Ci-joint le code de la stratégie modifiée qui exécute des sorties partielles.

Bonjour nicolas,

je me suis permis d’utiliser ton code pour la vente partielle sur cfd mais je ne vois pas mon erreur, mon résultat ne change pas pourrais tu m’aider.

je te joins le code , désolé je l’ai partagé plusieurs fois.

dans l’attente de te lire

// Définition des paramètres du code

DEFPARAM CumulateOrders = False // Cumul des positions désactivé

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position avant l'heure spécifiée

noEntryBeforeTime = 145000

timeEnterBefore = time >= noEntryBeforeTime

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position après l'heure spécifiée

noEntryAfterTime = 235900

timeEnterAfter = time < noEntryAfterTime

// Empêche le système de placer de nouveaux ordres sur les jours de la semaine spécifiés

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

// Conditions pour ouvrir une position en vente à découvert

indicator1 = SenkouSpanB[9,26,52]

c1 = (close CROSSES UNDER indicator1)

indicator2 = SenkouSpanA[9,26,52]

c2 = (close CROSSES UNDER indicator2)

IF (c1 AND c2) AND timeEnterBefore AND timeEnterAfter AND not daysForbiddenEntry and tally < maxTrades THEN

sellshort 2 CONTRACT AT MARKET

closed=0

endif

if onmarket then

buy 1 contract at (tradeprice +0.0010*pipsize) limit

endif

//---------------------------------------------------------------------------------------------------------------

once maxTrades = 10 //maxNumberDailyTrades

once tally = 0

if intradayBarIndex = 0 then

tally = 0

endif

newTrades = (onMarket and not onMarket[1]) or ((not onMarket and not onMarket[1]) and (strategyProfit <> strategyProfit[1])) or (longOnMarket and ShortOnMarket[1]) or (longOnMarket[1] and shortOnMarket) or ((tradeIndex(1) = tradeIndex(2)) and (barIndex = tradeIndex(1)) and (barIndex > 0) and (strategyProfit = strategyProfit[1]))

if newTrades then

tally = tally +1

endif

//------------------------------------------------------------------------------------------------------------------------

//---------------------------------------------------------------------------------------------------------------

//Max-Orders per Day

once maxOrdersL = 1 //long

once maxOrdersS = 1 //short

if intradayBarIndex = 0 then //reset orders count

ordersCountL = 0

ordersCountS = 0

endif

if longTriggered then //check if an order has opened in the current bar

ordersCountL = ordersCountL + 1

endif

if shortTriggered then //check if an order has opened in the current bar

ordersCountS = ordersCountS + 1

endif

//------------------------------------------------------------------------------------------------------------------------

// Stops et objectifs

set stop %loss 0.58

set target %profit 0.21

IF Not OnMarket THEN

//

// when NOT OnMarket reset values to default values

//

TrailStart = 2.79 //30 Start trailing profits from this point

BasePerCent = 0.000 //20.0% Profit percentage to keep when setting BerakEven

StepSize = 1 //10 Pip chunks to increase Percentage

PerCentInc = 0.000 //10.0% PerCent increment after each StepSize chunk

BarNumber = 10 //10 Add further % so that trades don't keep running too long

BarPerCent = 0.235 //10% Add this additional percentage every BarNumber bars

RoundTO = -0.5 //-0.5 rounds always to Lower integer, +0.4 rounds always to Higher integer, 0 defaults PRT behaviour

PriceDistance = 9 * pipsize //7 minimun distance from current price

y1 = 0 //reset to 0

y2 = 0 //reset to 0

ProfitPerCent = BasePerCent //reset to desired default value

TradeBar = BarIndex

ELSIF LongOnMarket AND close > (TradePrice + (y1 * pipsize)) THEN //LONG positions

//

// compute the value of the Percentage of profits, if any, to lock in for LONG trades

//

x1 = (close - tradeprice) / pipsize //convert price to pips

IF x1 >= TrailStart THEN // go ahead only if N+ pips

Diff1 = abs(TrailStart - x1) //difference from current profit and TrailStart

Chunks1 = max(0,round((Diff1 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks1 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y1 = max(x1 * ProfitPerCent, y1) //y1 = % of max profit

