On you result screen below which variable did you use?

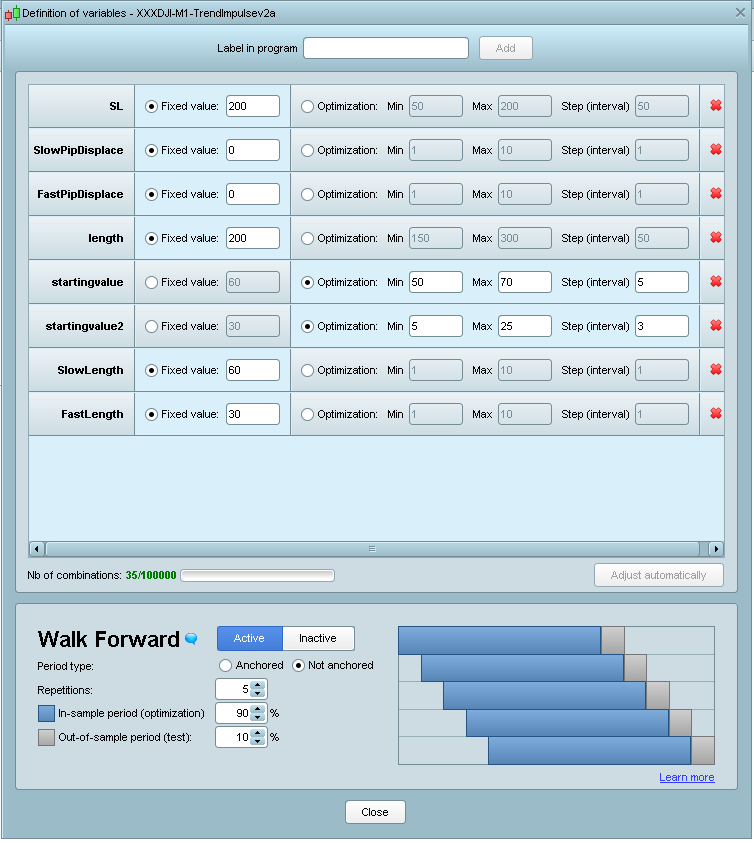

Hi Yomihou, I’m optimizing the variables startingvalue and startingvalue2. See the picture attached. There are other variables I put in optimization, but I have set them to static value. For these static value, I did the first optimization to find the reasonable value and fixed them, e.g. choosing the right range of Stop Loss, I don’t look for the most optimized value for those static variables, just on reasonable range, similar to some fixed value in the strategy (e.g. minvalue, maxvalue that you can see is round and even number, because I didn’t optimized them to optimum, just a rough range). So at the end I only focus on startingvalue and startingvalue2 to optimize on different period of time.

Otherwise, if you import the .itf, you should have the same result as me, I capture right away the result and export right away the .itf, no other modification. Only thing to bare in mind is the time zone that I used is UTC + 8

Since you mentioned were looking at the previous version, if you have any suggestion, feel free to let me know.

congratulations for your contribution,

on which criteria, did you define the value 3.5 for

“IF timeok AND Not OnMarket AND C1 AND volindic < 3.5 THEN ”

best regards

on which criteria, did you define the value 3.5 for “IF timeok AND Not OnMarket AND C1 AND volindic < 3.5 THEN ”

I put up the daily timeframe ATR[5] to analyze the chart manually, to see the area where volatility/risk is too high (i.e. there is plenty of huge gap down/up ~easily 1-2k points in 1 day) and fixed the value accordingly. Purpose is to avoid huge and sudden gain or loss, by skipping to trade in such period (automatically via indicator) as the parameters can be influenced by such spike thus not the goal of this strategy.

thank you for your answer

Hi @yahootew3000,

I was wondering if you could help me with your Strategy? It works great in backtest mode but I get the following message (See Image) when I run it in live test mode. I’m not a coder so just need a bit of an understanding on what values I need to edit. Also I am from the UK so I assume I need to alter the UTC to +8 is that correct? Apologies if this is an idiot question…

