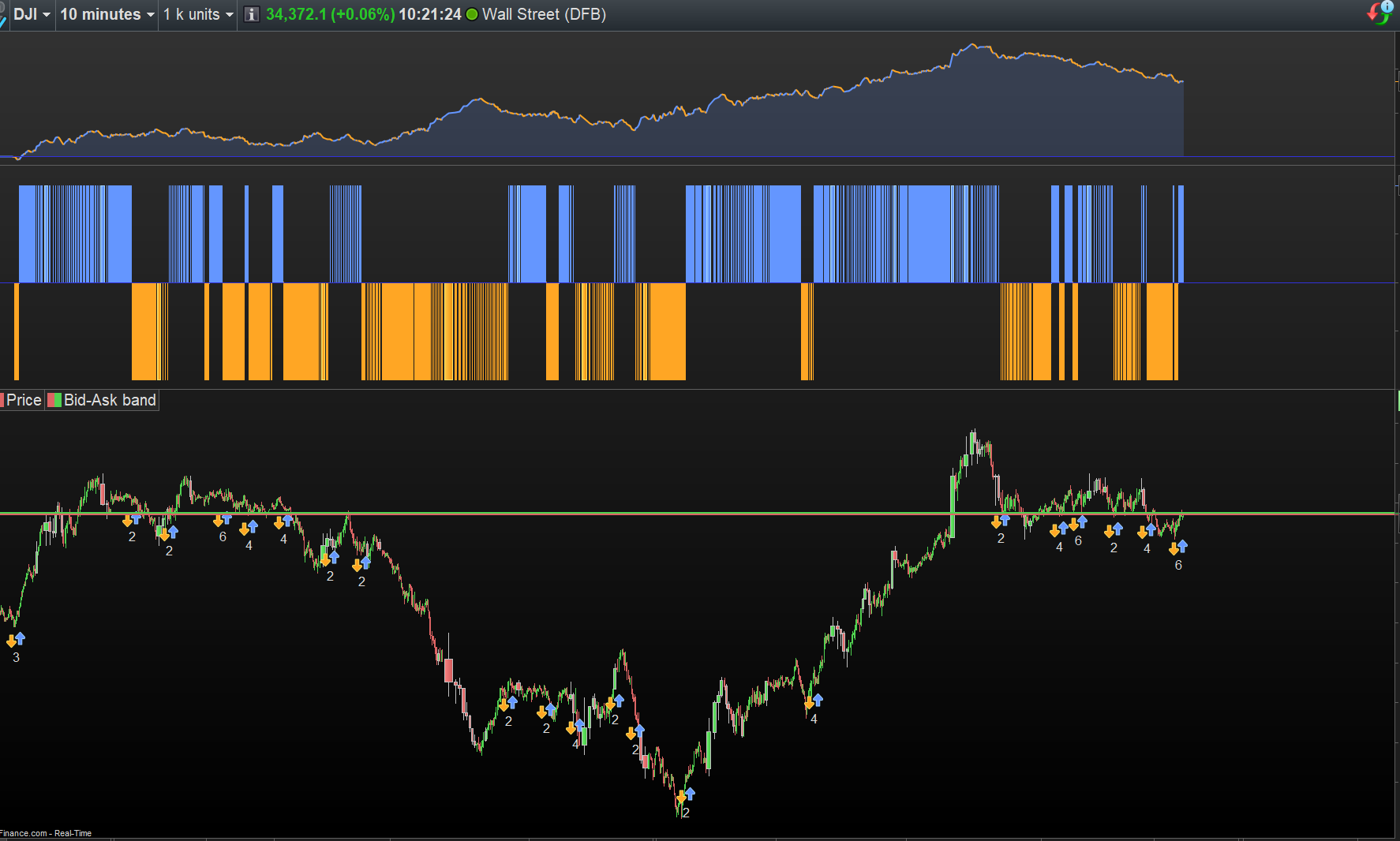

Hi

Please see below to code.

//@version=5

indicator(‘SuperTrended Moving Averages’, ‘ST MA’, overlay=true, format=format.price, precision=2, timeframe=”, timeframe_gaps=false)

src = input(close, title=’Source’)

mav = input.string(title=’Moving Average Type’, defval=’EMA’, options=[‘SMA’, ‘EMA’, ‘WMA’, ‘DEMA’, ‘TMA’, ‘VAR’, ‘WWMA’, ‘ZLEMA’, ‘TSF’, ‘HULL’, ‘TILL’])

length = input.int(100, ‘Moving Average Length’, minval=1)

Periods = input(title=’ATR Period’, defval=10)

Multiplier = input.float(title=’ATR Multiplier’, step=0.1, defval=0.5)

changeATR = input(title=’Change ATR Calculation Method ?’, defval=true)

showsignals = input(title=’Show Buy/Sell Signals ?’, defval=false)

highlighting = input(title=’Highlighter On/Off ?’, defval=true)

T3a1 = input.float(0.7, ‘TILLSON T3 Volume Factor’, step=0.1)

Var_Func(src, length) =>

valpha = 2 / (length + 1)

vud1 = src > src[1] ? src – src[1] : 0

vdd1 = src < src[1] ? src[1] – src : 0

vUD = math.sum(vud1, 9)

vDD = math.sum(vdd1, 9)

vCMO = nz((vUD – vDD) / (vUD + vDD))

VAR = 0.0

VAR := nz(valpha * math.abs(vCMO) * src) + (1 – valpha * math.abs(vCMO)) * nz(VAR[1])

VAR

VAR = Var_Func(src, length)

