Actually I’ve got another problem with that TS (as posted above). It moves to breakeven then stops, doesn’t trail with the price movement. Obviously it’s working correctly in backtest, but in live trading it gets stuck. Have you seen this as well?

Paul

PaulParticipant

Master

no not yet, it never stops 😉 Your dj 5m mod v5 stopped suddenly with a strange message but I think unrelated to this.

On the 10s frame I use 2 trailingstops in demo and they seem to work alright, but because of using 2 I don’t know which was triggered. I will check.

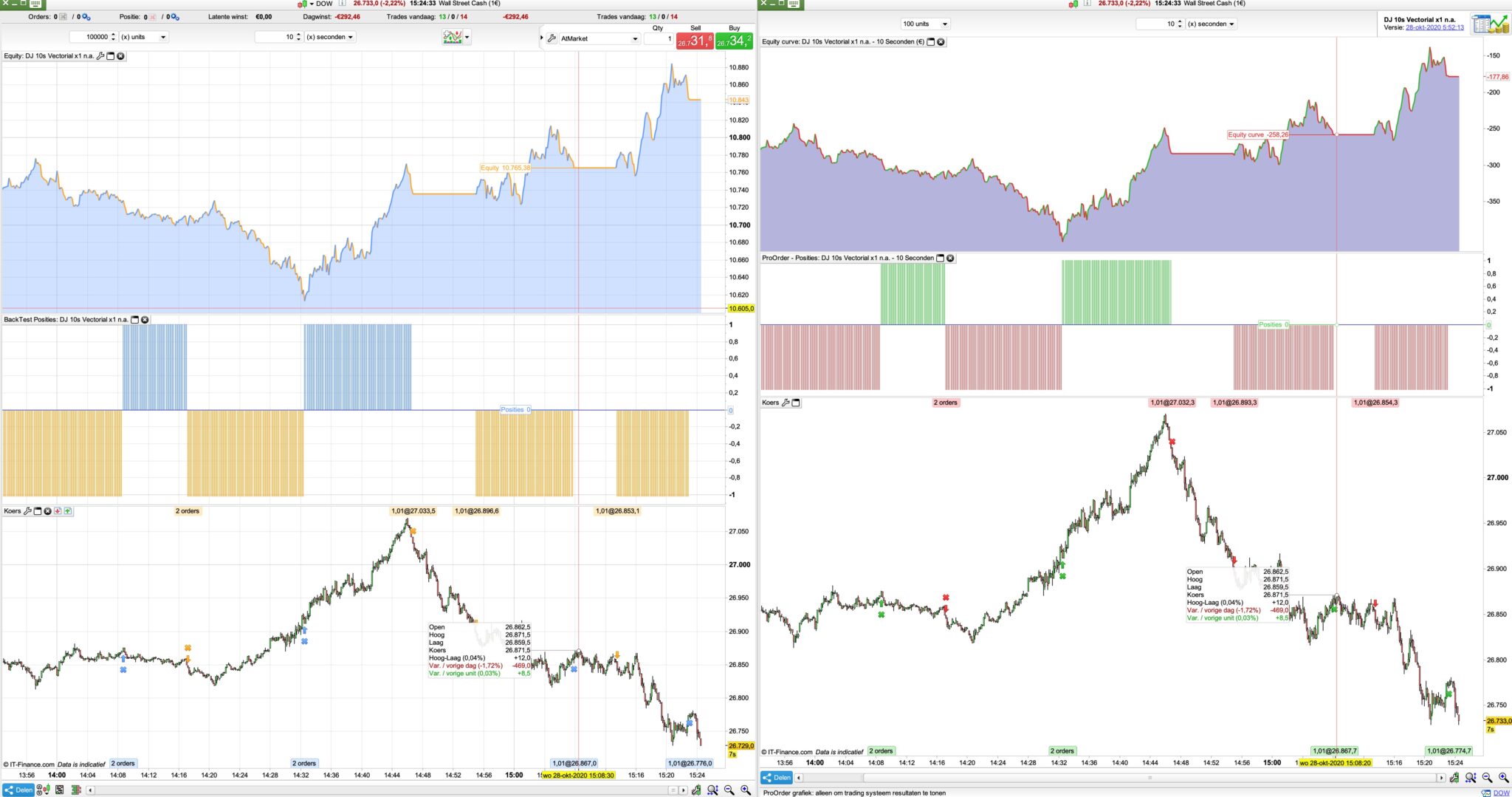

Can you provide a pic?

