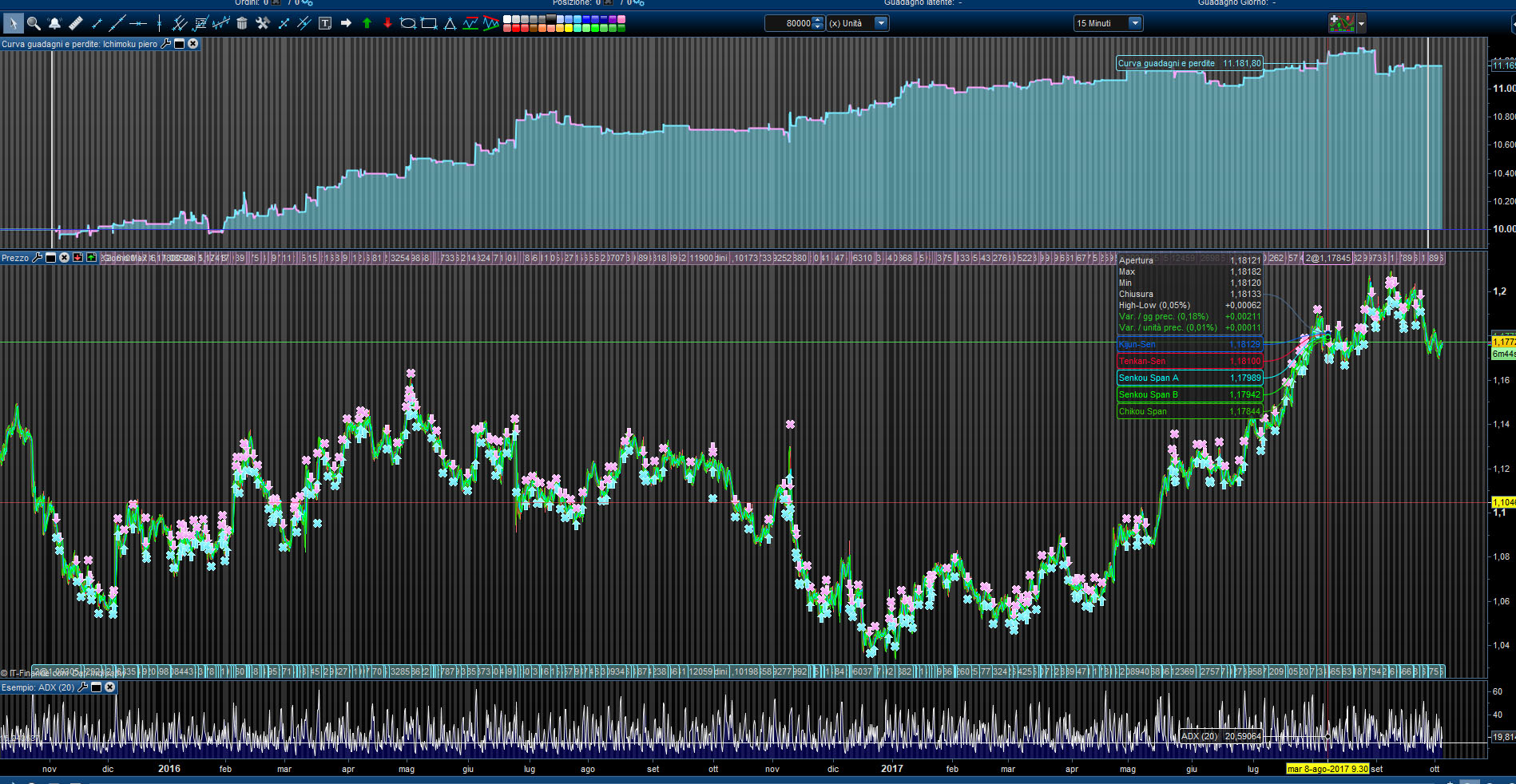

This is a very simple EA, I wrote it in the simplest way possible so that anyone can understand and work on it.

I’m not very happy with the result, the problem is that ichimoku is strongly related to the trend, and I’m thinking about how to do a prt analysis of the trend on different TSs.

Anyway, I hope you also want to work on it.

