wasn’t this a test version?

Maybe that was why I put ?? in the title.

Wide spread overnight does not necessarily have to be bad thing provided the wide spread is not accompanied by illogical volatility which a System has no chance of predicting?

Spread at 6 overnight may be better compared to 40 to 80 points movement on a 1 min bar when spread is 2.4 and the professionals are tricking / faking us and our Systems into taking the wrong direction!? 🙁

Then 5 mins or so later … oh sorry you’re going the wrong way again now, us pro’s have reversed our positions … you must try and keep up with us if you want to make money!!?? 🙂

Paul

PaulParticipant

Master

after posting ofcouse I see the first line of the code… 🙂

// test trailingstop and breakeven on the dax

indeed high spread doesn’t need to be a bad thing. Looking at barhunter it acts only when the spread is the highest and still it preforms!

About tricking, something to use with barhunter? Maybe there are special times where the markets makes a move to do the opposite? Like before closing or opening, or of other markets? I don’t give it much chance but if it can be coded quick it would be fun to test on a higher timeframe.

PaulParticipant

Master

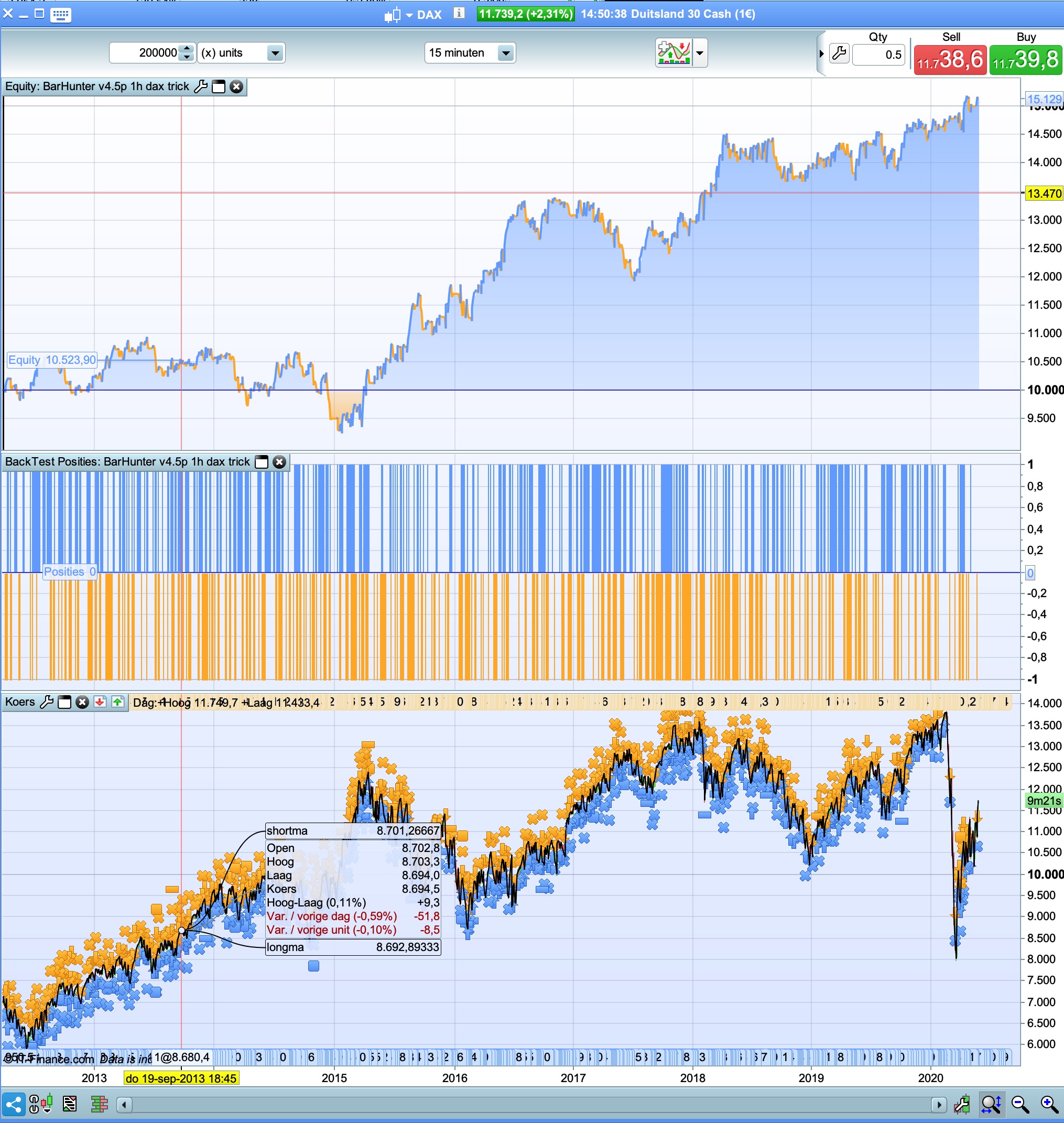

@grahal, there’s a quick try on 15min dax

It searches for the bar(=time) of the crosses from the moving average.

It can then go 1x long and 1x short within the next xx (=4) bars. Max trades is 2 a day. I didn’t look at sl/pt/ts and just took some averages and tested only 15m.

