Solved… a stupid mistake.. pardon..

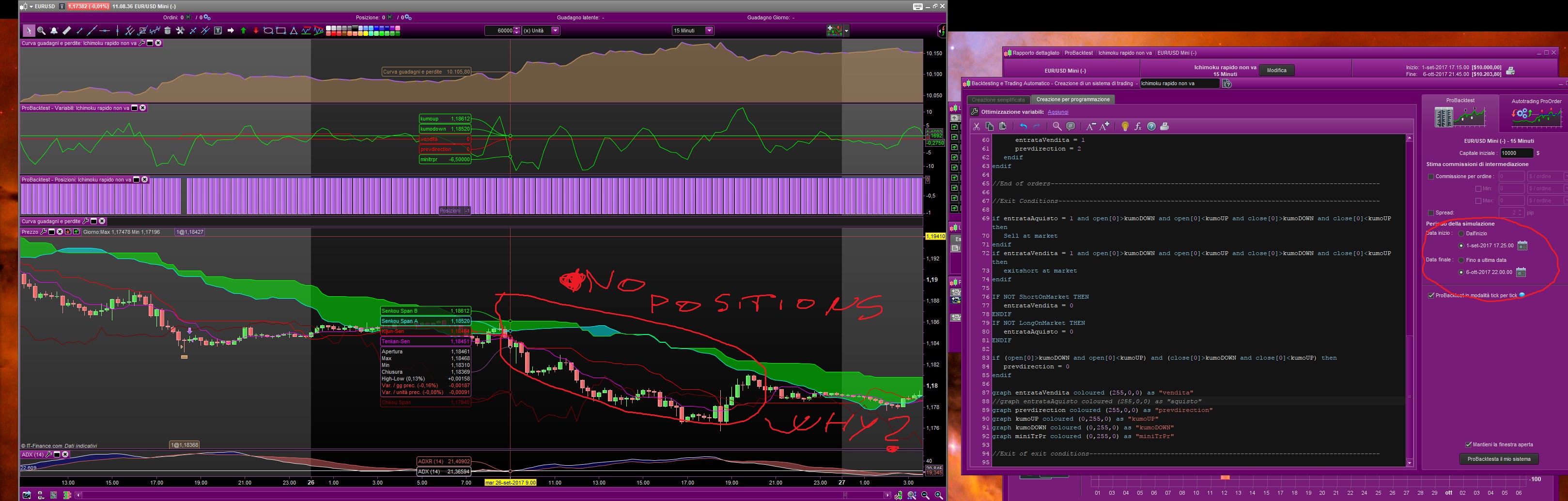

This is a very simple strategy for better understanding programming with PRT. But the backtest gives me strange results .. what I’m doing of wrong?

//Stategy: Ichim

Defparam CUMULATEORDERS = False

once prevdirection = 0 //1 = buy, 2 = sell

possize = 1

stoploss = 0.0100 //points 0.0010 10 pips

profitto = 0.0100

//indicators---------------------------------------------------------------------------------

T = 9 //Tenkan-Sen Period (9)

I = 26 //Chikou-Span Period (26)

K = 52 //Kijun-Sen Period (52)

TS = (highest[T](high)+lowest[T](low))/2 //Tenkan-Sen

KS = (highest[I](high)+lowest[I](low))/2 //Kijun-Sen

SA = (TS[I]+KS[I])/2 //Senkou-Span A

SB = (highest[K](high[I])+lowest[K](low[I]))/2 //Senkou-Span B

//end of indicators--------------------------------------------------------------------------

//Signals------------------------------------------------------------------------------------

//Kumo parameters

kumoUP =0

kumoDOWN =0

if SA[0]>SB[0] then

kumoUP=SA[0]

kumoDOWN=SB[0]

else

kumoUP=SB[0]

kumoDOWN=SA[0]

endif

//mini price trend

primo = (high[3]+low[3])/2

ultimo = (high[0]+low[0])/2

spread = pointsize*2

miniTrPr= ultimo-primo

miniTrPr= miniTrPr/spread

//end of signals------------------------------------------------------------------------------------

//Orders--------------------------------------------------------------------------------------------

if prevdirection = 2 or prevdirection = 0 then

if countofposition = 0 and entrataAquisto = 0 and entrataVendita = 0 and open[0]>kumoUP and close[0]>open[0] and miniTrPr>5 then

Buy possize contracts at market

set target profit profitto// profit in points

SET STOP LOSS stoploss

entrataAquisto = 1

prevdirection = 1

endif

endif

if prevdirection = 1 or prevdirection = 0 then

if countofposition = 0 and entrataVendita = 0 and entrataAquisto = 0 and close[0]<kumoDOWN and close[0]<open[0] and miniTrPr<-5 then

Sellshort possize contracts at market

set target profit profitto// profit in points

SET STOP LOSS stoploss

entrataVendita = 1

prevdirection = 2

endif

endif

//End of orders-------------------------------------------------------------------------------------

//Exit Conditions-----------------------------------------------------------------------------------

if entrataAquisto = 1 and open[0]>kumoDOWN and open[0]<kumoUP and close[0]>kumoDOWN and close[0]<kumoUP then

Sell at market

endif

if entrataVendita = 1 and open[0]>kumoDOWN and open[0]<kumoUP and close[0]>kumoDOWN and close[0]<kumoUP then

exitshort at market

endif

IF NOT ShortOnMarket THEN

entrataVendita = 0

ENDIF

IF NOT LongOnMarket THEN

entrataAquisto = 0

ENDIF

if (open[0]>kumoDOWN and open[0]<kumoUP) and (close[0]>kumoDOWN and close[0]<kumoUP) then

prevdirection = 0

endif

graph entrataVendita coloured (255,0,0) as "vendita"