DEMA = 2 * ta.ema(src, length) – ta.ema(ta.ema(src, length), length)

Wwma_Func(src, length) =>

wwalpha = 1 / length

WWMA = 0.0

WWMA := wwalpha * src + (1 – wwalpha) * nz(WWMA[1])

WWMA

WWMA = Wwma_Func(src, length)

Zlema_Func(src, length) =>

zxLag = length / 2 == math.round(length / 2) ? length / 2 : (length – 1) / 2

zxEMAData = src + src – src[zxLag]

ZLEMA = ta.ema(zxEMAData, length)

ZLEMA

ZLEMA = Zlema_Func(src, length)

Tsf_Func(src, length) =>

lrc = ta.linreg(src, length, 0)

lrc1 = ta.linreg(src, length, 1)

lrs = lrc – lrc1

TSF = ta.linreg(src, length, 0) + lrs

TSF

TSF = Tsf_Func(src, length)

HMA = ta.wma(2 * ta.wma(src, length / 2) – ta.wma(src, length), math.round(math.sqrt(length)))

T3e1 = ta.ema(src, length)

T3e2 = ta.ema(T3e1, length)

T3e3 = ta.ema(T3e2, length)

T3e4 = ta.ema(T3e3, length)

T3e5 = ta.ema(T3e4, length)

T3e6 = ta.ema(T3e5, length)

T3c1 = -T3a1 * T3a1 * T3a1

T3c2 = 3 * T3a1 * T3a1 + 3 * T3a1 * T3a1 * T3a1

T3c3 = -6 * T3a1 * T3a1 – 3 * T3a1 – 3 * T3a1 * T3a1 * T3a1

T3c4 = 1 + 3 * T3a1 + T3a1 * T3a1 * T3a1 + 3 * T3a1 * T3a1

T3 = T3c1 * T3e6 + T3c2 * T3e5 + T3c3 * T3e4 + T3c4 * T3e3

getMA(src, length) =>

ma = 0.0

if mav == ‘SMA’

ma := ta.sma(src, length)

ma

if mav == ‘EMA’

ma := ta.ema(src, length)

ma

if mav == ‘WMA’

ma := ta.wma(src, length)

ma

if mav == ‘DEMA’

ma := DEMA

ma

if mav == ‘TMA’

ma := ta.sma(ta.sma(src, math.ceil(length / 2)), math.floor(length / 2) + 1)

ma

if mav == ‘VAR’

ma := VAR

ma

if mav == ‘WWMA’

ma := WWMA

ma

if mav == ‘ZLEMA’

ma := ZLEMA

ma

if mav == ‘TSF’

ma := TSF

ma

if mav == ‘HULL’

ma := HMA

ma

if mav == ‘TILL’

ma := T3

ma

ma

MA = getMA(src, length)

atr2 = ta.sma(ta.tr, Periods)

atr = changeATR ? ta.atr(Periods) : atr2

up = MA – Multiplier * atr

up1 = nz(up[1], up)

up := close[1] > up1 ? math.max(up, up1) : up

dn = MA + Multiplier * atr

dn1 = nz(dn[1], dn)

dn := close[1] < dn1 ? math.min(dn, dn1) : dn

trend = 1

trend := nz(trend[1], trend)

trend := trend == -1 and close > dn1 ? 1 : trend == 1 and close < up1 ? -1 : trend

upPlot = plot(trend == 1 ? up : na, title=’Up Trend’, color=color.new(color.green, 100), linewidth=0, style=plot.style_linebr)

buySignal = trend == 1 and trend[1] == -1

plotshape(buySignal ? up : na, title=’UpTrend Begins’, location=location.absolute, style=shape.circle, size=size.tiny, color=color.new(color.green, 100))

plotshape(buySignal and showsignals ? up : na, title=’Buy’, text=’Buy’, location=location.absolute, style=shape.labelup, size=size.tiny, color=color.new(color.green, 0), textcolor=color.new(color.white, 0))

dnPlot = plot(trend == 1 ? na : dn, title=’Down Trend’, style=plot.style_linebr, linewidth=0, color=color.new(color.red, 100))

sellSignal = trend == -1 and trend[1] == 1

plotshape(sellSignal ? dn : na, title=’DownTrend Begins’, location=location.absolute, style=shape.circle, size=size.tiny, color=color.new(color.red, 100))

plotshape(sellSignal and showsignals ? dn : na, title=’Sell’, text=’Sell’, location=location.absolute, style=shape.labeldown, size=size.tiny, color=color.new(color.red, 0), textcolor=color.new(color.white, 0))

mPlot = plot(ohlc4, title=”, style=plot.style_circles, linewidth=0)

colorup = input.color(defval = color.new(color.green, 60), title = “ColorU”, inline = ‘color’)

colordown = input.color(defval = color.new(color.red, 60), title = “ColorD”, inline = ‘color’)

longFillColor = highlighting ? trend == 1 ? colorup : color.white : color.new(color.white, 100)

shortFillColor = highlighting ? trend == -1 ? colordown : color.white : color.new(color.white, 100)

fill(mPlot, upPlot, title=’UpTrend Highligter’, color=longFillColor)

fill(mPlot, dnPlot, title=’DownTrend Highligter’, color=shortFillColor)

alertcondition(buySignal, title=’SuperTrend Buy’, message=’SuperTrend Buy!’)

alertcondition(sellSignal, title=’SuperTrend Sell’, message=’SuperTrend Sell!’)

changeCond = trend != trend[1]

alertcondition(changeCond, title=’SuperTrend Direction Change’, message=’SuperTrend has changed direction!’)

Cheers