//the 13th V1.5 /////////////by Joe Szeles//////////////////////

//IDEA BASED ON:

// The13thWarrior_V1.1

// 06.09.2020 (Release 1.1)

// Thomas Geisler

// Sharing ProRealTime knowledge

// https://www.prorealcode.com/library/////

Defparam cumulateorders = false

positionsize=2

myOBVn = 5

myCandle = 1

//Heikin Ashi

ONCE haOpen = OPEN

ONCE haClose = CLOSE

N = 0

IF BARINDEX = 0 THEN

haOpen = OPEN

haClose = CLOSE

ELSIF N = 0 THEN

haClose =(OPEN+HIGH+LOW+CLOSE)/4

haOpen =(haOpen[1]+haClose[1])/2

ENDIF

once tradetype = 1 // [1]long&short;[2]long;[3]short

mm6= average[299]

mm5= average[120]

mm4= average[10]

mm3= average[7]

mm2= average[4]

mm1= average[3]

mm0= average[2]

mm= average[1]

//long

tradelong = mm>mm0 and mm0>mm1 and mm1>mm2 and mm2>mm3 and mm3>mm4 and mm4>mm5 and mm5>mm6

//short

tradeshort = mm<mm0 and mm0<mm1 and mm1<mm2 and mm2<mm3 and mm3<mm4 and mm4<mm5 and mm5<mm6

//Candle-Colour from OBV and HA

IF myCandle = 1 THEN

myOBV = OBV(CLOSE)

myAV = Average[myOBVn](myOBV)

IF myOBV > myAV AND haClose > haOpen and (tradetype=1 or tradetype=2) and tradelong THEN

if not onmarket then

buy positionsize contract at market

endif

endif

if myOBV < myAV AND haClose < haOpen and (tradetype=1 or tradetype=3) and tradeshort THEN

if not onmarket then

sellshort positionsize contract at market

endif

endif

ENDIF

//%trailing stop function

trailingPercent = .278 //org .26

stepPercent = .0155//org .014

if onmarket then

trailingstart = tradeprice(1)*(trailingpercent/100) //trailing will start @trailinstart points profit

trailingstep = tradeprice(1)*(stepPercent/100) //% step to move the stop

endif

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart THEN

newSL = tradeprice(1)+trailingstep

ENDIF

//next moves

IF newSL>0 AND close-newSL>trailingstep THEN

newSL = newSL+trailingstep

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart THEN

newSL = tradeprice(1)-trailingstep

ENDIF

//next moves

IF newSL>0 AND newSL-close>trailingstep THEN

newSL = newSL-trailingstep

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

set stop loss 400

set target profit 1600

Thanks for sharing your idea and yourcode.

Any suggestion about which TF’s and instruments are best best suited for this strategy?

HA candlesticks are used only for entry conditions, not for indicators nor trailing stop, is that correct?

Attached is one possibility … spread = 5, position size = 1

Strangely with 200K spead 5 and position size 1 it doesn’t give any trades before July 2016 ??

On a 2h system, there are probably not bars before that date if tick-by-tick option is selected. Try not selecting it.

Already done but the result is identical.

Yes, the same start for the 4h TF. It’s similar for many instruments, so I think that’s the limit.

