I tried this :

if close[val]>0 and close[val]<close[val[1]] and close[val[1]]>0 and close[val[1]]>close[val[2]] then

IF LONGONMARKET THEN

SELL 1 SHARES AT MARKET

SELLSHORT 1 SHARES AT MARKET

ELSE

SELLSHORT 1 SHARES AT MARKET

ENDIF

ENDIF

if close[val]<0 and close[val]>close[val[1]] and close[val[1]]<0 and close[val[1]]<close[val[2]]then

IF SHORTONMARKET THEN

EXITSHORT 1 SHARES AT MARKET

BUY 1 SHARES AT MARKET

ELSE

BUY 1 SHARES AT MARKET

ENDIF

ENDIF

but still doesn’t work…

How about below, also try including volume also?

if Close > average[200](close) AND close[val]<0 and close[val]>close[val[1]] and close[val[1]]<0 and close[val[1

Ok, I finally made it work my way, then I added your code (+5% win ratio), then I added volume, it didn’t change much, same thing for volatility.

I’ve got good %win ratio but awful win/loss ratio, any idea how to improve this ?

What about adding a momentum indicator, e.g. Chande Momentum Index or similar; RSI maybe??

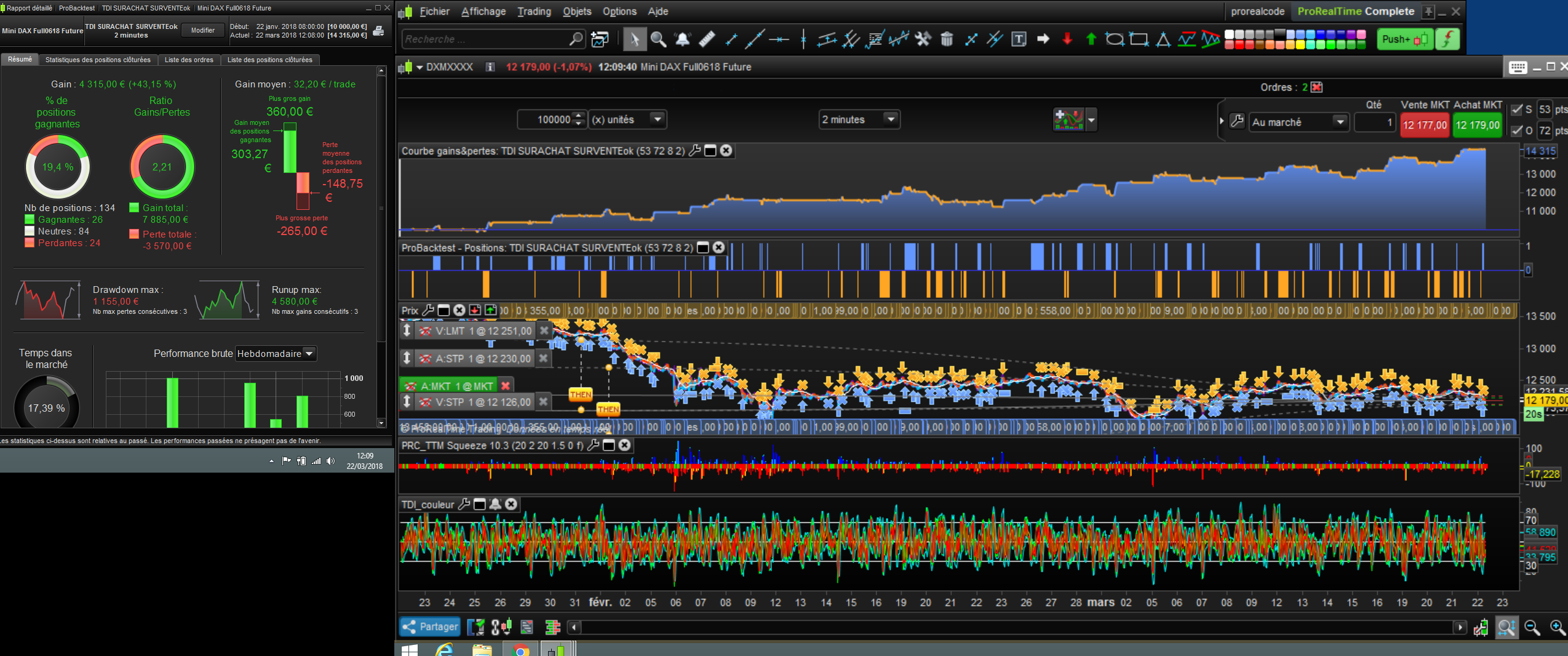

OK, eventually I filtered it with supertrend extended (see attached), looks better now, I’ll try to push it.