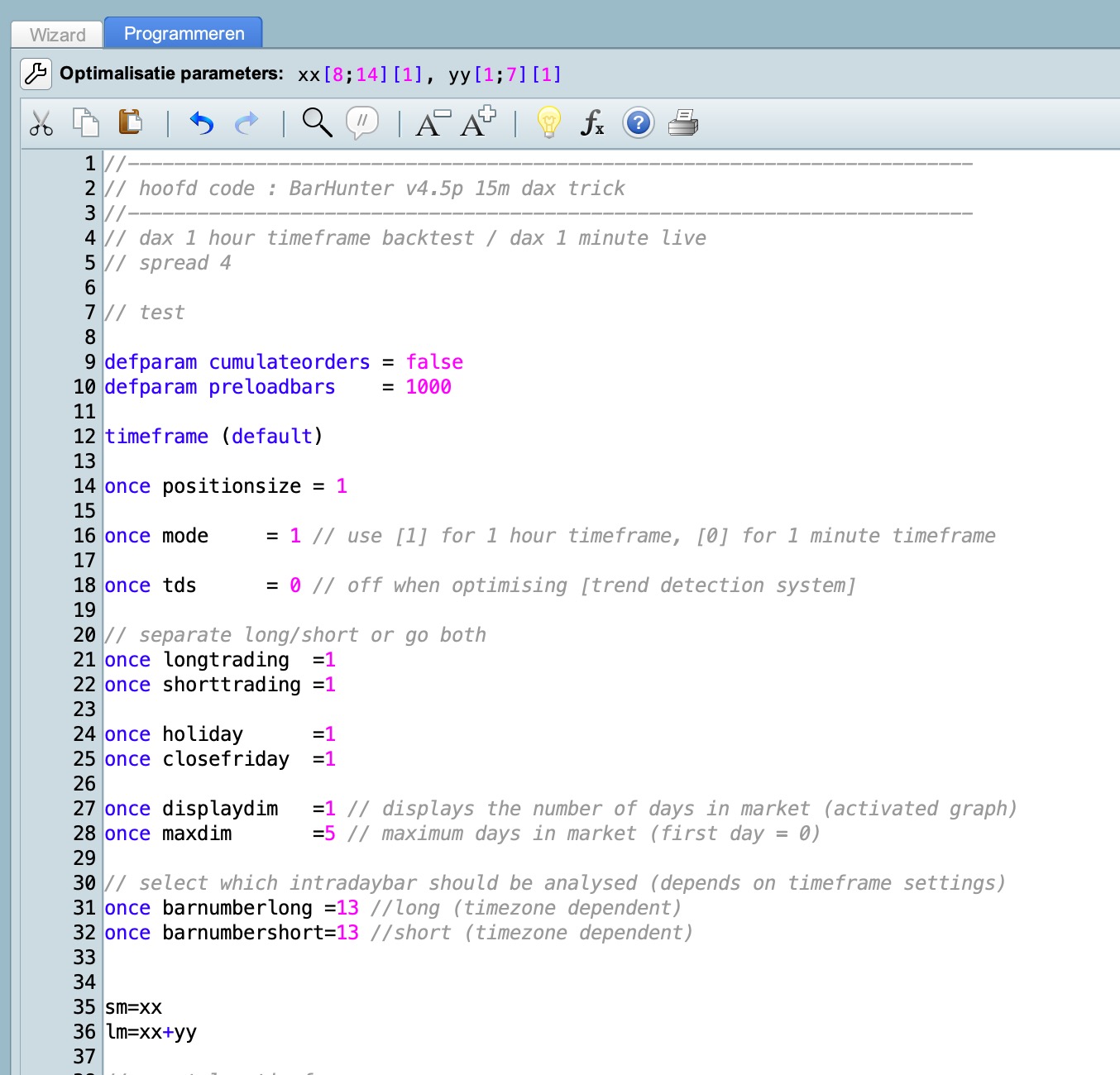

//-------------------------------------------------------------------------

// hoofd code : BarHunter v4.5p 15m dax trick

//-------------------------------------------------------------------------

// dax 1 hour timeframe backtest / dax 1 minute live

// spread 4

// test

defparam cumulateorders = false

defparam preloadbars = 1000

timeframe (default)

once positionsize = 1

once mode = 1 // use [1] for 1 hour timeframe, [0] for 1 minute timeframe

once tds = 0 // off when optimising [trend detection system]

// separate long/short or go both

once longtrading =1

once shorttrading =1

once holiday =1

once closefriday =1

once displaydim =1 // displays the number of days in market (activated graph)

once maxdim =5 // maximum days in market (first day = 0)

// select which intradaybar should be analysed (depends on timeframe settings)

once barnumberlong =13 //long (timezone dependent)

once barnumbershort=13 //short (timezone dependent)

sm=3

lm=15

// reset low timeframe

if intradaybarindex=0 then

tradecounter=0

tradecounterlong=0

tradecountershort=0

tradeday=1

endif

// holiday

if holiday then

if (month = 5 and day = 1) or (month = 12 and day >=24) then

tradeday=0

else

tradeday=1

endif

endif

// set high / low points to break

if longtrading or (longtrading and shorttrading) then

longma = average[lm](close)

shortma = average[sm](close)

endif

if shorttrading or (longtrading and shorttrading) then

longma = average[lm](close)

shortma = average[sm](close)

endif

// trend detection system

if tds=0 then

trendup=1

trenddown=1

else

if tds=1 then

trendup=(average[10](close)>average[10](close)[1])

trenddown=(average[10](close)<average[10](close)[1])

else

if tds=2 then

period= 2

inner = 2*weightedaverage[round( period/2)](typicalprice)-weightedaverage[period](typicalprice)