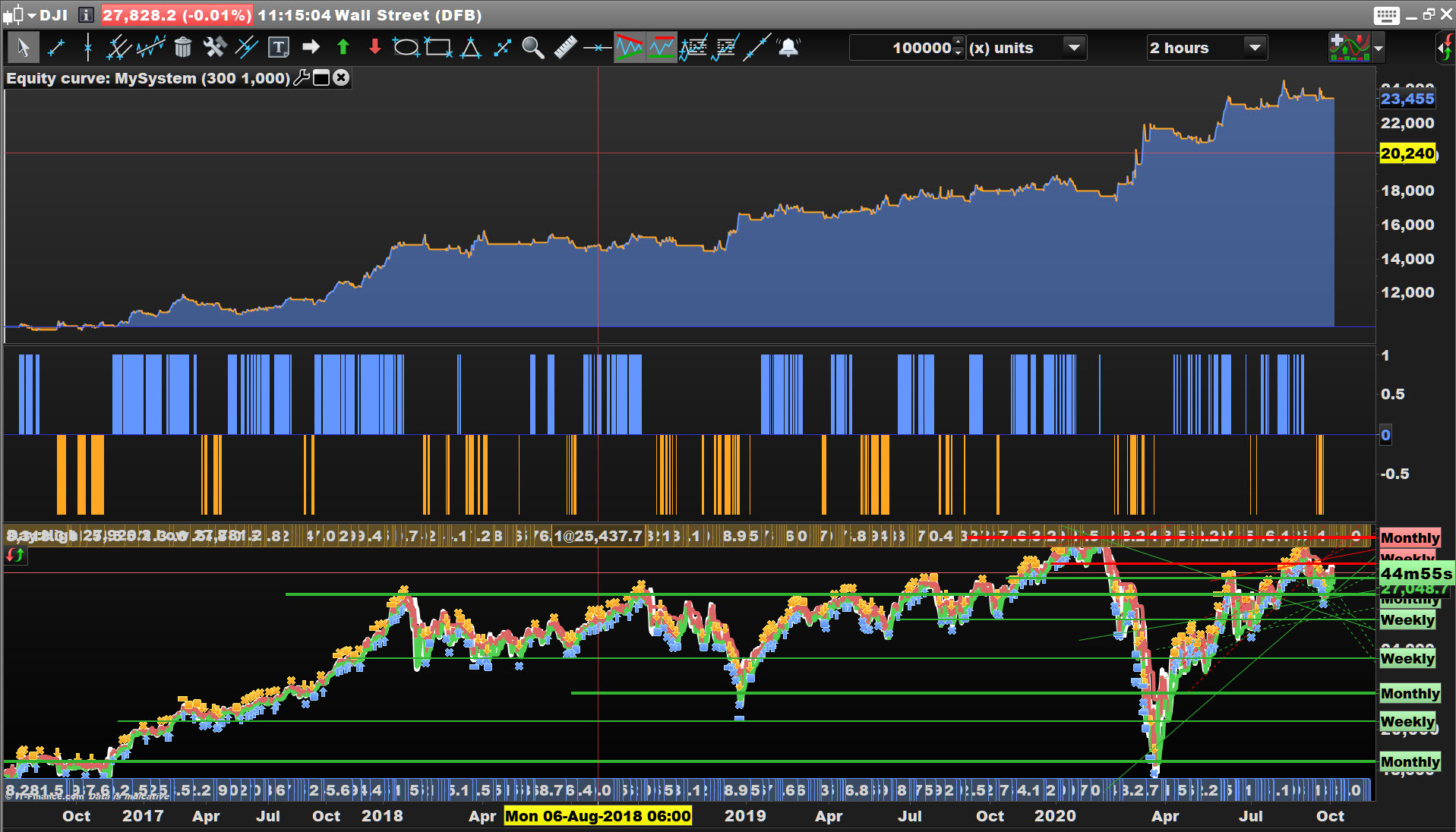

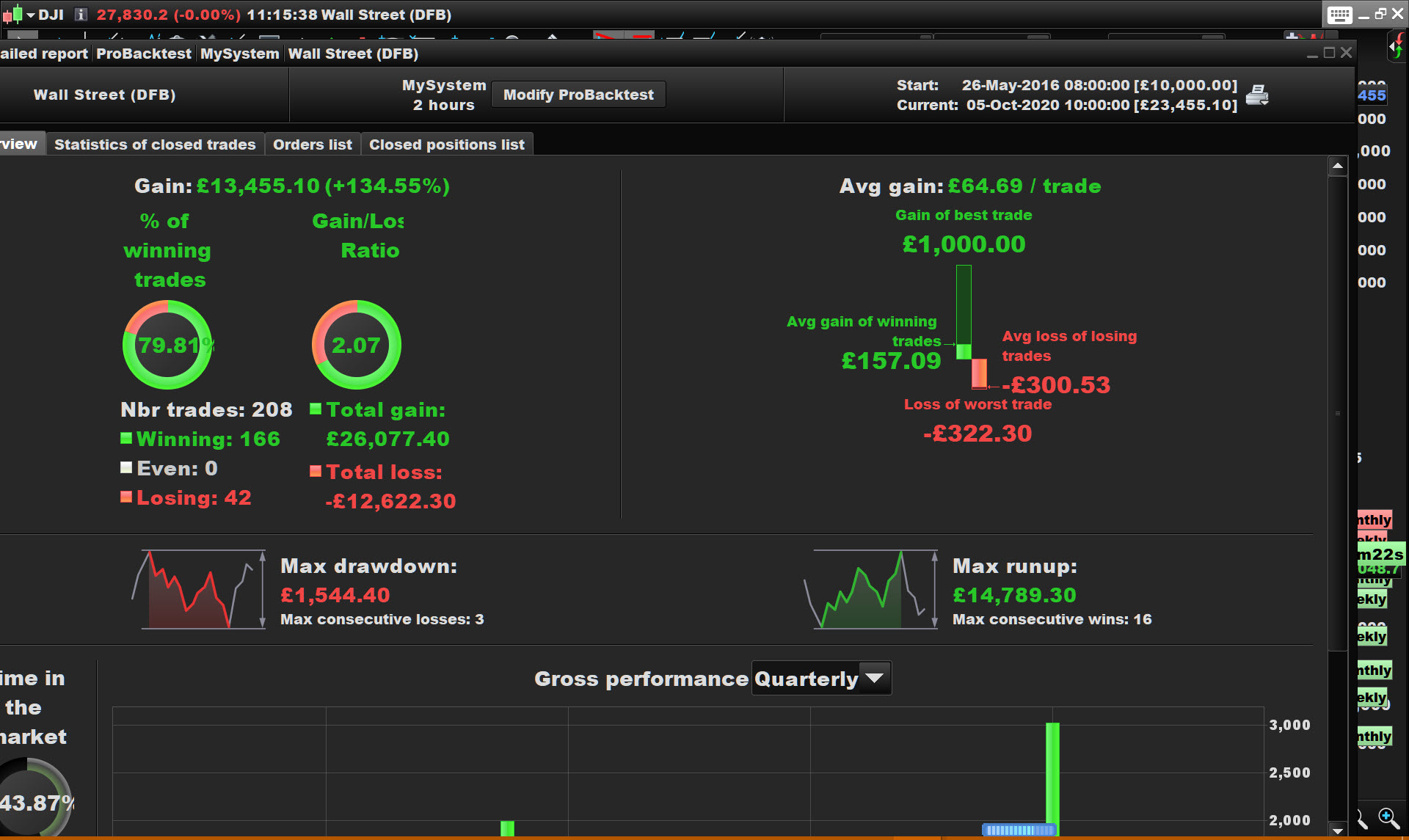

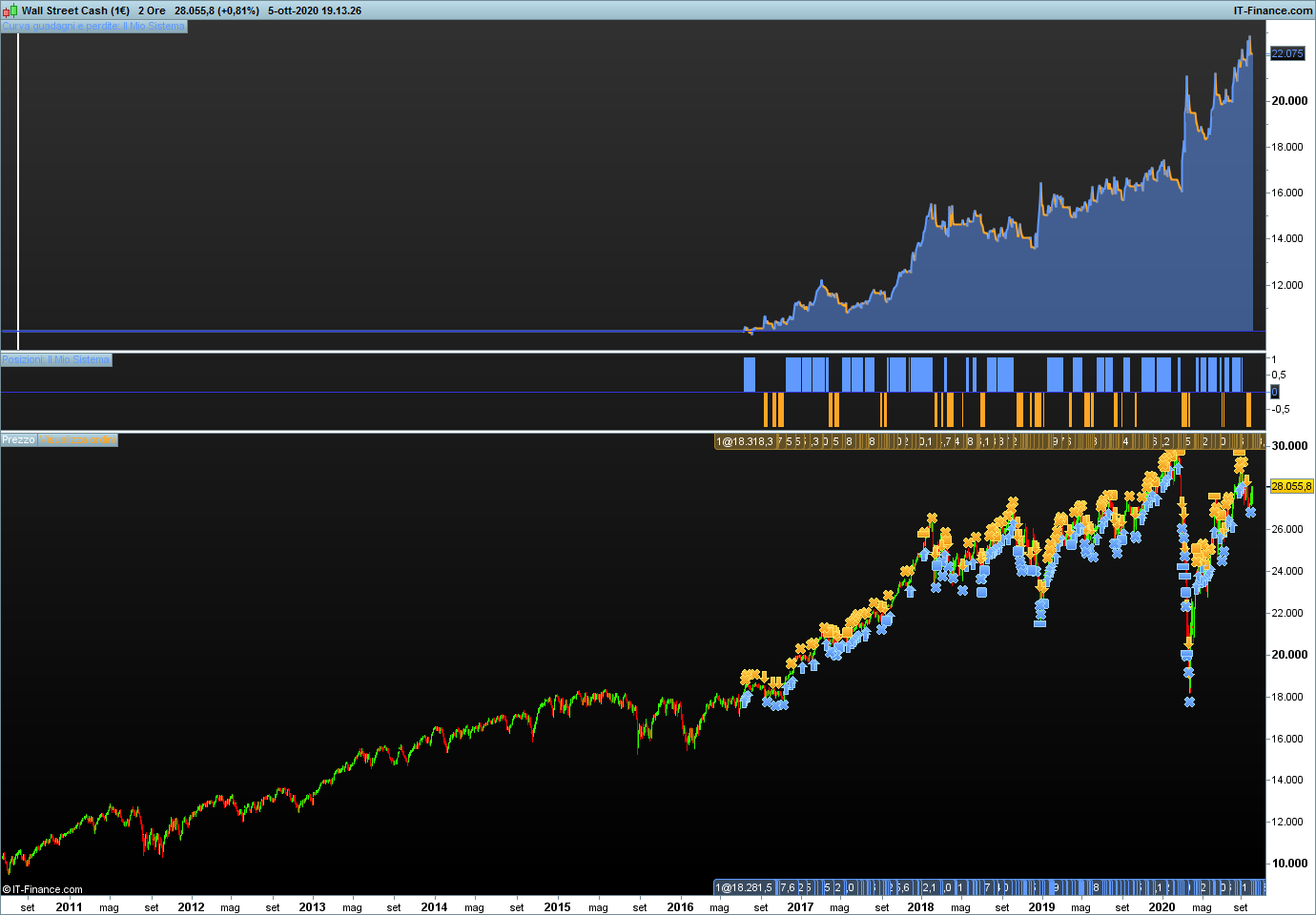

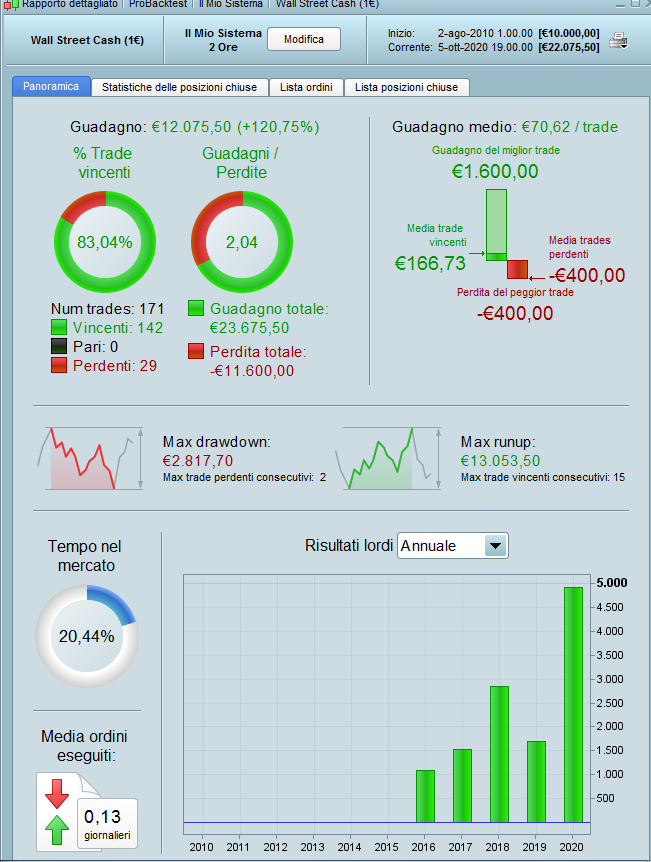

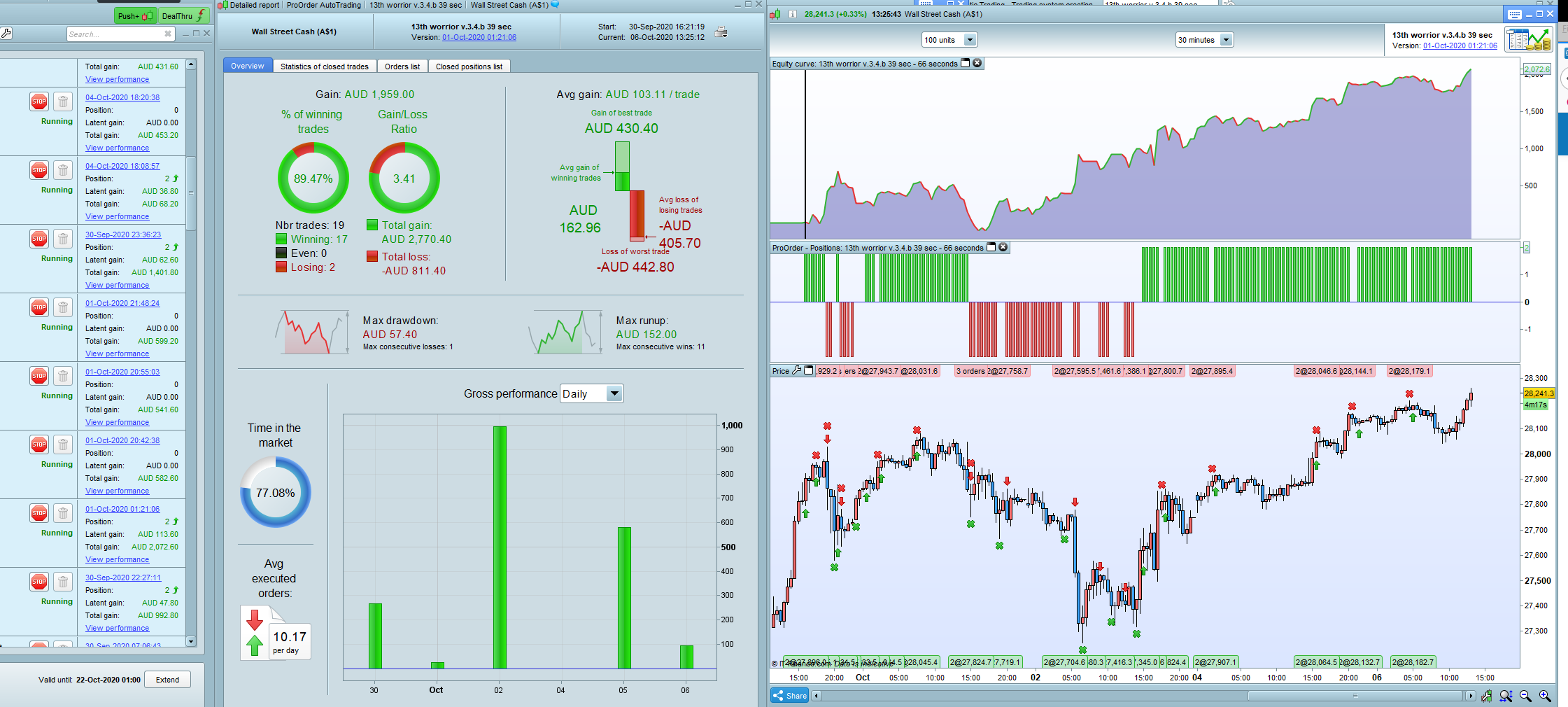

I had really good results with wall street cash $1 at 2h time-frame.

I tried it for day trading in various x-seconds (2, 6 19, 24, 71) , but they need readjustment every 2 or 3 days. the ones i started 4 days ago still work, but they fail in the simulation at the current date. because of that I added a maximum for the strategy profit and trading time