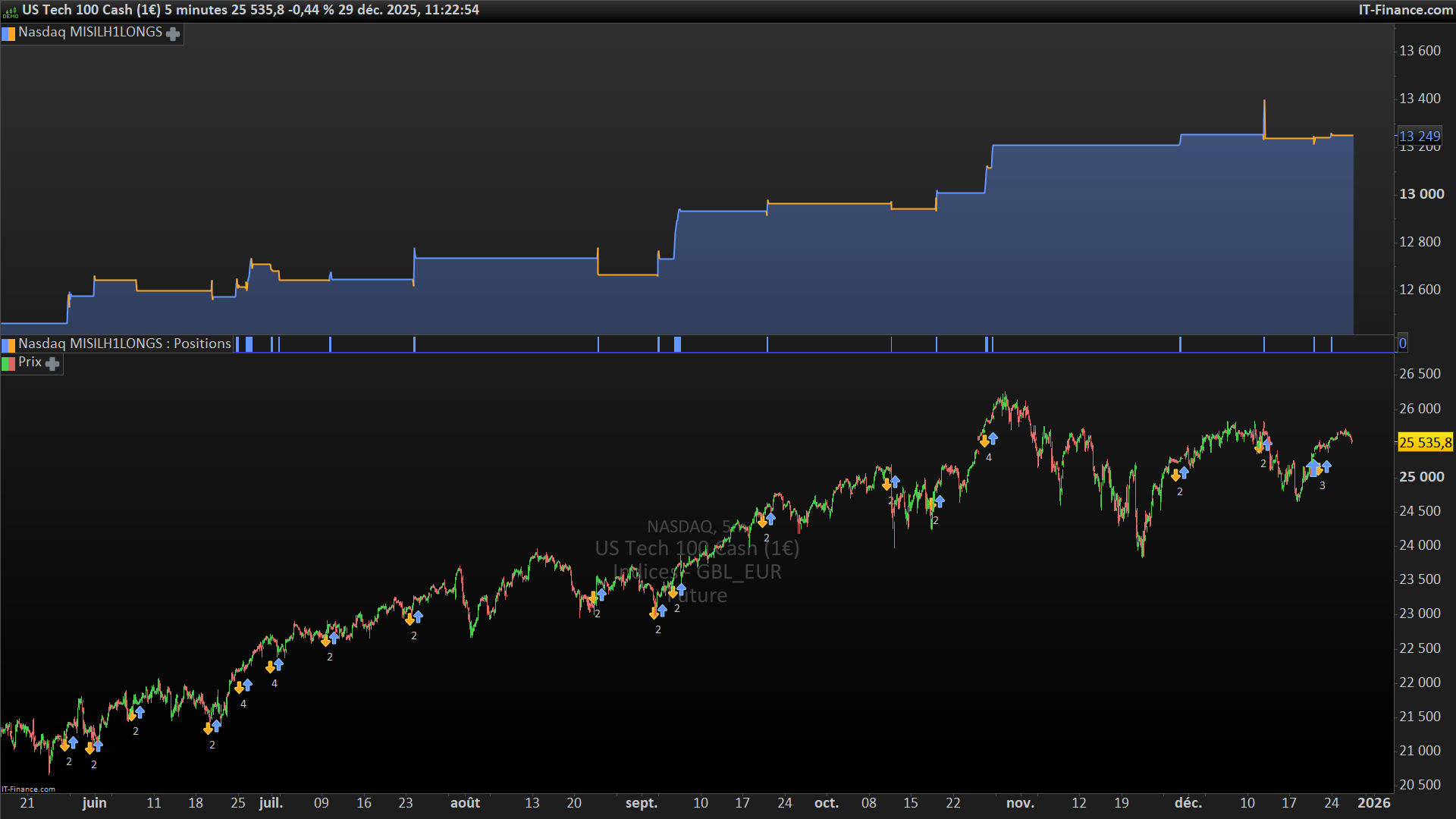

Nasdaq MISILH1LONGS (M5 with H1 context)

{kind=link}

Hello, colleagues! 👋

I have been building automated systems in Prorealtime for some time now, which generate returns for a while and then, like all systems, suffer from Alpha Decay. In my day job, I come from a background in the maintenance of large industrial facilities, where we have successfully implemented predictive maintenance that allows us to keep the facilities operational for longer without failures, achieving greater reliability. I would like to transfer this concept to the portfolio of automated systems. Lately, I have seen videos with interviews with algorithmic traders with accounts funded with €1 million or more. The common pattern among these traders is that they use StrategyQuant to build automated systems with an 80% survival rate over a one-year period, which allows them to have a very robust portfolio of systems and keep it in production for more than six months. During this time, they build new systems that remain in reserve for when one of the robust portfolio systems needs to be replaced. This allows them to remain profitable while some continue to work for others and others devote themselves full time to trading.

