Hi

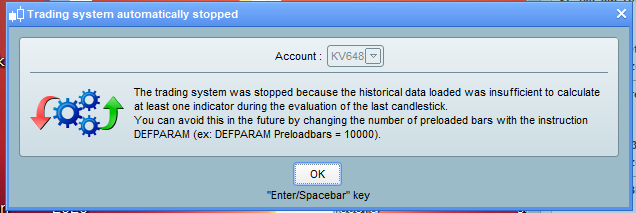

Who can explain the meaning the following code? because I had run some, but sometimes was stopped by systems. It said I need to amend this. Many thanks.

defparam cumulateorders = true / false ???

defparam preloadbars = 10000

Try below …

defparam cumulateorders = True //or False, but not both :)

Thanks GraHal

I tried it “True” and “False”, system still reject it immediately.

It’s also a problem with preloadbars instruction. Try to increase the number.. There is a problem with history data of an indicator inside

I tried it “True” and “False”, system still reject it immediately.

What happens if you delete defparam cumulateorders altogether?

If Algo still gets rejected then something else is causing Rejection?

Try testing on a reduced number of bars until the Algo does not get Rejected.

Let us know how you get on please?

I have deleted the “defparam cumulateorders”, ran 3 hours, then also was stopped. 🙁

This system has also run in other instruments, no this issue.

p.s., I am using Vectorial, and Mother of Dragon also have this problem.

You should post the code and tell us the instrument you are trading, in order to try to replicate the issue.

ran 3 hours

Try it on 3 hour timeframe and on 100 bars and let us know how you get on?

defparam cumulateorders = true

defparam preloadbars = 10000

once tradetype = 1 // [1]long/short [2]long [3]short

once reenter = 1 // [1]on [0]off (off ignores positionperftype/value below)

once positionperftype = 0 // [0]loss/gain [1]loss [2]gain

once positionperfvalue = 0.1 // % (0 or higher)

once stochasticrsi = 1

once sll = 1.6 // stoploss long

once sls = 1.8 // stoploss short

once ptl = undefined // profit target long

once pts = undefined // profit target short

once overnightposition = 1

once weekendposition = 1

// money management

MM = 0 // = 0 for optimization

if MM = 0 then

positionsize=1 //

ENDIF

if MM = 1 then

ENDIF

ENDIF

if overnightposition=1 and weekendposition=1 then

ctime = (time>=14000 and time=<240000 or time>=000000 and time<3500) and not (time>=120000 and time<130000 or time>=50000 and time<60000)

elsif overnightposition=0 then

ctime = (time>=044500 and time<220000) //and not (time>=153000 and time<163300)

elsif overnightposition=1 and weekendposition=0 then

ctime = ((dayofweek<5 and time>=044500 and time<230000) or (dayofweek=5 and time>=044500 and time<220000)) //and not (time>=153000 and time<163300)

endif

once periodea = 33 //14

once nbchandeliera = 14 //20

once periodeb = 32 //29

once nbchandelierb = 48 //41

mma = exponentialaverage[periodea](close)

adjasuroppo = (mma-mma[nbchandeliera]*pipsize) / nbchandeliera

angle = (atan(adjasuroppo))

mmb = exponentialaverage[periodeb](close)

pente = (mmb-mmb[nbchandelierb]*pipsize) / nbchandelierb

trigger = exponentialaverage[periodeb](pente)

cb1 = angle >= 34

cs1 = angle <= -28

cb2 = (pente crosses over trigger) and (pente >-6 and pente < 1)

cs2 = (pente crosses under trigger) and (pente >-11 and pente < 9)

