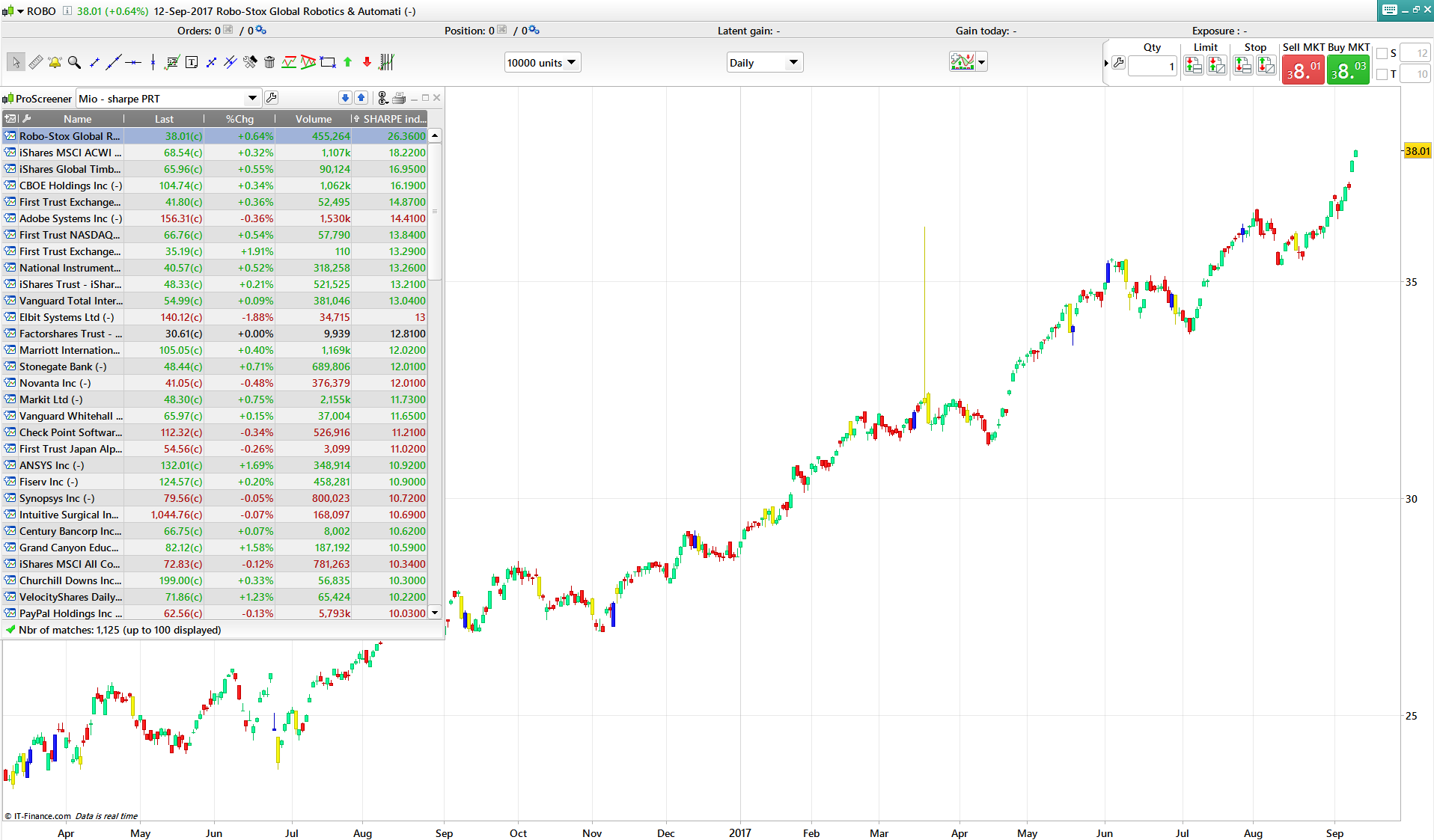

Modified Sharpe index screener

September 13, 2017, 11:15 AM

Screeners

15 Comments

{kind=link}

This screener uses a modified Sharpe index to identify stocks with a strong momentum. The rules are as follows:

1. screen the markets and select the strongest 20-30 stocks (the first stocks on the screener are the strongest)

2. buy those stocks position-sizing them based on the Yhang-Zhan variation of Garman-Klass volatility (indicator I posted previously) :

3. after 3 months run the same procedure and get rid of the stocks that are out of the first tier of the list and get the new entries

OR

3. hold the stocks for 1 year and then sell.

I’ve been using this portfolio for 6 years now and the average gain of the folio was excellent for me. You can improve the profit by buying at the SMA60 point.

Blue skies!!

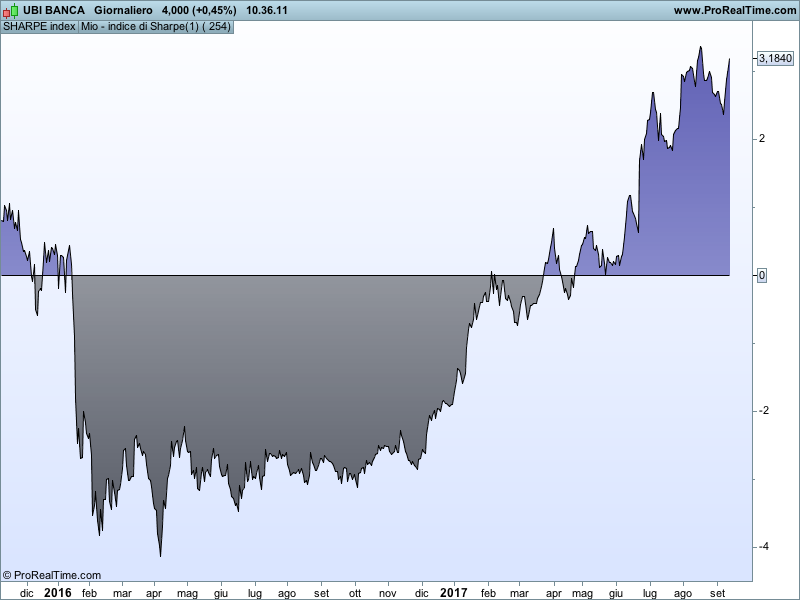

//computation of return and volatility on annual bases

periodo=254

RitMensNoRiskTitle=0

a=log(close/close[1])

b=summation[periodo](a)

s=sqrt(254)*std[periodo](a)

//computation of modified Sharpe index

sharpe=(b-RitMensNoRiskTitle/100)/(s*s)

//launch of screener

c1 = (sharpe > 0)

SCREENER[c1] (sharpe AS "SHARPE index")

Download

Filename:

Mio-sharpe-PRT.itf

Downloads:

267

Download

{kind=link}

Filename:

sharpe-15052918214cpl8.png

Downloads:

131

Master

This author is like an anonymous function, present but not directly identifiable. More details on this code architect as soon as they exit 'incognito' mode.

Author’s Profile

Loading...