limitation in some versions, to lower the risk of loosing the gains. some gained 1000$ over night, but the bad trades are mostly really bad. the Friday crash was really bad and took all the gains from the days before. Also good results with HUF Hungary 12 cach (13thworrior v1.3 HUF 30min.itf)

It worked fine @ 39 seconds for days, when i simulate now it doesn`t work at all, except i move one second forward to 40 second time frame. strange psitionsize =2, spread =6, 40 second timeframe, DJ $1

////////v.3.3.c 2 sec DOW/////////////////////////////////////

//the 13th warrior

Defparam cumulateorders = true

positionsize=2

myOBVn = 5

myCandle = 1

//Heikin Ashi

ONCE haOpen = OPEN

ONCE haClose = CLOSE

N = 0

IF BARINDEX = 0 THEN

haOpen = OPEN

haClose = CLOSE

ELSIF N = 0 THEN

haClose =(OPEN+HIGH+LOW+CLOSE)/4

haOpen =(haOpen[1]+haClose[1])/2

ENDIF

once positionsize = 1

once tradetype = 1 // [1]long&short;[2]long;[3]short

//========= STRATEGY ===================================

mm6= average[299]

mm5= average[120]

mm4= average[10]

mm3= average[7]

mm2= average[4]

mm1= average[3]

mm0= average[2]

mm= average[1]

//long/////////////////////////////////////////////////////////////////////////

c10=low<lowest[2](low[1])

c11=close<low[1]

tradelong = (c10 and c11) or (mm>mm0 and mm0>mm1 and mm1>mm2 and mm2>mm3 and mm3>mm4 and mm4>mm5 and mm5>mm6)

//short

c20=high>highest[2](high[1])

c21=close>high[1]

tradeshort = (c20 and c21) or (mm<mm0 and mm0<mm1 and mm1<mm2 and mm2<mm3 and mm3<mm4 and mm4<mm5 and mm5<mm6)

//Candle-Colour from OBV and HA//////////////////////////////////////////

IF myCandle = 1 THEN

myOBV = OBV(CLOSE)

myAV = Average[myOBVn](myOBV)

