If some of you can improve this strategy, please share. Logic is pretty robust normally for markets that can trend. Basically you have some bands (like bollinger, but it’s not) on a higher timeframe, and if your outside the bands, it may mean there is a strong trend and you bet it will continue, while you enter into position on a lower TF.

DEFPARAM FlatAfter = 235500

DEFPARAM cumulateorders=false

DEFPARAM PRELOADBARS = 10000

ONCE positionsize=10

Once ministop=2

tradetime=time >080000 and time < 215000 and dayofweek<>0

timeframe (30 minute, updateonclose)

stdev=1

aa = average[100,1]

HBand = aa+average[200](std[100]*stdev)

LBand = aa-average[200](std[100]*stdev)

c1=close crosses over Hband and high>high[1] and summation[100](close>Hband)<65 //and summation[10](close>Hband)[1]<xx//and high<highest[4](high)[1]

cs1=close crosses under Lband and low<low[1] and summation[100](close<LBand)<65 //and summation[10](close<LBand)[1]<xx//and low>lowest[4](low)[1]

High1H=high

Low1H=Low

Timeframe (5 minute)

EMA8=exponentialaverage[8](close)

SMA20=average[20](close)

c2=close>highest[12](high)[1] and close>High1H and BARINDEX-TRADEINDEX(1)>=3

cs2=close<lowest[12](low)[1] and close<Low1H and BARINDEX-TRADEINDEX(1)>=3

if tradetime then

if c1 and c2 and not onmarket then

Buy positionsize contracts at market

stoplevel=lowest[6](low)-close/500//lowest[5](low)-close/1000

endif

if cs1 and cs2 and not onmarket then

Sellshort positionsize contracts at market

stoplevel=highest[6](high)+close/500//lowest[5](low)-close/1000

endif

endif

stoplevelactive=1

if longonmarket and stoplevelactive=1 then

sell at stoplevel stop

endif

if shortonmarket and stoplevelactive=1 then

exitshort at stoplevel stop

endif

targetactive=1

if longonmarket and close<low[1] and close<SMA20 and targetactive=1 and positionperf>0.001 then //and positionperf>0.001

sell at market

endif

if shortonmarket and close>high[1] and close>SMA20 and targetactive=1 and positionperf>0.001 then //and positionperf>0.001

exitshort at market

endif

//si le trade ne part pas

flat=1

if longonmarket and BARINDEX-TRADEINDEX(1)>=18 and positionperf<0.001 and flat and close<positionprice then

sell at positionprice+ministop limit

endif

//si le trade part pas

if shortonmarket and BARINDEX-TRADEINDEX(1)>=18 and positionperf<0.001 and close>positionprice and flat then

exitshort at positionprice-ministop limit

endif

//vendredi le marché cloture plus tot

if dayofweek=5 and longonmarket and time=225500 then

sell at market

endif

if dayofweek=5 and shortonmarket and time=225500 then

exitshort at market

endif

set stop %loss 0.5

set target %profit 1

Watch out, I have backtested your strategy on 1M units (since 2010), see the result attached

Thx. I think I still need to add a filter of some sort. Also either the strat is overfitted, which I don’t believe, either it works best when there is lot of uncertainty in the market like in 2022, so maybe the bands parameters should change in function of a measure of this uncertainty, which is maybe not easy to do.

