japan 225 cash 1 h

February 21, 2022, 8:39 AM

Strategies

31 Comments

{kind=link}

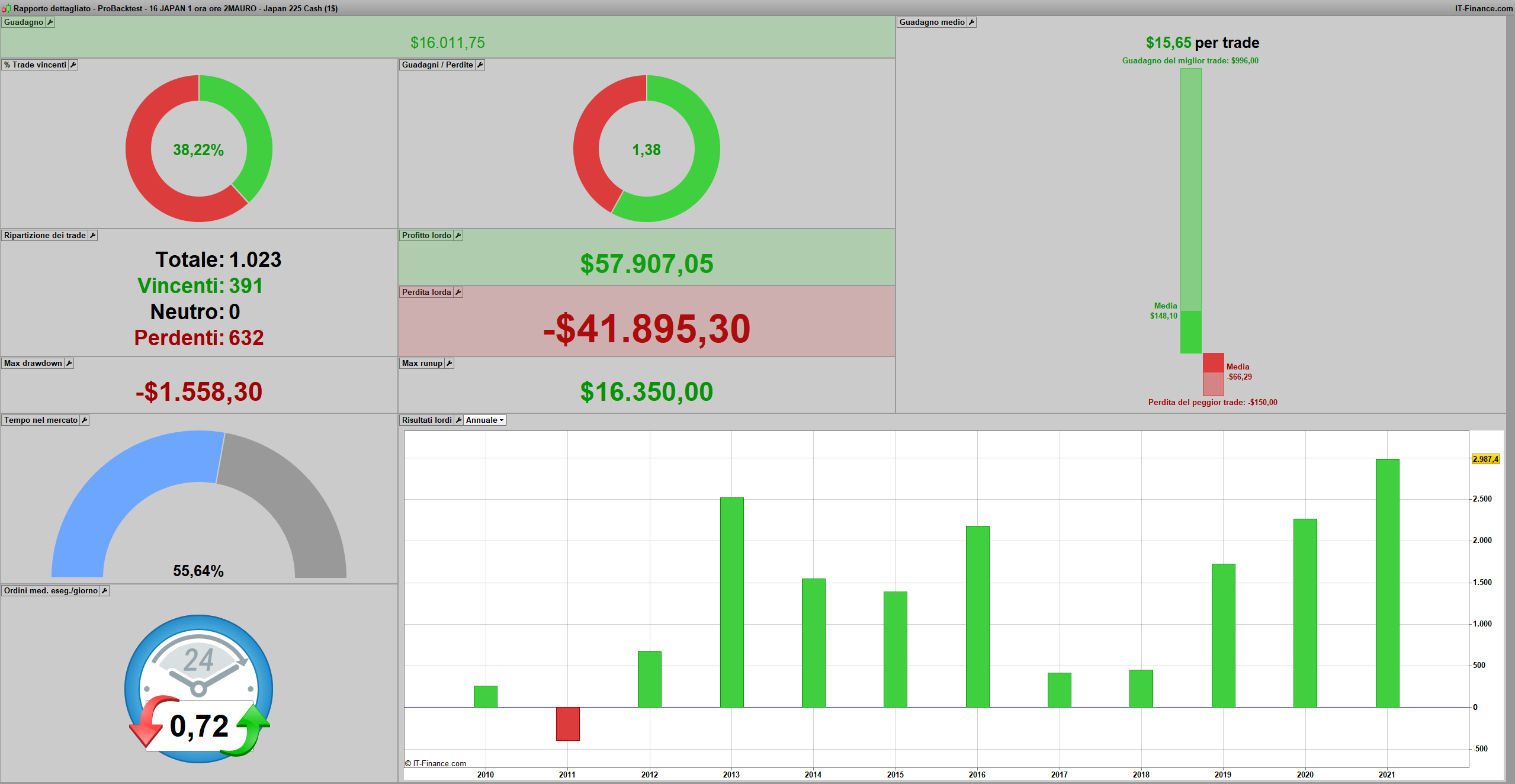

I share this simple strategy with the forum. i put spread 9 against the spread of 7 at 2 am. has been running on the demo for months with positive results. if you come up with something to improve it, contact me. Thank you

Defparam cumulateorders = false

DEFPARAM PreLoadBars = 100000000

n = 0.50

PERIODO= TIME=020000

if longonmarket then

sell at CLOSE-(CLOSE*0.010) STOP //0.012

ENDIF

IF SHORTONMARKET THEN

EXITSHORT AT CLOSE+(CLOSE*0.0081) STOP //0.0077

ENDIF

// STOP LOSS & TAKE PROFIT (%)

SL = 0.815 //0.85

TP = 7 //7

//MARGINE = 300

// LONGS & SHORTS : every day except Fridays

// entre StartTime et EndTime

if PERIODO and dayOfWeek <> 5 AND CLOSE[4]<OPEN[4] AND abs(CLOSE[4]-OPEN[4])>10 then //12

buy n shares at CLOSE+(CLOSE*0.000001) limit //0.000003

endif

if PERIODO and dayOfWeek <> 5 AND CLOSE[4]>OPEN[4] AND abs(CLOSE[4]-OPEN[4])>10.50 then

SELLSHORT n shares AT CLOSE+(CLOSE*0.00003) limit //0.00003

endif

// Stop Loss & Take Profit

set stop %loss SL

set target %profit TP

// Exit Time

Download

Filename:

japan-225-cash-1-h.itf

Downloads:

333

Average

This author is like an anonymous function, present but not directly identifiable. More details on this code architect as soon as they exit 'incognito' mode.

Author’s Profile

Loading...