ENDIF

ELSIF ShortOnMarket AND close < (TradePrice - (y2 * pipsize)) THEN //SHORT positions

//

// compute the value of the Percentage of profits, if any, to lock in for SHORT trades

//

x2 = (tradeprice - close) / pipsize //convert price to pips

IF x2 >= TrailStart THEN // go ahead only if N+ pips

Diff2 = abs(TrailStart - x2) //difference from current profit and TrailStart

Chunks2 = max(0,round((Diff2 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks2 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y2 = max(x2 * ProfitPerCent, y2) //y2 = % of max profit

ENDIF

ENDIF

IF y1 THEN //Place pending STOP order when y1 > 0 (LONG positions)

SellPrice = Tradeprice + (y1 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - SellPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close >= SellPrice THEN

SELL AT SellPrice STOP

ELSE

SELL AT SellPrice LIMIT

ENDIF

ELSE

//

//sell AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

SELL AT Market

ENDIF

ENDIF

IF y2 THEN //Place pending STOP order when y2 > 0 (SHORT positions)

ExitPrice = Tradeprice - (y2 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - ExitPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close <= ExitPrice THEN

EXITSHORT AT ExitPrice STOP

ELSE

EXITSHORT AT ExitPrice LIMIT

ENDIF

ELSE

//

//ExitShort AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

EXITSHORT AT Market

ENDIF

ENDIF

Cet ordre de vente fonctionne très bien, mais nécessite la clôture de bougie pour être exécuté. Est il possible de placer un ordre Take Profit partiel, pour une demi position par exemple ? Cela permettrait une exécution sûre de l’ordre, mais je ne vois rien dans la doc de PRT qui le permette…

Pour clôturer partiellement un ordre, il faut utiliser un ordre au marché et pour cela il faut que le code soit lu et le code n’est lu qu’une seule fois par bougie à sa clôture.

Pour agir intra bougie, on peut utiliser une unité de temps plus petite qui va lire le code plus souvent pour la gestion des ordres (sans toucher à la logique propre d’entrée qui elle restera sur l’unite de temps qu’elle utilise déjà).

Ci-joint la version MTF, on la lance sur le timeframe désiré pour gérer les sorties partielles, ici dans mon exemple ci-joint en 5-minutes.

Merci beaucoup pour votre réponse rapide ! Je teste cela de suite !

Il semble y avoir un problème sur le fichier itf joint… PRT refuse de l’ouvrir en indiquant que le format du fichier n’est pas correct

J’ai aussi essayé de passer en 1 mn la partie de mon code relative au stop suiveur, qui est de base en 5 minutes, mais PRT refuse car 1 n’est pas multiple de 5. Il faut donc que je ré-écrive tout le code en 1 minute ?

Même en partant d’un code basé en 1 minute, cela ne fonctionne pas, j’ai le même message d’erreur…

En attendant de pouvoir résoudre ce problème d’import de fichier, ci-dessous le code complet à copier/coller pour bien comprendre la logique des 2 timeframes.

// ===========================

// WS 15MN LONG BE

// ===========================

DEFPARAM CumulateOrders = false

DEFPARAM Preloadbars = 10000

TIMEFRAME(15 minutes,updateonclose)

// ========== TAILLE DES POSITIONS ==========

// 3 VARIABLES A PARAMETRER

CapitalInit = 10000 // Capital initial (pour le réinvestissement des gains)

REINV = 0 // 0 = sans réinvestir / 1 = réinvestir les gains

NCONTRATS = 2 // nombre par défaut de minicontrats (longs)