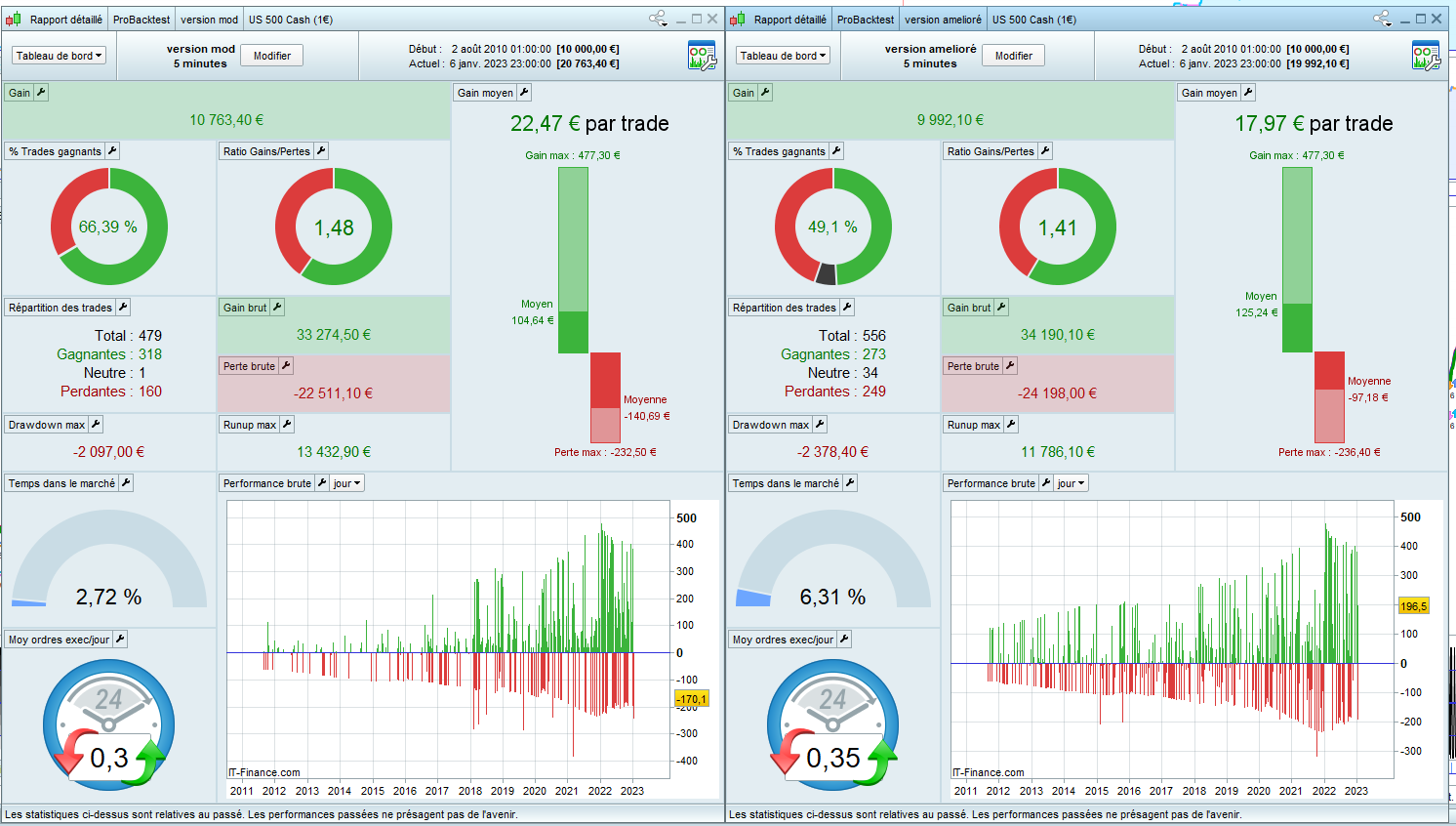

improved version.

DEFPARAM FlatAfter = 235500

DEFPARAM cumulateorders=false

DEFPARAM PRELOADBARS = 10000

ONCE positionsize=10

Once ministop=2

tradetime=time >153000 and time < 215000 and dayofweek<>0

timeframe (30 minutes, updateonclose)

once stdev=1

aa = average[100,1]

HBand = aa+average[200](std[100]*stdev)

LBand = aa-average[200](std[100]*stdev)

c1=close crosses over Hband and high>high[1] and summation[100](close>Hband)<65 //and summation[10](close>Hband)[1]<xx//and high<highest[4](high)[1]

cs1=close crosses under Lband and low<low[1] and summation[100](close<LBand)<65 //and summation[10](close<LBand)[1]<xx//and low>lowest[4](low)[1]

High1H=high

Low1H=Low

Timeframe (5 minute)

if month<>month[1]then

dmonthly=0

else

dmonthly=dmonthly+1

endif

If volume >0 then

VWAPmonthly = SUMMATION[max(1,dmonthly)](volume*typicalprice)/SUMMATION[max(1,dmonthly)](volume)

endif

EMA8=exponentialaverage[8](close)