hull = weightedaverage[round(sqrt(period))](inner)

trendup = hull > hull[1]

trenddown = hull < hull[1]

else

if tds=3 then

period= 2

inner = 2*weightedaverage[round( period/2)](totalprice)-weightedaverage[period](totalprice)

hull = weightedaverage[round(sqrt(period))](inner)

trendup = hull > hull[1]

trenddown = hull < hull[1]

endif

endif

endif

endif

// conditions

condbuy=intradaybarindex >= barnumberlong

condbuy=condbuy and shortma crosses over longma

condbuy=condbuy and trendup

condsell=intradaybarindex >= barnumbershort

condsell=condsell and shortma crosses under longma

condsell=condsell and trenddown

timeframe (default)

// entry criteria

if mode then // mode[1] backtesting on 1 hour timeframe

if tradeday and tradecounter < 100 then

if (longtrading and not shorttrading) or (longtrading and shorttrading) then

if condbuy and tradecounterlong < 1 and (tradecounter<2 and (intradaybarindex < barnumberlong+4)) then

buy positionsize contract at market

tradecounter=tradecounter+1

endif

endif

if (shorttrading and not longtrading) or (longtrading and shorttrading) then

if condsell and tradecountershort < 1 and (tradecounter<2 and (intradaybarindex < barnumbershort+4)) then

sellshort positionsize contract at market

tradecounter=tradecounter+1

endif

endif

endif

else // mode[0] running demo / live on 1 minute timeframe

if tradeday and tradecounter < 1 then

if (longtrading and not shorttrading) or (longtrading and shorttrading) then

if condbuy and tradecounterlong < 1 then

buy positionsize contract at market

tradecounter=tradecounter+1

endif

endif

if (shorttrading and not longtrading) or (longtrading and shorttrading) then

if condsell and tradecountershort < 1 then

sellshort positionsize contract at market

tradecounter=tradecounter+1

endif

endif

endif

endif

//timeframe (1 hour, updateonclose)