IF myOBV > myAV AND haClose > haOpen and (tradetype=1 or tradetype=2) and tradelong THEN

if not onmarket then

buy positionsize contract at market

endif

endif

endif

if myOBV < myAV AND haClose < haOpen and (tradetype=1 or tradetype=3) and tradeshort THEN

if not onmarket then

sellshort positionsize contract at market

endif

endif

//%trailing stop function/////////////////////////////////////////////////////////////

trailingPercent = .23 //org .26

stepPercent = .015//org .014

if onmarket then

trailingstart = tradeprice(1)*(trailingpercent/100) //trailing will start @trailinstart points profit

trailingstep = tradeprice(1)*(stepPercent/100) //% step to move the stop

endif

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions/////////////////////////////////////////////////////////////////////

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart THEN

newSL = tradeprice(1)+trailingstep

ENDIF

//next moves

IF newSL>0 AND close-newSL>trailingstep THEN

newSL = newSL+trailingstep

ENDIF

ENDIF

//manage short positions/////////////////////////////////////////////////////////////////

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart THEN

newSL = tradeprice(1)-trailingstep

ENDIF

//next moves

IF newSL>0 AND newSL-close>trailingstep THEN

newSL = newSL-trailingstep

ENDIF

ENDIF

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

////////EXIT STRATEGY DAYTRADING - GRAB CASH AND RUN///////////////////

x=250-rsi// max stop loss value in $$

contractprofit = 3000 //maximum target profit

set stop loss x

set target profit contractprofit/3

if strategyprofit >= contractprofit then //stop bot from trading and take profits

quit

endif

now it doesn`t work at all,

Maybe just no conditions that match your trigger conditions?

Anyway we are all best to steer clear of Non Standard Timeframes (TF) that don’t add up to 1 min (so 40 sec in non standard TF also) and 1 hour etc.

There is a big discussion topic on here about use of the 29 second TF if you need to be convinced?

There is a big discussion topic on here about use of the 29 second TF if you need to be convinced?

Im convinced, I was experimenting with the code and was surprised about the results, but its too hard to replicate the results, so ill stay clear of these TF in real trades, thanks a lot.

