Hallo,

schon wieder habe ich ein Problem.

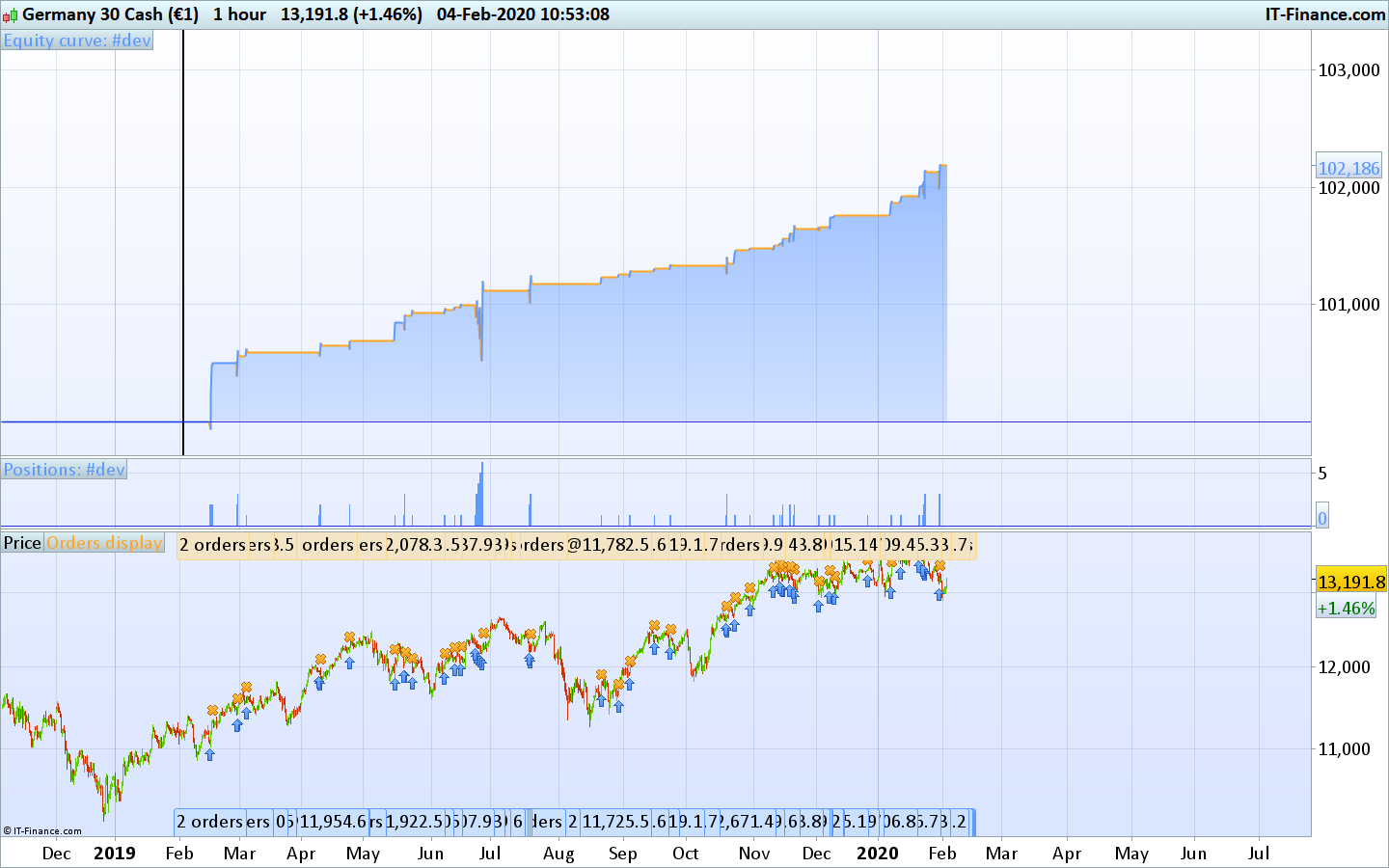

Ich benutze im Livehandel dieses System auf DAX H1 mit ziemlich guter Performance.

Nun habe ich versucht ein Grid-System mit Averaging Down einzubauen… ich kriegs einfach nicht hin. Die Performance sinkt rapide… irgendwas mach ich mit meinen beschränkten Fähigkeiten falsch.

Hier das System wie es jetzt läuft. Es handelt in Rücksetzer eines Uptrends hinein.

Könnte mir bitte jemand ein Grid, Abstand frei wählbar, mit einer Average Down Technik einbauen?