IF REINV = 0 THEN

n = NCONTRATS

Capital = CapitalInit

ELSIF REINV = 1 THEN

capital = CapitalInit + strategyprofit

n = (capital / CapitalInit) * NCONTRATS

ENDIF

// ACTIVATION OU NON DES LONGS / SHORTS

// 0 = désactiver / 1 = activer

LongsOK = 1

ShortsOK = 0

//Coefficient SHORT

Coef = 15/10

// PARAMETRES BREAKEVEN

Breakeven1 = 1 // 0 = désactiver 1 = activer

IF not onmarket THEN

BElongactif = 0

BEshortactif = 0

ENDIF

IF not longonmarket THEN

BElongactif = 0

ENDIF

IF not shortonmarket THEN

BEshortactif = 0

ENDIF

// Paramètres Breakeven

// LONGS

BEniveauLong = 50

BELongKeep = 5

// SHORTS

BEniveauShort = 60

BEShortKeep = 5

// ACTIVATION DES PLAGES HORAIRES D'ENTRÉE EN POSITION

// 0 = désactiver la plage / 1 = activer la plage (conseillé)

// LONGS

PlageOKL1 = 1

PlageOKL2 = 0

PlageOKL3 = 0

PlageOKL4 = 0

PlageOKL5 = 0

PlageOKL6 = 0

// SHORTS

PlageOKS0 = 0

PlageOKS1 = 0

PlageOKS2 = 0

PlageOKS3 = 0

PlageOKS4 = 0

PlageOKS5 = 0

//PLAGE HORAIRE

// LONGS

CtimeAchat1 = time >= 090000 and time < 113000

CtimeAchat2 = time >= 113000 and time < 153000

CtimeAchat3 = time >= 153000 and time < 173000

CtimeAchat4 = time >= 173000 and time < 190000

CtimeAchat5 = time >= 190000 and time < 203000 and dayofweek <> 5

CtimeAchat6 = time >= 203000 and time < 213000 and dayofweek <> 5

// FILTRE : % VARIATION DE LA JOURNEE PRECEDENTE

// Pas de trade long / short si fort % variation long / short la veille

IF dayofweek = 1 THEN

dayclose = DClose(2)

dayopen = DOpen(2)

ELSIF dayofweek >=2 and dayofweek < 6 THEN

dayclose = DClose(1)

dayopen = DOpen(1)

ENDIF

PrevDayVar = dayclose - dayopen

PrevDayVarPercent = (PrevDayVar *100 / dayclose)

CaPrevDay1 = PrevDayVarPercent < 2.3

CaPrevDay2 = PrevDayVarPercent < 2.4

CaPrevDay3 = PrevDayVarPercent < 3.2

CaPrevDay4 = PrevDayVarPercent < 1.6

CaPrevDay5 = PrevDayVarPercent < 3

CaPrevDay6 = PrevDayVarPercent < 2.1

CvPrevDay0 = PrevDayVarPercent > -3

CvPrevDay1 = PrevDayVarPercent > -1.8

CvPrevDay2 = PrevDayVarPercent > -3

CvPrevDay3 = PrevDayVarPercent > -2.5

CvPrevDay4 = PrevDayVarPercent > -2.8

CvPrevDay5 = PrevDayVarPercent > -2.5

// FILTRE : MOMENTUM

MOM1a = Momentum[5]

Cam1 = MOM1a > MOM1a[1]

MOM2a = Momentum[4]

Cam2 = MOM2a > MOM2a[4]

MOM3a = Momentum[13]

Cam3 = MOM3a > MOM3a[2]

MOM4a = Momentum[8]

Cam4 = MOM4a > MOM4a[1]

MOM5a = Momentum[13]

Cam5 = MOM5a > MOM5a[4]

MOM6a = Momentum[14]

Cam6 = MOM6a > MOM6a[7]

MOM0v = Momentum[8]

Cvm0 = MOM0v < MOM0v[3]

MOM1v = Momentum[10]

Cvm1 = MOM1v < MOM1v[1]

MOM2v = Momentum[13]

Cvm2 = MOM2v < MOM2v[1]

MOM3v = Momentum[6]

Cvm3 = MOM3v < MOM3v[2]

MOM4v = Momentum[3]

Cvm4 = MOM4v < MOM4v[1]

MOM5v = Momentum[14]

Cvm5 = MOM5v < MOM5v[1]

// FILTRE : PENTE VWAP

d = max(1, intradaybarindex)

