Jan

JanParticipant

Veteran

You are invited to comment on the strategy “DI TEMA Trendfollowing strategy on DAX 5 min”

Thank you very much in advance for findings, comments, robustness.

You can find it in the library.

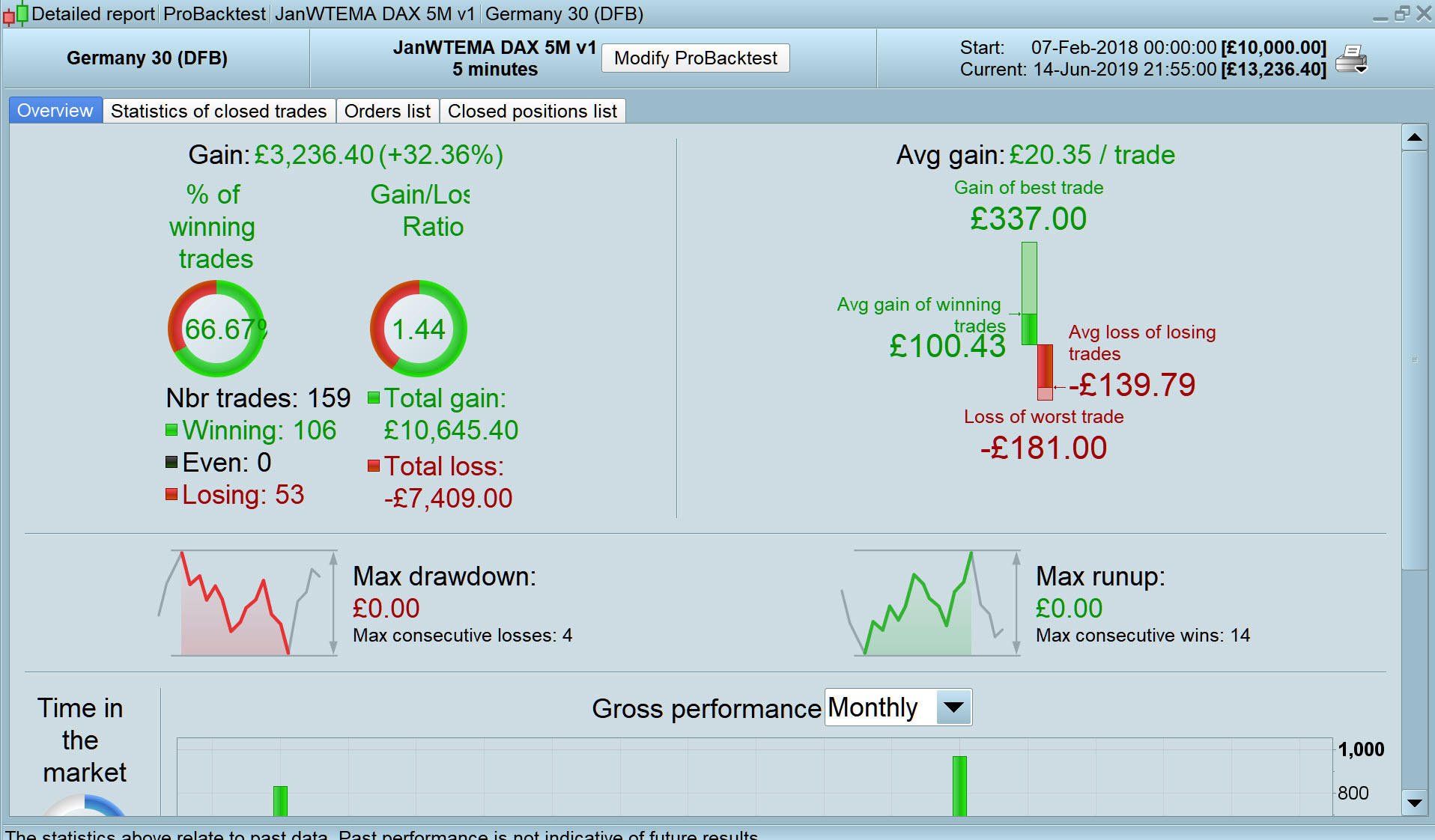

Attached for DAX spread = 2

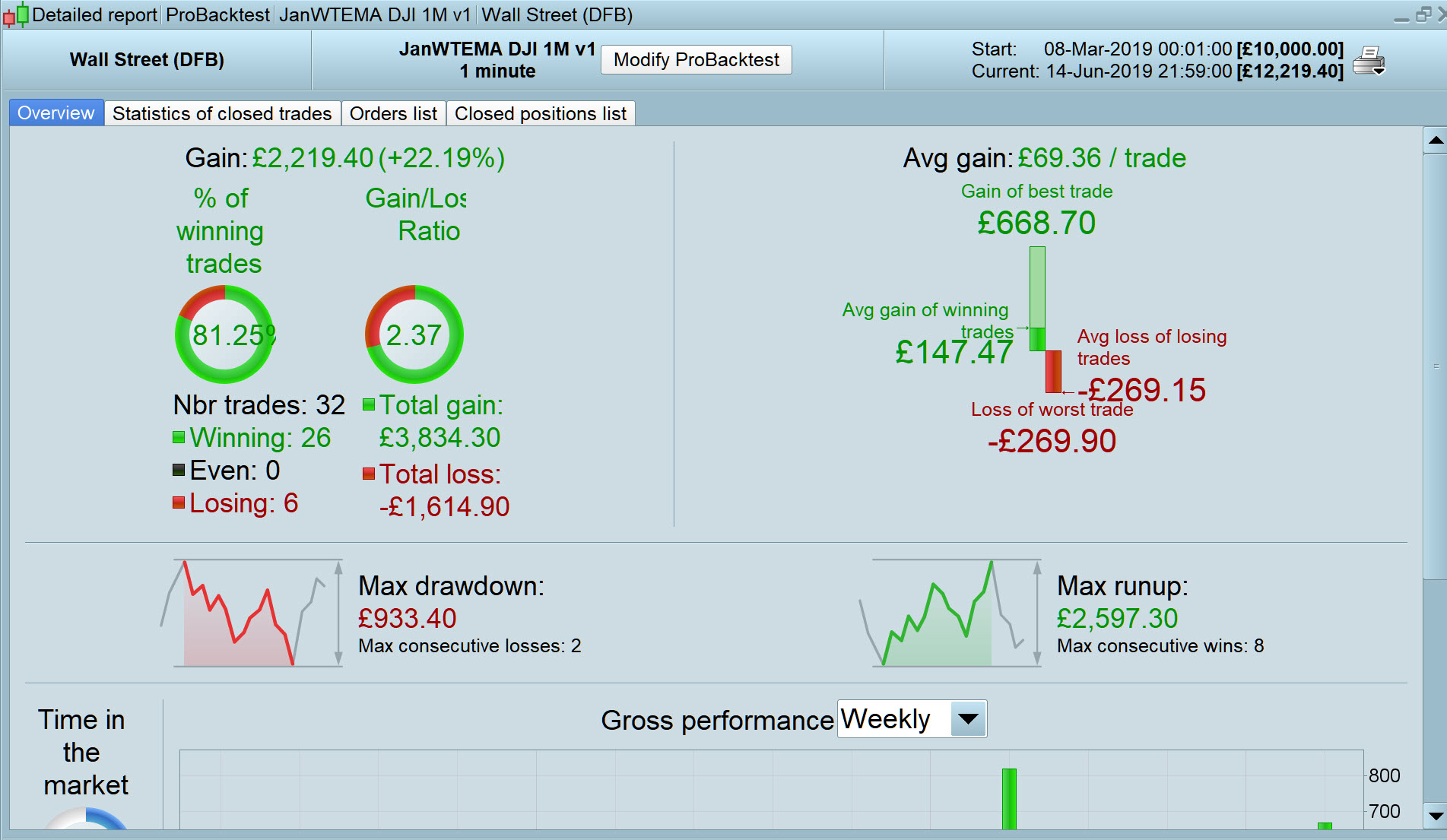

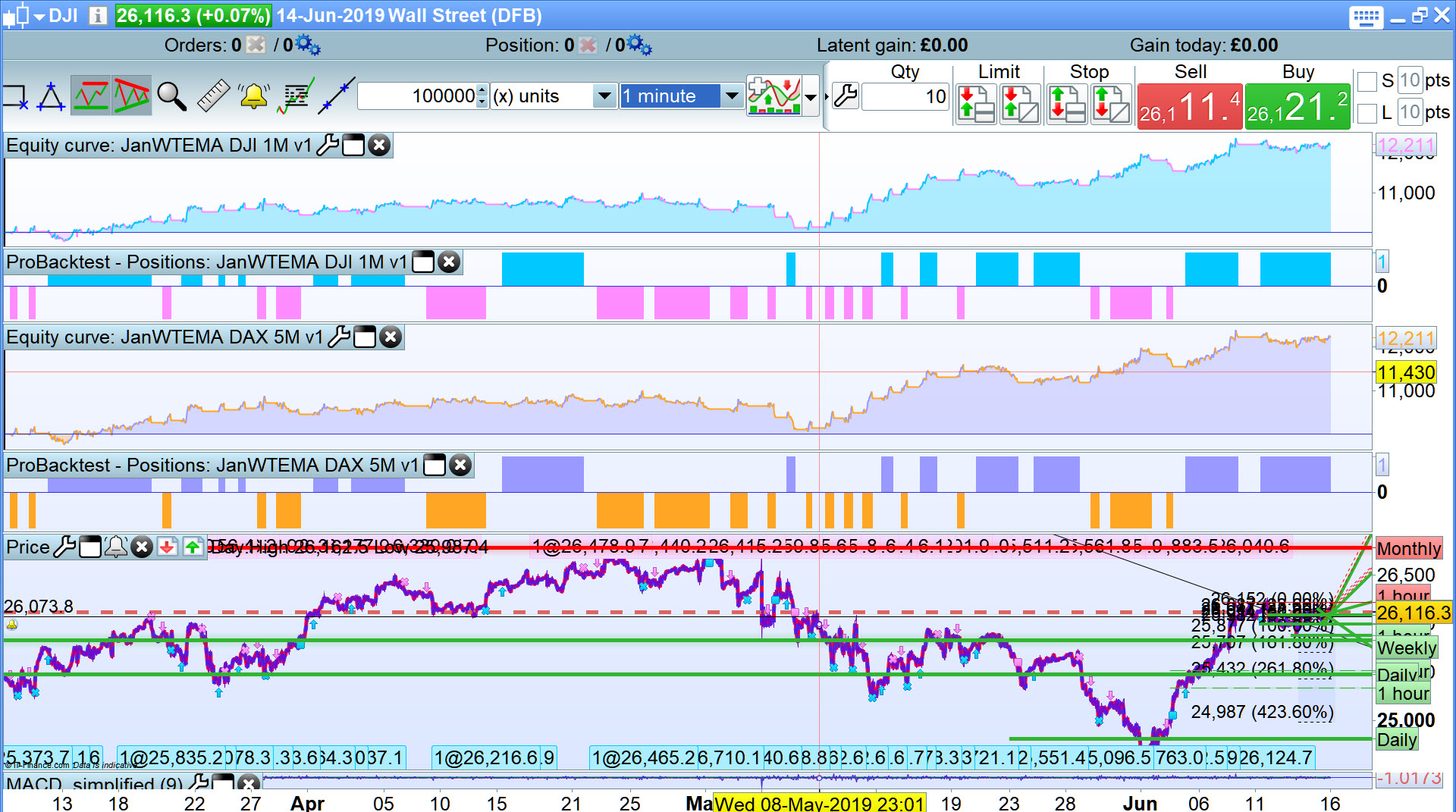

Works even better on DJI 1 min spread = 4

Jan,

thanks for sharing. I played around with time settings but nothing worked.

My results are attached.

/Peter

I’m trying to figure out why leaving out the overnight data makes such a big difference on the outcome as the algo is server side?

I´m using this now with real $ and its working good i use the 30 min chart with settings.

DEFPARAM CumulateOrders = false // Cumulating positions deactivated

//VARIABLES

once SLperc = 105 // Stoploss percentage 105/10000 * Close (150)

once TrailSLPerc = 60 // Trailng Stoploss percentage 85/10000 * Close 60

once Tema2 = 10 // Tema setting for opening long/short positions 10

once DI2 = 7 //DI setting for opening long/short positions 7

once Duration = 12 // number of bars in trade before reducing the trailing stop 12

once Factor = 7/10//factor to reduce trailing stoploss after some time in the trade

once StartE = 74500 //start time for opening positions

once StartL = 103000 //ending time for opening positions (only trading in the morning)

once N = 1 // initieel aantal contracten

OTD = Barindex - TradeIndex(2) > IntradayBarIndex // limits the (opening) trades till 1 per day

kalleklovn – please use the ‘Insert PRT Code’ button to embed code when posting as it makes it much easier for every one to read. I have tidied up your post for you. 🙂

Thanks i´m still new and never really been active on any forums 🙂

@kalleklovn thank you for sharing your settings.

