We all know that also if we have a profitable system, during the years markets changes and we need to re-optimize the system in order to fit the current period.

Let’s look at the vectorial dax: a perfect system that worked with huge gains, then suddenly from january it became an account burner.

So the question is, when and how a coder realize that the values of the system needs to be re-optimized in order to not achieve too much losses? How a coder can understand that it’s not just a drawdown period forming part of the nature of the system? And on which basis we can do that re-optimization? (since the system started to perform worst? on 200k? or other?)?

From January, especially end of January, many unpredictable events occurred.

In my opinion you should re-optimize it once in a while if results are quite different (even if still positive) from the last optimization done.

Some months ago, @GraHal and I tried to ‘systematically’ explore the benefits of regular re-optimization – monthly for the previous quarter, quarterly for the previous half year etc. Lots of permutations. The results were inconclusive. Some bots seemed to benefit enormously from a regular refresh, others came out worse off. I would love to develop some set of rules to work by, but not sure it exists. At least not as a one-size-fits-all. I think you just have to keep an eye on the curve and watch for when it starts to go flat, then maybe re-optimize a new version and if poss, run them both to see if the first one doesn’t come alive again.

I thought for sure I’d breathed life into the Vectorial DAX then on its first day the new version made 2 stinking trades for nearly €500 loss — as they say, be careful what you wish for!

Yes but some problems still remains.

While i don’t understand that the worsening of the curve it’s not physiological or influenced by particular events but it’s due to a necessary re-optimization, i will lose money, a lot of money probably…

Probably the vectorial dax is dead for now, or forever, who knows 🙂

i would argue that a system dosnt have to be reoptimized. I try to make all my systems as robust as possible so they work in up/down/choppy markets all the same with an as even equity line as possible. Sometimes this will make it underperform and sometimes it will overperform vs the underlying market, and thats fine.

Another thing i have researched, at least on my systems is a fixed dollar/pip stop/target. Ive tried ATR, ive tried %, but i get the best results using fixed dollar/pip stops. I recently read that Kevin Davey actually uses pip/dollar stop and that his research has brough him to the same conclusion: its not really that big of a difference what you use.

And while researching this for myself, i found that very often the same pip stop/target is usable through LARGE data/time. Meaning if i do a anchored walk forward, looking at the stop and target numbers only, i will often get the same numbers or very close to the same numbers throughout the whole dataset.

And this sort of was my thought as well. Charting up with resistance and support levels they are often very closely similare pip amounts between each level, even going back years.

I dont reoptimize my codes at all, and even if it sometimes look like a bigger stop loss could have saved the day, or a smaller target, it usually dosnt help in the long run trying to change it.

Might just be me, but I was re-listening to Andrea Unger on Better system trader #45 yesterday and he also dosnt seem to usually re-optimize his systems, he would rather have a robust and stable system throughout the whole data set. That being said he did mentioned that he has done it, but not so often and not on a regular basis.

Personally i think that reoptimizing means you never really have the same system, so how would you know how it actually is performing if you keep changing how it works all the time.

It’s a very good point of view Jebus, but does this assume that you think a good system never dies?

I like this philosophy, and I would love to believe in it as it would be much more “comfortable”, but you speak as if it is very simple to create a system that is robust “forever”.

The point then is, is it easier to create a lifetime system or a system that requires re-optimization every tot?

I am quite new in this field, but for what little I have seen it is very simple that super systems fail from month to month, how can the coder could knew that after a lot of profitable years suddenly everything would became junk? Maybe he also believed the system would be robust forever, but….

Personally I never optimize a system, sometimes I only improve it if I can decrease the download ….. when a system loses reliability I delete it …. I have trading systems that have been active for three years and even at this time they work well …. but everyone must do as he thinks is better there are others I know and if they could re-optimize him every day … there is no right thing.

The destructor of accounts recuperated the middle of loss money.

Vectorial is a great strategy of this forum.

And while researching this for myself, i found that very often the same pip stop/target is usable through LARGE data/time. Meaning if i do a anchored walk forward, looking at the stop and target numbers only, i will often get the same numbers or very close to the same numbers throughout the whole dataset. And this sort of was my thought as well.

I’m not sure that the actual data would agree with you! It also very much depends on what instrument you are trading.