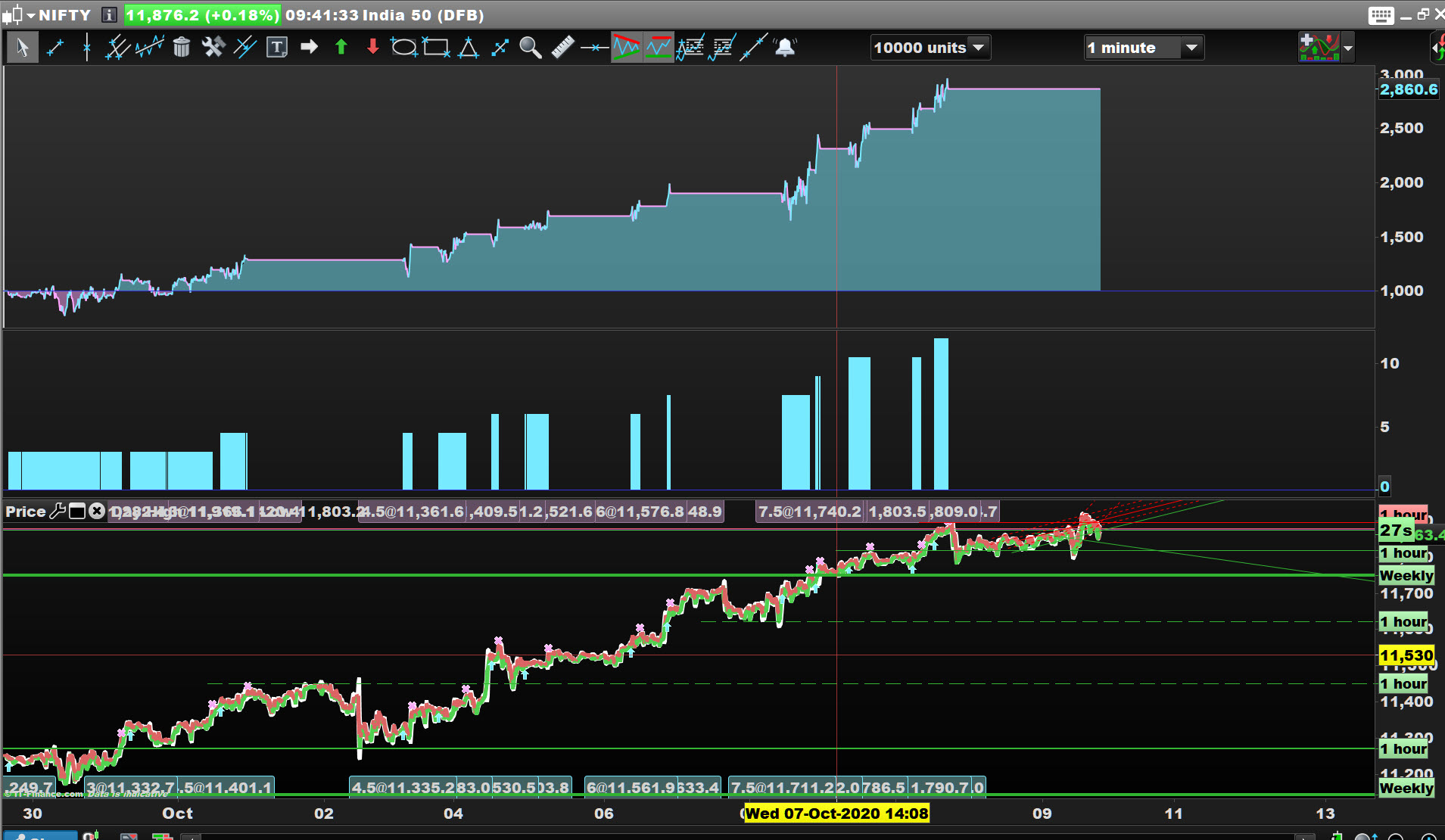

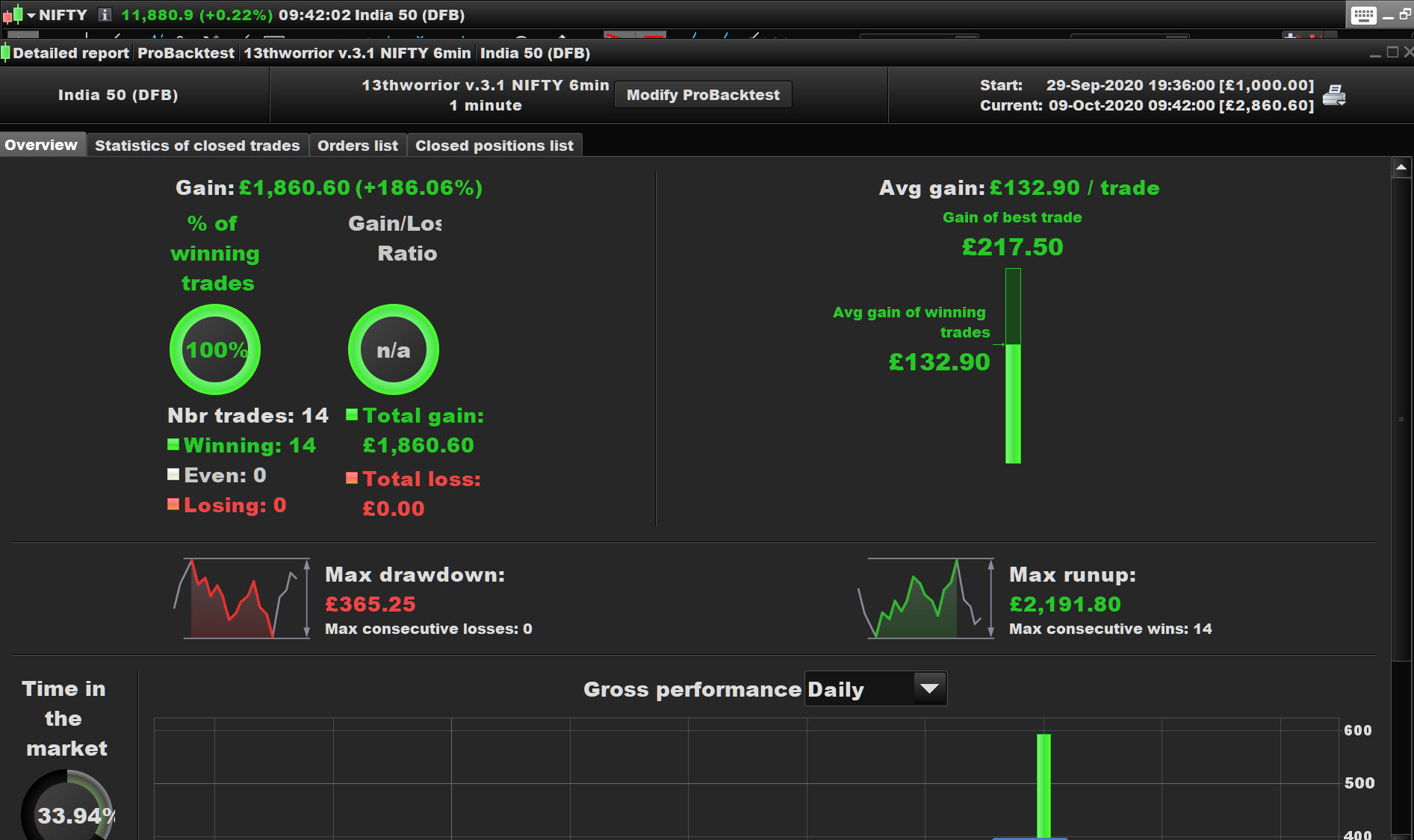

I couldnt get it going on the standard timeframe , just works fine on the 11 minute and 6 minute time frame. but couldnt simulate longer than 2 months