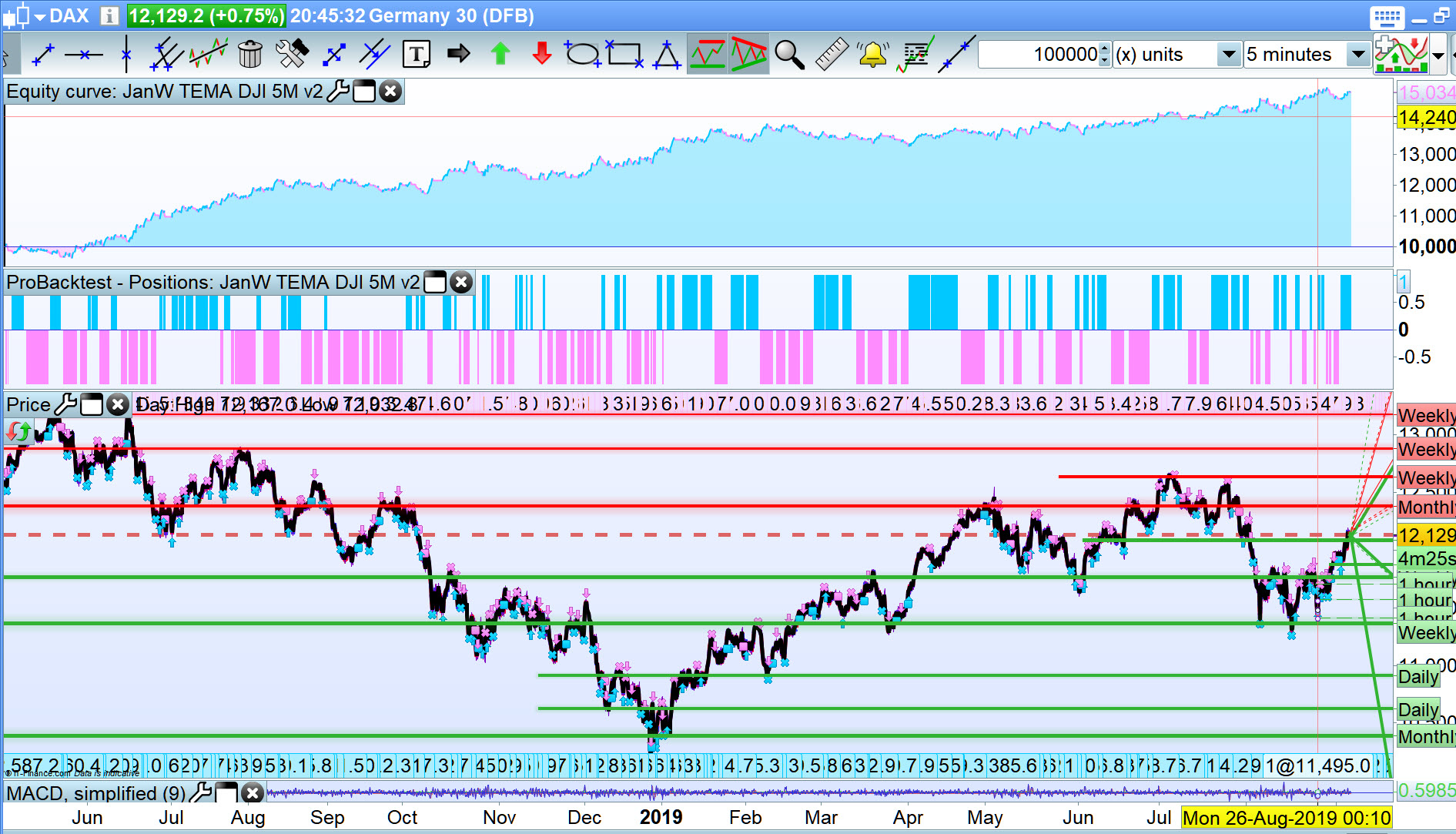

Your share prompted me to look at the 5 min version and I can see that it dropped off in performance after publishing in the library (as so many Systems do).