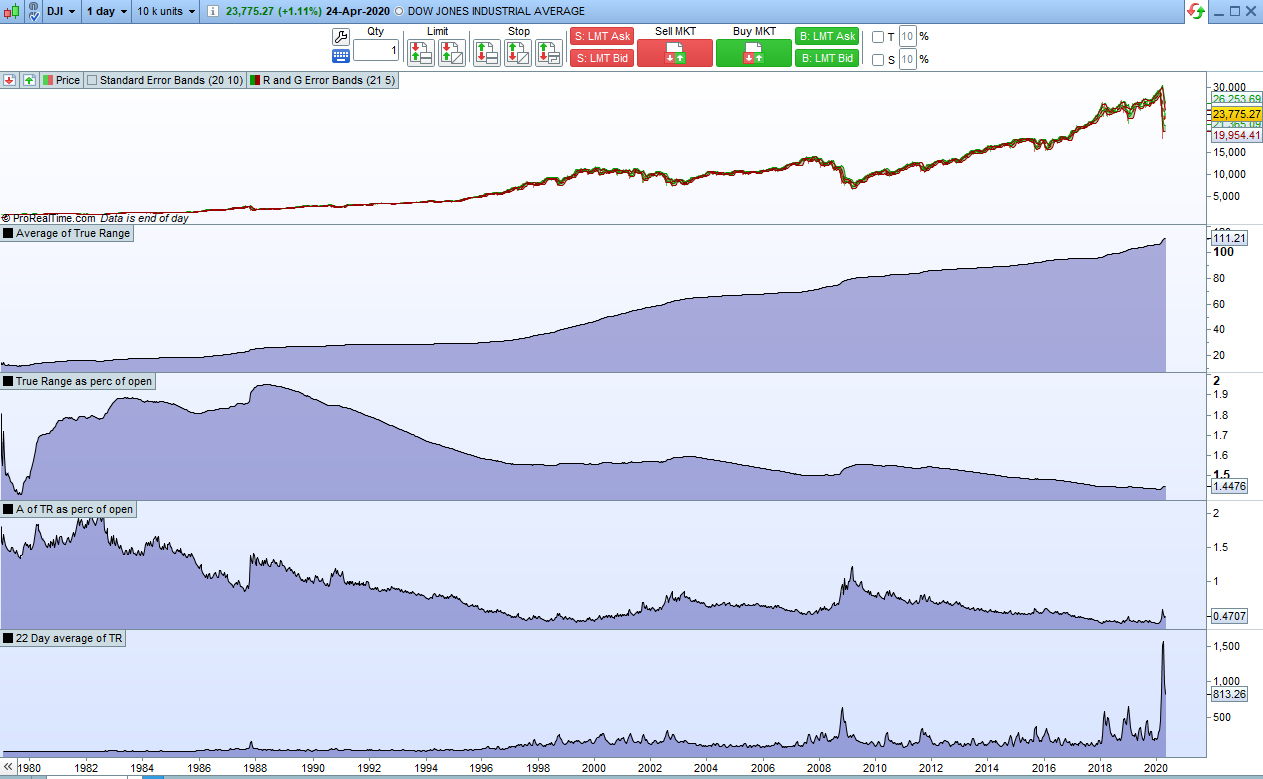

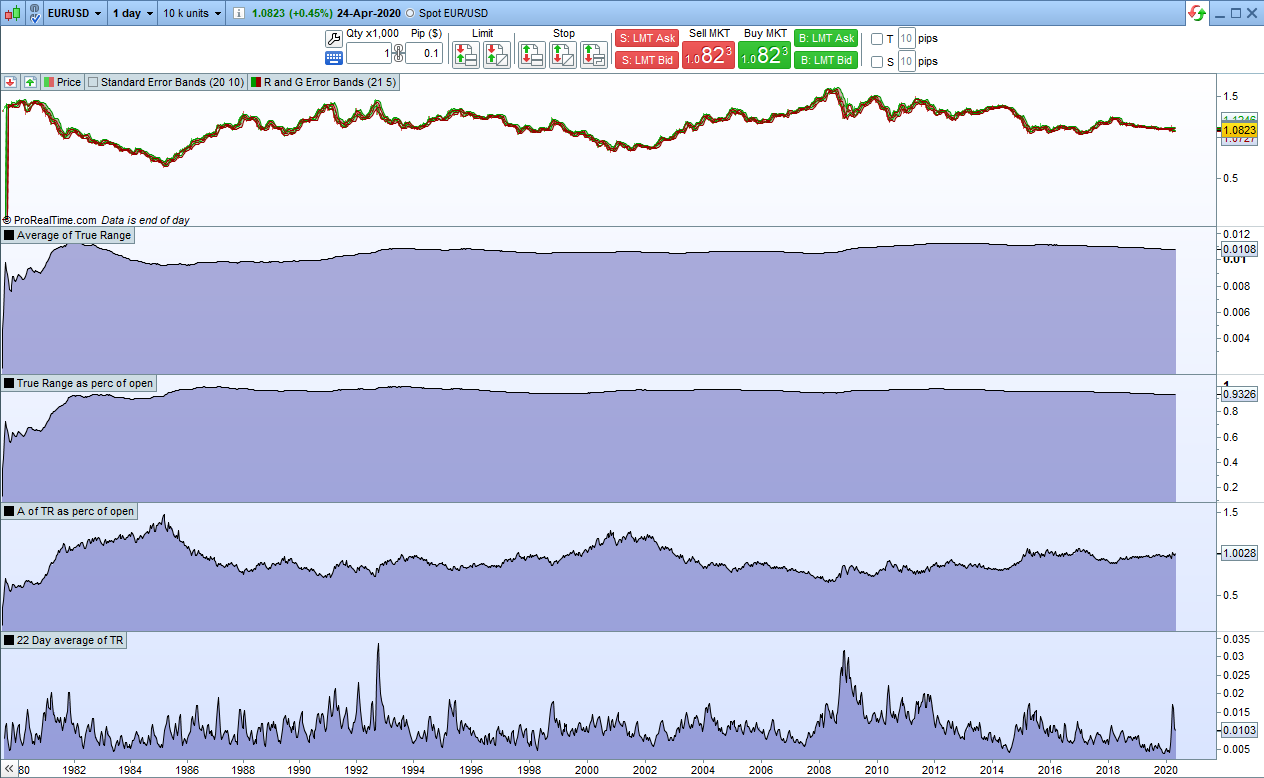

The first two images show the DOW and the EURUSD with four indicators on.