//entrees en position

condbuy = cb1 and cb2 //and low<>dlow(0) //and close<>low

condsell = cs1 and cs2 //and high<>dhigh(0) //and close<>high

//stochastic rsi | indicator

if stochasticrsi then

lengthrsi = 11 // 2 rsi period

lengthstoch = 2 // 6 stochastic period

smoothk = 4 // 4 smooth signal of stochastic rsi

smoothd = 10 // 8 smooth signal of smoothed stochastic rsi

myrsi = rsi[lengthrsi](totalprice)

minrsi = lowest[lengthstoch](myrsi)

maxrsi = highest[lengthstoch](myrsi)

stochrsi = (myrsi-minrsi) / (maxrsi-minrsi)

k = average[smoothk](stochrsi)*100

d = average[smoothd](k)

c13 = k>d

c14 = k<d

condbuy = condbuy and c13

condsell= condsell and c14

else

c13=c13

c14=c14

endif

// entry criteria

if ctime then

if (tradetype=1 or tradetype=2) then

if condbuy and not longonmarket then

buy positionsize contract at market

if tradetype=1 then

set stop %loss sll

set target %profit ptl

elsif tradetype=2 then

set stop %loss sll

set target %profit ptl

endif

endif

endif

if (tradetype=1 or tradetype=3) then

if condsell and not shortonmarket then

sellshort positionsize contract at market

if tradetype=1 then

set stop %loss sls

set target %profit pts

elsif tradetype=3 then

set stop %loss sls

set target %profit pts

endif

endif

endif

if reenter then

if positionperftype=1 then

positionperformance=positionperf(0)*100<-positionperfvalue

elsif positionperftype=2 then

positionperformance=positionperf(0)*100>positionperfvalue

else

positionperformance=((positionperf(0)*100)<-positionperfvalue or (positionperf(0)*100)>positionperfvalue)

endif

if (tradetype=1 or tradetype=2) then

if condbuy and longonmarket and positionperformance then

sell at market

endif

if condbuy[1] and not longonmarket then

buy positionsize contract at market

if tradetype=1 then

set stop %loss sll

set target %profit ptl

elsif tradetype=2 then

set stop %loss sll

set target %profit ptl

endif

endif

endif

if (tradetype=1 or tradetype=3) then

if condsell and shortonmarket and positionperformance then

exitshort at market

endif

if condsell[1] and not shortonmarket then

sellshort positionsize contract at market

if tradetype=1 then

set stop %loss sls

set target %profit pts

elsif tradetype=3 then

set stop %loss sls

set target %profit pts

endif

endif

endif

endif

else

if longonmarket and condsell then

//sell at market

endif

if shortonmarket and condbuy then

//exitshort at market

endif

endif

// break even stop

once enablebe = 1

if enablebe then

once besg = 0.89//0.25 //% break even stop gain

once besl = -0.001//0.75 //% break even stop level (+ or -)

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

benewsl=0

endif

if longonmarket then

if high-tradeprice(1)>=((tradeprice(1)/100)*besg)*pointsize then

benewsl=tradeprice(1)+((tradeprice(1)/100)*besl)*pointsize

endif

endif

if shortonmarket then

if tradeprice(1)-low>=((tradeprice(1)/100)*besg)*pointsize then

benewsl=tradeprice(1)-((tradeprice(1)/100)*besl)*pointsize

endif

endif

if barindex-tradeindex>1 then

if longonmarket then

if benewsl>0 then

sell at benewsl stop

endif

if benewsl>0 then

if low crosses under benewsl then

sell at market

endif

endif

endif

if shortonmarket then

if benewsl>0 then

exitshort at benewsl stop

endif

if benewsl>0 then

if high crosses over benewsl then

exitshort at market

endif

endif

endif

endif

endif

// trailing atr stop

once trailingstoptype1 = 1 // trailing stop - 0 off, 1 on

if trailingstoptype1 then

once tsincrements = 0.11 // set to 0 to ignore tsincrements

once tsminatrdist = 1

once tsatrperiod = 9 // ts atr parameter

once tsminstop = 20 // ts minimum stop distance

once tssensitivity = 1 // [0]close;[1]high/low

if barindex=tradeindex then

trailingstoplong = 10 // ts atr distance

trailingstopshort = 8 // ts atr distance

else

if longonmarket then

if tsnewsl>0 then

if trailingstoplong>tsminatrdist then

if tsnewsl>tsnewsl[1] then

trailingstoplong=trailingstoplong

else

trailingstoplong=trailingstoplong-tsincrements

endif

else

trailingstoplong=tsminatrdist

endif

endif

endif

if shortonmarket then

if tsnewsl>0 then

if trailingstopshort>tsminatrdist then

if tsnewsl<tsnewsl[1] then

trailingstopshort=trailingstopshort

else

trailingstopshort=trailingstopshort-tsincrements

endif

else

trailingstopshort=tsminatrdist

endif

endif

endif

endif

tsatr=averagetruerange[tsatrperiod]((close/10)*pipsize)/1000

//tsatr=averagetruerange[tsatrperiod]((close/1)*pipsize) // (forex)

tgl=round(tsatr*trailingstoplong)

tgs=round(tsatr*trailingstopshort)

