To continue, because it’s an intersting topic (Thanks @juanj and all contributors), I made a test

I use a very simple code

// Définition des paramètres du code

DEFPARAM CumulateOrders = False // Cumul des positions désactivé

// Conditions pour ouvrir une position acheteuse

indicator1 = ExponentialAverage[a](close)

indicator2 = ExponentialAverage[b](close)

c1 = (indicator1 CROSSES OVER indicator2)

indicator3 = WilderAverage[c](close)

c2 = (close > indicator3)

IF c1 AND c2 THEN

BUY 1 SHARES AT MARKET

ENDIF

// Conditions pour ouvrir une position en vente à découvert

indicator4 = ExponentialAverage[a](close)

indicator5 = ExponentialAverage[b](close)

c3 = (indicator4 CROSSES UNDER indicator5)

indicator6 = WilderAverage[c](close)

c4 = (close < indicator6)

IF c3 AND c4 THEN

SELLSHORT 1 SHARES AT MARKET

ENDIF

// Stops et objectifs

SET TARGET pPROFIT d

SET STOP pLOSS 2*d

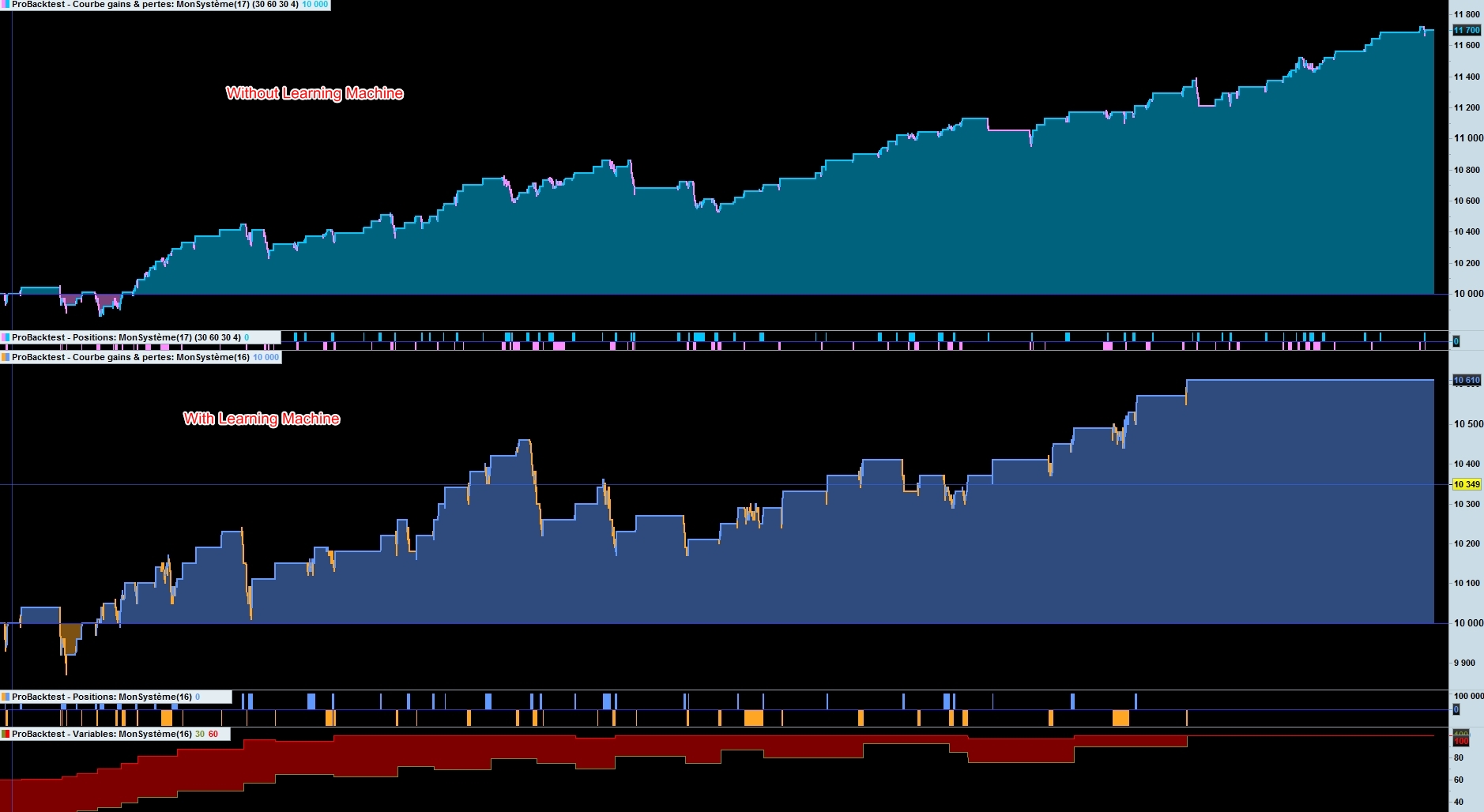

On EUR/USD 1 minute. I do a backtest and obtain the “best” value who are a=30 b=60 c=30 d=4

I put these values in the Learning machine in Starting Value as you can see below with min/max as the values aroud these values on the backtest

defparam cumulateorders = false

//////////////////////////////////////////////////////////////

StartingValue = 30

ResetPeriod = 3 //Specify no of months after which to reset optimization

Increment = 1

MaxIncrement = 20 //Limit of no of increments either up or down

Reps = 3 //Number of trades to use for analysis

MinValue = 10 //Minimum allowed value

MaxValue = 100 //Maximum allowed value

//////////////////////////////////////////////////////////////

StartingValue2 = 60

ResetPeriod2 = 3 //Specify no of months after which to reset optimization

Increment2 = 1

MaxIncrement2 = 20 //Limit of no of increments either up or down

Reps2 = 3 //Number of trades to use for analysis

