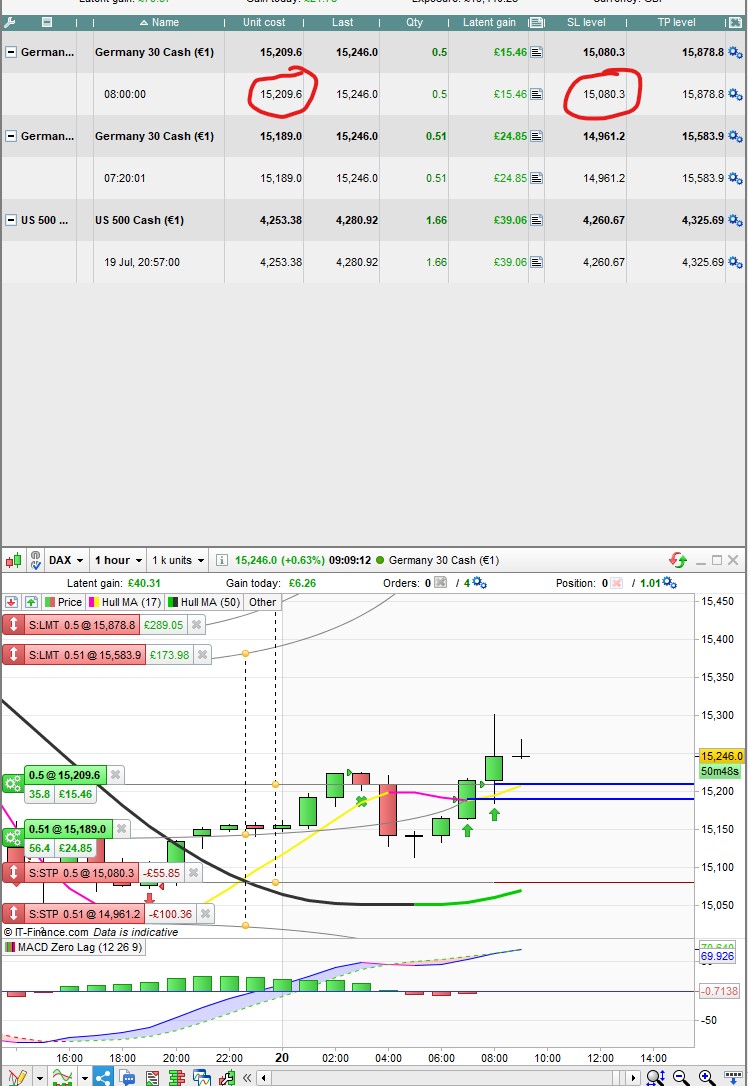

The attached shows a position I have open at the moment on a 1 hour TF.

Opened at 8:00 15209 with the trail to start after a high of 0.56% (15294.8)

In the first bar it hits a high of 15301 and at the start of the 9:00 bar it should have moved to breakeven … but it didn’t.

This is the trail that I’m using (courtesy of Paul):

once trailingstoptype1= 1

if trailingstoptype1 then

//====================

trailingpercentlong = 0.56 // %

trailingpercentshort = 0.49 // %

once acceleratorlong = 0.08 // [1] default; always > 0 (i.e. 0.5-3)

once acceleratorshort= 0.09 // 1 = default; always > 0 (i.e. 0.5-3)

ts2sensitivity = 2 // 1 = close 2 = High/Low 3 = Low/High 4 = typicalprice (not use once)

//====================

once steppercentlong = (trailingpercentlong/10)*acceleratorlong

once steppercentshort = (trailingpercentshort/10)*acceleratorshort

if onmarket then

trailingstartlong = positionprice*(trailingpercentlong/100)

trailingstartshort = positionprice*(trailingpercentshort/100)

trailingsteplong = positionprice*(steppercentlong/100)

trailingstepshort = positionprice*(steppercentshort/100)

endif

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

newsl = 0

mypositionprice = 0

endif

positioncount = abs(countofposition)

if newsl > 0 then

if positioncount > positioncount[1] then

if longonmarket then

newsl = max(newsl,positionprice * newsl / mypositionprice)

else

newsl = min(newsl,positionprice * newsl / mypositionprice)

