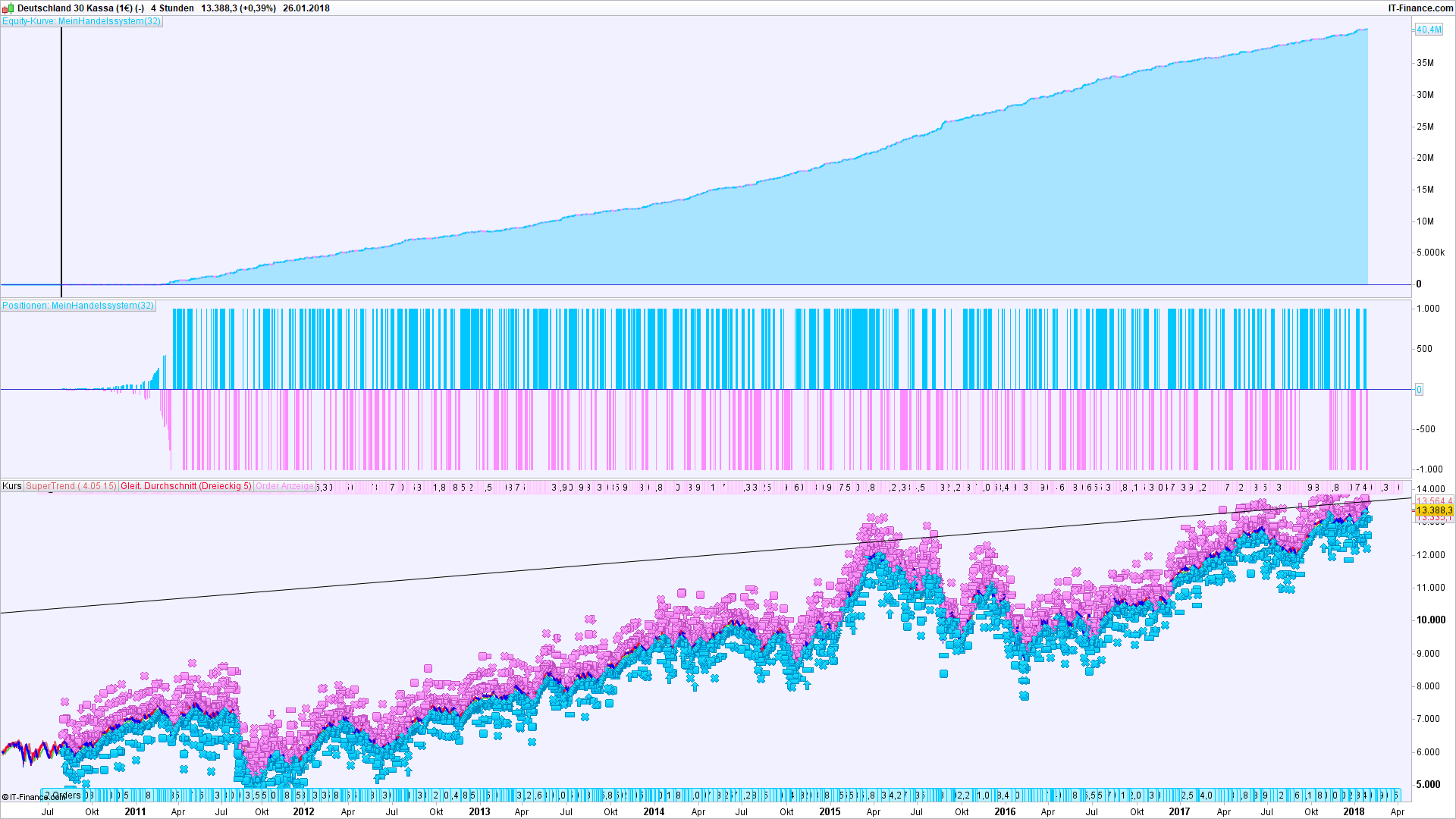

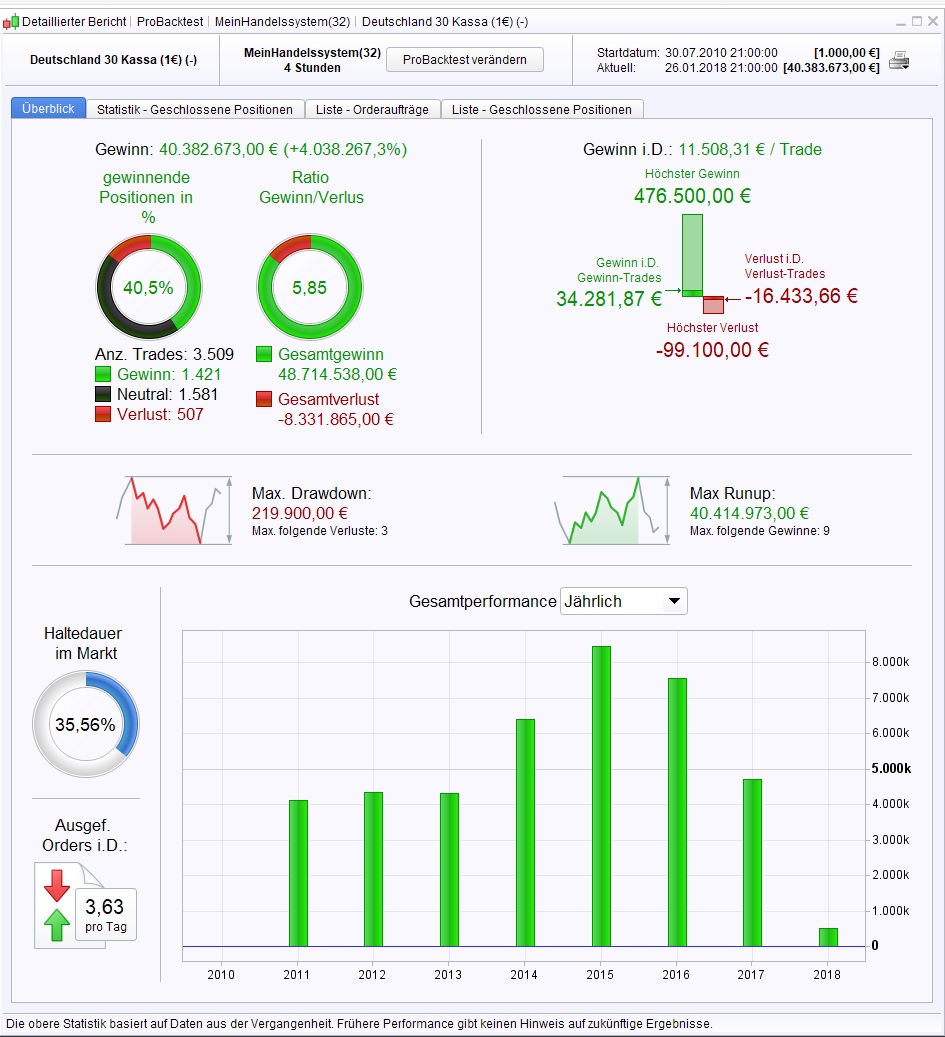

Starting capital on 01.08.2010 is € 1000, and we start trading with only 1 initial DAX mini contract. The system reinvests profits and grows in position size until a maximum number of 1000 DAX mini contracts is reached.

Defparam cumulateorders = false

//exponential growth of position size - reinvestment of profit

cp = countofposition

pp = positionperf

pprice = positionprice

SP = strategyprofit

number = 1 + ((SP + pp * pprice * ABS(cp)) / 250)

n = round(number)

