Always Keep It Simple (In code and strategy). 3 Variables only, 100 000 units.

Strategy without overfitting (or as little as possible) based on Stochastics I develop today, but no matter for the strategy on backtest. Need to test on OOS now

Have a nice evening

[attachment file=”143235″]

Your new strategy looks nice, @zilliq, thanks for the tips too.

Btw, recently I picked up a topic thanks to @vonasi, I think it is helpful on reducing the optimization time as well (which I believe everyone is so eager).

Control of yearly/monthly/weekly profit/loss => https://www.prorealcode.com/topic/annual-percentage-returns/#post-93664

The article is originally for yearly, but you can transform it to monthly/weekly (below I share example for monthly). The better is even set a range of highest profit and lowest loss allowed.

Since we added a quit once the bad month happened, thus the back test is faster, it will not continue to test for the rest of the months.

You can even add a condition check to not have consecutive month/weeks (even days) of loss, e.g. do a summation[3](monthlyreturn) <= 0 for no 3 months consecutive loss.

capital = 5000

once lastcapital = capital

runningperc = ((strategyprofit - laststrategyprofit) / lastcapital) * 100

if month <> month[1] then

monthlyreturn = runningperc[1]

laststrategyprofit = strategyprofit

lastcapital = capital + strategyprofit

total = total + monthlyreturn

count = count + 1

//monthlyaverage = total/count

endif

if monthlyreturn < -0.5 then

QUIT

endif

Since the optimization timing is faster (thanks to skip the bad parameters), you can have a bigger range of optimization.

I guess you are teasing us and you are not going to share your excellent looking Strategy??

@GraHal, you can subscribe when he put in market place, haha 🙂 But I’m sure you also have such strategy, right? Perhaps same for many people here as well…

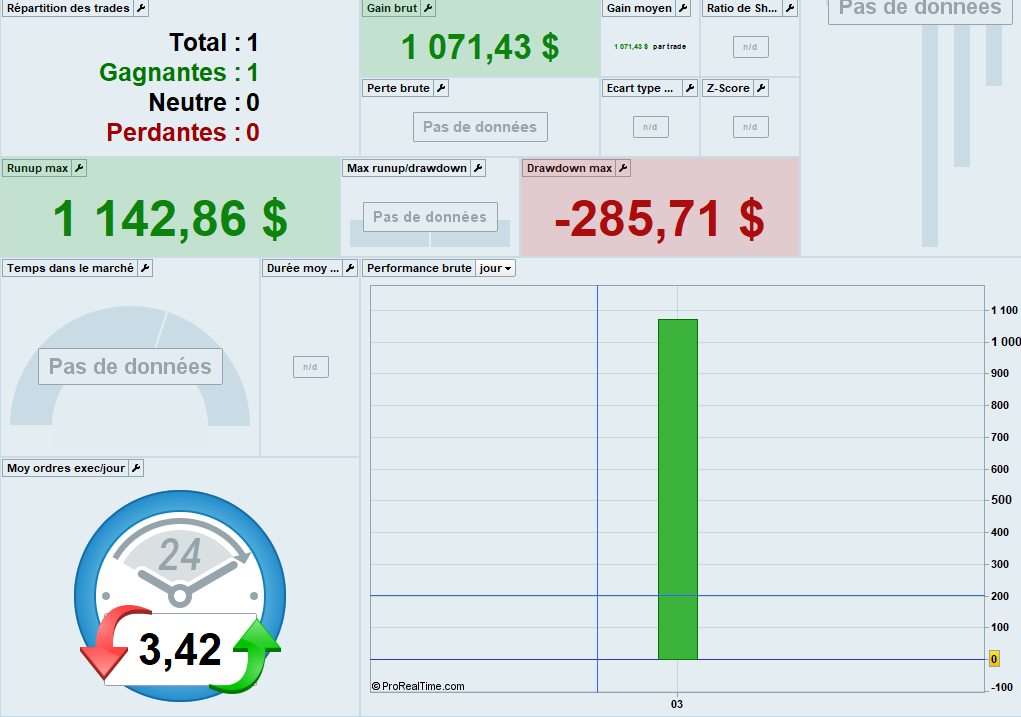

No loosers?