MinValue2 = 20 //Minimum allowed value

MaxValue2 = 100 //Maximum allowed value

//////////////////////////////////////////////////////////////

//period1=7

//period2=14

HeuristicsCycleLimit = 2

once HeuristicsCycle = 0

once HeuristicsAlgo1 = 1

once HeuristicsAlgo2 = 0

If HeuristicsCycle >= HeuristicsCycleLimit Then

If HeuristicsAlgo1 = 1 Then

HeuristicsAlgo2 = 1

HeuristicsAlgo1 = 0

ElsIf HeuristicsAlgo2 = 1 Then

HeuristicsAlgo1 = 1

HeuristicsAlgo2 = 0

EndIf

HeuristicsCycle = 0

EndIf

//

//If HeuristicsAlgo1 = 1 Then

//Heuristics Algorithm 1 Start

If (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) Then

optimize = optimize + 1

EndIf

If monthinit = 1 or monthinit = 3 or monthinit = 5 or monthinit = 7 or monthinit = 8 or monthinit = 10 or monthinit = 12 Then

MonthDays = 31

ElsIf monthinit = 4 or monthinit = 6 or monthinit = 9 or monthinit = 11 Then

MonthDays = 30

ElsIf monthinit = 2 Then

If (yearinit/4 = round(yearinit/4)) or (yearinit/400 = round(yearinit/400)) Then //haha not sure how exactly to do this

MonthDays = 29 //leap year

Else

MonthDays = 28

EndIf

EndIf

If (month = monthinit and day = dayinit + ResetPeriod) or (month = monthinit + 1 and (day + (MonthDays - dayinit)) >= ResetPeriod) Then

ValueX = StartingValue

WinCountB = 0

StratAvgB = 0

BestA = 0

BestB = 0

dayinit = day

monthinit = month

yearinit = year

EndIf

once ValueX = StartingValue

once PIncPos = 1 //Positive Increment Position

once NIncPos = 1 //Neative Increment Position

once Optimize = 0 ////Initialize Heuristicks Engine Counter (Must be Incremented at Position Start or Exit)

once Mode = 1 //Switches between negative and positive increments

//once WinCountB = 3 //Initialize Best Win Count

//GRAPH WinCountB coloured (0,0,0) AS "WinCountB"

//once StratAvgB = 4353 //Initialize Best Avg Strategy Profit

//GRAPH StratAvgB coloured (0,0,0) AS "StratAvgB"