// trailing atr stop on high timeframe

once trailingstoptype = 1 // trailing stop - 0 off, 1 on

once trailingstoplong = 5 // trailing stop atr relative distance

once trailingstopshort = 5 // trailing stop atr relative distance

once atrtrailingperiod = 14 // atr parameter value

once minstop = 10 // minimum trailing stop distance

//----------------------------------------------

atrtrail = averagetruerange[atrtrailingperiod]((close/10)*pipsize)/1000

trailingstartl = round(atrtrail*trailingstoplong)

trailingstarts = round(atrtrail*trailingstopshort)

if trailingstoptype = 1 then

tgl =trailingstartl

tgs=trailingstarts

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

maxprice = 0

minprice = close

newsl = 0

endif

if longonmarket then

maxprice = max(maxprice,close)

if maxprice-tradeprice(1)>=tgl*pointsize then

if maxprice-tradeprice(1)>=minstop then

newsl = maxprice-tgl*pointsize

else

newsl = maxprice - minstop*pointsize

endif

endif

endif

if shortonmarket then

minprice = min(minprice,close)

if tradeprice(1)-minprice>=tgs*pointsize then

if tradeprice(1)-minprice>=minstop then

newsl = minprice+tgs*pointsize

else

newsl = minprice + minstop*pointsize

endif

endif

endif

endif

timeframe (default)

// trailing atr stop exits on low timeframe

if longonmarket then

if newsl>0 then

sell at newsl stop

endif

endif

if shortonmarket then

if newsl>0 then

exitshort at newsl stop

endif

endif

// close to reduce risk in the weekend

if closefriday then

if onmarket then

if (dayofweek=5 and hour=22) then

sell at market

exitshort at market

endif

endif

endif

// stoploss & profit target

set target %profit 2

set stop %loss 2

// display days in market

if displaydim then

if (not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket))) then

dim=0

endif

if not ( dayofweek=1 and hour <= 1) then

if onmarket then

if openday <> openday[1] then

dim = dim + 1

endif

endif

endif

if onmarket and dayofweek=1 and hour=1 then

//dim=-1 // shows when position is active on monday first hour

endif

if onmarket and dim>=maxdim then

sell at market

exitshort at market

endif

endif

//graph dim // display days in market

//graphonprice newsl coloured(0,0,255,255) as "trailingstop atr"

//graphonprice breakvaluelong coloured(121,141,35,255) as "breakpoint"

//graphonprice breakvalueshort coloured(121,141,35,255) as "breakpoint"

//graph breakvaluelong coloured(255,0,0,255) as "breakvaluelong"

//graph breakvalueshort coloured(255,0,0,255) as "breakvalueshort"