PaulParticipant

Master

those exits were because the atr trialingstop. I will run it without.

I haven’t got a pic, when I realised it was stuck I closed the position manually. That was with NAS 5m Mod v4S

PaulParticipant

Master

Interested in testing your mod with the atr trailingstop instead to see if it behaves the same live?

I updated that one, and the breakeven too, both to use cumulative positions, it’s included in de maex strategy

yeah, I’ll def check it out when I get a minute, it’s either that or go back to the old %TS I had been using. It’s a bit basic but does the job. The big advantage to yours is the separate values for long/short, so maybe I can build that in to the other one (of Nicolas)

PaulParticipant

Master

Thought of another way if you take that trailingstop (it’s all based on the original)

Duplicate the code and make sure both not overlap each other.

1st one for long and remove all short code, and the second one for short with all long removed.

Should be the same effect (besides the accelerator and sensitivity) but still the advantage for separate values.

My thoughts exactly. Does this look right to you? Seems to test ok

//%trailing stop function

trailingpercentlong = tst // %

trailingpercentshort = tss // %

stepPercentlong = st

stepPercentshort = st2

if onmarket then

trailingstartlong = tradeprice(1)*(trailingpercentlong/100) //trailing will start @trailingstart points profit

trailingstartshort = tradeprice(1)*(trailingpercentshort/100) //trailing will start @trailingstart points profit

trailingsteplong = tradeprice(1)*(stepPercentlong/100) //% step to move the stoploss

trailingstepshort = tradeprice(1)*(stepPercentshort/100) //% step to move the stoploss

endif

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstartlong THEN

newSL = tradeprice(1)+trailingsteplong

ENDIF

//next moves

IF newSL>0 AND close-newSL>trailingsteplong THEN

newSL = newSL+trailingsteplong

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstartshort THEN

newSL = tradeprice(1)-trailingstepshort

ENDIF

//next moves

IF newSL>0 AND newSL-close>trailingstepshort THEN

newSL = newSL-trailingstepshort

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

Not sure about tradeprice(1), whereas you have positionprice. I know the difference, it’s more the (1) I’m unsure of

PaulParticipant

Master

looks good. Tradeprice as written is correct. Only the reset is off when reversing a position, but most of the time the difference is smal to nothing.

Thanks Paul. I added

sensitivity = (low+high+close)/3

instead of close and the performance is back to where it was using your TS – at least in backtest it is. Let’s see how it runs live.

Hi @Paul, I’ve got more problems with this cumulative orders TS. This is the code I’m using:

// %trailing stop function incl. cumulative positions

once trailingstoptype = 1

if trailingstoptype then

//====================

trailingpercentlong = 0.26 // %

trailingpercentshort = 0.26 // %

once acceleratorlong = 0.003 // [1] default; always > 0 (i.e. 0.5-3)

once acceleratorshort= 0.023 // 1 = default; always > 0 (i.e. 0.5-3)

ts2sensitivity = 4 // [1] default [2] hl [3] lh [4] typicalprice (not use once)