I’m afraid that Prorealtime makes it difficult to calculate the survival rate of the systems, so before making the leap to StrategyQuant, I wanted to check with my colleagues to see if there is any way to calculate this rate or even create a working group to see if, between several colleagues, we can come up with a method to increase the robustness of the systems we create.

The idea is to start the consultation and focus it on a very practical question, so I would like to share with you an automatic strategy that I am going to start testing in demo mode for IG’s Nasdaq 1 € while I replicate it for other assets:

// ===================================================================

// ESTRATEGIA: NQ M5 MisilH1longs

// Basado en plantilla OHLC "PDH, PDL, PWH, PWL, maxdia, mindia, maxAsia, minAsia"

// Sistema que abre largo cuando hay vela H1 anterior alcista y la vela H1 actual tiene open-low<2 y el precio cruza al alza el máx H1 de la vela anterior

// Nasdaq 1€

// Autor: Alfonso Diciembre 2025

// Timeframe: M5

// ===================================================================

DEFPARAM CumulateOrders = False

DEFPARAM Preloadbars=1000

positionsize=1

velasanteriores=1

// ===================== MEDIAS DIARIAS / M5 =========================

// Estamos en M5, así que las MAs son sobre M5 (para sistemas que las utilicen)

sma6 = average[6](close)

sma70 = average[70](close)

sma200 = average[200](close)

// Configuración bajista de las medias: 6 < 70 < 200

confMediasBajista = sma6 < sma70 and sma70 < sma200

//Datos PWH y PWL

Timeframe(1week,updateonclose)

PWH = high

PWL = low

Timeframe(default)

// Reset diario para el cálculo del máximo y mínimo del día

timeframe(1hour,updateonclose)

// Mínimo Asia 00:00-09:00 (fijado a las 09:00)

if time = 090000 then

AsiaMin = lowest[9](low)

AsiaMax = highest[9](high)

endif

// DATOS PDH Y PDL del día anterior

If time=000000 then

PDH = highest[24](high)

PDL = lowest[24](low)

Endif

if dayofweek=5 and time=230000 then

PDHV = highest[23](high)

PDLV = lowest[23](low)

Endif

Timeframe(default)

//MÁXIMO Y MÍNIMO DEL DÍA

if intradaybarindex = 0 then

maxdia=0

mindia=30000

orderlongsent = 0

Endif

maxdia=max(maxdia,high)

mindia=min(mindia,low)

// =================== DEFINICIÓN DEL SETUP DE ENTRADA =============

timeframe(1hour,updateonclose)

sma6H1 = average[6](close)

sma70H1 = average[70](close)

sma200H1 = average[200](close)

Alcista=close>SMA6H1//>SMA70H1 and SMA70H1>SMA200H1

MisilH1=0

//Precio H1 por encima de SMA6, vela H1 anterior alcista y vela H1 actual con open-low<2 y precio cruza al alza el máx H1 de la vela anterior

If Alcista and close[1]>open[1] and abs(open-low)<2 and close crosses over high[1] then //

MisilH1=1

SL = low[1]-5

endif

Timeframe(default)

// =================== ENTRADA LARGA =============

if time >=120000 and MisilH1=1 and orderlongsent = 0 then //and alcista = 0

entrylong = close

riskpoints = entrylong-SL

Buy positionsize CONTRACT AT market

SET STOP pLOSS riskpoints

SET TARGET pPROFIT 3 * riskpoints

orderlongsent = 1

endif

// ========== TRAILING MINIMO VELA ANTERIOR CON ACTIVACIÓN =========

// Umbral de activación (en euros)

activationprofit = 100

// Margen bajo el mínimo (en puntos)

buffer = 0

// Variable persistente del stop

IF barindex = 0 THEN

trailstop = 0

ENDIF

IF longonmarket THEN

// Beneficio latente en euros

latentprofit = (close - tradeprice) * positionsize

// Activar trailing solo a partir de +100 €

IF latentprofit >= activationprofit THEN

// Stop propuesto: mínimo de la vela anterior

newstop = low[velasanteriores] - buffer //2

// Inicializar stop

IF trailstop = 0 THEN

trailstop = newstop

ENDIF

// Solo mover el stop a favor

IF newstop > trailstop THEN

trailstop = newstop

ENDIF

// Aplicar stop dinámico

SET STOP pLOSS (close - trailstop)

ENDIF

ELSE

trailstop = 0

ENDIF

// =======================SALIDAS ================

timeframe(1hour,updateonclose)

If longonmarket and close[1]<high[2] and close<open then //

Sell positionsize contract at market

Endif

If longonmarket and close<sma6H1 then //

Sell positionsize contract at market

Endif

If longonmarket and close>positionprice and dayofweek=5 and time=220000 then //

Sell positionsize contract at market

Endif

Timeframe(default)

📌 Strategy summary

• Trade exclusively longs on Nasdaq, with context in H1 and trades in M5.• Trade exclusively longs on Nasdaq, with context in H1 and trades in M5.