//graph barindex-tradeindex

//graph intradaybarindex

graphonprice longma

graphonprice shortma

PaulParticipant

Master

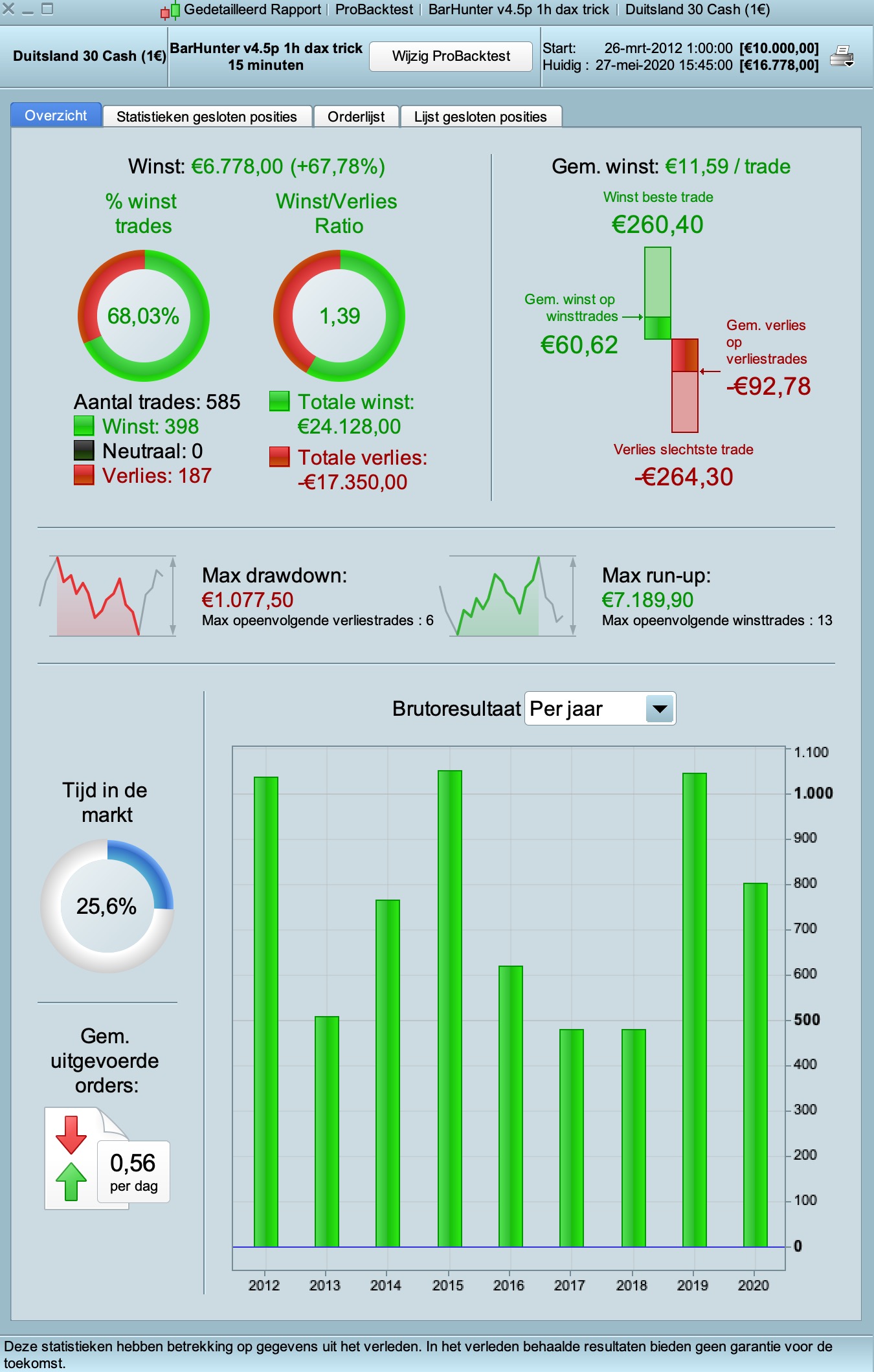

well didn’t expect that!

here’s a new one , same code, change in moving average.

1 month on this one is still doing very good … see attached.

I put the equity curve on 15 mins TF so you could see the steadily increasing equity curve!