IF SUMMATION[d](volume) <> 0 Then

VWAP = SUMMATION[d](volume*typicalprice)/SUMMATION[d](volume)

ELSE

VWAP = 0

ENDIF

IF CtimeAchat1 AND VWAP[15] <> 0 THEN

IF VWAP >= VWAP[15] THEN

Slope = (VWAP - VWAP[15]) / VWAP[15]

ELSIF VWAP < VWAP[15] THEN

Slope = (VWAP - VWAP[15]) / VWAP

ENDIF

caVwap1 = Slope < 40/10000

ENDIF

IF CtimeAchat2 AND VWAP[90] <> 0 THEN

IF VWAP >= VWAP[90] THEN

Slope = (VWAP - VWAP[90]) / VWAP[90]

ELSIF VWAP < VWAP[90] THEN

Slope = (VWAP - VWAP[90]) / VWAP

ENDIF

caVwap2 = Slope < 45/10000

ENDIF

IF CtimeAchat3 AND VWAP[5] <> 0 THEN

IF VWAP >= VWAP[5] THEN

Slope = (VWAP - VWAP[5]) / VWAP[5]

ELSIF VWAP < VWAP[5] THEN

Slope = (VWAP - VWAP[5]) / VWAP

ENDIF

caVwap3 = Slope < 60/10000

ENDIF

IF CtimeAchat4 AND VWAP[65] <> 0 THEN

IF VWAP >= VWAP[65] THEN

Slope = (VWAP - VWAP[65]) / VWAP[65]

ELSIF VWAP < VWAP[65] THEN

Slope = (VWAP - VWAP[65]) / VWAP

ENDIF

caVwap4 = Slope < 5/10000

ENDIF

IF CtimeAchat5 AND VWAP[75] <> 0 THEN

IF VWAP >= VWAP[75] THEN

Slope = (VWAP - VWAP[75]) / VWAP[75]

ELSIF VWAP < VWAP[75] THEN

Slope = (VWAP - VWAP[75]) / VWAP

ENDIF

caVwap5 = Slope < 75/10000

ENDIF

IF CtimeAchat6 AND VWAP[5] <> 0 THEN

IF VWAP >= VWAP[5] THEN

Slope = (VWAP - VWAP[5]) / VWAP[5]

ELSIF VWAP < VWAP[5] THEN

Slope = (VWAP - VWAP[5]) / VWAP

ENDIF

caVwap6 = Slope < 35/10000

ENDIF

IF PlageOKS0 AND VWAP <> 0 AND VWAP[80] <> 0 THEN

IF VWAP >= VWAP[80] THEN

Slope = (VWAP - VWAP[80]) / VWAP[80]

ELSIF VWAP < VWAP[80] THEN

Slope = (VWAP - VWAP[80]) / VWAP

ENDIF

cvVwap0 = Slope < 100/10000

ELSE

cvVwap0 = 1

ENDIF

IF PlageOKS1 AND VWAP <> 0 AND VWAP[60] <> 0 THEN

IF VWAP >= VWAP[60] THEN

Slope = (VWAP - VWAP[60]) / VWAP[60]

ELSIF VWAP < VWAP[60] THEN

Slope = (VWAP - VWAP[60]) / VWAP

ENDIF

cvVwap1 = Slope < 5/10000

ELSE

cvVwap1 = 1

ENDIF

IF PlageOKS2 AND VWAP <> 0 AND VWAP[5] <> 0 THEN

IF VWAP >= VWAP[5] THEN

Slope = (VWAP - VWAP[5]) / VWAP[5]

ELSIF VWAP < VWAP[5] THEN

Slope = (VWAP - VWAP[5]) / VWAP

ENDIF

cvVwap2 = Slope < 5/10000

ELSE

cvVwap2 = 1

ENDIF

IF PlageOKS3 AND VWAP <> 0 AND VWAP[5] <> 0 THEN

IF VWAP >= VWAP[5] THEN

Slope = (VWAP - VWAP[5]) / VWAP[5]