// Festlegen der Code-Parameter

DEFPARAM CumulateOrders = False // Kumulieren von Positionen deaktiviert

DEFPARAM Preloadbars = 300

// Verhindert das Platzieren von neuen Ordern zum Markteintritt oder Vergrößern von Positionen vor einer bestimmten Uhrzeit

noEntryBeforeTime = 010000

timeEnterBefore = time >= noEntryBeforeTime

// Verhindert das Platzieren von neuen Ordern zum Markteintritt oder Vergrößern von Positionen nach einer bestimmten Uhrzeit

noEntryAfterTime = 233000

timeEnterAfter = time < noEntryAfterTime

// Verhindert das Trading an bestimmten Wochentagen

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

// Bedingungen zum Einstieg in Long-Positionen

indicator1 = Average[20](close)//20

indicator2 = Average[70](close)//70

c1 = (indicator1 CROSSES UNDER indicator2)

indicator3 = ADX[14]

c2 = (indicator3 > 10)

indicator4 = ADX[14]

c3 = (indicator4 < 30)

IF (c1 AND c2 AND c3) AND timeEnterBefore AND timeEnterAfter AND not daysForbiddenEntry THEN

BUY 1 CONTRACT AT MARKET

ENDIF

// Bedingungen zum Ausstieg von Long-Positionen

indicator5 = Average[20](close)//20

indicator6 = Average[70](close)//70

c4 = (indicator5 CROSSES OVER indicator6)

IF c4 THEN

SELL AT MARKET

ENDIF

// Stops und Targets

SET STOP pLOSS 150 //150

//************************************************************************

//trailing stop function

trailingstart = 20 //20 trailing will start @trailinstart points profit

trailingstep = 10 //10 trailing step to move the "stoploss"

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart*pipsize THEN

newSL = tradeprice(1)+trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND close-newSL>=trailingstep*pipsize THEN

newSL = newSL+trailingstep*pipsize

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart*pipsize THEN

newSL = tradeprice(1)-trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND newSL-close>=trailingstep*pipsize THEN

newSL = newSL-trailingstep*pipsize

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

This is the modified code that embed an averaging down system. I removed the stoploss and it is the trailing stop that manage the exit when in profit.

// Festlegen der Code-Parameter

DEFPARAM CumulateOrders = true // Kumulieren von Positionen deaktiviert

DEFPARAM Preloadbars = 300

gridStep = 20

// Verhindert das Platzieren von neuen Ordern zum Markteintritt oder Vergrößern von Positionen vor einer bestimmten Uhrzeit

noEntryBeforeTime = 010000

timeEnterBefore = time >= noEntryBeforeTime

// Verhindert das Platzieren von neuen Ordern zum Markteintritt oder Vergrößern von Positionen nach einer bestimmten Uhrzeit

noEntryAfterTime = 233000

timeEnterAfter = time < noEntryAfterTime

// Verhindert das Trading an bestimmten Wochentagen

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

// Bedingungen zum Einstieg in Long-Positionen

indicator1 = Average[20](close)//20

indicator2 = Average[70](close)//70

c1 = (indicator1 CROSSES UNDER indicator2)

indicator3 = ADX[14]

c2 = (indicator3 > 10)

indicator4 = ADX[14]

c3 = (indicator4 < 30)

IF not longonmarket and (c1 AND c2 AND c3) AND timeEnterBefore AND timeEnterAfter AND not daysForbiddenEntry THEN

BUY 1 CONTRACT AT MARKET

ENDIF

//grid

if longonmarket and tradeprice-close>=gridStep*pointsize then

buy 1 contract at market

endif

// Bedingungen zum Ausstieg von Long-Positionen

indicator5 = Average[20](close)//20

indicator6 = Average[70](close)//70

c4 = (indicator5 CROSSES OVER indicator6)

IF c4 THEN

SELL AT MARKET

ENDIF

// Stops und Targets

//SET STOP pLOSS 150 //150

//************************************************************************

//trailing stop function

trailingstart = 20 //20 trailing will start @trailinstart points profit

trailingstep = 10 //10 trailing step to move the "stoploss"

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-positionprice>=trailingstart*pipsize THEN

newSL = positionprice+trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND close-newSL>=trailingstep*pipsize THEN

newSL = newSL+trailingstep*pipsize

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND positionprice-close>=trailingstart*pipsize THEN

newSL = positionprice-trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND newSL-close>=trailingstep*pipsize THEN

newSL = newSL-trailingstep*pipsize

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

Of course, like any other martingale, the result could be worse than the benefit. It always risky to not close the losing orders!

Danke, jetzt hab ich meinen Fehler auch erkannt.

Ich hab den Stoploss wieder verändert hinzugefügt und countofposition hinzugefügt. Damit läuft es über 100000bars sehr stabil. Also federt auch kleinere Downtrends ab.

Haben Sie die Möglichkeit über 200000bars zu testen?

Egal in welchem Verlauf Sie die Strategie testen, sie stürzt immer eines Tages ab. Es kommt also darauf an, wann du anfängst … Viel Glück.

Das ist richtig. Das Schicksal des Martingale…

Erstmal vielen Dank.