If n <= 1 then

n = 1

endif

If n > 1000 then

n = 1000

endif

possize = n

//////////////////////////////////////////////////////////////

//Andrew Abraham Trend Trader

//Posted by @Nicolas in PRC Library

/////////////////////////////////////////////////////////////

Length = 21

Multiplier = 3

avrTR = weightedaverage[Length](AverageTrueRange[1](close))

highestC = highest[Length](high)

lowestC = lowest[Length](low)

hiLimit = highestC[1]-(avrTR[1]*Multiplier)

lolimit = lowestC[1]+(avrTR[1]*Multiplier)

if(close > hiLimit AND close > loLimit) THEN

ret = hiLimit

ELSIF (close < loLimit AND close < hiLimit) THEN

ret = loLimit

ELSE

ret = ret[1]

ENDIF

/////////////////////////////////////////////////////////////

//Simplified supertrend (without volatility component ATR)

//Posted by @verdi55 in PRC Library

/////////////////////////////////////////////////////////////

ONCE direction = 1

ONCE STlongold = 0

ONCE STshortold = 1000000000000

factor = 0.005

indicator1 = medianprice

indicator3 = close

indicator2 = indicator3 * factor

STlong = indicator1 - indicator2

STshort = indicator1 + indicator2

If direction = 1 and STlong < STlongold then

STlong = STlongold

endif

If direction = -1 and STshort > STshortold then

STshort = STshortold

endif

If direction = 1 and indicator3 < STlong then

direction = -1

endif

If direction = -1 and indicator3 > STshort then

direction = 1

endif

STlongold = STlong

STshortold = STshort

If direction = 1 then

ST = STlong

else

ST = STshort

endif

/////////////////////////////////////////////////////////////

//PRC_adaptive SuperTrend (r-square method) | indicator

//Posted by @Nicolas in PRC Library

/////////////////////////////////////////////////////////////

Period = 10

mult = 2

Data = customclose

SumX = 0

SumXX = 0

SumXY = 0

SumYY = 0

SumY = 0

if barindex>Period then

// adaptive r-squared periods

for k=0 to period-1 do

tprice = Data[k]

SumX = SumX+(k+1)

SumXX = SumXX+((k+1)*(k+1))

SumXY = SumXY+((k+1)*tprice)

SumYY = SumYY+(tprice*tprice)

SumY = SumY+tprice

next

Q1 = SumXY - SumX*SumY/period

Q2 = SumXX - SumX*SumX/period

Q3 = SumYY - SumY*SumY/period

iRsq=((Q1*Q1)/(Q2*Q3))

avg = supertrend[mult,round(Period+Period*(iRsq-0.25))]

EndIf

//////////////////////////////////////////////////////////////////

OriginalST = Supertrend[3,5]

/////////////////////////////////////////////////////////////////

margin = 7*pointsize

If countofposition = 0 and abs(ret[1]-ST[1]) > margin and abs(ret-ST) > margin Then

If close > ret and close > ST and close > avg Then

Buy possize contract at market

ElsIf close < ret and close < ST and close < avg Then

Sellshort possize contract at market

EndIf

ElsIf longonmarket and ((abs(ret[1]-ST[1]) < margin and abs(ret-ST) < margin) or ((close < ret and close < ST and close < avg and close < OriginalST) and (close[1] < ret[1] and close[1] < ST[1] and close[1] < avg[1] and close[1] < OriginalST[1]))) Then

Sell at market

ElsIf shortonmarket and ((abs(ret[1]-ST[1]) < margin and abs(ret-ST) < margin) or ((close > ret and close > ST and close > avg and close > OriginalST) and (close[1] < ret[1] and close[1] < ST[1] and close[1] > avg[1] and close[1] < OriginalST[1]))) Then

Exitshort at market

EndIf

SL = 20//15//20 // Initial SL

TP = 0//30

TSL = 1 // Use TSL?