Much appreciated,

Plaedies

Hi Plaedis,

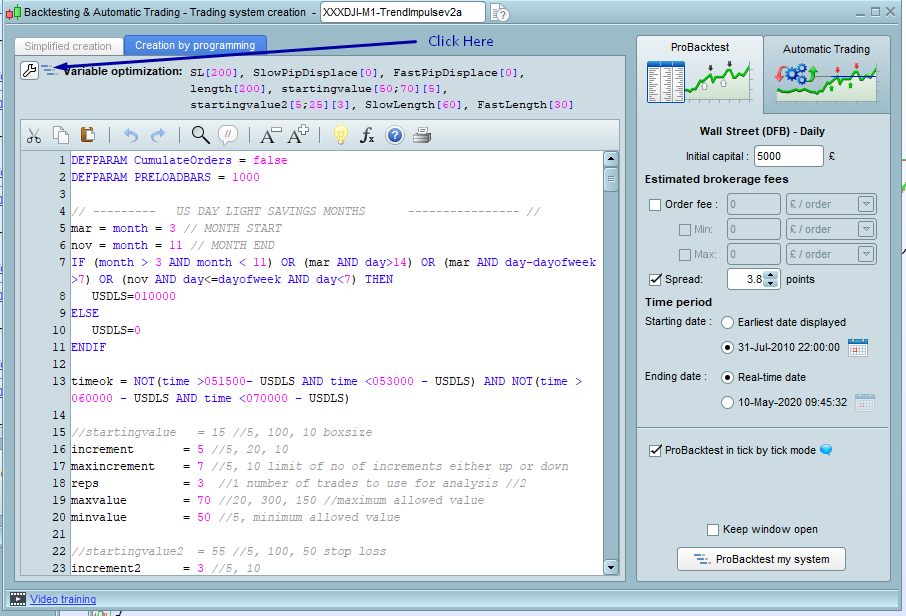

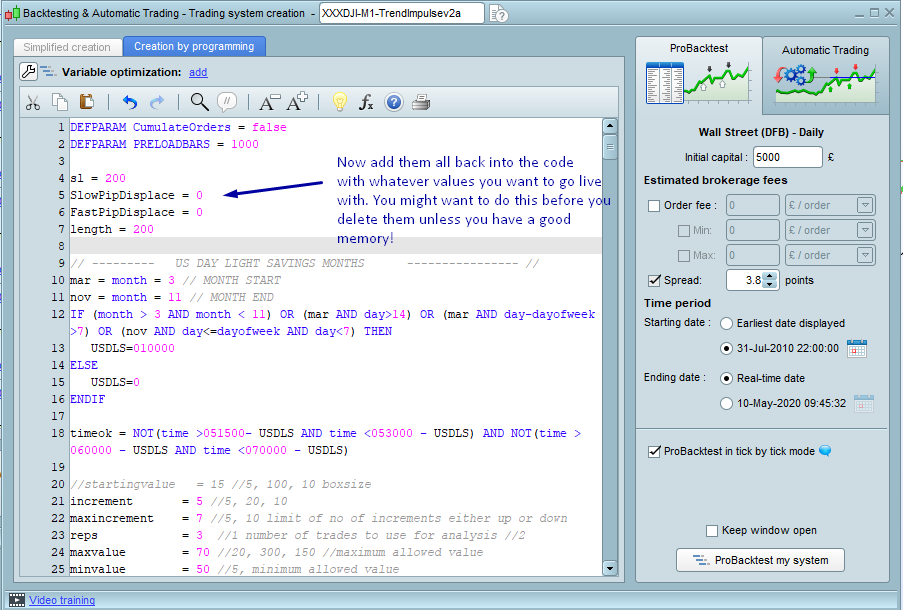

You need define in your code the values that are in the optimization box when you want to run it live. First you can test them in the optimization box to see which are more profitable then define them in the code.

And indeed if you are in the UK you should use the DSL of the UK, Yahootew3000 posted it.

Plaedies – Thank you for wasting my time trying to assist you in your identical question asked in another topic. I have deleted that topic as it is a double post and so breaks forum rules. Please re-read the few simple forum rules before posting again.

The forum rules are as follows:

Post your topic in the correct forum.

ProRealTime Platform Support only platform related issues.

ProOrder only strategy topics.

ProBuilder only indicator topics.