//Stategy: Ichimoku

//Author: Piero Petrosillo

//version: 1

//Timeframe: 15 and 30 minutes - eurusd only

//Backtested from 01/11/2015 to 27/09/2017

//I'm sorry for my bad english.. :-)

//work in progress..

Defparam CUMULATEORDERS = False

once segnale = 0

once barcount = 0

once barcountClose = 0

once blocForzato = 0

possize = 2

//indicators---------------------------------------------------------------------------------

T = 9 //Tenkan-Sen Period (9)

I = 26 //Chikou-Span Period (26)

K = 52 //Kijun-Sen Period (52)

TS = (highest[T](high)+lowest[T](low))/2 //Tenkan-Sen

KS = (highest[I](high)+lowest[I](low))/2 //Kijun-Sen

CS = close[I] //Chikou-Span

SA = (TS[I]+KS[I])/2 //Senkou-Span A

SB = (highest[K](high[I])+lowest[K](low[I]))/2 //Senkou-Span B

myADX = ADX[20]

//end of indicators--------------------------------------------------------------------------

//Signals------------------------------------------------------------------------------------

if blocForzato = 1 then //wait after the order close

if Barindex>barcountClose+2 then

blocForzato = 0

endif

endif

//Chikou-Span position respect to the price

prezzoCSLow = low[26]

prezzoCSHigh= high[26]

spreadCS = pointsize*4

prezzoCSLow = prezzoCSLow - spreadCS

prezzoCSHigh=prezzoCSHigh + spreadCS

// Tenkan-Sen/Kijun-Sen crossing

num1 = TS[0]

num2 = KS[0]

num1p = TS[1]

num2p = KS[1]

if segnale = 0 then

incrocio = 0

if num1>num2 and num2p>=num1p then

incrocio = 1 //long

segnale = Barindex+2

endif

if num2>num1 and num1p>=num2p then

incrocio = -1//short

segnale = Barindex+2

endif

endif

if Barindex > segnale then

segnale = 0

endif

//Kumo parameters

kumoUP =0

kumoDOWN =0

kumoUPold =0

kumoDOWNold =0

spesKumoMin =pointsize*1//-------------- minimum kumo size ---------------------

speKum =0

mode =0

if SA[0]>SB[0] then

kumoUP=SA[0]

kumoDOWN=SB[0]

mode=3

kumoUPold=SA[1]

kumoDOWNold=SB[1]

else

kumoUP=SB[0]

kumoDOWN=SA[0]

mode=4

kumoUPold=SB[1]

kumoDOWNold=SA[1]

endif

spesKumo = kumoUPold-kumoDOWNold

if spesKumo>spesKumoMin then

speKum = 1//kumo size signal

endif

//mini ts trend

primo = TS[3]

ultimo = TS[0]

spread = pointsize*2

miniTr= ultimo-primo

miniTr= miniTr/spread

//mini price trend - not used now

primo = typicalprice[1]

ultimo = typicalprice[0]

spread = pointsize*1

miniTrPr= ultimo-primo

miniTrPr= miniTrPr/spread

//ChikouSpan out of span A e B - not used now

//senkChiko = 0

if SA[26]>SB[26] then

if CS[26]>SB[26] and CS[26]<SA[26] then

//senkChiko = 1

endif

else

if CS[26]>SA[26] and CS[26]<SB[26] then

//senkChiko = 1

endif

endif

//kumo side

segnale1 =0

segnale2 =0

segnale3 =0

segnale4 =0

kumoLatLong = 0

kumoLatShort = 0

if mode = 3 then // A up, B down

last = SA[0]

candele = SA[1]

if candele > (last+spesKumoMin) then//long

segnale1 = segnale1 + 1

endif

last = SB[0]

candele = SB[1]

if (candele+spesKumoMin) < last then//short

segnale2 = segnale2 + 1

endif

endif

if mode = 4 then// B up, A down

last = SB[0]

candele = SB[1]

if candele > (last+spesKumoMin) then//long

segnale3 = segnale3 + 1

endif

last = SA[0]

candele = SA[1]

if (candele+spesKumoMin) < last then//short

segnale4 = segnale4 + 1

endif

endif

if (segnale1+segnale3) > 0 then

kumoLatLong = 1//signal

endif

if (segnale2+segnale4) > 0 then

kumoLatShort = 1//signal

endif

//end of signals------------------------------------------------------------------------------------