• The system opens longs with a previous bullish H1 candle and the current bullish H1 candle, with abs(open-low)<2 in H1 and when the price crosses above the H1 high of the previous candle.

• The SL is a few pips below the H1 low of the previous candle, seeking TP for 3R.

• A trailing stop has been incorporated that is activated from a latent gain of 1R based on the low of the previous M5 candle. It can be optimised.

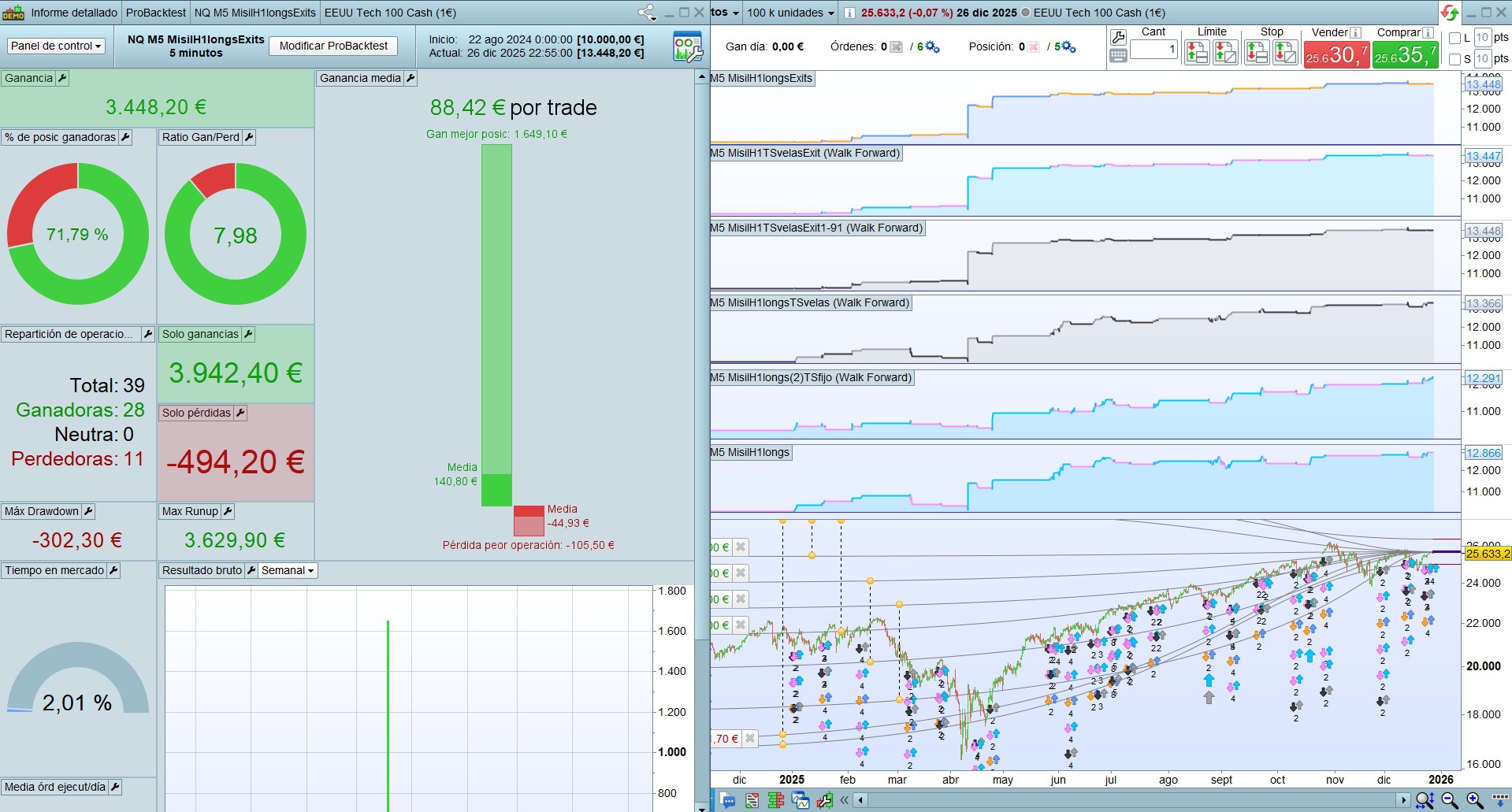

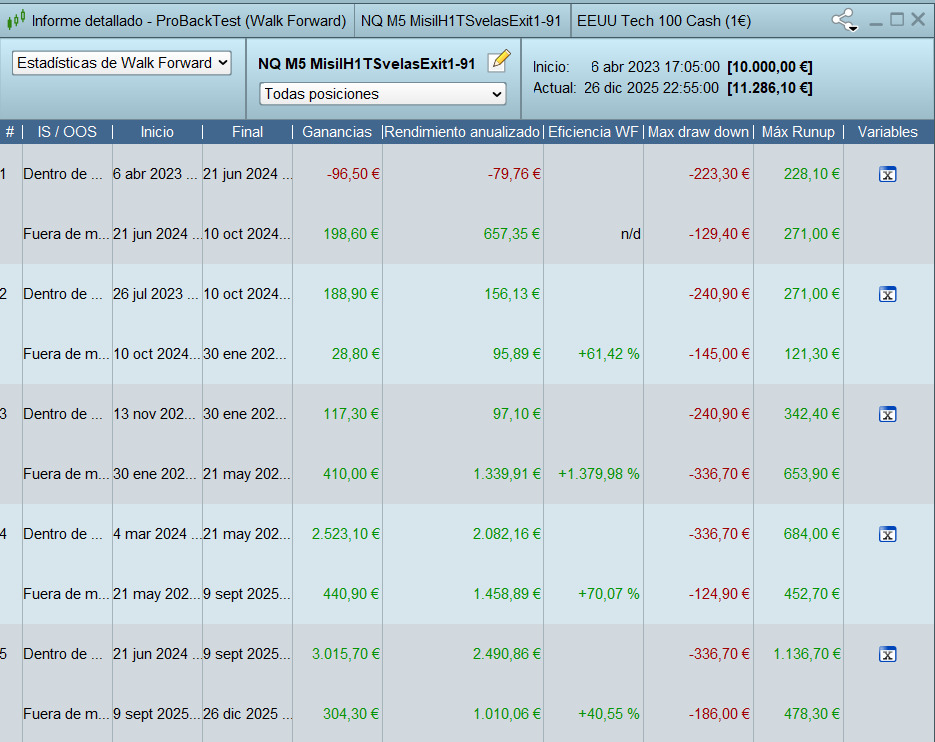

• Results with WF show efficiency in all sections. I have done the Monte Carlo simulation with AI and the results are robust. The parameters are “previous candles” = 1 and “activation profit” = 91 for 100 and 200k.

• I subsequently tried leaving the system with additional exits for cases where the price reverses without reaching 3R, concluding that the backtest results with only the additional exits are similar to the version with trailing.

The system is coded based on a template I use to build systems that calculate OHLC values in PRT to match those of IG: Maxdia, Mindia, PDH, PDL, PWH, PWL, so you will see in the code the calculation of these OHLCs, which are not used later: it is a template for building faster systems based on it.

🔍 What does this strategy offer?

• H1 context for filtering addresses.

• Intraday mechanics with good operational efficiency.

• Reproducible tests for anyone who wants to verify.

📊 Invitation to discuss SURVIVAL RATE / Future robustness

I am publishing this not because it is perfect, but because I want to make it better 🤝.

What I would really like to achieve with this post is to open up a dialogue on something crucial and rarely discussed here: the survival of the strategy in the future.

📌 I ask the experts:

How would you assess the future survival rate of a strategy like this?

I would be particularly interested in:

🔸 Opinions on using Prorealtime to estimate the survival rate of automated strategies and improve the predictive power of automated systems.

🔸 What methods do you use to predict whether a strategy will continue to work in new markets?

🔸 Which metrics do you find most reliable (PF, CAGR, DD, Expectancy, WF Robustness)?

🙌 Final invitation

🔔 If you like this type of intraday development on Nasdaq, comment 👍, contribute your version of the code, or share improvements!

📩 I am willing to collaborate and integrate the best of the community.

I opened a forum topic to discuss about, please fee to join the conversation:

https://www.prorealcode.com/topic/beyond-backtests-long-term-survival-rate-of-automated-strategies-in-prorealtime/

Best regards.

Alfonso

{kind=link}

{kind=link}