As seen from attached the drop off just needs a bit of re-opti to get back on track. I found the variables very very responsive!

I’ll try and remember to check the settings regularly! 🙂

Thank you @Jan Wind for sharing this Strategy with us all.

EDIT / PS

The .itf should state DAX (not DJI) … one eye on the TV again, sorry! 🙂

JanParticipant

Veteran

Hello GraHal

“As seen from attached the drop off just needs a bit of re-opti to get back on track. I found the variables very very responsive!

I’ll try and remember to check the settings regularly! 🙂 ”

Do you have any guidelines of re optimizing your auto trading model ? Do you do it every week, and than for 1 year of history for instance ? Or how do you do this ? Re-optimizing implicitly means that you are assuming that the last data gives the best change of predicting future movements. Then a very important question is what is “the best” set of data ?

Kind regards, Jan Wind

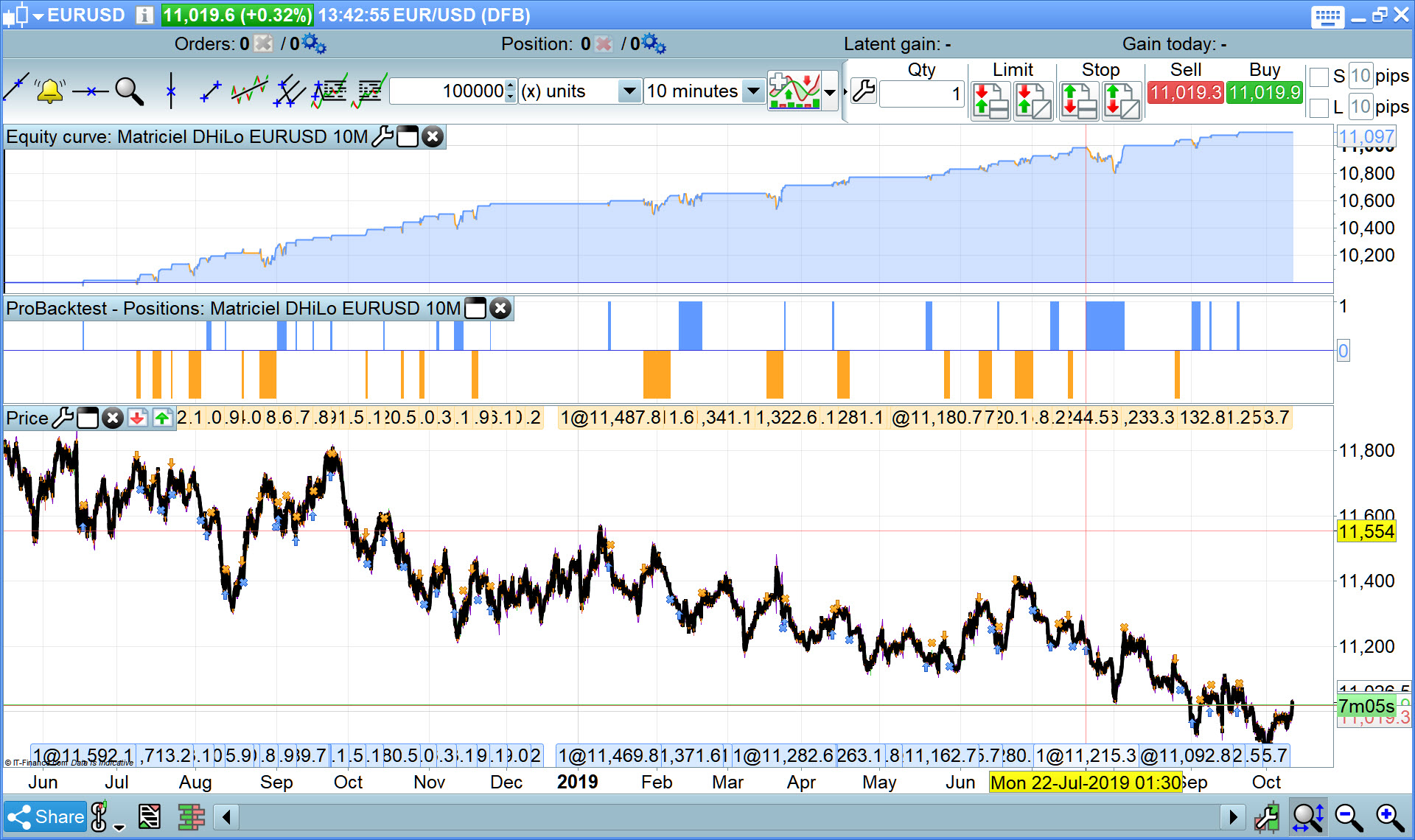

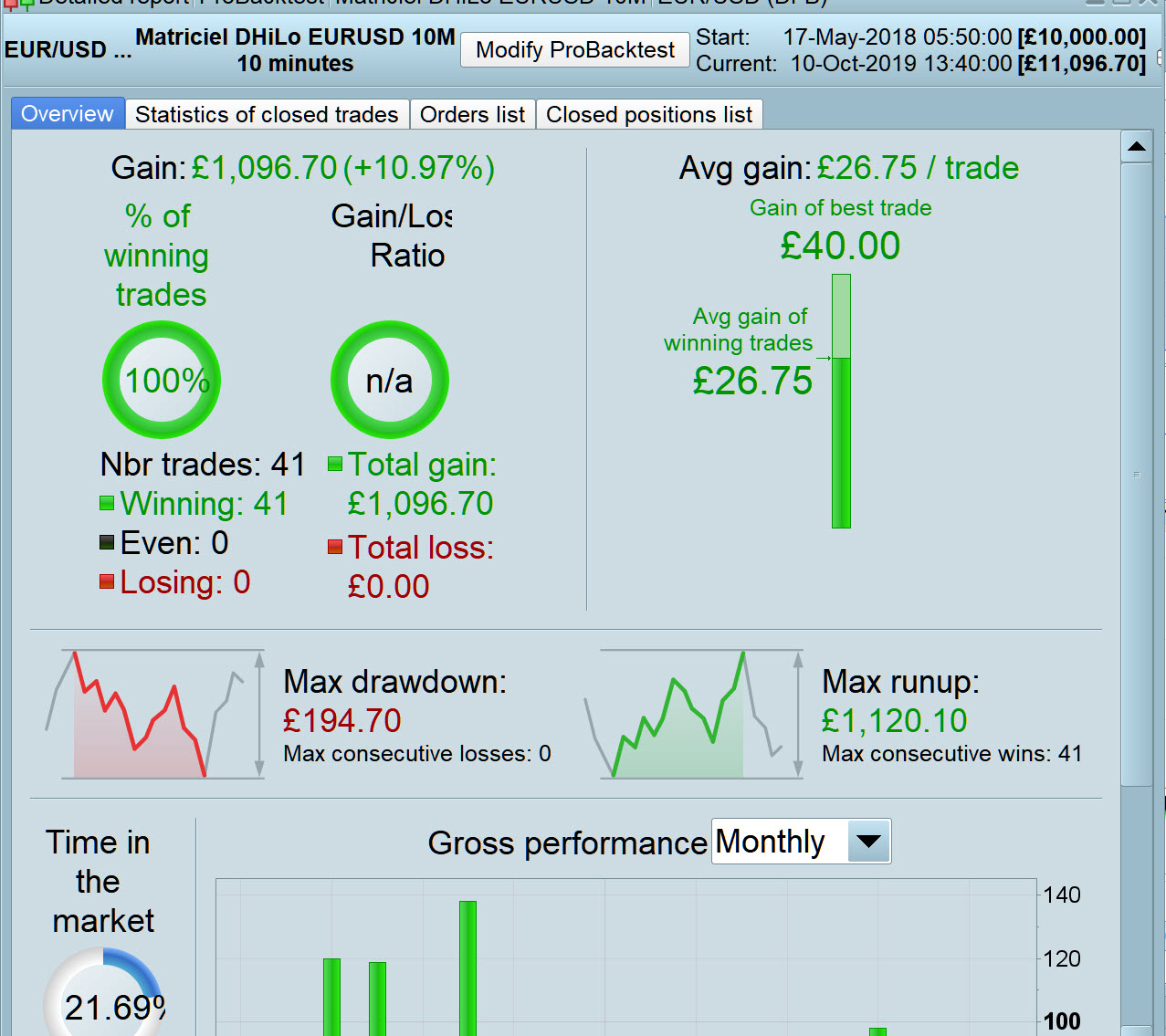

A new strategy for Jan Wind !

Works on EUR/USD 15 minutes timeframe.