ProScreener only screener topics

General Discussion any other topics.

Welcome New Members for new forum members to introduce themselves.

Only post in the language of the forum that you are posting in. For example English only in the English speaking forums and French only in the French speaking forums.

Always use the ‘Insert PRT Code’ button when putting code in your posts to make it easier for others to read.

Do not double post. Ask your question only once and only in one forum. All double posts will be deleted anyway so posting the same question multiple times will just be wasting your own time and will not get you an answer any quicker. Double posting just creates confusion in the forums.

Be careful when quoting others in your posts. Only use the quote option when you need to highlight a particular bit of text that you are referring to or to highlight that you are replying to a particular member if there are several involved in a conversation. Do not include large amounts of code in your quotes. Just highlight the text you want to quote and then click on ‘Quote’.

Give your topic a meaningful title. Describe your question or your subject in your title. Do not use meaningless titles such as ‘Coding Help Needed’.

Do not include personal information such as email addresses or telephone numbers in your posts. If you would like to contact another forum member directly outside of the forums then contact the forums administrator via ‘Contact Us’ and they will pass your details on to the member that you wish to contact.

Always be polite and courteous to others.

Have fun.

I have edited your post where required. Please ensure that your future posts meet these few simple forum rules. 🙂

@Vonasi,

Please accept my apologies.

Best wishes,

Plaedies

@Yomihou & @vonasi

I’m really sorry I know this is probably a simple thing but within the code I don’t know what to delete/change. I know the startingvalue and startingvalue2 need to simply = the static numeric values that were obtained from the optimisation but even when I do that i get an error messeges stating the code is invalid.

Thank you for your support

Best wishes

Plaedies

Yes – it is a very simple thing but at this time of night I don’t have my PRT platform open and a glass of wine is more interesting than firing it up again so I can’t show you in pictures how to do this very simple thing. Perhaps tomorrow – unless someone else is kind enough to draw screenshot them for you in the mean time. 🙂

@Vonasi

🤣🤣🤣 Yes I completely agree the Vino always comes 1st 🤣🤣

Have a great evening

best wishes

Plaedies

Thank you ever so much @vonasi I learned a valuable lesson here!

just one more thing, there are around 8 variables to add from the variable tables so just simply add all of them right? I say that as you added 4 but I’m guessing that was an example to illustrate the idea?

Best Wishes,

Andrew

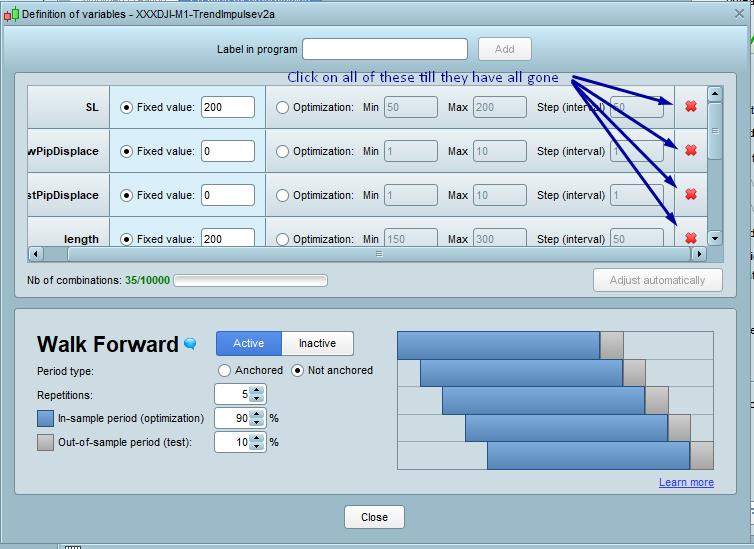

Yes it was just an example and I got bored typing! Add them all or the strategy won’t work.