//Orders--------------------------------------------------------------------------------------------

//Chikou-Span redefinition

CS = close[0]

blocco = 0//not used now

speKum2 = 0

//long position

//and spesKumo>spesKumomin and senkChiko = 0 and miniTr>4 and miniTrPr>0 and incrocio = 1

if myADX>15 and blocForzato=0 then

if speKum=1 then//spessore kumo buono

if countofposition = 0 and entrataAquisto = 0 and entrataVendita = 0 and incrocio=1 and TS[0]>KS[0] and CS[0]>prezzoCSHigh and miniTr>4 then

//TS position compared to kumo

if kumoLatLong = 0 and TS[0]>kumoUP and KS[0]>kumoUP then

speKum2 = 1

else

if kumoLatLong = 1 and TS[0]>kumoDOWNold and TS[0]<kumoUPold then //to optimize it

speKum2 = 1

endif

endif

if blocco = 0 and speKum2 = 1 then

Buy possize contracts at market

barcount = Barindex

segnale = 0

entrataAquisto = 1

EndIf

endif

//Short Position

//and senkChiko = 0 and miniTr<-4 and miniTrPr<0 and incrocio = -1

if countofposition = 0 and entrataVendita = 0 and entrataAquisto = 0 and incrocio=-1 and TS[0]<KS[0] and CS[0]<prezzoCSLow and miniTr<-4 then

if kumoLatShort = 0 and TS[0]<kumoDOWN and KS[0]<kumoDOWN then

speKum2 = 1

else

if kumoLatShort = 1 and TS[0]<kumoDOWNold and TS[0]>kumoUPold then //to optimize it

speKum2 = 1

endif

endif

if blocco = 0 and speKum2 = 1 then

Sellshort possize contracts at market

barcount = Barindex

segnale = 0

entrataVendita = 1

EndIf

endif

else//slim kumo -----------------------------------------

//and miniTr>4 and miniTrPr>0and incrocio = 1

if countofposition = 0 and entrataAquisto = 0 and entrataVendita = 0 and incrocio=1 and TS[0]>KS[0] and CS[0]>prezzoCSHigh and miniTr>4 and blocco = 0 then

Buy possize contracts at market

barcount = Barindex

segnale = 0

entrataAquisto = 1

endif

//and senkChiko = 0and miniTr<-4 and miniTrPr<0and incrocio = -1

if countofposition = 0 and entrataVendita = 0 and entrataAquisto = 0 and incrocio=-1 and TS[0]<KS[0] and CS[0]<prezzoCSLow and miniTr<-4 and blocco = 0 then

Sellshort possize contracts at market

barcount = Barindex

segnale = 0

entrataVendita = 1

endif

endif

endif

//GRAPH CS[0] coloured(0,255,0) AS "CS0"

//GRAPH prezzoCSLow coloured(0,0,255) AS "prezzoCSLow"

//GRAPH incrocio coloured(255,0,0) AS "incrocio"

//GRAPH miniTr coloured(255,0,0) AS "miniTr"

//GRAPH miniTrPr coloured(255,0,0) AS "miniTrPr"

//GRAPH kumoLatShort coloured(255,0,0) AS "klat"

//GRAPH TS[0] coloured(255,0,0) AS "ts0"

//GRAPH FastSMA[0] coloured(255,0,0) AS "SMA"

//GRAPH KS[0] coloured(255,0,0) AS "ks0"

//GRAPH miniTrSma coloured(255,0,0) AS "miniTrSma"

//GRAPH speKum coloured(255,0,0) AS "speKum"

//End of orders-------------------------------------------------------------------------------------