ELSIF VWAP < VWAP[5] THEN

Slope = (VWAP - VWAP[5]) / VWAP

ENDIF

cvVwap3 = Slope < 5/10000

ELSE

cvVwap3 = 1

ENDIF

IF PlageOKS4 AND VWAP <> 0 AND VWAP[10] <> 0 THEN

IF VWAP >= VWAP[10] THEN

Slope = (VWAP - VWAP[10]) / VWAP[10]

ELSIF VWAP < VWAP[10] THEN

Slope = (VWAP - VWAP[10]) / VWAP

ENDIF

cvVwap4 = Slope < 10/10000

ELSE

cvVwap4 = 1

ENDIF

IF PlageOKS5 AND VWAP <> 0 AND VWAP[30] <> 0 THEN

IF VWAP >= VWAP[30] THEN

Slope = (VWAP - VWAP[30]) / VWAP[30]

ELSIF VWAP < VWAP[30] THEN

Slope = (VWAP - VWAP[30]) / VWAP

ENDIF

cvVwap5 = Slope < 5/10000

ELSE

cvVwap5 = 1

ENDIF

//FILTRE : TAILLE DE BOUGIE ET VOLATILITE

CandleOKL = abs(open-close)<(65/10000)*close and AverageTrueRange[100](close)<=105

CandleOKS = abs(open-close)<(62/10000)*close and AverageTrueRange[100](close)<=110

// LONGS

IF LongsOK = 1 THEN

IF not longonmarket THEN

IF PlageOKL1 and CtimeAchat1 THEN

HautRange1 = highest[40](high)

c1 = close > HautRange1[1]

c2 = close[1] > HautRange1[2]

c3 = average[40](close) > average[50](close) AND average[50](close) > average[195](close)

c3bis = RSI[8] < 94 and RSI[18] > 48

IF c1 and c2 and c3 and c3bis and CtimeAchat1 and not onmarket and CandleOKL and CaPrevDay1 and Cam1 and caVwap1 THEN

Buy n shares at market

SET STOP %LOSS 0.65

SET TARGET %PROFIT 1

ENDIF

ENDIF

IF PlageOKL2 and CtimeAchat2 THEN

HautRange2 = highest[40](high)

c4 = close > HautRange2[1]

c5 = close[1] > HautRange2[2]

c6 = average[5](close) > average[15](close) AND average[15](close) > average[50](close)

c6bis = RSI[4] < 98

IF c4 and c5 and c6 and c6bis and CtimeAchat2 and not onmarket and CandleOKL and CaPrevDay2 and Cam2 and caVwap2 THEN

Buy n shares at market

SET STOP %LOSS 0.6

SET TARGET %PROFIT 1

ENDIF

ENDIF

IF PlageOKL3 and CtimeAchat3 THEN

HautRange3 = highest[58](high)

c7 = close > HautRange3[1]

c8 = close[1] > HautRange3[2]

c9 = average[20](close) > average[40](close) AND average[40](close) > average[100](close)

c9bis = RSI[6] < 96

IF c7 and c8 and c9 and c9bis and CtimeAchat3 and not onmarket and CandleOKL and CaPrevDay3 and Cam3 and caVwap3 THEN

Buy n shares at market

SET STOP %LOSS 0.6

SET TARGET %PROFIT 1

ENDIF

ENDIF

IF PlageOKL4 and CtimeAchat4 THEN

HautRange4 = highest[5](high)

c10 = close > HautRange4[1]

c11 = close[1] > HautRange4[2]

c12 = average[70](close) > average[60](close)

c12bis = RSI[12] < 82

IF c10 and c11 and c12 and c12bis and CtimeAchat4 and not onmarket and CandleOKL and CaPrevDay4 and Cam4 and caVwap4 THEN

Buy n shares at market

SET STOP %LOSS 0.5

SET TARGET %PROFIT 1

ENDIF

ENDIF

IF PlageOKL5 and CtimeAchat5 THEN

HautRange5 = highest[50](high)

c13 = close > HautRange5[1]

c14 = close[1] > HautRange5[2]

c15 = average[20](close) > average[35](close) AND average[35](close) > average[215](close)

c15bis = RSI[6] < 84

IF c13 and c14 and c15 and c15bis and CtimeAchat5 and not onmarket and CandleOKL and CaPrevDay5 and Cam5 and caVwap5 THEN