TrailingDistance =5// 20//20//20 // Distance from close to TSL

TrailingStep =5// 20//20//3 // Pips locked at start of TSL

//************************************************************************

IF TSL = 1 THEN

//reset the stoploss value

IF NOT ONMARKET THEN

newSL = 0

CAND = 0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL = 0 AND CLOSE - TRADEPRICE(1) >= TrailingDistance*PipSize THEN

newSL = TRADEPRICE(1) + TrailingStep*PipSize

ENDIF

//next moves

CAND = BarIndex - TradeIndex

IF newSL > 0 AND CLOSE[1] >= HIGHEST[CAND](CLOSE) THEN

newSL = CLOSE[1] - TrailingDistance*PipSize

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL = 0 AND TRADEPRICE(1) - CLOSE[1] >= TrailingDistance*PipSize THEN

newSL = TRADEPRICE(1) - TrailingStep*PipSize

ENDIF

//next moves

CAND = BarIndex - TradeIndex

IF newSL > 0 AND CLOSE[1] <= LOWEST[CAND](CLOSE) THEN

newSL = CLOSE[1] + TrailingDistance*PipSize

ENDIF

ENDIF

//stop order to exit the positions

IF newSL > 0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

SET STOP pLOSS SL

set target pprofit tp

ENDIF

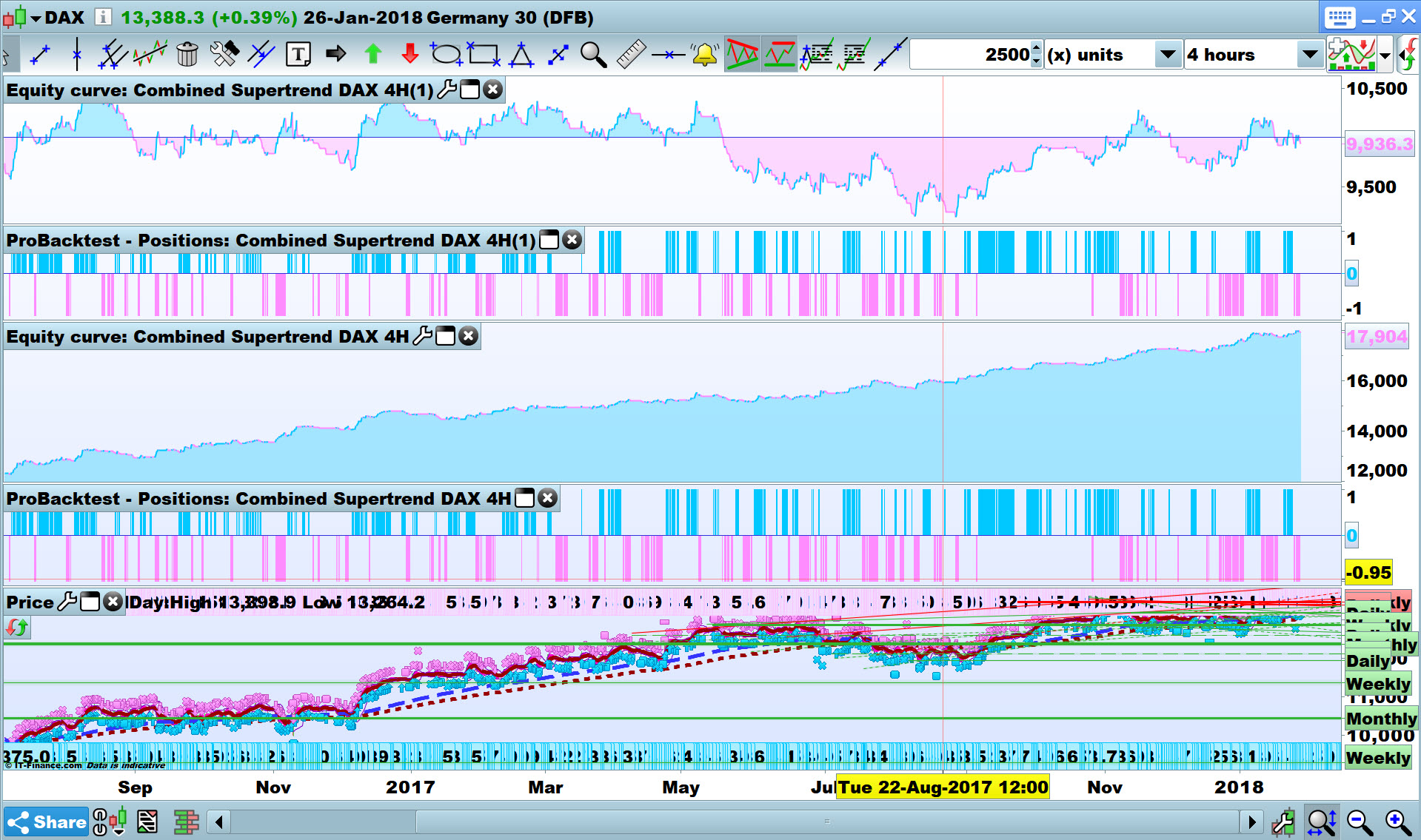

Now look at the result ! 40 Millions out of € 1000 within 8 years, constant growth, almost no drawdown. And all of this by simple combination of 4 different supertrends ! No parameter optimization required anymore, forever !

Lo se, he añadido también un sistema de reinversión pero mi pregunta es…es esto un juego para ver quién consigue el mejor backtest?? de que sirve el backtest si luego realmente no tiene nada que ver con las operaciones en real?..

Se supone que proreatime es una plataforma de pago y debería ser fiable.A mi no me interesa tener un gran backtest, me interesa un backtest modesto pero fiable 100 o 80%…Invertir hors de trabajo para nada la verdad que no es mi idea..

ProRealtime is a mechanical software that does what you tell it to do. Whether it is real or not, is your decision, and you need to check it.