//Exit Conditions-----------------------------------------------------------------------------------

bars = 3

if entrataAquisto = 1 and TS[0]<KS[0] then

Sell at market

segnale = 0

entrataAquisto = 0

blocForzato=1

barcountClose=Barindex

endif

if entrataAquisto = 1 and blocForzato = 1 then

Sell at market

segnale = 0

entrataAquisto = 0

blocForzato=1

barcountClose=Barindex

endif

if entrataAquisto = 1 and Barindex>barcount+bars and close[0]<close[bars] then

Sell at market

segnale = 0

entrataAquisto = 0

blocForzato=1

barcountClose=Barindex

endif

if entrataVendita = 1 and TS[0]>KS[0] then

exitshort at market

segnale = 0

entrataVendita = 0

blocForzato=1

barcountClose=Barindex

endif

if entrataVendita = 1 and blocForzato = 1 then

exitshort at market

segnale = 0

entrataVendita = 0

blocForzato=1

barcountClose=Barindex

endif

if entrataVendita = 1 and Barindex>barcount+bars and close[0]<close[bars] then

exitshort at market

segnale = 0

entrataVendita = 0

blocForzato=1

barcountClose=Barindex

endif

//Exit of exit conditions---------------------------------------------------------------------------

How can we help you? Do you need more assistance about:

how to do a prt analysis of the trend on different TSs

❓

Hi,

if I want compare the current graph TF ichimoku with the ichimoku values on a higher TF, for example at 1 hour respect the 15 minutes of the graph, it is possible with prt?

Thank’s

Piero

Not right out of the box (for now… still waiting for this crucial update 😀 ), but since Ichimoku is only built upon highest high and lowest low of different periods, we could try to get accurate values of higher timeframe, just by simulating them with periods multiplication. I think it should do the trick for Ichimoku.

Well done @pieroim, you are making excellent progress!

I can see that you are a seasoned coder looking at your programming style.

I will look a bit closer at your strategy and see if I can make any improvements.

I have a few tricks up my sleeve that I can try.

Ok.

To speed up writing the code, I used “pointize” as a constant in various functions. This works fine with eurusd at 15 and 30 minutes, otherwise it is worth to be calculated.

Remember, this is only the first version…

Nicolas, is there a way to close an order to a specific price? Example: to a 1.17113 in eurusd

Of course, you can use contrarian pending orders to close orders at specific price. If you want to close a BUY position above its current price:

SELL at myprice LIMIT

or to close the BUY position below its current price:

SELL at myprice STOP

Now I’m working on the code for the pseudo higher timeframe..

if Barindex>barcountClose+15 then //ogni 16 barre

barcountClose = Barindex

high4h=high[0]

low4h=low[0]

for x = 0 to 15 do

if high[x] > high1h then

high4h=high[x]

endif

if low[x] < low1h then

low4h=low[x]

endif

next

piuDM = MAX(high1h-high1h[1], 0)

menoDM = MAX(low1h[1]-low1h, 0)

IF piuDM > menoDM THEN

menoDM = 0

ENDIF

IF piuDM < menoDM THEN

piuDM = 0

ENDIF

IF piuDM = menoDM THEN

piuDM = 0

menoDM = 0

ENDIF

REM Calcolo degli indicatori direzionali

piuDI = WILDERAVERAGE[14](piuDM)

menoDI = WILDERAVERAGE[14](menoDM)

REM Calcolo del ADX

DX = ABS(piuDI - menoDI) / (piuDI + menoDI) * 100

myADX1h = WILDERAVERAGE[14](DX)

endif

with the above code i would like to calculate an 4h ADX in a 15m chart .. but it does not go .. the chart values, no matter if fragmented, are far from those of a 4 hour ADX ..

errata/corrige..

if Barindex>barcountClose+15 then //ogni 16 barre

barcountClose = Barindex

high4h=high[0]

low4h=low[0]

for x = 0 to 15 do

if high[x] > high4h then

high4h=high[x]

endif

if low[x] < low4h then

low4h=low[x]

endif

next

piuDM = MAX(high4h-high4h[16], 0)

menoDM = MAX(low4h[16]-low4h, 0)

IF piuDM > menoDM THEN

menoDM = 0

ENDIF

IF piuDM < menoDM THEN

piuDM = 0

ENDIF

IF piuDM = menoDM THEN

piuDM = 0

menoDM = 0

ENDIF

REM Calcolo degli indicatori direzionali

piuDI = WILDERAVERAGE[223](piuDM)

menoDI = WILDERAVERAGE[223](menoDM)

REM Calcolo del ADX

DX = ABS(piuDI - menoDI) / (piuDI + menoDI) * 100

myADX4h = WILDERAVERAGE[223](DX)

endif

now vorks a little better..