If Optimize = Reps Then

WinCountA = 0 //Initialize current Win Count

StratAvgA = 0 //Initialize current Avg Strategy Profit

HeuristicsCycle = HeuristicsCycle + 1

For i = 1 to Reps Do

If positionperf(i) > 0 Then

WinCountA = WinCountA + 1 //Increment Current WinCount

EndIf

//StratAvgA = StratAvgA + (((PositionPerf(i)*countofposition[i]*100000)*-1)*-1)

StratAvgA = StratAvgA + (((PositionPerf(i)*pointvalue)*countofposition[i])/pipsize)

Next

StratAvgA = StratAvgA/Reps //Calculate Current Avg Strategy Profit

//Graph (PositionPerf(1)*countofposition[1]*100000)*-1 as "PosPerf1"

//Graph (PositionPerf(2)*countofposition[2]*100000)*-1 as "PosPerf2"

//Graph StratAvgA*-1 as "StratAvgA"

//once BestA = 300

//GRAPH BestA coloured (0,0,0) AS "BestA"

If StratAvgA >= StratAvgB Then

StratAvgB = StratAvgA //Update Best Strategy Profit

BestA = ValueX

EndIf

//once BestB = 300

//GRAPH BestB coloured (0,0,0) AS "BestB"

If WinCountA >= WinCountB Then

WinCountB = WinCountA //Update Best Win Count

BestB = ValueX

EndIf

If WinCountA > WinCountB and StratAvgA > StratAvgB Then

Mode = 0

ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode = 1 Then

ValueX = ValueX - (Increment*NIncPos)

NIncPos = NIncPos + 1

Mode = 2

ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode = 1 Then

ValueX = ValueX + (Increment*PIncPos)

PIncPos = PIncPos + 1

Mode = 1

ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode = 2 Then

ValueX = ValueX + (Increment*PIncPos)

PIncPos = PIncPos + 1

Mode = 1

ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode = 2 Then

ValueX = ValueX - (Increment*NIncPos)

NIncPos = NIncPos + 1

Mode = 2

EndIf

If NIncPos > MaxIncrement or PIncPos > MaxIncrement Then

If BestA = BestB Then

ValueX = BestA

Else

If reps >= 10 Then

WeightedScore = 10

Else

WeightedScore = round((reps/100)*100)

EndIf

ValueX = round(((BestA*(20-WeightedScore)) + (BestB*WeightedScore))/20) //Lower Reps = Less weight assigned to Win%

EndIf

NIncPos = 1

PIncPos = 1

ElsIf ValueX > MaxValue Then

ValueX = MaxValue

ElsIf ValueX < MinValue Then

ValueX = MinValue

EndIF

Optimize = 0

EndIf

// Heuristics Algorithm 1 End

//ElsIf HeuristicsAlgo2 = 1 Then

//Heuristics Algorithm 2 Start

If (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) Then

optimize2 = optimize2 + 1

EndIf

If monthinit2 = 1 or monthinit2 = 3 or monthinit2 = 5 or monthinit2 = 7 or monthinit2 = 8 or monthinit2 = 10 or monthinit2 = 12 Then

MonthDays2 = 31

ElsIf monthinit2 = 4 or monthinit2 = 6 or monthinit2 = 9 or monthinit2 = 11 Then

MonthDays2 = 30

ElsIf monthinit2 = 2 Then

If (yearinit2/4 = round(yearinit2/4)) or (yearinit2/400 = round(yearinit2/400)) Then //haha not sure how exactly to do this

MonthDays2 = 29 //leap year

Else

MonthDays2 = 28

EndIf

EndIf

If (month = monthinit2 and day = dayinit2 + ResetPeriod2) or (month = monthinit2 + 1 and (day + (MonthDays2 - dayinit2)) >= ResetPeriod2) Then

ValueY = StartingValue2

WinCountB2 = 0

StratAvgB2 = 0

BestA2 = 0

BestB2 = 0

dayinit2 = day

monthinit2 = month

yearinit2 = year

EndIf

once ValueY = StartingValue2

once PIncPos2 = 1 //Positive Increment Position

once NIncPos2 = 1 //Neative Increment Position

once Optimize2 = 0 ////Initialize Heuristicks Engine Counter (Must be Incremented at Position Start or Exit)

once Mode2 = 1 //Switches between negative and positive increments

//once WinCountB2 = 3 //Initialize Best Win Count

//GRAPH WinCountB2 coloured (0,0,0) AS "WinCountB2"