endif

endif

endif

if ts2sensitivity=1 then

ts2sensitivitylong=close

ts2sensitivityshort=close

elsif ts2sensitivity=2 then

ts2sensitivitylong=high

ts2sensitivityshort=low

elsif ts2sensitivity=3 then

ts2sensitivitylong=low

ts2sensitivityshort=high

elsif ts2sensitivity=4 then

ts2sensitivitylong=typicalprice

ts2sensitivityshort=typicalprice

endif

if longonmarket then

if newsl=0 and ts2sensitivitylong-positionprice>=trailingstartlong*pipsize then

newsl = positionprice+trailingsteplong*pipsize

endif

if newsl>0 and ts2sensitivitylong-newsl>=trailingsteplong*pipsize then

newsl = newsl+trailingsteplong*pipsize

endif

endif

if shortonmarket then

if newsl=0 and positionprice-ts2sensitivityshort>=trailingstartshort*pipsize then

newsl = positionprice-trailingstepshort*pipsize

endif

if newsl>0 and newsl-ts2sensitivityshort>=trailingstepshort*pipsize then

newsl = newsl-trailingstepshort*pipsize

endif

endif

if barindex-tradeindex>1 then

if longonmarket then

if newsl>0 then

sell at newsl stop

endif

if newsl>0 then

if low crosses under newsl then

sell at market

endif

endif

endif

if shortonmarket then

if newsl>0 then

exitshort at newsl stop

endif

if newsl>0 then

if high crosses over newsl then

exitshort at market

endif

endif

endif

endif

mypositionprice = positionprice

endif

Any thoughts on this?

Because in lines 13, 48 and 51 (the same for the Short direction) you are using a reference to a price (trailingstartlong), but in lines 48 and 51 you added *PIPSIZE, which is not correct, both are prices so no conversion is needed.

Simply remove it.

Thanks Roberto, i’ll try that 👍👍👍

Just to clarify, I should remove *pipsize from this entire section (8 occurrences) ?

if longonmarket then

if newsl=0 and ts2sensitivitylong-positionprice>=trailingstartlong*pipsize then

newsl = positionprice+trailingsteplong*pipsize

endif

if newsl>0 and ts2sensitivitylong-newsl>=trailingsteplong*pipsize then

newsl = newsl+trailingsteplong*pipsize

endif

endif

if shortonmarket then

if newsl=0 and positionprice-ts2sensitivityshort>=trailingstartshort*pipsize then

newsl = positionprice-trailingstepshort*pipsize

endif

if newsl>0 and newsl-ts2sensitivityshort>=trailingstepshort*pipsize then

newsl = newsl-trailingstepshort*pipsize

Yes, since at the beginning all started with a PRICE, not PIPS.

You can use GRAPH to monitor newsl, trailingstartlong, etc…

Actually NEWSL can be better monitored with GRAPHONPRICE.

thanked this post

Ok, what about this one, should i remove *pointsize at lines 78, 80, 82 and 88, 90, 92 ?

once trailingstopATR = 0

if trailingstopATR = 1 then

//====================

once tsincrements = 0 // set to 0 to ignore tsincrements

once tsminatrdist = 0

once tsatrperiod = 14 // ts atr parameter

once tsminstop = 5 // ts minimum stop distance

tssensitivity = 2 // 1 = close 2 = High/Low 3 = Low/High 4 = typicalprice (not use once)

//====================

if barindex=tradeindex then

trailingstoplong = 6 // ts atr distance

trailingstopshort = 6 // ts atr distance

else

if longonmarket then

if tsnewsl>0 then

if trailingstoplong>tsminatrdist then

if tsnewsl>tsnewsl[1] then

trailingstoplong=trailingstoplong

else

trailingstoplong=trailingstoplong-tsincrements

endif

else

trailingstoplong=tsminatrdist

endif

endif

endif

if shortonmarket then

if tsnewsl>0 then

if trailingstopshort>tsminatrdist then

if tsnewsl<tsnewsl[1] then

trailingstopshort=trailingstopshort

else

trailingstopshort=trailingstopshort-tsincrements

endif

else

trailingstopshort=tsminatrdist

endif

endif

endif

endif

tsatr=averagetruerange[tsatrperiod]((close/10))/1000

//tsatr=averagetruerange[tsatrperiod]((close/1)) // (forex)

tgl=round(tsatr*trailingstoplong)

tgs=round(tsatr*trailingstopshort)