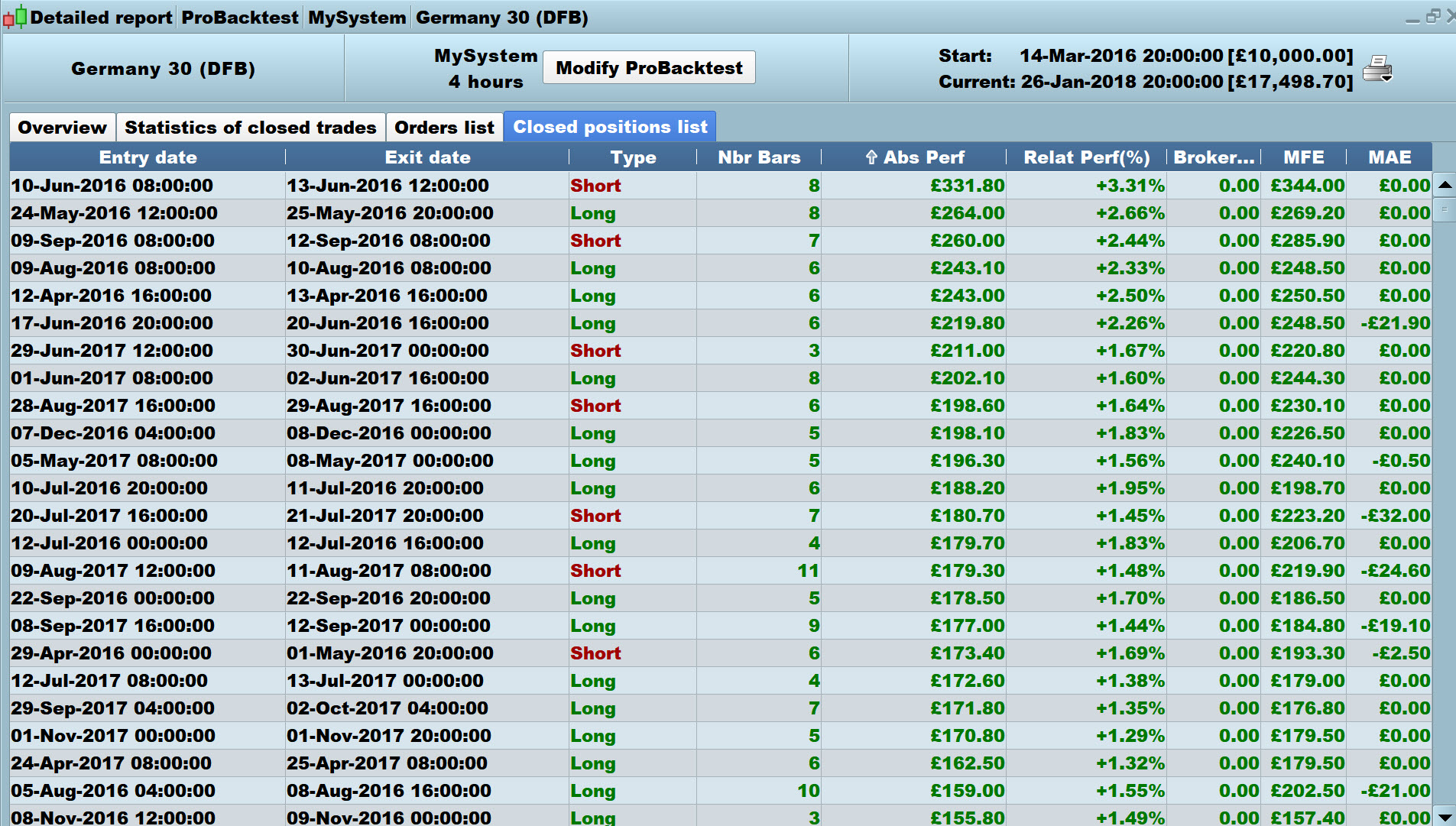

Apologies @Juanan71 for me saying … logically the value TP = 0 is corrupting all the figures … I checked the top 3 profit makers (in the results) as I couldn’t believe there was 0 MAE (maximum adverse excursion). But the figures are correct, all 3 trades opened and took off and never looked back!!! See attached figures and one trade as an example.

I am going to set the Strat going live tomorrow, but only while I am sitting there watching it! 🙂 It be interesting to see how a trade develops!!! I’ll just stop the Strat if it starts losing … I do this all the time anyway on my own Strats! 🙂

I’ll let you know how I get on!!!

GraHal

Warning: Trading may expose you to risk of loss greater than your deposits and is only suitable for experienced clients who have sufficient financial means to bear such risk. The articles, codes and content on this website only contain general information. They are not personal or investment advice nor a solicitation to buy or sell any financial instrument. Each investor must make their own judgement about the appropriateness of trading a financial instrument to their own financial, fiscal and legal situation.

Pero que código estas usando??

I will set Live the code from your post #60713 but with a SL of 55 (your SL value was set at 20).

I anticipate a trade will open then immediately close at a Take Profit of 0 + or – slippage … what else can it do with TP set at 0??

Juanan71 what in your opinion are the exit conditions in your code version?

SELL AT newSL STOP

EXITSHORT AT newSL STOP

do not sell at a difference from the positionprice, but at the exact price given by newSL.

Furthermore, when newSL = 0, these commands are not carried out, because of

IF newSL > 0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

Guys, don’t let yourselves be fooled – there is no money printing machine. Something must be wrong with this system, but I’m too lazy to find out what.

Juanan71 easiest is to type in your native tongue then right click and select translate to english and then copy and paste the english into the comments box.

Oh you need to be using Chrome browser to follow above, but you can also use the Translate button at the top of each page.

There is a simple bug with tp.

tp is always 0 (check by graphing it).

So then the code says all the time :

set target pprofit 0

which, according to the manual, should switch off all target profit orders. However, it does not, and this is where all these fake 0 profit positions come from.

Just leave the

set target pprofit tp

command away (this should not change anything , but it does) , and all the nice profits are gone, too bad…

Does this seem right @nicolas ?