Buy n shares at market

SET STOP %LOSS 0.5

SET TARGET %PROFIT 1

ENDIF

ENDIF

IF PlageOKL6 and CtimeAchat6 THEN

HautRange6 = highest[54](high)

c16 = close > HautRange6[1]

c17 = close[1] > HautRange6[2]

c18 = average[20](close) > average[25](close) AND average[25](close) > average[165](close)

c18bis = RSI[6] < 84

IF c16 and c17 and c18 and c18bis and CtimeAchat6 and not onmarket and CandleOKL and CaPrevDay6 and Cam6 and caVwap6 THEN

Buy n shares at market

SET STOP %LOSS 0.35

SET TARGET %PROFIT 1

ENDIF

ENDIF

ENDIF

ENDIF

// SORTIE LONGS LE VENDREDI SOIR À 21H30

IF time >= 213000 and longonmarket and DayOfWeek=5 THEN

sell at market

ENDIF

// GESTION DU BREAKEVEN - Longs

IF Breakeven1 = 1 THEN

nivBElong = BEniveauLong/10000*tradeprice(1)

IF longonmarket and close-tradeprice(1)>=nivBElong THEN

Breakevenlevel = tradeprice(1) + (BELongKeep/10000*tradeprice(1))

BElongactif = 1

ENDIF

IF BElongactif = 1 THEN

sell at Breakevenlevel stop

ENDIF

ENDIF

//STAGNATION (LONGS) : SORTIE SI PERTE >= 120 pips APRES 48 BOUGIES

floatingprofit = close-tradeprice(1)

IF longonmarket and floatingprofit<=-120 and BarIndex-TradeIndex>48 THEN

sell at market

ENDIF

TIMEFRAME(default)