//once StratAvgB2 = 4353 //Initialize Best Avg Strategy Profit

//GRAPH StratAvgB2 coloured (0,0,0) AS "StratAvgB2"

If Optimize2 = Reps2 Then

WinCountA2 = 0 //Initialize current Win Count

StratAvgA2 = 0 //Initialize current Avg Strategy Profit

HeuristicsCycle = HeuristicsCycle + 1

For i2 = 1 to Reps2 Do

If positionperf(i) > 0 Then

WinCountA2 = WinCountA2 + 1 //Increment Current WinCount

EndIf

//StratAvgA2 = StratAvgA2 + (((PositionPerf(i)*countofposition[i]*100000)*-1)*-1)

StratAvgA2 = StratAvgA2 + (((PositionPerf(i)*pointvalue)*countofposition[i])/pipsize)

Next

StratAvgA2 = StratAvgA2/Reps2 //Calculate Current Avg Strategy Profit

//Graph (PositionPerf(1)*countofposition[1]*100000)*-1 as "PosPerf1-2"

//Graph (PositionPerf(2)*countofposition[2]*100000)*-1 as "PosPerf2-2"

//Graph StratAvgA2*-1 as "StratAvgA2"

//once BestA2 = 300

//GRAPH BestA2 coloured (0,0,0) AS "BestA2"

If StratAvgA2 >= StratAvgB2 Then

StratAvgB2 = StratAvgA2 //Update Best Strategy Profit

BestA2 = ValueY

EndIf

//once BestB2 = 300

//GRAPH BestB2 coloured (0,0,0) AS "BestB2"

If WinCountA2 >= WinCountB2 Then

WinCountB2 = WinCountA2 //Update Best Win Count

BestB2 = ValueY

EndIf

If WinCountA2 > WinCountB2 and StratAvgA2 > StratAvgB2 Then

Mode = 0

ElsIf WinCountA2 < WinCountB2 and StratAvgA2 < StratAvgB2 and Mode2 = 1 Then

ValueY = ValueY - (Increment2*NIncPos2)

NIncPos2 = NIncPos2 + 1

Mode2 = 2

ElsIf WinCountA2 >= WinCountB2 or StratAvgA2 >= StratAvgB2 and Mode2 = 1 Then

ValueY = ValueY + (Increment2*PIncPos2)

PIncPos2 = PIncPos2 + 1

Mode = 1

ElsIf WinCountA2 < WinCountB2 and StratAvgA2 < StratAvgB2 and Mode2 = 2 Then

ValueY = ValueY + (Increment2*PIncPos2)

PIncPos2 = PIncPos2 + 1

Mode2 = 1

ElsIf WinCountA2 >= WinCountB2 or StratAvgA2 >= StratAvgB2 and Mode2 = 2 Then

ValueY = ValueY - (Increment2*NIncPos2)

NIncPos2 = NIncPos2 + 1

Mode2 = 2

EndIf

If NIncPos2 > MaxIncrement2 or PIncPos2 > MaxIncrement2 Then

If BestA2 = BestB2 Then

ValueY = BestA

Else

If reps2 >= 10 Then

WeightedScore2 = 10

Else

WeightedScore2 = round((reps2/100)*100)

EndIf

ValueY = round(((BestA2*(20-WeightedScore2)) + (BestB2*WeightedScore2))/20) //Lower Reps = Less weight assigned to Win%

EndIf

NIncPos2 = 1

PIncPos2 = 1

ElsIf ValueY > MaxValue2 Then

ValueY = MaxValue2

ElsIf ValueY < MinValue2 Then

ValueY = MinValue2

EndIF

Optimize2 = 0

EndIf

// Heuristics Algorithm 2 End

//EndIf

//c1=average[valuex](close)

//c2=average[valuey](close)

//

//condbuy =c1 crosses over c2 and rsi[14](close)<70

//condsell=c1 crosses under c2 and rsi[14](close)>30

//

//if condbuy then

//buy at market

//endif

//if condsell then

//sellshort at market

//endif

//pp=positionperf(0)*100

//if pp<-0.125 then

//sell at market

//exitshort at market

//endif

//set stop %loss 0.5 // exit sooner on performance criteria above

//set target %profit 0.25

graph valuex coloured(121,141,35,255)

graph valuey coloured(255,0,0,255)