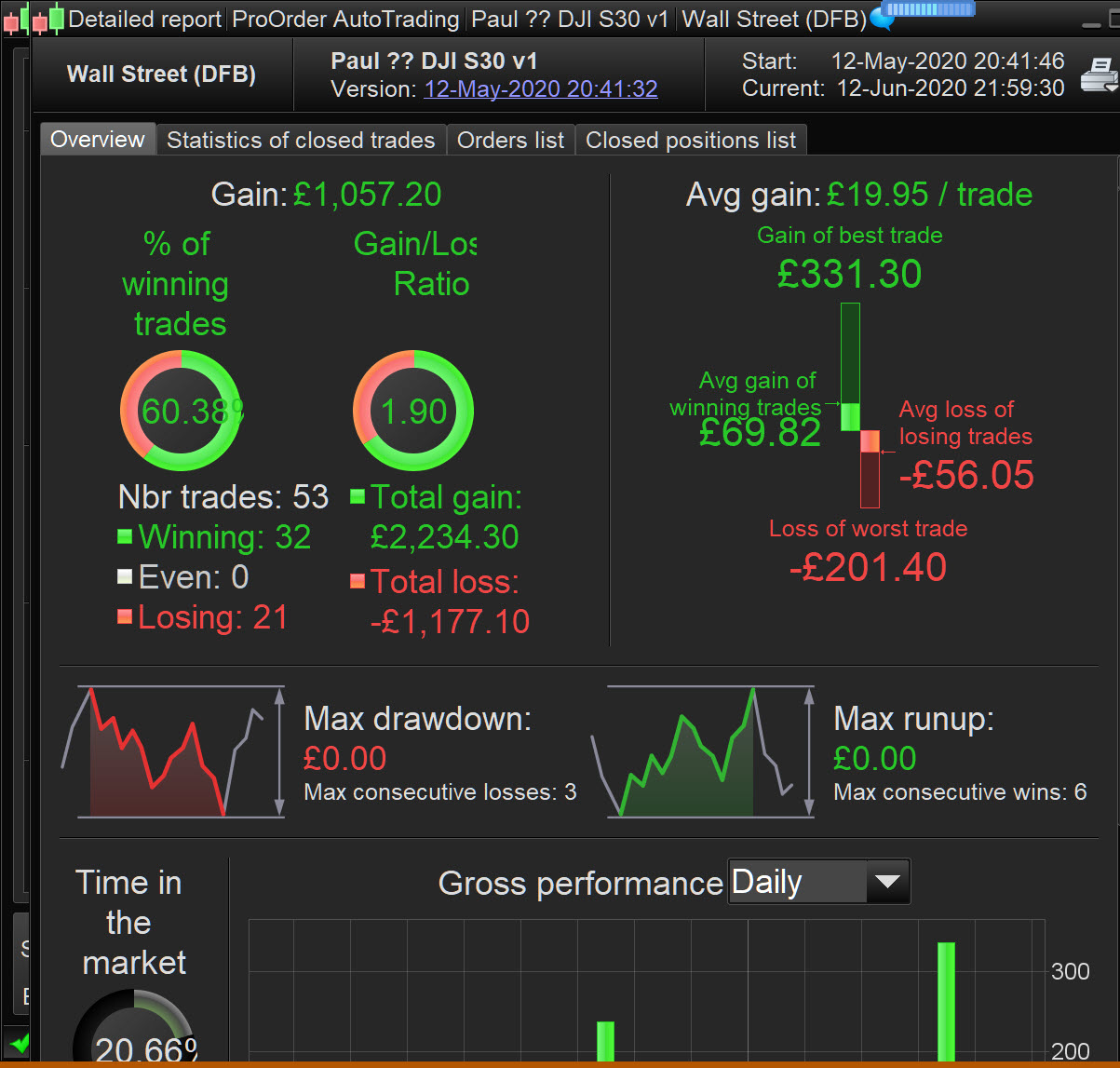

@Paul what lines of code cause most trades to open between 230000 and 240000 (but there a few after 240000 and before 020000)? See Paul 3 to see trade open times.

I did search for time, hour etc. It can’t be coincidence … the time band over which trades open is too regular to be a random occurence??

PaulParticipant

Master

@GraHal That there’s sometimes a trade between 23h-24h could be because of the weekend and how it handles the first hour on monday, perhaps in combination with uk settings? Because the trade is taking on sunday 23h on 31 may & 7 june. Using extra criteria like dayofweek should work to skip those trades on sunday. Nice find btw. Didn’t expect that was necessary!

Hi @GraHal, every time I say ‘no more’ to sub-1m TFs I seem to get drawn back in. It’s all your fault.