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

tsmaxprice=0

tsminprice=close

tsnewsl=0

endif

if tssensitivity then

tssensitivitylong=high

tssensitivityshort=low

else

tssensitivitylong=close

tssensitivityshort=close

endif

if longonmarket then

tsmaxprice=max(tsmaxprice,tssensitivitylong)

if tsmaxprice-tradeprice(1)>=tgl*pointsize then

if tsmaxprice-tradeprice(1)>=tsminstop then

tsnewsl=tsmaxprice-tgl*pointsize

else

tsnewsl=tsmaxprice-tsminstop*pointsize

endif

endif

endif

if shortonmarket then

tsminprice=min(tsminprice,tssensitivityshort)

if tradeprice(1)-tsminprice>=tgs*pointsize then

if tradeprice(1)-tsminprice>=tsminstop then

tsnewsl=tsminprice+tgs*pointsize

else

tsnewsl=tsminprice+tsminstop*pointsize

endif

endif

endif

if barindex-tradeindex>1 then

if longonmarket then

if tsnewsl>0 then

sell at tsnewsl stop

endif

if tsnewsl>0 then

if low crosses under tsnewsl then

sell at market

endif

endif

endif

if shortonmarket then

if tsnewsl>0 then

exitshort at tsnewsl stop

endif

if tsnewsl>0 then

if high crosses over tsnewsl then

exitshort at market

endif

endif

endif

endif

endif

// trailing stop percentage

once trailingstoptype2=1

if trailingstoptype2 then

once trailingpercent = 1

once steppercent = (trailingpercent/10)*1

if onmarket then

trailingstart = tradeprice(1)*(trailingpercent/100)

trailingstep = tradeprice(1)*(steppercent/100)

endif

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

newsl=0

endif

if longonmarket then

if newsl=0 and high-tradeprice(1)>=trailingstart then

newsl = tradeprice(1)+trailingstep

endif

if newsl>0 and high-newsl>trailingstep then

newsl = newsl+trailingstep

endif

endif

if shortonmarket then

if newsl=0 and tradeprice(1)-low>=trailingstart then

newsl = tradeprice(1)-trailingstep

endif

if newsl>0 and newsl-low>trailingstep then

newsl = newsl-trailingstep

endif

endif

if barindex-tradeindex>1 then

if longonmarket then

if newsl>0 then

sell at newsl stop

endif

if newsl>0 then

if low crosses under newsl then

sell at market

endif

endif

endif

if shortonmarket then

if newsl>0 then

exitshort at newsl stop

endif

if newsl>0 then

if high crosses over newsl then

exitshort at market

endif

endif

endif

endif

endif

// market resilience

once mr=1

if mr then

starttime = 0 // 08h00 Pré Market EU (Cac, Dax, Footsie, ect...)

