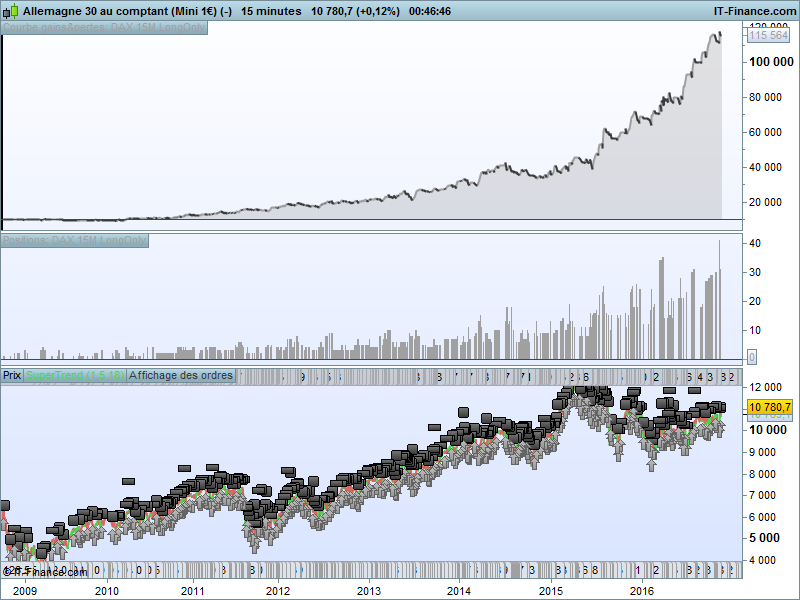

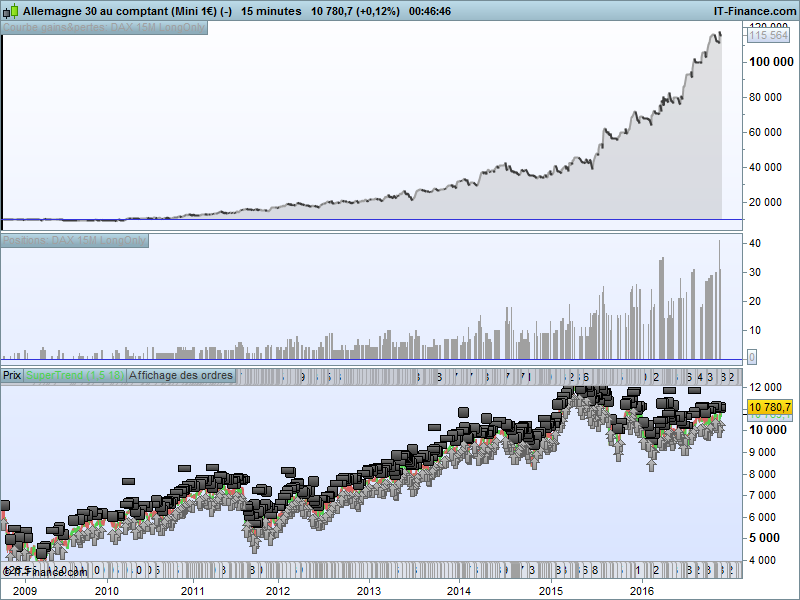

DAX 15Min - False Breakout / SuperTrend

November 16, 2016, 10:12 AM

Strategies

20 Comments

{kind=link}

Hi everyone,

First I’d like to thank you all for your contribution on this website. It’s been a goldmine for me so far 😉

You all found good names for your strategies but to be honest I haven’t find mine yet..

Anyway, here is the thing:

- Index: Dax 1€

- TF: 15M

- $Risk: You choose ! 😉 – 1.5% of capital per trade in my backtest. Up to 3.7% due to seasonality (Thanks ALE for your piece of code about seasonality)

- Spread: 2 pips

Variables were optimized different ways. Optimization from the beggining of PRT datas to 31/12/13 shows substantially the same trend. I hope my curve remains not so fitted..