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

tsmaxprice=0

tsminprice=close

tsnewsl=0

mypositionpriceatr = 0

endif

positioncountatr = abs(countofposition)

if tsnewsl > 0 then

if positioncountatr > positioncountatr[1] then

if longonmarket then

tsnewsl = max(tsnewsl,positionprice * tsnewsl / mypositionpriceatr)

else

tsnewsl = min(tsnewsl,positionprice * tsnewsl / mypositionpriceatr)

endif

endif

endif

if tssensitivity=1 then

tssensitivitylong=close

tssensitivityshort=close

elsif tssensitivity=2 then

tssensitivitylong=high

tssensitivityshort=low

elsif tssensitivity=3 then

tssensitivitylong=low

tssensitivityshort=high

elsif tssensitivity=4 then

tssensitivitylong=typicalprice

tssensitivityshort=typicalprice

endif

if longonmarket then

tsmaxprice=max(tsmaxprice,tssensitivitylong)

if tsmaxprice-positionprice>=tgl*pointsize then

if tsmaxprice-positionprice>=tsminstop then

tsnewsl=tsmaxprice-tgl*pointsize

else

tsnewsl=tsmaxprice-tsminstop*pointsize

endif

endif

endif

if shortonmarket then

tsminprice=min(tsminprice,tssensitivityshort)

if positionprice-tsminprice>=tgs*pointsize then

if positionprice-tsminprice>=tsminstop then

tsnewsl=tsminprice+tgs*pointsize

else

tsnewsl=tsminprice+tsminstop*pointsize

endif

endif

endif

if longonmarket then

if tsnewsl>0 then

sell at tsnewsl stop

endif

if tsnewsl>0 then

if low crosses under tsnewsl then

sell at market // when stop is rejected

endif

endif

endif

if shortonmarket then

if tsnewsl>0 then

exitshort at tsnewsl stop

endif

if tsnewsl>0 then

if high crosses over tsnewsl then

exitshort at market // when stop is rejected

endif

endif

endif

mypositionpriceatr = positionprice

endif

Yes, because tsatr is a price (range) as well as all the other variables.

The code is based on PRICE, not on PIPS, so all that refers to pips is incorrect.

Lines 13 and 14 are a bit subtle, they are set as prices (as from their comments), but that is fine for indices where the price-to-pips ratio is 1:1 (Dax, SP, ….) but when used with FX pirs it wouldn’t be correct. In This case you should multiply 6 by PIPSIZE to make sure the numeric constant is converted to a price (divide by PIPSIZE, or POINTSIZE, the other way round that is when converting a price to pips, instead).

Thanks loads Roberto, I think that explains a lot of odd behaviour. I never trade Forex so I’ll leave lines 13, 14 as they are.

😎

Actually if you’re using it with Dax, PIPSIZE should make no difference.

I need to test it more, to monitor HIGH and LOW more in depth.

I think it’s because it takes one candle for any system status constant to be updated, so the HIGH at 08:00 could not be detected, while the high at 09:00 was.

From your pic I cannot see any detail and I could not replicate your trades, but I think this can be the sole reason.

I suggest that you add these lines to your code, to better debug it:

graph steppercentlong

GraphOnPrice trailingstartlong + positionprice coloured(255,0,0,255)

GraphOnPrice trailingstartlong + positionprice coloured(255,0,0,255)

GraphOnPrice NewSL coloured(0,128,0,140)

The high of 15301.5 was hit at 08:14 (having opened at 08:00).

Running a backtest (having removed *pipsize) shows a loss for that trade, but it has the entry at 15215.7

The graph shows “trailingstartlong + positionprice = 15300.9” which would be correct (15215.7 + .56%) and allowing for spread, the high of 15301.5 doesn’t clear it.

But that doesn’t explain why my live trade (actually 15209.6) failed to breakeven after a high of 15294.7

With or without *pipsize seems to make no difference to backtests.

I could only guess, as I could not replicate your trades without the code.

Non fa niente, I’ve decided not to continue with that algo anyway. The other places I’m using it seem to work fine – all shorter TFs, 2m, 5m etc, so may be just a blip with the 1 hour TF.

Maybe by the time it got to the next candle it had ‘forgotten’ that the high had been reached 😁

Actually this happend to me with the same trail code. I got the same algo on different accounts and the trailing did move on one account but not the other. The price went the profitable way and it still did not move. Then the position got held over the weekend and when markets reopened on monday the algo updated its stop on both accounts. I dont think there was a visual bug (never happend before atleast?). It was with the *pointsize trailing.

This has happend 2 times before (this time explained here and one more time). So if I remove *pointsize the issue should be solved?