Here’s the code :

a = 89 (sl)

b = 28 (tp)

c = 20

d = 1

// Trend Surfer DAX Modified

DEFPARAM CumulateOrders = False

// code-Parameter

DEFPARAM FlatBefore = 080500

DEFPARAM FlatAfter = 180000

// DAX trading window

ONCE BuyTimeMorning = 080500

//ONCE SellTimeMorning = 110000

//ONCE BuyTimeAfternoon = 130000

ONCE SellTimeAfternoon = 173000

// trading parameter

ONCE sl = a

ONCE tp = b

ONCE lengthKC=20

// position management during trading window

IF (Time >= BuyTimeMorning AND Time <= SellTimeAfternoon) THEN

value = (Highest[lengthKC](high)+Lowest[lengthKC](low)+average[lengthKC](close))/3

val = linearregression[lengthKC](close-value)

indicator1, ignored = CALL "PRC_SuperTrend Extended"[2.236, 66, 1, 10]

ignored, indicator2 = CALL "PRC_SuperTrend Extended"[2.236, 66, 1, 10]

c1 = (indicator1 < indicator2)

c2 = (indicator1 > indicator2)

if val>0 and val[1]>0 and val[2]>0 and val<val[1] and val[1]>val[2] and c2 then

IF LONGONMARKET THEN

SELL 1 SHARES AT MARKET

SELLSHORT 1 SHARES AT MARKET

ELSE

SELLSHORT 1 SHARES AT MARKET

ENDIF

ENDIF

if val<0 and val[1]<0 and val[2]<0 and val>val[1] and val[1]<val[2] and c1 then

IF SHORTONMARKET THEN

EXITSHORT 1 SHARES AT MARKET

BUY 1 SHARES AT MARKET

ELSE

BUY 1 SHARES AT MARKET

ENDIF

ENDIF

StopdistanceBreakeven = c

NormalStop = sl

nb = barindex - tradeindex

minprice = lowest[nb + 1](Low)

maxprice = highest[nb + 1](High)

If longonmarket then

If maxprice >= positionprice + StopdistanceBreakeven then

sell at (positionprice + 1 ) stop

else

sell at positionprice - NormalStop stop

endif

endif

If shortonmarket then

If minprice <= positionprice - StopdistanceBreakeven then

exitshort at (positionprice - 1) stop

else

exitshort at positionprice + NormalStop stop

endif

endif

// stop and profit

//SET STOP pLOSS sl

SET TARGET pPROFIT tp

ENDIF

chears !

i just saw that i tested it on 10 000 bars, its still good thow, but not so good…

Again, it doesn’t do what I want, which also means it can be even more profitable.