endtime = 140000 // 09h00 Ouverture session européenne

if intradaybarindex = 0 then

hh = 0

ll = 0

endif

if time >= starttime and time < endtime then

if high > hh then

hh = high

endif

if low < ll or ll = 0 then

ll = low

endif

endif

fib38 = hh

fib0 = ll

fibobull200 = (fib38-fib0)*2.19+fib0

fibobull162 = (fib38-fib0)*1.59+fib0

fibobull124 = (fib38-fib0)*0.73+fib0

fibobull100 = (fib38-fib0)*0.07+fib38

fibobull76 = (fib38-fib0)+fib38

fibobull62 = (fib38-fib0)*1.87+fib0

fibobear62 = (fib0-fib38)*0.29+fib0

fibobear76 = (fib0-fib38)+fib0

fibobear100 = (fib0-fib38)*0.45+fib0

fibobear124 = (fib0-fib38)*0.99+fib0

fibobear162 = (fib0-fib38)*0.67+fib0

fibobear200 = (fib0-fib38)*0.08+fib0

fibobull200=fibobull200

fibobull162=fibobull162

fibobull124=fibobull124

fibobull100=fibobull100

fibobull76=fibobull76

fibobull62=fibobull62

fibobear62=fibobear62

fibobear76=fibobear76

fibobear100=fibobear100

fibobear124=fibobear124

fibobear162=fibobear162

fibobear200=fibobear200

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

flag1=0

flag2=0

flag3=0

flag4=0

flag5=0

flag6=0

flag7=0

flag8=0

flag9=0

flag10=0

flag11=0

flag12=0

endif

if time>=0 then

if longonmarket then

if close crosses over fibobull62 then

flag1=1

endif

if flag1=1 then

if close crosses under (ll+fibobull62)/2 then

sell at market

endif

endif

if close crosses over fibobull76 then

flag2=1

endif

if flag2=1 then

if close crosses under (hh+fibobull76)/2 then

sell at market

endif

endif

if close crosses over fibobull100 then

flag3=1

endif

if flag3=1 then

if close crosses under (fibobull62+fibobull100)/2 then

sell at market

endif

endif

if close crosses over fibobull124 then

flag4=1

endif

if flag4=1 then

if close crosses under (fibobull76+fibobull124)/2 then

sell at market

endif

endif

if close crosses over fibobull162 then

flag5=1

endif

if flag5=1 then

if close crosses under (fibobull100+fibobull162)/2 then

sell at market

endif

endif

if close crosses over fibobull200 then

flag6=1

endif

if flag6=1 then

if close crosses under (fibobull124+fibobull200)/2 then

sell at market

endif

endif

endif

if shortonmarket then

if close crosses under fibobear62 then

flag7=1

endif

if flag7=1 then

if close crosses over (hh+fibobear62)/2 then

exitshort at market

endif

endif

if close crosses under fibobear76 then

flag8=1

endif

if flag8=1 then

if close crosses over (ll+fibobear76)/2 then

exitshort at market

endif

endif

if close crosses under fibobear100 then

flag9=1

endif

if flag9=1 then

if close crosses over (fibobear62+fibobear100)/2 then

exitshort at market

endif

endif

if close crosses under fibobear124 then

flag10=1

endif

if flag10=1 then

if close crosses over (fibobear76+fibobear124)/2 then

exitshort at market

endif

endif

if close crosses under fibobear162 then

flag11=1

endif

if flag11=1 then

if close crosses over (fibobear100+fibobear162)/2 then

exitshort at market

endif

endif

if close crosses under fibobear200 then

flag12=1

endif

if flag12=1 then

if close crosses over (fibobear124+fibobear200)/2 then

exitshort at market

endif

endif

endif

endif

endif

// display days in market

once displaydim =0 // displays the number of days in market (activated graph)

once maxdim =99 // maximum days in market

if displaydim then

if not onmarket then

dim=0

else

if onmarket and not onmarket[1] or (longonmarket and shortonmarket[1]) or (shortonmarket and longonmarket[1]) then

dim=1

endif

endif

if not opendayofweek=0 then

if onmarket then

if openday <> openday[1] then

dim = dim + 1

endif

endif

endif

if onmarket and dim>=maxdim then

sell at market

exitshort at market

endif

//graph dim // display days in market

endif

if not overnightposition then

if time>=215400 then

sell at market

exitshort at market

endif

endif

if not weekendposition then

if (dayofweek=5 and time>=215400) then

exitshort at market

sell at market

endif

Hi Robertogozzi

This is the code and running in Hong Kong instrument with HK time.

It is based on Vectorial strategy and only adjusted the figures for HK. I have also ran in DJI, DAX, no such issue.

Sometimes, I used the strategy “Mother of Dragon” in Japan and Singapore instruments, also have this issue.

Thanks.

running in Hong Kong instrument

Which Hong Kong instrument?

Do you mean the Hang Seng Index?

Runs okay for me (no error message etc) on 10k bars on 3 H TF on the Hang Seng … see attached.

When you confirm what Instrument and TF and No of bars and Timezone you are having Issues with then I will run same on my Platform for you.

yes, UTC +8 and 3 min. & 100,000 bar