Of course there is losers;- 87 % winners

100 % winners on 100 000 units = Overfitting for me

@dow jones LOL not even.

I consider to sell an algo is a scam because it need always some work and retesting

Paul

PaulParticipant

Master

Zilliq, pure a simple risk/reward strategy with a certain ratio or other exit methods included?

Classical exit based on ATR @Paul

Of course there is losers;- 87 % winners

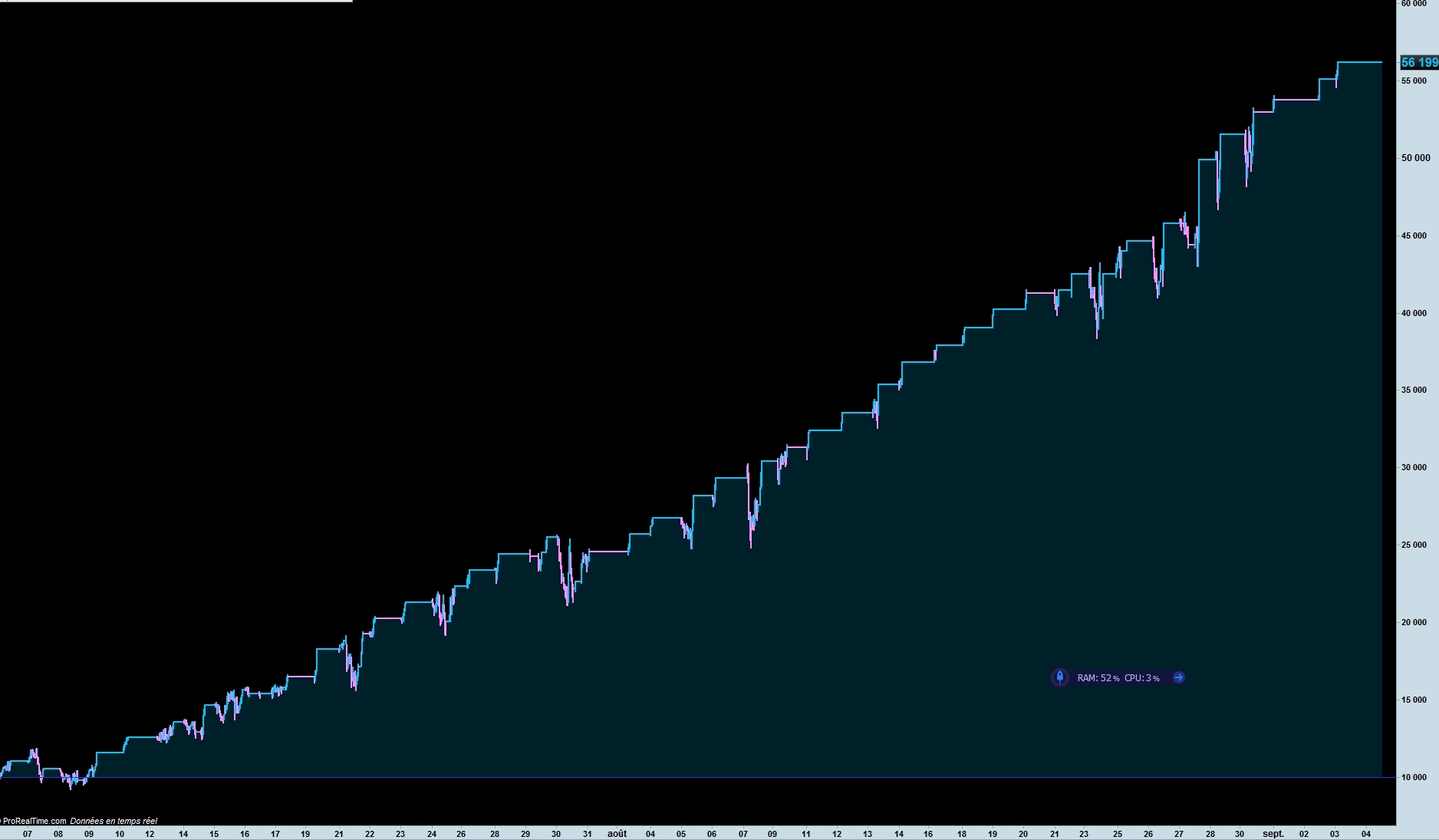

Good! Any chance to share the same screenshot with position size window below the equity curve?

