Finally the last strategy, Strategy #3 of group 3, along with the 3 indicators:

//-------------------------------------------------------------------------

// Klinger-Rvi-Lsma DAX 5 min

//-------------------------------------------------------------------------

DEFPARAM CumulateOrders = False

DEFPARAM FlatBefore = 090000 //no trades before 09:00:00

DEFPARAM FlatAfter = 213000 //no trades after 21:30:00

ONCE nLots = 1 //number of LOTs traded

ONCE TP = 23 //23 pips Take Profit

ONCE SL = 16 //16 pips Stop Loss

RviVal, RviSignal = CALL "RVI by John Ehlers"[7] //7

KlingerVal, KlingerTrigger = CALL "Klinger oscillator"[25,44,55,1] //25,44,55,1 (ema)

LeastSquareEMA = CALL "ELSMA - Least Square EMA"[11,4] //11,4

//***************************************************************************************

IF LongOnMarket THEN

IF close < LeastSquareEMA THEN

SELL AT MARKET //Exit LONGs when MACD reverses southwards

ENDIF

ENDIF

IF ShortOnMarket THEN

IF close > LeastSquareEMA THEN

EXITSHORT AT MARKET //Exit SHORTs when MACD reverses northwards

ENDIF

ENDIF

//***************************************************************************************

trailingstart = 10 //10 trailing will start @trailinstart points profit

trailingstep = 13 //13 trailing step to move the "stoploss"

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart*pipsize THEN

newSL = tradeprice(1)+trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND close-newSL>=trailingstep*pipsize THEN

newSL = newSL+trailingstep*pipsize

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart*pipsize THEN

newSL = tradeprice(1)-trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND newSL-close>=trailingstep*pipsize THEN

newSL = newSL-trailingstep*pipsize

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

//***************************************************************************************

// LONG trades

//***************************************************************************************

a1 = close > open //BULLish bar

a2 = KlingerTrigger CROSSES OVER KlingerVal //Klinger trigger is going north

a3 = RviSignal CROSSES OVER RviVal //RVI long signal occurred

IF a1 AND a2 AND a3 THEN

BUY nLots CONTRACT AT MARKET

ENDIF

//***************************************************************************************

// SHORT trades

//***************************************************************************************

b1 = close < open //BEARish bar

b2 = KlingerTrigger CROSSES UNDER KlingerVal //Klinger trigger is going south

b3 = RviSignal CROSSES UNDER RviVal //RVI short signal occurred

IF b1 AND b2 AND b3 THEN

SELLSHORT nLots CONTRACT AT MARKET

ENDIF

//

SET TARGET PPROFIT TP

SET STOP PLOSS SL

ElSMA indicator:

//-------------------------------------------------//

// ELSMA - Exponential Least Square Moving Average //

//-------------------------------------------------//

DEFPARAM CalculateOnLastBars = 200

Period = MAX(Period, 1)

if NumBars < 1 then

NumBars = 4

endif

LR = LinearRegression[NumBars](close)

AFR = ExponentialAverage[Period](LR)

RETURN AFR

RVI indicator:

// Relative Vigor Index (RVI) by John Ehlers

// Paramètres:

// Per = periods for summation (12 as défault)

DEFPARAM CalculateOnLastBars = 200

diff = close - open

ind1 = (diff + 2*diff[1] + 2*diff[2] + diff[3]) / 6

ind2 = (Range + 2*Range[1] + 2*Range[2] + Range[3]) / 6

cond = Summation[per](ind2)

IF cond = 0 THEN

temp = 0.0001

ELSE

temp = cond

ENDIF

RVI = Summation[per](ind1) / temp

RVIsig = (RVI + 2*RVI[1] + 2*RVI[2] + RVI[3]) / 6

RETURN RVI COLOURED (255, 0, 0) AS"Relative Vigor Index", RVIsig COLOURED (0, 0, 255) AS"Relative Vigor Index Signal"

KLINGER oscillator:

// KLINGER oscillator

// variable AVGTYPE can hold values:

//

// 0 = SMA

// 1 = EMA

// 2 = WMA

// 3 = Wilder MA

// 4 = Triangular MA

// 5 = End point MA

// 6 = Time series MA

//------------------------------------------------

DEFPARAM CalculateOnLastBars = 200

hlc3= (high + low + close)/3

if(hlc3>hlc3[1]) THEN

xTrend = volume * 100

ELSE

xTrend = -volume * 100

ENDIF

if (AvgType < 0) OR (AvgType > 6) then //default to ONE if parameter is

AvgType = 1 // out of range 0-6

endif

xFast = average[FastX,AvgType](xTrend)

xSlow = average[SlowX,AvgType](xTrend)

xKvO = xFast-xSlow

xTrigger = average[TrigLen,AvgType](xKvO)

RETURN xKvO AS "Klinger oscillator", xTrigger AS "trigger"

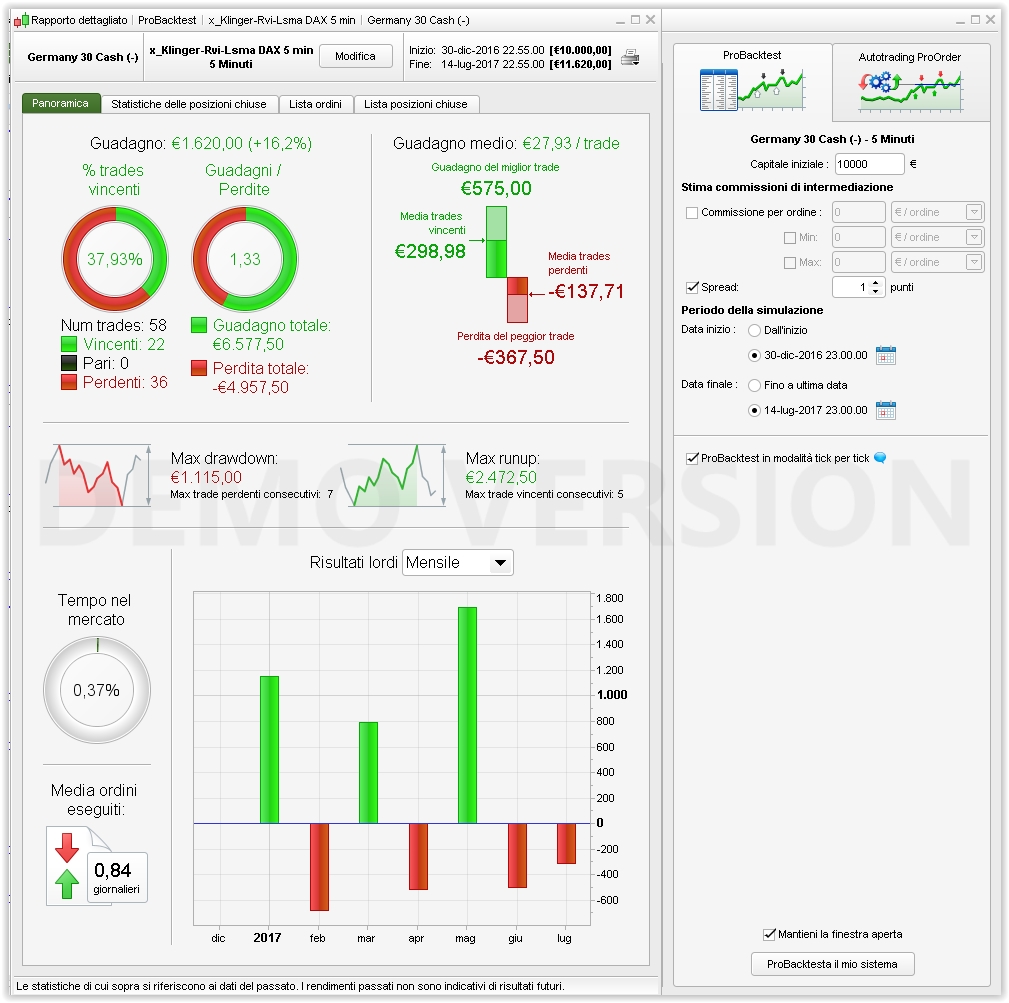

This strategy is not performing like the first two in the group.

Any suggestion for improvements is highly welcome!