///////v.3.1.d 19 sec DOW//////////////////////////////////

//the 13th warrior NIFTY 6min/////////////////

Defparam cumulateorders = false

//Money Management DOW

MM = 1 // = 0 for optimization

if MM = 0 then

positionsize=2

ENDIF

if MM = 1 then

ONCE startpositionsize = 2

accelerator=1.5 //goes parabolic in an extreme volatile market

ONCE factor = 5 // factor of 10 means margin will increase/decrease @ 10% of strategy profit; factor 20 = 5% etc

ONCE margin = (close*.005) // tier 1 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE margin2 = (close*.01)// tier 2 margin value of 1 contract in instrument currency; change decimal according to available leverage

ONCE tier1 = 55 // DOW €1 IG first tier margin limit

ONCE maxpositionsize = 550 // DOW €1 IG tier 2 margin limit

ONCE minpositionsize = 2 // enter minimum position allowed

IF Not OnMarket THEN

positionsize = round (startpositionsize + Strategyprofit/(factor*margin))*accelerator

ENDIF

IF Not OnMarket THEN

IF startpositionsize + Strategyprofit/(factor*margin) > tier1 then

positionsize = round((((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1)*accelerator //incorporating tier 2 margin

ENDIF

IF Not OnMarket THEN

if startpositionsize + Strategyprofit/(factor*margin) < minpositionsize THEN

positionsize = round (minpositionsize) //keeps positionsize from going below allowed minimum

ENDIF

IF (((startpositionsize + (Strategyprofit/(factor*margin))-tier1)*(factor*margin))/(factor*margin2)) + tier1 > maxpositionsize then

positionsize = round (maxpositionsize)// keeps positionsize from going above IG tier 2 margin limit

ENDIF

ENDIF

ENDIF

ENDIF

myOBVn = 5

myCandle = 1

//Heikin Ashi

ONCE haOpen = OPEN

ONCE haClose = CLOSE

N = 0

IF BARINDEX = 0 THEN

haOpen = OPEN

haClose = CLOSE

ELSIF N = 0 THEN

haClose =(OPEN+HIGH+LOW+CLOSE)/4

haOpen =(haOpen[1]+haClose[1])/2

ENDIF

once positionsize = 1

once tradetype = 2 // [1]long&short;[2]long;[3]short

//========= STRATEGY ===================================

//long

c10=low<lowest[2](low[1])

c11=close<low[1]

tradelong = c10 and c11

//short////

c20=high>highest[2](high[1])

c21=close>high[1]

tradeshort = c20 and c21

//Candle-Colour from OBV and HA

IF myCandle = 1 THEN

myOBV = OBV(CLOSE)

myAV = Average[myOBVn](myOBV)

IF myOBV > myAV AND haClose > haOpen and (tradetype=1 or tradetype=2) and tradelong THEN

if not onmarket then

buy positionsize contract at market

set stop loss 41+rsi

set target profit 70+rsi

endif

endif

if myOBV < myAV AND haClose < haOpen and (tradetype=1 or tradetype=3) and tradeshort THEN

if not onmarket then

sellshort positionsize contract at market

set stop loss 43+rsi

set target profit 70+rsi

endif

endif

ENDIF

//%trailing stop function//////////////////////////////////////////////////////////

trailingPercent = .19 //org .26

stepPercent = .0155//org .014

if onmarket then

trailingstart = tradeprice(1)*(trailingpercent/100) //trailing will start @trailinstart points profit

trailingstep = tradeprice(1)*(stepPercent/100) //% step to move the stop

endif

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions/////////////////////////////////////////////////////////////////////

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart THEN

newSL = tradeprice(1)+trailingstep

ENDIF

//next moves

IF newSL>0 AND close-newSL>trailingstep THEN

newSL = newSL+trailingstep

ENDIF

ENDIF

//manage short positions/////////////////////////////////////////////////////////////////

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart THEN

newSL = tradeprice(1)-trailingstep

ENDIF

//next moves

IF newSL>0 AND newSL-close>trailingstep THEN

newSL = newSL-trailingstep

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

lol forgot the screenshot

Runs good on 1 min on the Nifty on 10k bars (10K bars compare directly with what you show above).

I’m going to put it on Demo Forward Test … keep em coming! 🙂