Of course Nicolas, I just need to do another backtest. I will tomorrow

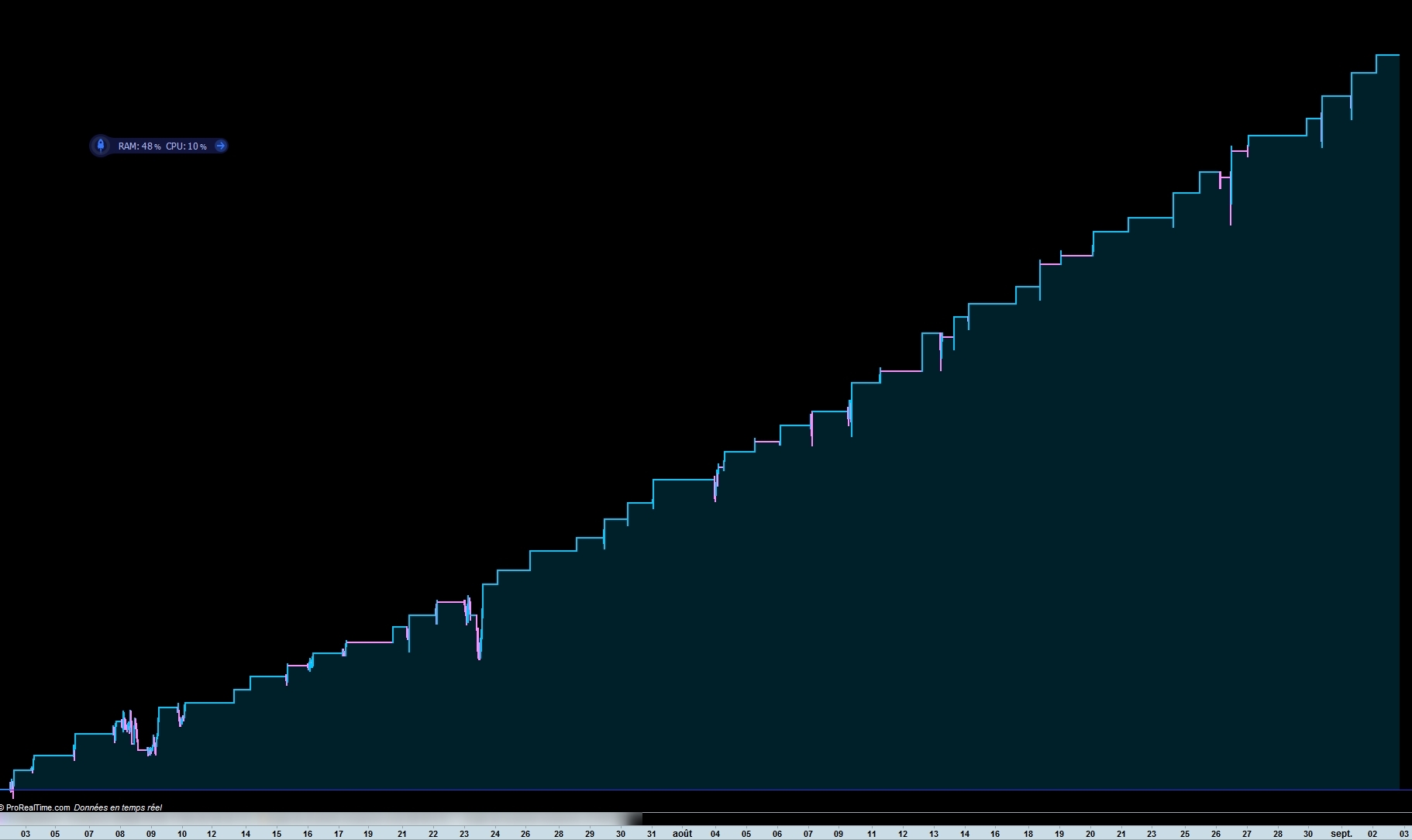

First OOS day for this Algos (Mean nothing as you now, but good start).