if not onmarket then

partial=0

endif

// sortie partielle

if longonmarket and positionperf>.6/100 and partial=0 then

sell countofposition/2 contract at market

partial = 1

endif

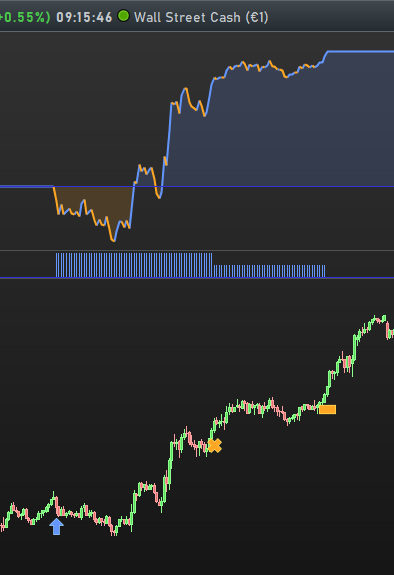

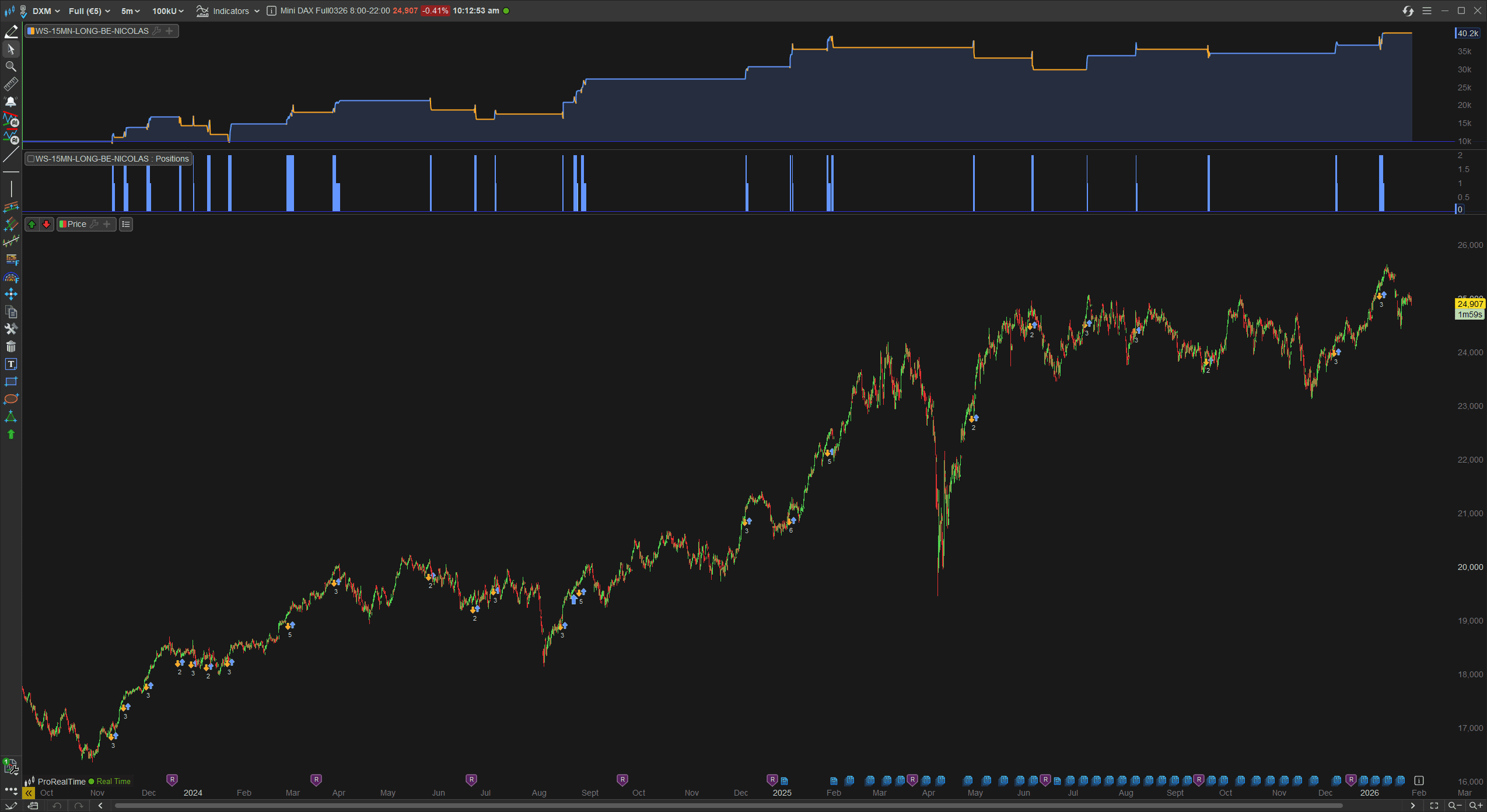

voici un export d’une plateforme PRT d’un compte IG demo pour vérifier l’export et re-import.

autre export d’une plateforme PRT software.

Merci beaucoup pour ces exemples ! Si je comprends bien : quand je veux que l’une de mes variables soit calculée en 1 minute, le graphe par défaut doit être affiché en 1 minute (ce qui limite l’historique de BT à 200 000 bougies (6 mois) dans ma version de PRT). Dans ce cas je peux choisir de calculer d’autres variables en UT différentes, cela fonctionne. Par contre si je veux que mon UT de base soit le 5 minutes, pour avoir un historique de 1 ou 2 ans, je ne peux pas programmer de variable en 1 minute, mais uniquement dans des UT plus longues que le 5 minutes.

C’est bien cela ?

C’est dommage, car le suivi en 1 minute pourrait être très intéressant pour les stops suiveurs par exemple, dans une stratégie basée en 5 ou 15 minutes…

Oui c’est bien cela, on ne peut accéder qu’aux données des unités de temps supérieures et non celles inférieures. Donc ici toutes les UT au dessus de 1-minute sont accessibles et pas celles en dessous (les UT en secondes en l’occurrence).

OK ! Merci pour ces explications !