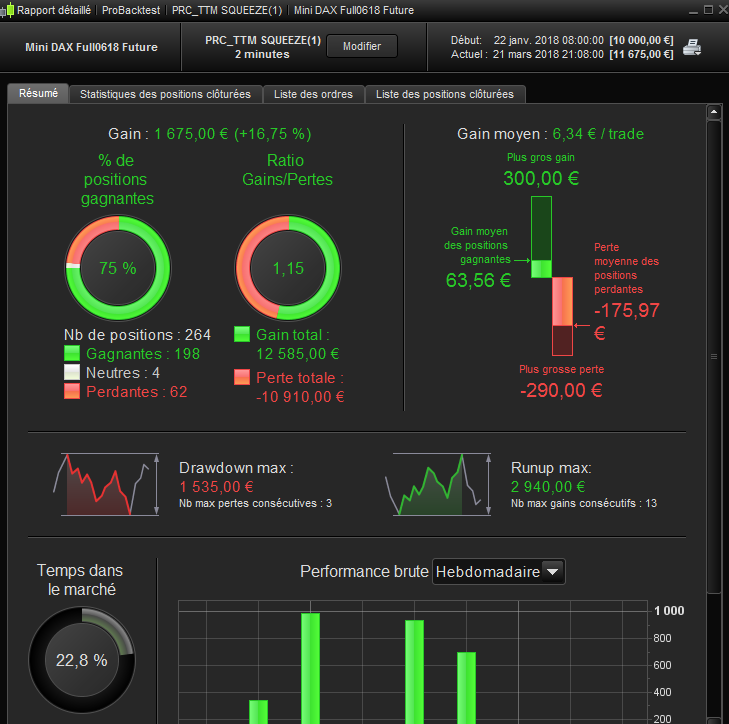

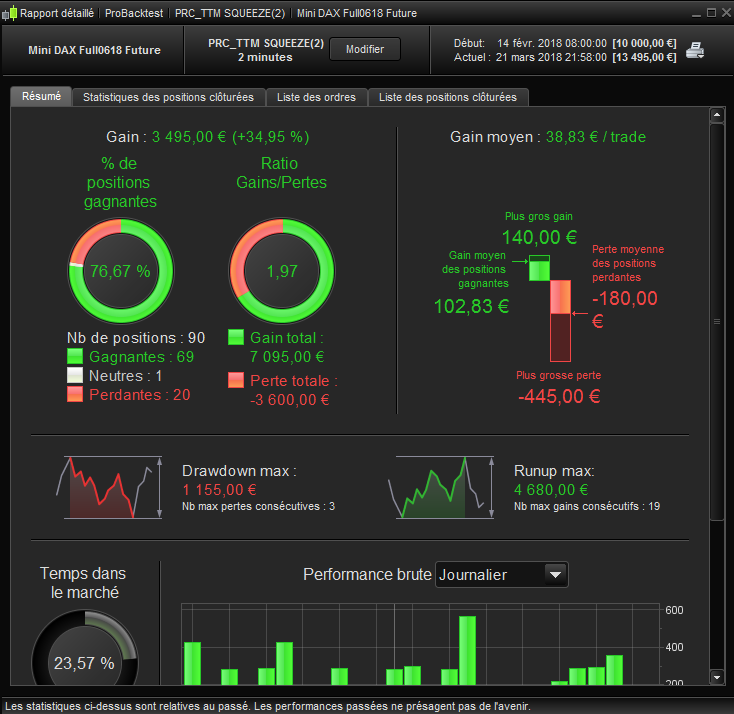

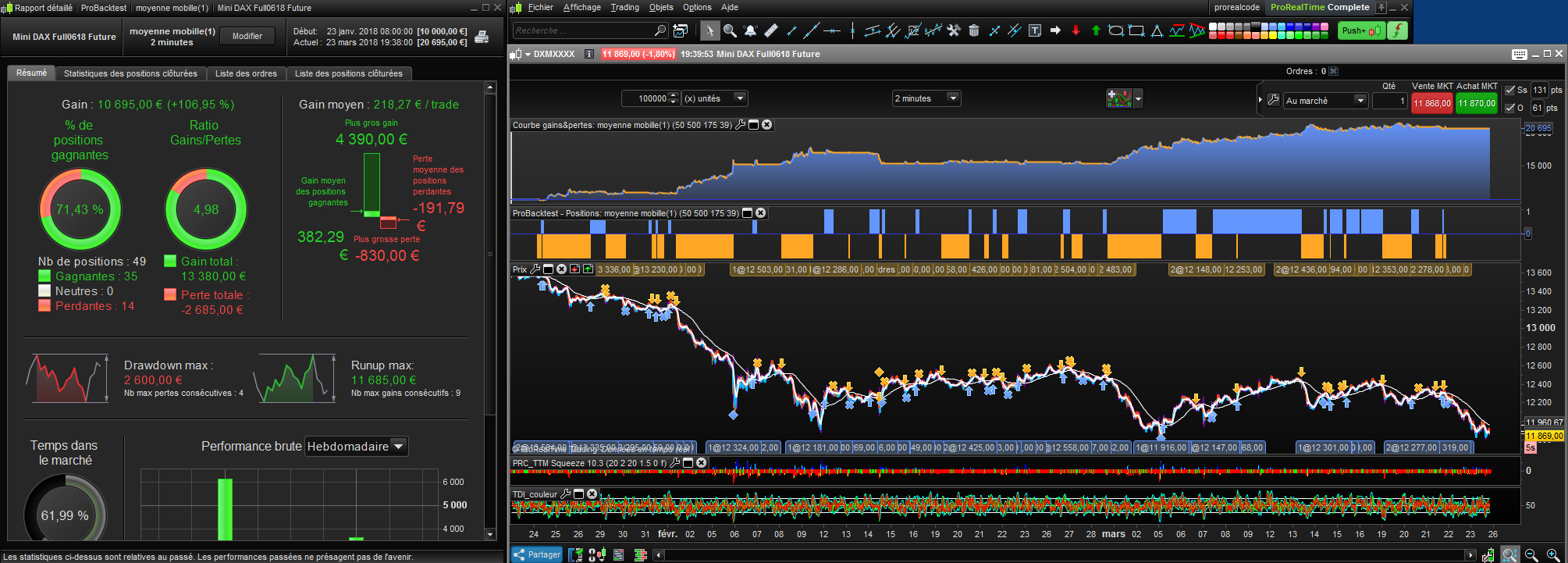

See picture attached, any suggestions are welcome.

I cooked another one that seems to work : ut 2min, trades on TDI overbought/oversold.

Neutral trades are in fact winners of 1 pip (spread + 1)