Hi @vonasi,

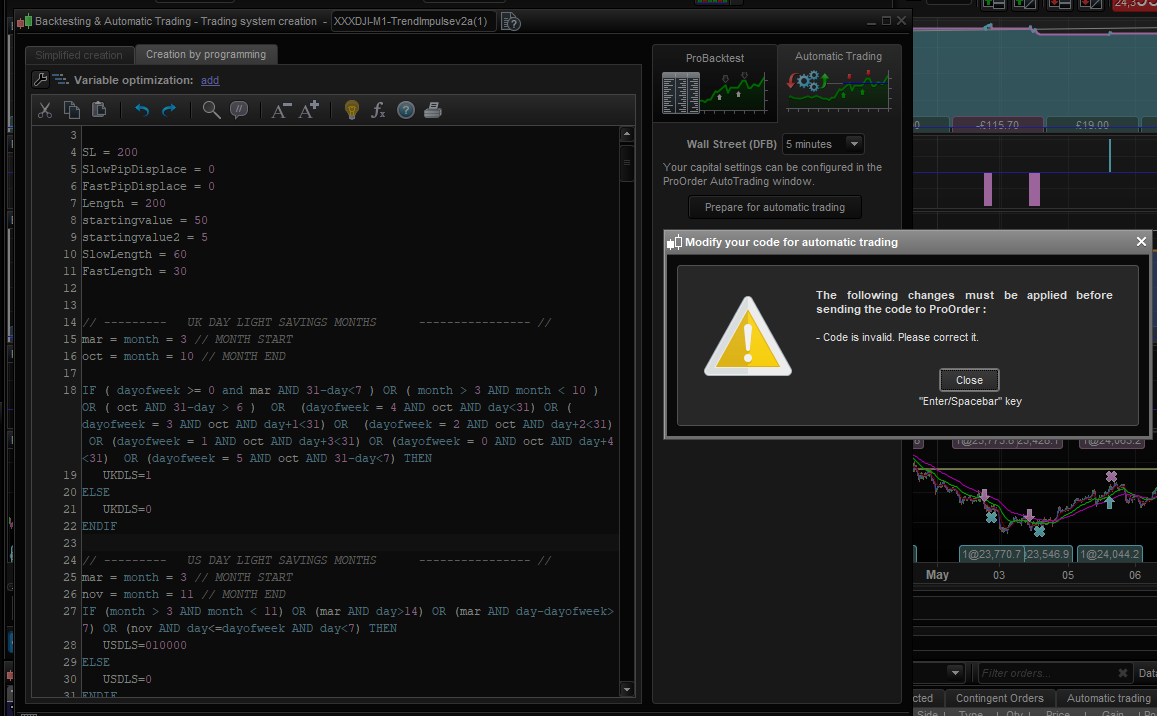

I’ve mirrored what you showed me in the screen grabs and included the UKDLS element (See attached) still getting the code error message? Any ideas? Ive also inserted the code that i have added. Nothing else within the code has been touched.

DEFPARAM CumulateOrders = false

DEFPARAM PRELOADBARS = 1000

SL = 200

SlowPipDisplace = 0

FastPipDisplace = 0

Length = 200

startingvalue = 50

startingvalue2 = 5

SlowLength = 60

FastLength = 30

// --------- UK DAY LIGHT SAVINGS MONTHS ---------------- //

mar = month = 3 // MONTH START

oct = month = 10 // MONTH END

IF ( dayofweek >= 0 and mar AND 31-day<7 ) OR ( month > 3 AND month < 10 ) OR ( oct AND 31-day > 6 ) OR (dayofweek = 4 AND oct AND day<31) OR (dayofweek = 3 AND oct AND day+1<31) OR (dayofweek = 2 AND oct AND day+2<31) OR (dayofweek = 1 AND oct AND day+3<31) OR (dayofweek = 0 AND oct AND day+4<31) OR (dayofweek = 5 AND oct AND 31-day<7) THEN

UKDLS=1

ELSE

UKDLS=0

ENDIF

// --------- US DAY LIGHT SAVINGS MONTHS ---------------- //

mar = month = 3 // MONTH START

nov = month = 11 // MONTH END

IF (month > 3 AND month < 11) OR (mar AND day>14) OR (mar AND day-dayofweek>7) OR (nov AND day<=dayofweek AND day<7) THEN

USDLS=010000

ELSE

USDLS=0

ENDIF

timeok = NOT(time >051500- USDLS AND time <053000 - USDLS) AND NOT(time >060000 - USDLS AND time <070000 - USDLS)

Kind regards,

Plaedies