Drawbacks:

- Not so many trades

- Several trades could last a very long time

- Time between trades is also too long

- The reverse short strategy does not lead to gains..

Thus, if you have any comments, ideas or anything that could improve this strategy, it would be really appreciated ! 😉

Thank you all and keep posting interesting things here, I like it !

Maxime

DEFPARAM CumulateOrders = false

//DAX - 15M

sl=80

tp=150

p=18

d=20

m=1.5

Rg = 0.5

ONCE Januaryl = 1

ONCE Februaryl = 2

ONCE Marchl = 3

ONCE Aprill = 1

ONCE Mayl = 1

ONCE Junel = 2

ONCE Julyl = 3

ONCE Augustl = 1

ONCE Septemberl = 1

ONCE Octoberl = 1

ONCE Novemberl =2

ONCE Decemberl = 2

ONCE Monday = 2

ONCE Tuesday = 2

ONCE Wednesday = 1

Once Thursday = 1

Once Friday = 1

Once Saturday = 1

Once Sunday = 1

If Opendayofweek = 1 then

DayMult = Monday

ElsIf Opendayofweek = 2 then

DayMult = Tuesday

ElsIf Opendayofweek = 3 then

DayMult = Wednesday

ElsIf Opendayofweek = 4 then

DayMult = Thursday

ElsIf Opendayofweek = 5 then

DayMult = Friday

ElsIf Opendayofweek = 6 then

DayMult = Saturday

ElsIf Opendayofweek = 7 then

DayMult = Sunday

Endif

// saisonal pattern long position

IF CurrentMonth = 1 THEN

saisonalPatternMultiplierl = Januaryl

ELSIF CurrentMonth = 2 THEN

saisonalPatternMultiplierl = Februaryl

ELSIF CurrentMonth = 3 THEN

saisonalPatternMultiplierl = Marchl

ELSIF CurrentMonth = 4 THEN

saisonalPatternMultiplierl = Aprill

ELSIF CurrentMonth = 5 THEN

saisonalPatternMultiplierl = Mayl

ELSIF CurrentMonth = 6 THEN

saisonalPatternMultiplierl = Junel

ELSIF CurrentMonth = 7 THEN

saisonalPatternMultiplierl = Julyl

ELSIF CurrentMonth = 8 THEN

saisonalPatternMultiplierl = Augustl

ELSIF CurrentMonth = 9 THEN

saisonalPatternMultiplierl = Septemberl

ELSIF CurrentMonth = 10 THEN

saisonalPatternMultiplierl = Octoberl

ELSIF CurrentMonth = 11 THEN

saisonalPatternMultiplierl = Novemberl

ELSIF CurrentMonth = 12 THEN

saisonalPatternMultiplierl = Decemberl

ENDIF

aMax = Highest[d](High)

aMin = Lowest[d](Low)

SupTnd = SuperTrend[m,p]

RngOk = (High-Low)/(aMax-aMin)<Rg

Equity = 10000+StrategyProfit

Risk = 0.015

n = Max(1,Equity*Risk/Sl/PipValue*SQRT(DayMult*saisonalPatternMultiplierl))

//n=1

cBuy = aMin[1]<aMin[2] And High<aMax[1] And Close>Open And RngOk And Close>SupTnd

If cBuy Then

Buy n Shares at Market

EndIf

SET STOP ploss sl

SET TARGET pPROFIT tp

Download

Filename:

WF_Dax.xlsx

Downloads:

176

Download

{kind=link}

Filename:

Equity_Curve.png

Downloads:

241

Download

Filename:

Resume.pdf

Downloads:

339

Download

Filename:

DAX-15M-LongOnly.itf

Downloads:

847

New

I usually let my code do the talking, which explains why my bio is as empty as a newly created file. Bio to be initialized...

Author’s Profile

Loading...