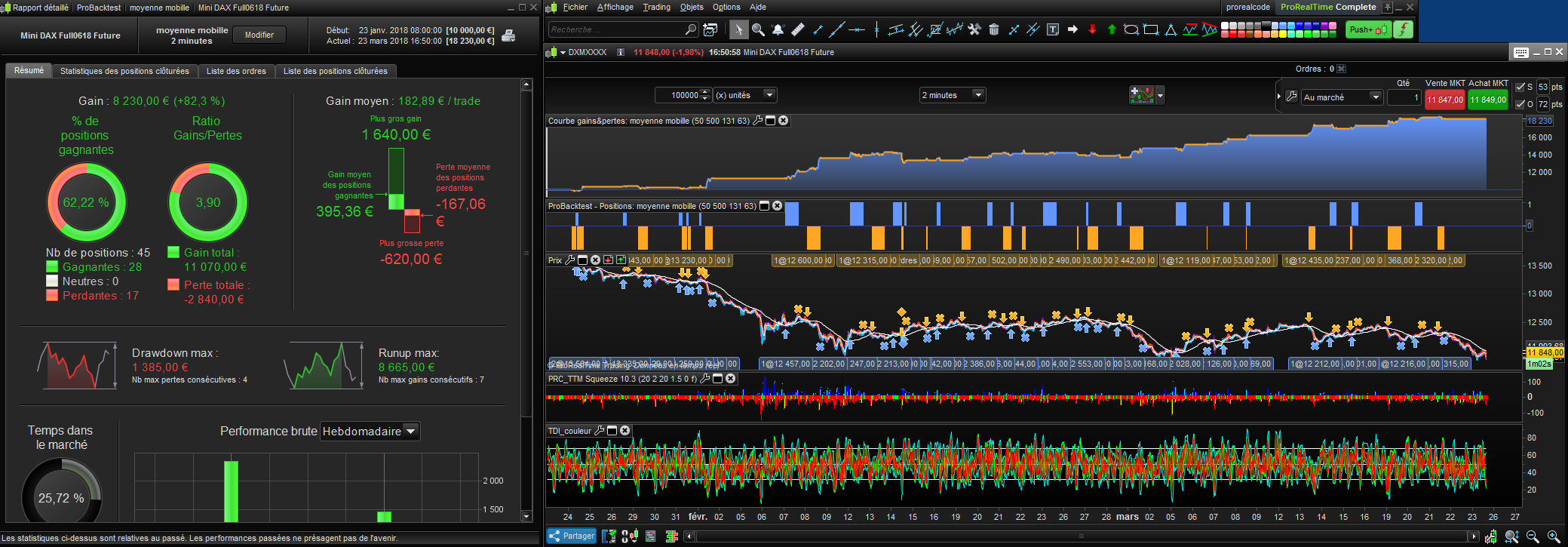

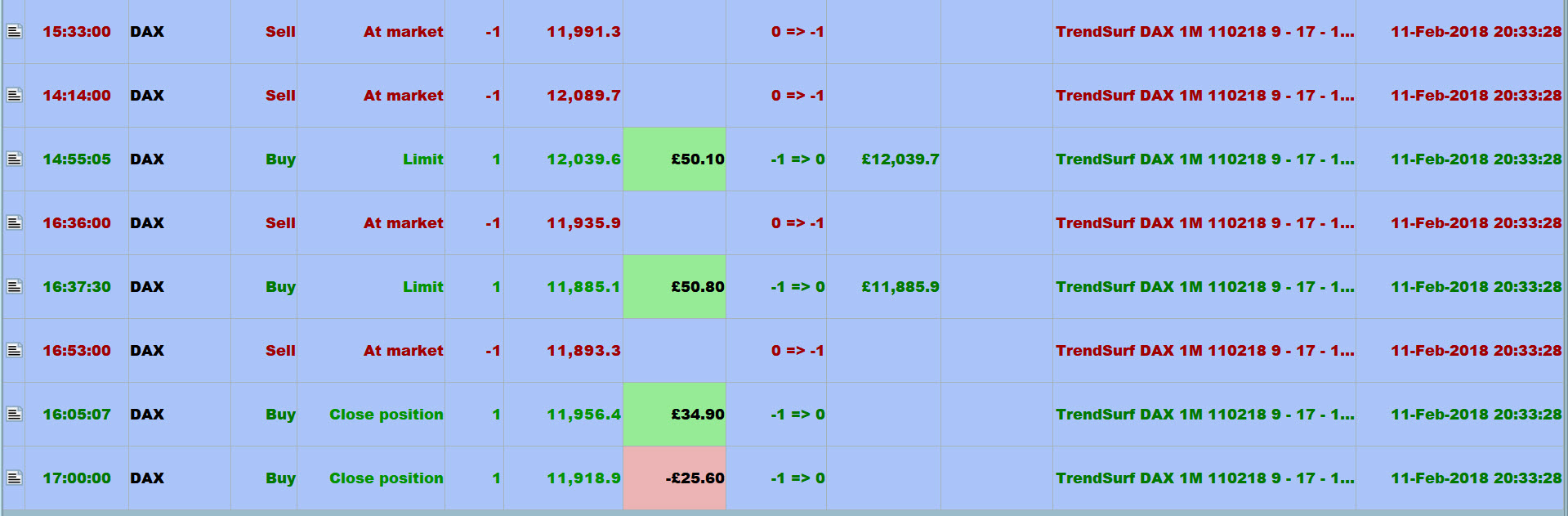

Here is an other one, much more profitable, based on moving avegerage 50 and 500 (optimized) crossing.

Sometimes, the simpler, the better. I can’t go back further 3 months thow…

Even better if we make it swinng trading.

Hi again !

I’m trying to make some tweaks on the last code I posted, but I need help…

I took nicolas’ trailing code here https://www.prorealcode.com/blog/trading/complete-trailing-stop-code-function/

I’m keeping the break even part, but I want the trailing step to be the last high or low (if we go short or long) of “n” or “m” periods (n and m being different for long or short and to be optimized).

here’s what I changed, but it doesn’t seem to work :

trailingstart = 39

clow = tradeprice - (lowest[m](low))

chigh= (highest[n](high))-tradeprice

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart*pipsize THEN

newSL = tradeprice(1)+clow*pipsize

ENDIF

//next moves

IF newSL>0 AND close-newSL>=clow*pipsize THEN

newSL = newSL+clow*pipsize

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart*pipsize THEN

newSL = tradeprice(1)-chigh*pipsize

ENDIF

//next moves

IF newSL>0 AND newSL-close>=chigh*pipsize THEN

newSL = newSL-chigh*pipsize

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

//************************************************************************

GRAPH newSL as "trailing"

It is defined to 39, I missed it when I copied/pasted the code, I edited the post to correct that, sorry

Aha I thought my eyes were deceiving me so I nipped in and deleted my comment re the Trailingstart! 🙂 🙂

Have you use GRAPH to see what the value of tradeprice – (lowest[m](low)) is? Because if it is > Trailing start then it wouldn’t work anyway??

ok I am going to look closer, I ‘ll report back when I shall find the error.

Meanwhile, I added pyramiding code I founded in nicolas’ advanced training videos,

I tweaked it so that position size increases also after a win (and not just deacreases after a loss).

Win/loss ratio jumped from 4,73 to 5,71.

here’s the code to put at the begining :

taille=1

for i = 1 to 2 do

if positionperf(i)<0 then

taille=taille-1

else

if taille<5 then

taille=taille+1

endif

endif

next

Please could you put your latest full code on here and then I can see if I can offer any improvements, but doubt I will as you are doing great on your own … your code has done me well today!

Thank You

GraHal