//endif

indicator1 = ExponentialAverage[valuex](close)

indicator2 = ExponentialAverage[valuey](close)

c1 = (indicator1 CROSSES OVER indicator2)

indicator3 = WilderAverage[30](close)

c2 = (close > indicator3)

IF c1 AND c2 THEN

BUY 1 SHARES AT MARKET

ENDIF

// Conditions pour ouvrir une position en vente à découvert

indicator4 = ExponentialAverage[valuex](close)

indicator5 = ExponentialAverage[valuey](close)

c3 = (indicator4 CROSSES UNDER indicator5)

indicator6 = WilderAverage[30](close)

c4 = (close < indicator6)

IF c3 AND c4 THEN

SELLSHORT 1 SHARES AT MARKET

ENDIF

// Stops et objectifs

SET STOP pLOSS 8

SET TARGET pPROFIT 4

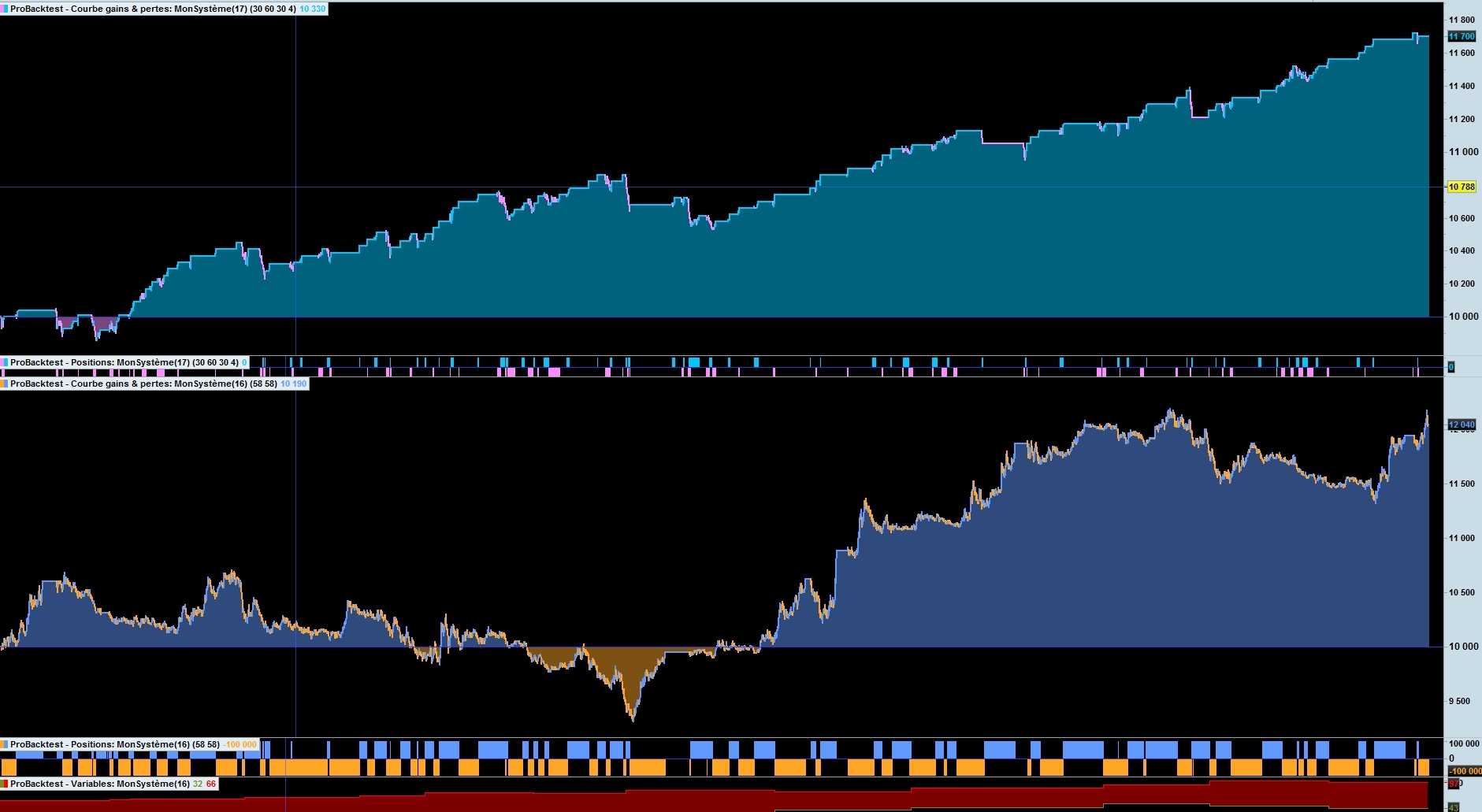

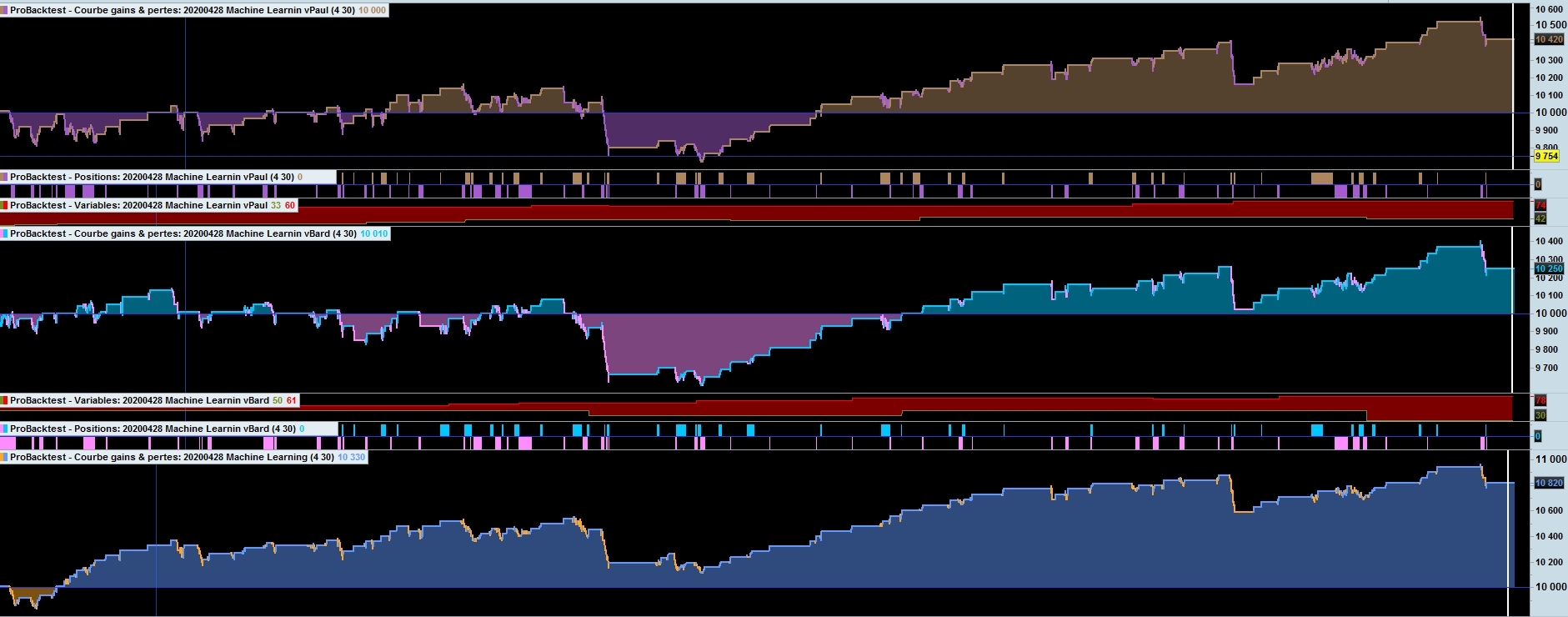

And I compare the results on 2 graph. But sadly the results are worst with the learning machine

Can you test too with this procedure (I think it’s good) on another simple code: Backtest to determine the “best” values to put in starting values and compare

May be it’s the code or me 🙂 but it’s strange the results are worst

See U Coders