The top one is an all time average of true range. So the range of every bar to date is added up and divided by the number of bars. So we can see that the DJI’s true range has been getting bigger and bigger as time goes by. The EURUSD on the other hand has not.

The second indicator is an all time average of true range as a percentage of the opening price. On the DJI as price has gone up true range as a percentage of open has been falling. On the EURUSD it hasn’t.

The third indicator does the same calculation as the first to get the all time average of true range but then displays it as a percentage of the opening price of each bar. We can see that on the DJI as price rises it falls and as price falls it rises.

The fourth indicator is a simple 22 day average of true range. On the DJI it has been going up slowly with big peaks in the big crashes.

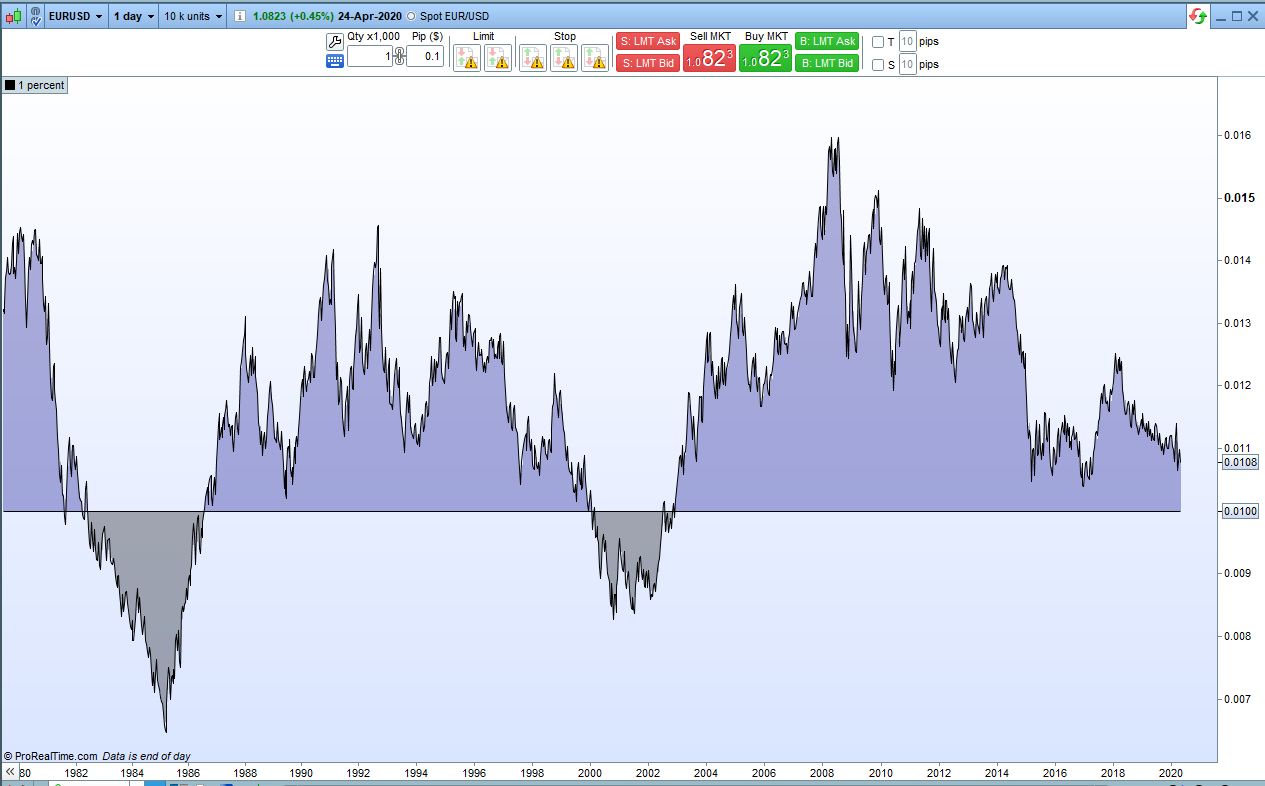

There are then two charts that show 1 percent of the opening price compared to a fixed value line. I just cant see how having a fixed value on something like the DJI for all of history makes any sense at all when I look at this.

Perhaps on something like the EURUSD you might get away with a fixed value for stop loss and take profit but it would still be pretty inefficient during certain market conditions. On an index like the DJI it would seem to make no sense at all to not have changed your stop loss and take profit levels if only for the single reason that true range has slowly been increasing over the years.