GBPJPY breakout strategy

November 30, 2017, 8:20 AM

Strategies

0 Comments

{kind=link}

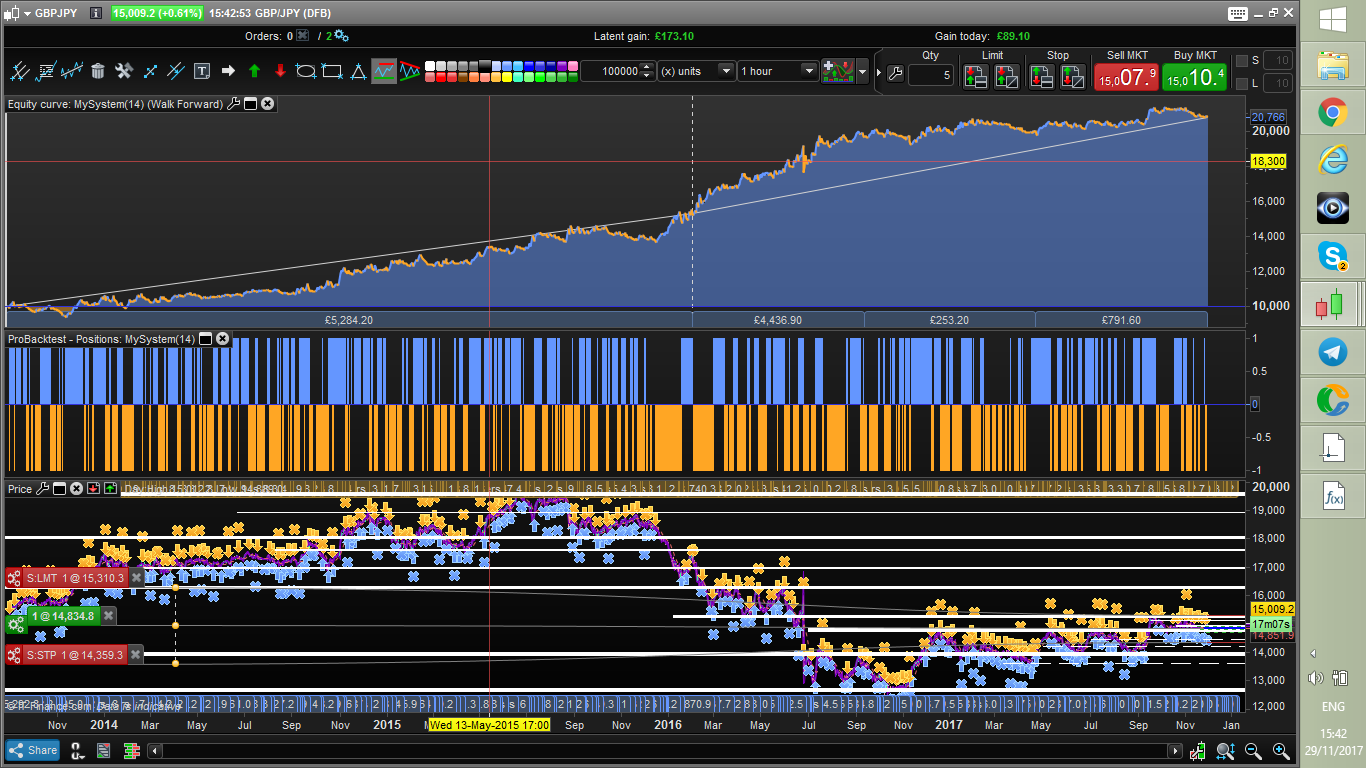

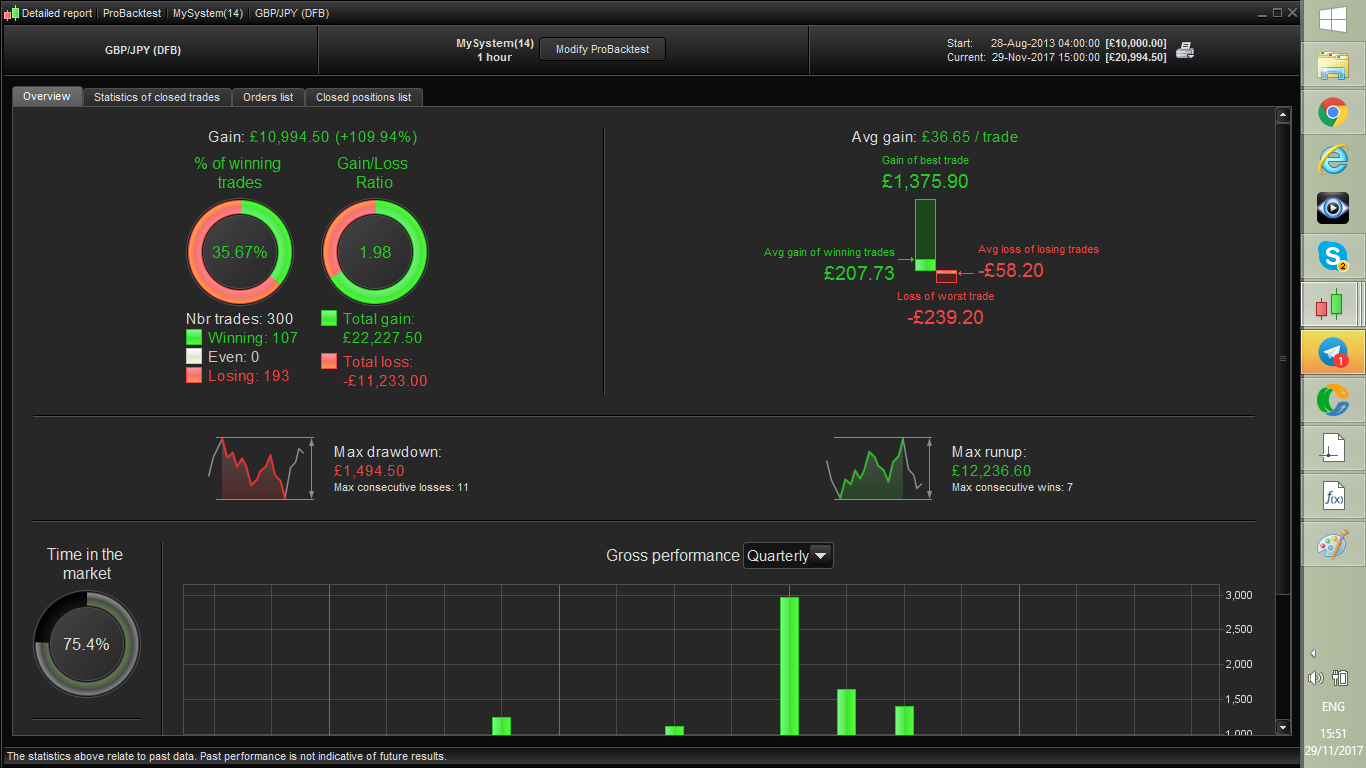

Hello everyone. This strategy is the inverse of the mean reverting strategy on sp 500 I posted some time ago. It waits for candle who open and close above/below the bollinger bands to enter in the same direction. 2 parameter are optimized. Walk Forward analysis is attached.

//-------------------------------------------------------------------------

// Main code : meanreverting_boll_gbpjpy

//-------------------------------------------------------------------------

// Definition of code parameters

DEFPARAM CumulateOrders = False // Cumulating positions deactivated

//optimized parameters

bollingerperiod = 30

exitaverageperiod = 120

///trend indicator

fastavperiod = 10

slowavperiod = 100

slowav = average[slowavperiod](close)

fastav = average[fastavperiod](close)

// Conditions to enter long/short positions

bollup = BollingerUp[bollingerperiod](close)

bolldown = BollingerDown[bollingerperiod](close)

cl = (close >= bollup)

cl = cl AND (open >= bollup)

cl = cl and close >max(fastav,slowav)

cs = (close <= bolldown)

cs = cs AND (open <= bolldown)

cs = cs and close <min(fastav,slowav)

IF cl THEN

buy 1 PERPOINT AT MARKET

ENDIF

if cs then

sellshort 1 perpoint at market

endif

// Conditions to exit long/short positions

exitaver = Average[exitaverageperiod](close)

c1 = (close CROSSES under exitaver)

c2 = (close CROSSES over exitaver)

IF c1 and longonmarket THEN

sell AT MARKET

ENDIF

if c2 and shortonmarket then

exitshort at market

endifHope you will like it.

Download

{kind=link}

Filename:

gbpjpy_stat.png

Downloads:

414

Download

Filename:

gbpjpy_breakout_bollinger.itf

Downloads:

509

Master

Code artist, my biography is a blank page waiting to be scripted. Imagine a bio so awesome it hasn't been coded yet.

Author’s Profile

Loading...