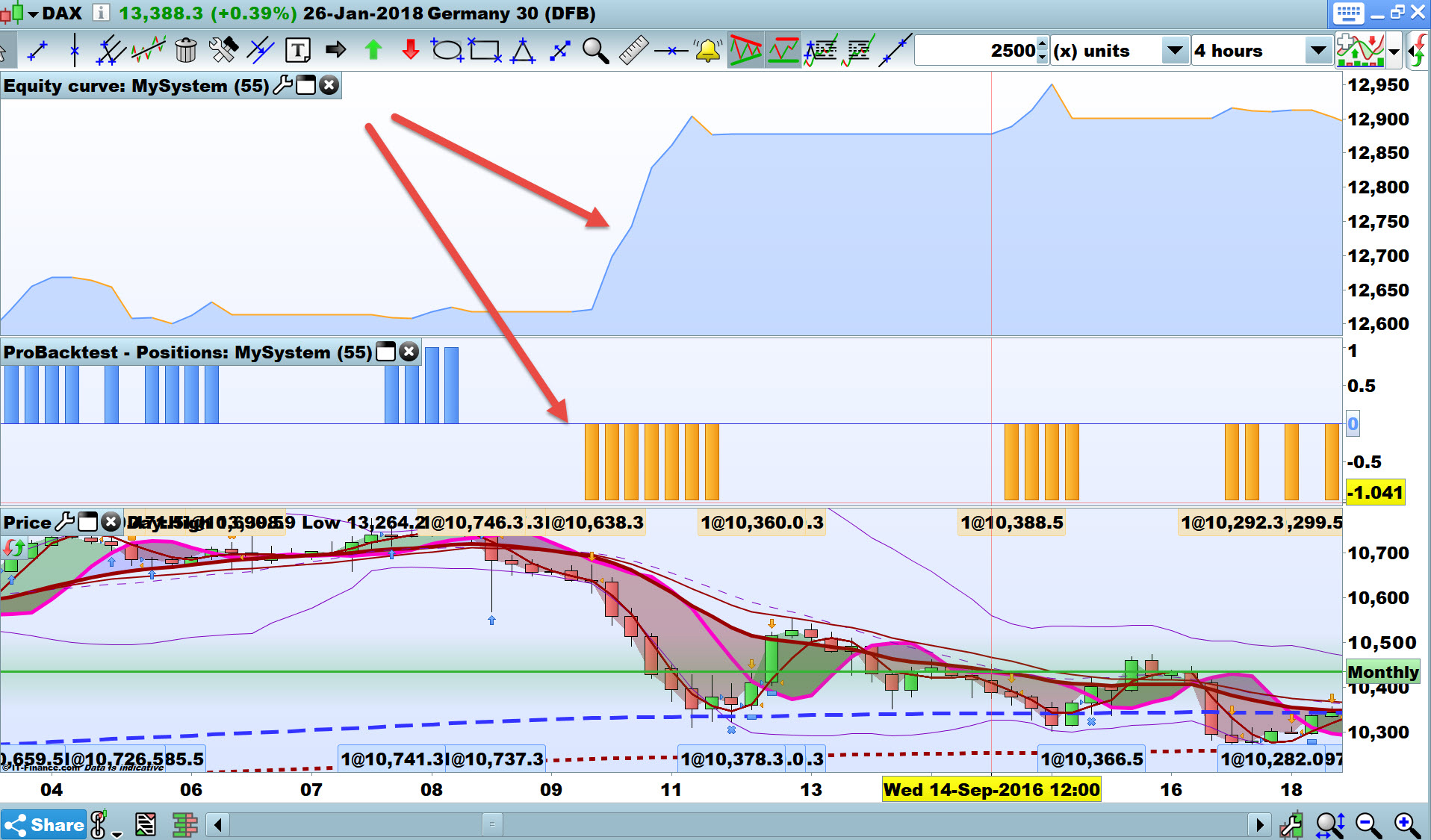

See attached … lower equity curve is with TP = 0 and top curve is with TP commented out. Weird or what??

//set target pprofit TP

Leo

LeoParticipant

Veteran

It isn’t very weird GraHal, thanks for testing it.

I am following this thread and working verdi55 suoertrend simplified.

I found a bit complex to use multiple supertrend of different kinds when we have simplified one done by our colleague.

vendri55 take it easy, once I use a in real money to reinvest the profit of my strategy poisoned for this idea and with 2 wrong trades it consume my profits.

…just tell us if you get millonaire though 😉

Irony is not for everyone. I’d better go to the TV format, then ?