//graph entrataAquisto coloured (255,0,0) as "aquisto"

graph prevdirection coloured (255,0,0) as "prevdirection"

graph kumoUP coloured (0,255,0) as "kumoUP"

graph kumoDOWN coloured (0,255,0) as "kumoDOWN"

graph miniTrPr coloured (0,255,0) as "miniTrPr"

//Exit of exit conditions---------------------------------------------------------------------------

Not Solved… entrataAquisto would be on 1 in the picture…

IF NOT ShortOnMarket THEN

entrataVendita = 0

ENDIF

IF NOT LongOnMarket THEN

entrataAquisto = 0

ENDIF

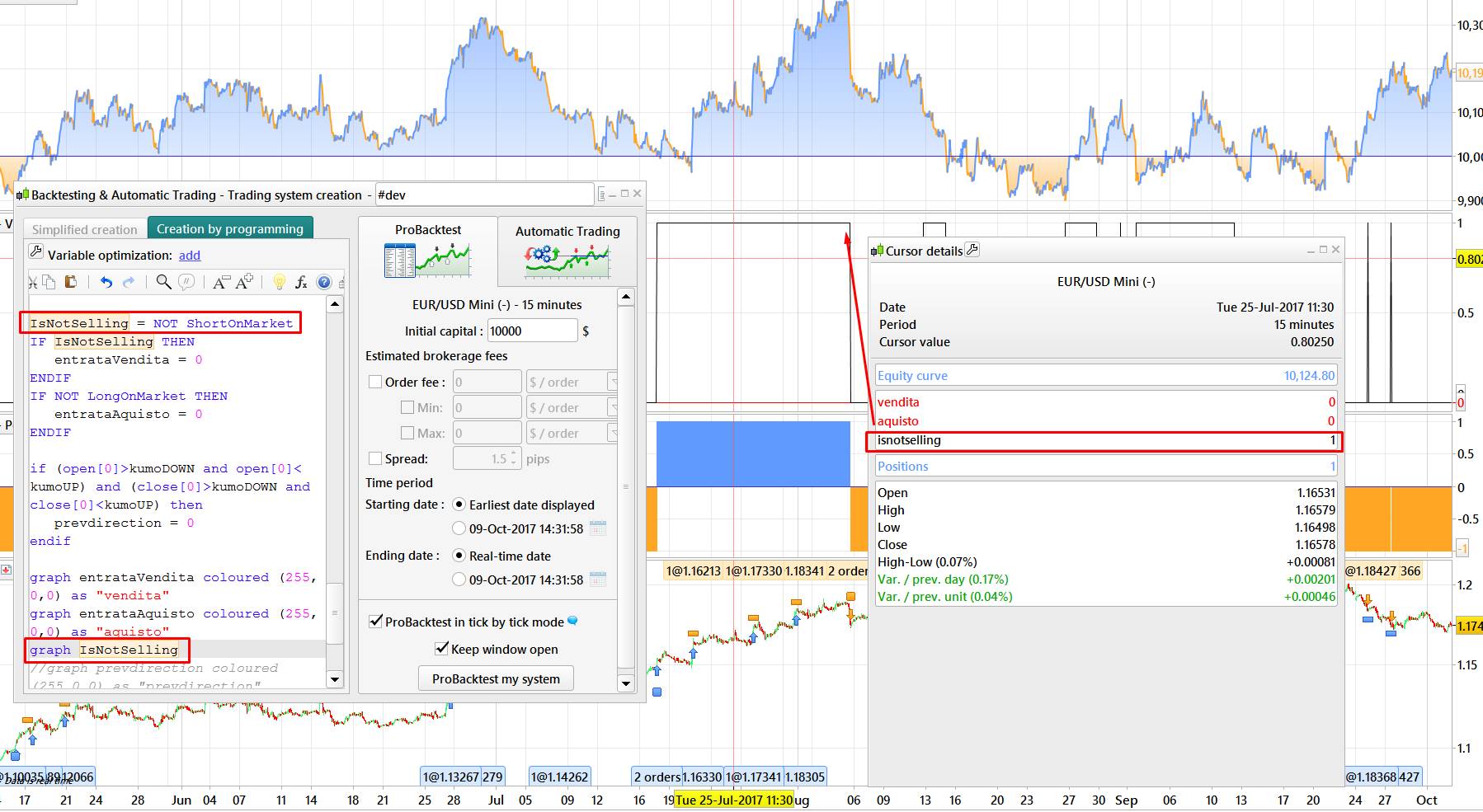

If you have no long position opened, then ‘entrataAquisto’ is set to 0. This value is set at bar Close and only visible in next bars, so when you set it to 1, you will only see it, at first at next bar open.

Ok Nicolas, but in picture that I attached, you can see that the variable woud be to 1 in the bars after the bar where a long position is opened.

The backtest in the graph gives me 0 valute..

I do not know what’s wrong, but maybe this is something that could help: create a boolean variable that use NOT SHORTONMARKET as its own test.

Thank’s Nicolas, very strange behavior of PRT backtest..

However, your suggestion has led me to the solution..

I replaced:

IF NOT ShortOnMarket THEN

entrataVendita = 0

ENDIF

IF NOT LongOnMarket THEN

entrataAquisto = 0

ENDIF

simply with:

entrataVendita = ShortOnMarket

entrataAquisto = LongOnMarket

Now all works great!

Thank’s

Piero