Anyway, I did a quick and dirty optimisation and you might want to try the following values:

|

|

SL = 0.75 // % stop loss

PT = 1.50 // % profit target

TS = .3 // % trailing stop

BESG = .15 // % break even stop gain

BESL = 0.00 // % break even stop level

sm = 20

lm = 40

|

Or for a higher win rate, v2

|

|

SL = 0.75 // % stop loss

PT = 1.50 // % profit target

TS = .2 // % trailing stop

BESG = .15 // % break even stop gain

BESL = 0.00 // % break even stop level

sm = 20

lm = 30

|

For it not to have blown up in 14 days of forward testing is good going – maybe it’s a cash cow?

Hi @nonetheless !

Did you continue this strategy ?

I would like to do some test with it but I did’nt find the initial post of it. Can you share these 2 versions please ? 🙂

Thanks in advance,

For it not to have blown up in 14 days of forward testing

Isn’t it 30 full days trading since 12 May?

Enthusiasm gets sapped by keep trying and trying with the same old code / strategy? Variety is the spice of life and sometimes the weirdest stuff works on odd timeframes and / or Instruments?? 🙂

Yeah thanks … I’ll try your settings also.

Hi Guys,

As we can’t do partial exits with IG (Who will be better for trailingstop), did you compare if it’s better to have a trailing stop / Breakeven or to exit all in one time with a R/R of 1/1 or 2/1 for example (No offense of course)

In my experience actually, I don’t have better results with TS/BE but may be I’m wrong

What’s your experience ?

SeeU

PaulParticipant

Master

breakeven I agree fully. Giving higher winchance, but often really small wins. Could better be used i.e. to lower the stoploss in half. Trailingstop is a must for me. Always open for improvements, so let’s see your exit criteria & calculation so I can compare in a strategy!

Hi @Paul

I think we need to use a classical/simple algos code and compare results with and without TS/BE.

If I have time tomorrow I willl do that 😉

SeeU

PaulParticipant

Master

hi zilliq

meantime I wanted to try to have a dynamic pt but stumbled on a problem.

goal is to log the highest mfe for each (long) trade.

second is to have a tradecounterlong

both above are done.

But then I need an average MFE runup based on the highest mfe from each trade. I can’t get through that part.

With average there could be a factor x as profittarget. But how to get an average?

That average could also be used as a dynamic level to activate the trailingstop.

Here’s what I have.

if barindex=0 then

tradecounterlong=0

endif

if not longonmarket then

lbc=0 // long bar counter

endif

if longonmarket then

lbc=lbc+1

hh=highest[lbc](high)

mfe=(round((hh-tradeprice(1)))*pipvalue)

endif

//added tradecounterlong=tradecounterlong + 1 when bought.

//graph tradecounterlong coloured(255,0,0,255)

//graph mfe coloured(0,0,255,255)

to code above could also be added to reset mfe to zero if there short or not onmarket.

any advise here on the average part?

PaulParticipant

Master

test setup dow or dax 1m tf

defparam cumulateorders = false

defparam preloadbars=0

c1=average[60](close)

c2=average[80](close)

condbuy=barindex>100 and c1 crosses over c2

timeframe (5 minutes,updateonclose)

st=supertrend[4,2]

timeframe (default)

condbuy = condbuy and close>st

if barindex=0 then

tradecounterlong=0

endif

if not longonmarket then

lbc=0 // long bar counter

endif

if longonmarket then

lbc=lbc+1

hh=highest[lbc](high)

mfeUP=round((hh-tradeprice(1)))*pipvalue

if mfeUP>0 then

mfelong=mfeUP

else

mfelong=0

endif

else

mfelong=0

endif

//

if condbuy and not longonmarket then

buy 1 contract at market

tradecounterlong=tradecounterlong + 1

endif

set stop ploss 100

set target pprofit 100

mfelong=mfelong

//graph tradecounterlong coloured(255,0,0,255)

graph mfelong coloured(0,0,255,255)

Hi Paul

Why do you want to a high MFE ? (And not a small MAE, or small Max drawdown an so on ) ?

PaulParticipant

Master

Hey Zilliq, This is the first part but goal is to get mfe & mae for long & short separate working. A.t.m. just want to have the calculation right and then later look what’s preferable.

Does it make sense and can it improve a strategy? I don’t know.

But the problem, it needs to take the highest mfe from each long trade, added together and divide that by the amount of long trades. Any ideas? Sounds simple but I can’t find the right way yet!