//====================

once steppercentlong = (trailingpercentlong/10)*acceleratorlong

once steppercentshort = (trailingpercentshort/10)*acceleratorshort

if onmarket then

trailingstartlong = positionprice*(trailingpercentlong/100)

trailingstartshort = positionprice*(trailingpercentshort/100)

trailingsteplong = positionprice*(steppercentlong/100)

trailingstepshort = positionprice*(steppercentshort/100)

endif

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

newsl = 0

mypositionprice = 0

endif

positioncount = abs(countofposition)

if newsl > 0 then

if positioncount > positioncount[1] then

if longonmarket then

newsl = max(newsl,positionprice * newsl / mypositionprice)

else

newsl = min(newsl,positionprice * newsl / mypositionprice)

endif

endif

endif

if ts2sensitivity=1 then

ts2sensitivitylong=close

ts2sensitivityshort=close

elsif ts2sensitivity=2 then

ts2sensitivitylong=high

ts2sensitivityshort=low

elsif ts2sensitivity=3 then

ts2sensitivitylong=low

ts2sensitivityshort=high

elsif ts2sensitivity=4 then

ts2sensitivitylong=(typicalprice)

ts2sensitivityshort=(typicalprice)

endif

if longonmarket then

if newsl=0 and ts2sensitivitylong-positionprice>=trailingstartlong*pipsize then

newsl = positionprice+trailingsteplong*pipsize

endif

if newsl>0 and ts2sensitivitylong-newsl>=trailingsteplong*pipsize then

newsl = newsl+trailingsteplong*pipsize

endif

endif

if shortonmarket then

if newsl=0 and positionprice-ts2sensitivityshort>=trailingstartshort*pipsize then

newsl = positionprice-trailingstepshort*pipsize

endif

if newsl>0 and newsl-ts2sensitivityshort>=trailingstepshort*pipsize then

newsl = newsl-trailingstepshort*pipsize

endif

endif

if barindex-tradeindex>1 then

if longonmarket then

if newsl>0 then

sell at newsl stop

endif

if newsl>0 then

if low crosses under newsl then

sell at market

endif

endif

endif

if shortonmarket then

if newsl>0 then

exitshort at newsl stop

endif

if newsl>0 then

if high crosses over newsl then

exitshort at market

endif

endif

endif

endif

mypositionprice = positionprice

endif

It goes to breakeven exactly as expected but then stops, doesn’t trail. In the attached image, the breakeven was at the circled candle. 6 candles later the stop is still at 11835.2. the step is .003% so it should move .35 per candle = 11837. Any thoughts on this?

Ok, never mind – I just realized that acceleratorlong = .003 does not mean .003%

I forgot because the other TS I use has a straight % value for trailingstep

This one does trail but sooooo slowly – effectively just holds the position open with the hope of getting to the target. With a setting of .003 I might as well just use the breakeven code.

PaulParticipant

Master

Hi Nonetheless good you found the reason.

I might still mention a few things.

Probably it misses *pointsize at the end, this is the part I changed

trailingstartlong = (tradeprice(countpos)*(trailingpercentlong/100))*pointsize

trailingstartshort = (tradeprice(countpos)*(trailingpercentshort/100))*pointsize

trailingsteplong = (tradeprice(countpos)*(steppercentlong/10000))*pointsize

trailingstepshort = (tradeprice(countpos)*(steppercentshort/10000))*pointsize

I also changed /100 to /10000 so steps are better manageable. Doesn’t change results, but the *pointsize might give different results on i.e 1 euro or 2 dollar DJ charts. (the countpos needs to be changed).

In the past I noticed that using if newsl>0 without defining longonmarket or shortonmarket sometimes, but not always, gave a few strange results, that why I at the end of the code had it specified.

Anyway for this part you could test 2 variations. Should have the same results.

if (shortonmarket and newsl > 0) or (longonmarket and newsl>0) then

if positioncount > positioncount[1] then

if longonmarket then

newsl = max(newsl,positionprice * newsl / mypositionprice)

endif

if shortonmarket then

newsl = min(newsl,positionprice * newsl / mypositionprice)

endif

endif

endif

or

positioncount = abs(countofposition)

if longonmarket and newsl > 0 then

if positioncount > positioncount[1] then

newsl = max(newsl,positionprice * newsl / mypositionprice)

endif

endif

if shortonmarket and newsl > 0 then

if positioncount > positioncount[1] then

newsl = min(newsl,positionprice * newsl / mypositionprice)

endif

endif

Maybe you can keep above as backup if you still find strange things trading live.

That’s great, I’ll try both those options – thanks again!

Do we have a final version of this.

Add to the snippet library?