Gael

GaelParticipant

Average

Salve,

volevo chiedervi la realizzazione di queste due idee in trading system:

1)

- Buy alla comparsa di un segnale SAR sotto le candele

- Sell alla comparsa di un segnale SAR sopra le candele

- Trailling stop sul segnale SAR, e va a spostarsi alla comparsa del nuovo segnale.

2)

Il secondo trading system è simile al primo, solo che chiude il sistema al raggiungimento del 12 segnale SAR consecutivo. Nel caso i segnali SAR dovessero essere inferiori a 12, il sistema chiude al segnale SAR inverso.

Grazie mille in anticipo

1 / questo sistema è molto semplice da creare con la creazione assistita, hai provato prima? Ad ogni modo, ecco qualcosa con cui puoi giocare:

defparam cumulateorders=false

isar = SAR[0.02,0.02,0.2]

if not longonmarket and close crosses over isar then

buy at market

sell at isar stop

endif

if not shortonmarket and close crosses under isar then

sellshort at market

exitshort at isar stop

endif

if longonmarket then

sell at isar stop

endif

if shortonmarket then

exitshort at isar stop

endif

2 / quel sistema taglia gli ordini quando ISAR è 12 volte consecutive dello stesso colore:

defparam cumulateorders=false

isar = SAR[0.02,0.02,0.2]

if not longonmarket and close crosses over isar then

buy at market

endif

if not shortonmarket and close crosses under isar then

sellshort at market

endif

bcount = summation[12](close>isar)=12

if bcount and longonmarket then

sell at market

endif

scount = summation[12](close<isar)=12

if scount and shortonmarket then

exitshort at market

endif

GaelParticipant

Average

Ho provato prima, ma sono ancora un principiante e volevo avere conferma, comunque grazie mille.

Buona giornata

GaelParticipant

Average

Scusa il disturbo, ma non riesco a metterlo in .itf

Basta creare una nuova strategia e inserire il codice lì, è facile 🙂

GaelParticipant

Average

Mi da la riga 1,6,7,9 con il punto esclamativo se faccio: indicatori –> nuovo –> incolla

Li devi copiare in una strategia non in un indicatore.

Eccoli

Ciao Gael

Visto che sei alle prime armi per aiutarti ti ho creato delle piccole aggiunte che ti verranno utili con il proseguo della tua esperienza che farai nella programmazione.

Ti ho aggiunto Target dinamico (con Atr ) e stop loss in percentuale e numero massimo di barre (oltre il sistema esce dalla posizione).

Il tutto è stato distinto se sono operazioni Long o Short.

Ciao

Buona Fortuna

defparam cumulateorders=false

isarlong = SAR[0.04,0.04,0.6]

isarShort = SAR[0.07,0.07,0.1]

if not longonmarket and close crosses over isarlong then

buy at market

sell at isarlong stop

set target profit 10* averagetruerange[5](close)

set Stop %loss 1.8

endif

if longonmarket then

sell at isarlong stop

endif

if not shortonmarket and close crosses under isarshort then

sellshort at market

exitshort at isarshort stop

set target profit 8* averagetruerange[12](close)

set Stop %loss 1.2

endif

if shortonmarket then

exitshort at isarshort stop

endif

// NUMERO BARRE OTTIMALI

ONCE maxCandlesLongWithProfit = 17 // profitto long

ONCE maxCandlesShortWithProfit = 10 // profitto short

ONCE maxCandlesLongWithoutProfit = 12 // Limite long

ONCE maxCandlesShortWithoutProfit = 9 // Limite short

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

numberCandles = (BarIndex - TradeIndex)

m1 = posProfit > 0 AND numberCandles >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND numberCandles >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND numberCandles >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND numberCandles >= maxCandlesShortWithoutProfit

IF LONGONMARKET AND (m1 OR m3) THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND (m2 OR m4) THEN

EXITSHORT AT MARKET

ENDIF

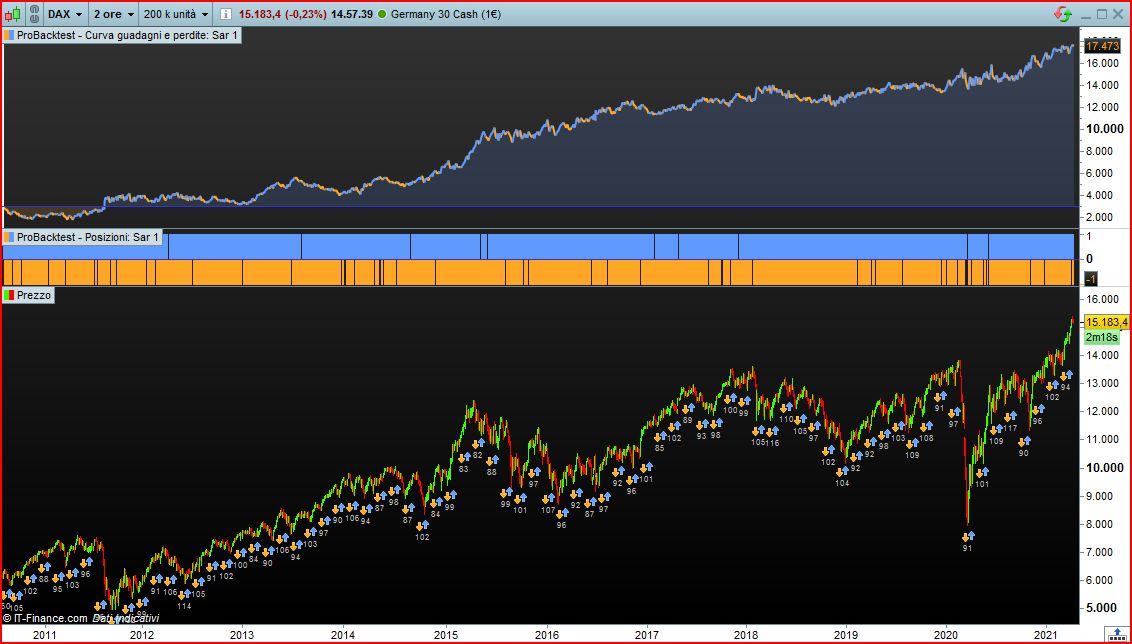

Questi sono i risultati con Dax 2 ore

GaelParticipant

Average

Grazie mille, sembra veramente molto interessante