Always a 1000 USD/day strategy (I don’t need more 🙂 )

To continue to minimize the overfitting, today I begin an OOS demo test with a strategy on SAR to have only 2 variables

58,99 % winners on the backtest but on 556 trades ! 100 000 units EUR/USD 1 mn Sharpe Ratio 1.1.

We will see if it was a good idea 🙂

Have a nice day

Zilliq

@zilliq you should open a fresh new topic for your OOS forward test about this specific strategy, we are a bit off-topic now here, if you don’t mind.

Control of yearly/monthly/weekly profit/loss

An update to this one, below is an example to control on the consecutive monthly and weekly loss.

You can probably extend it to maximum win for monthly/weekly too (I didn’t do it as it is already difficult to achieve no monthly and weekly loss over long period).

I kind of think that a stable strategy should have stable income, so no huge spike or huge drawdown on certain period that resulted good total gain only.

Adding this means the back test will stop for the combination if you will anyway don’t like it, e.g. if you won’t accept strategy that loss 2 consecutive months, then no point to continue the back test for whole period.

So making the back test a bit faster. Hope you guys like it and suggestion welcome.

//1. Check monthly not lower than expected profit and no consecutive month loss

capital = 5000

monthlymingain = -10

maxconsecutivemonthlyloss = 1

maxconsecutiveweeklyloss = 2

once lastmonthlycapital = capital

once lastweeklycapital = capital

once consecutiveweeklyloss = 0

once consecutivemonthlyloss = 0

runningmonthlyperc = ((strategyprofit - lastmonthstrategyprofit) / lastmonthlycapital) * 100

runningweeklyperc = ((strategyprofit - lastweekstrategyprofit) / lastweeklycapital) * 100

//Ensure none of the month less than expected gain

if month <> month[1] then

monthlyreturn = runningmonthlyperc[1]

lastmonthstrategyprofit = strategyprofit

lastmonthlycapital = capital + strategyprofit

if monthlyreturn < 0 then

consecutivemonthlyloss = consecutivemonthlyloss + 1

else

consecutivemonthlyloss = 0

endif

endif

if monthlyreturn < monthlymingain or consecutivemonthlyloss > maxconsecutivemonthlyloss then

QUIT

endif

//2. Check consecutive week of loss is acceptable

if opendayofweek < opendayofweek[1] then

weeklyreturn = runningweeklyperc[1]

lastweekstrategyprofit = strategyprofit

lastweeklycapital = capital + strategyprofit

if weeklyreturn < 0 then

consecutiveweeklyloss = consecutiveweeklyloss + 1

else

consecutiveweeklyloss = 0

endif

endif

if consecutiveweeklyloss > maxconsecutiveweeklyloss then

QUIT

endif

Very good idea and thank you for that great snippet DowJones. But, while it should improve backtest time, you will also introduce a form of over-fitting by avoiding bad months, yeah i know nothing’s perfect 😉

you will also introduce a form of over-fitting by avoiding bad months, yeah i know nothing’s perfect 😉

Nicolas is right (as always!) Also remember that a strategy cares nothing about things like when the name/number of the current month changes.

You could have a bad second half of a month and a bad first half of the next month and that back test is included in the results because both months are average results whereas if they same results had just happened a couple of weeks earlier and occurred all in the same month then that test would be excluded. Surely it is better just to have a rolling period or rolling quantity of trades and if the results are below what you would be happy to trade then quit the back test to save optimising time?