DEFPARAM CumulateOrders = True

DEFPARAM PRELOADBARS = 10000

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

Horaire = time >= 000000 and time <= 200000

CloturePartielle = 1// 1 = ON, 0 = OFF

PositionsizeA = 1

PositionsizeV = 1

MAXSHARES = abs(COUNTOFPOSITION) <= 19

IF CloturePartielle THEN

PositionsizeA = 4

PositionsizeV = 3

ENDIF

MM = Average[56,3](totalprice)

Newhighest = max(DHigh(0),DHigh(1))

Newlowest = min(DLow(0),DLow(1))

Milieu = (Newhighest+Newlowest)/2

Surachat = average[10,4]((Newhighest+Milieu)/2)

Survente = average[10,4]((Newlowest+Milieu)/2)

CA = (MM > Surachat) and (close crosses over Milieu)

CV = (MM < Survente) and (close crosses under Milieu)

// Long Entries

IF Horaire AND CA AND MAXSHARES AND not daysForbiddenEntry AND NOT SHORTONMARKET THEN

BUY PositionsizeA CONTRACTS AT MARKET

ENDIF

IF CloturePartielle THEN

IF LONGONMARKET AND COUNTOFLONGSHARES <= 16 THEN

SELL 1 CONTRACTS AT TRADEPRICE + 40*pointsize LIMIT

ENDIF

IF LONGONMARKET AND COUNTOFLONGSHARES <= 4 THEN

SELL 1 CONTRACTS AT TRADEPRICE + 20*pointsize LIMIT

ENDIF

IF LONGONMARKET AND COUNTOFLONGSHARES <= 6 THEN

SELL 1 CONTRACTS AT TRADEPRICE + 18*pointsize LIMIT

ENDIF

ENDIF

IF LONGONMARKET AND summation[35](close < close[6]) = 35 THEN

SELL AT MARKET

ENDIF

// Short Entries

IF Horaire AND CV AND MAXSHARES AND not daysForbiddenEntry AND NOT LONGONMARKET THEN

SELLSHORT PositionsizeV CONTRACTS AT MARKET

ENDIF

IF CloturePartielle THEN

IF SHORTONMARKET AND COUNTOFSHORTSHARES <= 20 THEN

EXITSHORT 1 CONTRACTS AT TRADEPRICE - 78*pointsize LIMIT

ENDIF

IF SHORTONMARKET AND COUNTOFLONGSHARES <= 1 THEN

EXITSHORT 1 CONTRACTS AT TRADEPRICE - 40*pointsize LIMIT

ENDIF

ENDIF

IF SHORTONMARKET AND summation[32](close > close[6]) = 32 THEN

EXITSHORT AT MARKET

ENDIF

//MFE

//trailing stop

trailingstop = 33

//resetting variables when no trades are on market

if not onmarket then

MAXPRICE = 0

MINPRICE = close

priceexit = 0

endif

//case SHORT order

if shortonmarket then

MINPRICE = MIN(MINPRICE,close) //saving the MFE of the current trade

if tradeprice(1)-MINPRICE>=trailingstop*pointsize then //if the MFE is higher than the trailingstop then

priceexit = MINPRICE+trailingstop*pointsize //set the exit price at the MFE + trailing stop price level

endif

endif

//case LONG order

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close) //saving the MFE of the current trade

if MAXPRICE-tradeprice(1)>=trailingstop*pointsize then //if the MFE is higher than the trailingstop then

priceexit = MAXPRICE-trailingstop*pointsize //set the exit price at the MFE - trailing stop price level

endif

endif

//exit on trailing stop price levels

if onmarket and priceexit>0 then

EXITSHORT AT priceexit STOP

SELL AT priceexit STOP

endif

//SET TARGET pPROFIT 46

SET STOP pLOSS 200

Thank you for your excellent work @Matriciel, but as it is a different strategy than this Topic (DI TEMA) would it not be better posted as a separate topic then the Community can easier discuss / comment / improve your strategy?

Not that it needs much improving! 🙂

I reduced to 1 Lot for easier comparison to other Systems, but we can’t do Fwd Test anyway with a strategy that Sells / ExitShort on partial Lot size (as your code does)… it has to be for example Sell at ….

I have enabled tick by tick mode! 🙂

Hi Grahal,

I know this is not the place for this strategy but it was Jan Wind who asked me because I have problems to copy / paste in the subject concerned.