SMA20=average[20](close)

if day<>day[1] then

barVWAP=0

else

barVWAP=barVWAP+1

endif

if volume>0 then

VWAP = SUMMATION[max(1,barVWAP)](volume*typicalprice)/SUMMATION[max(1,barVWAP)](volume)

endif

c2=close>highest[12](high)[1] and close>High1H and BARINDEX-TRADEINDEX(1)>=3 and close>VWAPmonthly

cs2=close<lowest[12](low)[1] and close<Low1H and BARINDEX-TRADEINDEX(1)>=3 and close<VWAPmonthly

if tradetime then

if c1 and c2 and not onmarket then

Buy positionsize contracts at market

endif

if cs1 and cs2 and not onmarket then

Sellshort positionsize contracts at market

endif

endif

targetactive=1

if longonmarket and close<SMA20 and targetactive=1 and positionperf>0.001 then //and positionperf>0.001

sell at low-ministop*1.5 stop

endif

if shortonmarket and close>SMA20 and targetactive=1 and positionperf>0.001 then //and positionperf>0.001

exitshort at high+ministop*1.5 stop

endif

if dayofweek=5 and longonmarket and time=225500 then

sell at market

endif

if dayofweek=5 and shortonmarket and time=225500 then

exitshort at market

endif

breakevenactive=1

If not OnMarket then

StopLoss = 0

Endif

If StopLoss = 0 and OnMarket and breakevenactive then

If PositionPerf > 0.004 then

If LongOnMarket then

StopLoss = PositionPrice // + ministop

Else

StopLoss = PositionPrice //- ministop

Endif

Endif

Endif

If StopLoss > 0 then

Sell at StopLoss STOP

Exitshort at StopLoss STOP

Endif

set stop %loss 0.5

set target %profit 1

the strategy working only if there is sufficient vol, adding ATR filter on the 30Min makes sense

I have modified the code,

how many spread do you need to do the backtest?

//DEFPARAM FlatAfter = 235500

DEFPARAM cumulateorders=false

DEFPARAM PRELOADBARS = 10000

ONCE positionsize=10

Once ministop=2

tradetime=time >080000 and time < 215000 and dayofweek<>0

timeframe (30 minute, updateonclose)

stdev=1

aa = average[100,1]

HBand = aa+average[200](std[100]*stdev)

LBand = aa-average[200](std[100]*stdev)

c1=close crosses over Hband and high>high[1] and summation[100](close>Hband)<65 //and summation[10](close>Hband)[1]<xx//and high<highest[4](high)[1]

cs1=close crosses under Lband and low<low[1] and summation[100](close<LBand)<65 //and summation[10](close<LBand)[1]<xx//and low>lowest[4](low)[1]

High1H=high

Low1H=Low

Timeframe (5 minute)

EMA8=exponentialaverage[8](close)

SMA20=average[20](close)

wil=Williams[40](close)

c2=close>highest[12](high)[1] and close>High1H and BARINDEX-TRADEINDEX(1)>=3

cs2=close<lowest[12](low)[1] and close<Low1H and BARINDEX-TRADEINDEX(1)>=3

c3=abs(open[1]-close[1])>1 and not(dhigh(0)=high and high-close<1 and low-ema8>5)and high>close and ema8[1]-sma20[1]<ema8-sma20

cs3=sma20[1]-ema8[1]<sma20-ema8

if tradetime then

if c1 and c2 and c3 and not onmarket then

Buy positionsize contracts at market

stoplevel=lowest[6](low)-close/500//lowest[5](low)-close/1000

endif

if cs1 and cs2 and cs3 and not onmarket then

//

Sellshort positionsize contracts at market

stoplevel=highest[6](high)+close/500//lowest[5](low)-close/1000

endif

set stop %loss 0.5

set target %profit 1

endif

stoplevelactive=0

if longonmarket and stoplevelactive=1 then

sell at stoplevel stop

endif

if shortonmarket and stoplevelactive=1 then

exitshort at stoplevel stop

endif

targetactive=1

if longonmarket and close<low[1] and close<SMA20 and targetactive=1 and positionperf>0.001 then //and positionperf>0.001

sell at market

endif

if shortonmarket and close>high[1] and close>SMA20 and targetactive=1 and positionperf>0.001 then //and positionperf>0.001

exitshort at market

endif

//si le trade ne part pas

flat=1

if longonmarket and BARINDEX-TRADEINDEX(1)>=18 and positionperf<0.001 and flat and close<positionprice then

sell at positionprice+ministop limit

endif

//si le trade part pas

if shortonmarket and BARINDEX-TRADEINDEX(1)>=18 and positionperf<0.001 and close>positionprice and flat then

exitshort at positionprice-ministop limit

endif

//vendredi le marché cloture plus tot

if dayofweek=5 and longonmarket and time=225500 then

//sell at market

endif

if dayofweek=5 and shortonmarket and time=225500 then

//exitshort at market

endif

if longonmarket and close>tradeprice and open=close and dhigh(0)=high then

sell at market

endif

Thx for the interest. Spread is around 0.8

Hello #fifi743, I have reviewed the conditions you added but don’t believe they have any added value unfortunately.

Spread =1

I’m in the market for less time

Less loss

More gain