The Endif at the bottom of wich section? sorry Nonetheless but I try to understand the code…!

// mfe & mae

count = 0

For zz = 1 to 5 do

IF range[zz]=0 THEN

count= 1

ENDIF

next

if count=0 then

n = 4

nn= 1

if method=1 then

maerec=0

mferec=0

for i=1 to n

maerec=maerec+(high[i]-open[i])

mferec=mferec+(open[i]-low[i])

next

for j=1 to nn

maerec=maerec+(open[j]-low[j])

mferec=mferec+(high[j]-open[j])

next

averecentmael=close-(maerec/nn)

averecentmfel=close+(mferec/nn)

averecentmaes=close+(maerec/n)

averecentmfes=close-(mferec/n)

avgl=(averecentmael+averecentmfel)/2

avgs=(averecentmaes+averecentmfes)/2

elsif method=2 then

maerec=0

mferec=0

maerec2=0

mferec2=0

for i=1 to n

maerec=maerec+(high[i]-open[i])

mferec=mferec+(open[i]-low[i])

next

for j=1 to nn

maerec2=maerec2+(open[j]-low[j])

mferec2=mferec2+(high[j]-open[j])

next

averecentmael=close-(maerec2/nn)

averecentmfel=close+(mferec2/nn)

averecentmaes=close+(maerec/n)

averecentmfes=close-(mferec/n)

avgl=(averecentmael+averecentmfel)

avgs=(averecentmaes+averecentmfes)

endif

avgmfemaes=average[25](avgs)

avgmfemael=average[25](avgl)

if vectorial then

periodea = 8

nbchandeliera = 3

mma = average[periodea,1](totalprice)

adjasuroppo = (mma-mma[nbchandeliera]*pipsize) / nbchandeliera

angle = (atan(adjasuroppo))

cb1 = angle < 0

cs1 = angle > 0

else

cb1=1

cs1=1

endif

ENDIF

stopped again … zero parameter. I’m losing the will to live.

Paul

PaulParticipant

Master

I get your frustration. Created a stripped down version, one last attempt.

One thing also I spotted, which doesn’t change results, and most likely will not be the cause, but there were 2 rows which were not written correct. The combination and & or at the condsell/condbuy area. It was missing ().

Anyway you could test this and then call it a day.

defparam cumulateorders = false

defparam preloadbars = 2000

once sll = 1.2 // stoploss long

once sls = 0.6 // stoploss short

once ptl = 1.2 // profit target long

once pts = 1.9 // profit target short

TIMEFRAME(15 minutes)

count1 = 0

For zz1 = 1 to 7 do

IF range[zz1]=0 THEN

count1= 1

ENDIF

next

if count1=0 then

indicator1 = SuperTrend[2,6]

indicator1a = SAR[0.005,0.005,0.01]

cnd1 = (close > indicator1) or (close > indicator1a)

cnd2 = (close < indicator1) or (close < indicator1a)

endif

TIMEFRAME(5 minutes)

count2 = 0

For zz2 = 1 to 11 do

IF range[zz2]=0 THEN

count2= 1

ENDIF

next

if count2=0 then

//Stochastic RSI | indicator

lengthRSIa = 10 //RSI period

lengthStocha = 10 //Stochastic period

smoothKa = 4 //Smooth signal of stochastic RSI

smoothDa = 2 //Smooth signal of smoothed stochastic RSI

myRSIa = RSI[lengthRSIa](close)

MinRSIa = lowest[lengthStocha](myrsia)

MaxRSIa = highest[lengthStocha](myrsia)

if (MaxRSIa-MinRSIa)<>0 then

StochRSIa = (myRSIa-MinRSIa) / (MaxRSIa-MinRSIa)

else

StochRSIa=StochRSIa[1]

endif

K2a = average[smoothKa](stochrsia)*100

D2a = average[smoothDa](K2a)

cnd3 = K2a>D2a

cnd4 = K2a<D2a

endif

TIMEFRAME(default)

// mfe & mae

count3 = 0

For zz3 = 1 to 26 do

IF range[zz3]=0 THEN

count3= 1

ENDIF

next

if count3=0 then

n = 4

nn= 1

maerec=0.01

mferec=0.01

for i=1 to n

maerec=maerec+(high[i]-open[i])

mferec=mferec+(open[i]-low[i])

next

for j=1 to nn

maerec=maerec+(open[j]-low[j])

mferec=mferec+(high[j]-open[j])

next

averecentmael=close-(maerec/nn)

averecentmfel=close+(mferec/nn)

averecentmaes=close+(maerec/n)

averecentmfes=close-(mferec/n)

avgl=(averecentmael+averecentmfel)/2

avgs=(averecentmaes+averecentmfes)/2

avgmfemaes=average[25](avgs)

avgmfemael=average[25](avgl)

periodea = 8

nbchandeliera = 3

mma = average[periodea,1](totalprice)

adjasuroppo = (mma-mma[nbchandeliera]*pipsize) / nbchandeliera

angle = (atan(adjasuroppo))

cb1 = angle < 0

cs1 = angle > 0

cb2=close>totalprice

cs2=close<totalprice

// conditions

condbuy = avgmfemael crosses over avgmfemaes

condbuy = condbuy and cb1 and cnd1 and cnd3

condbuy = condbuy and ((high>high[1] or close>open or low>low[1]))

condbuy=condbuy and cb2 and cb2>cb2[1]

condsell = avgmfemael crosses under avgmfemaes

condsell = condsell and cs1 and cnd2 and cnd4

condsell = condsell and ((high<high[1] or close<open or low<low[1]))

condsell = condsell and cs2 and cs2>cs2[1]

// entry

if condbuy then

buy 1 contract at market

set stop %loss sll

set target %profit ptl

endif

if condsell then

sellshort 1 contract at market

set stop %loss sls

set target %profit pts

endif

endif

hey, thanks Paul – gotta be worth a try. You think it’s better to test it without the trail?

PaulParticipant

Master

I just wanted it to be light and that it opens a position. The exit criteria are not important but have no influence I think about this error. So you could add that.

The code above I’ve put in demo and will let you know if it fails or not.

Hi nonetheless,

Thank you for your code. Just a small suggestion to the //EXIT ZOMBIE TRADE. It helps with both the long and short avg profit/loss figures. The overall result remains more or less the same but the risk are less. The 150 represents the max profit and loss the system takes on the backtest so the logic is that if you do not get to those figures in a reasonable amount of time you might as well cover the position. We all know that small timeframes can change quickly.

//EXIT ZOMBIE TRADE

IF longonmarket and barindex-tradeindex > 250 and close-positionprice<150 then

sell at market

endif

IF shortonmarket and barindex-tradeindex > 350 and positionprice-close<150 then

exitshort at market

endif

@ Paul,

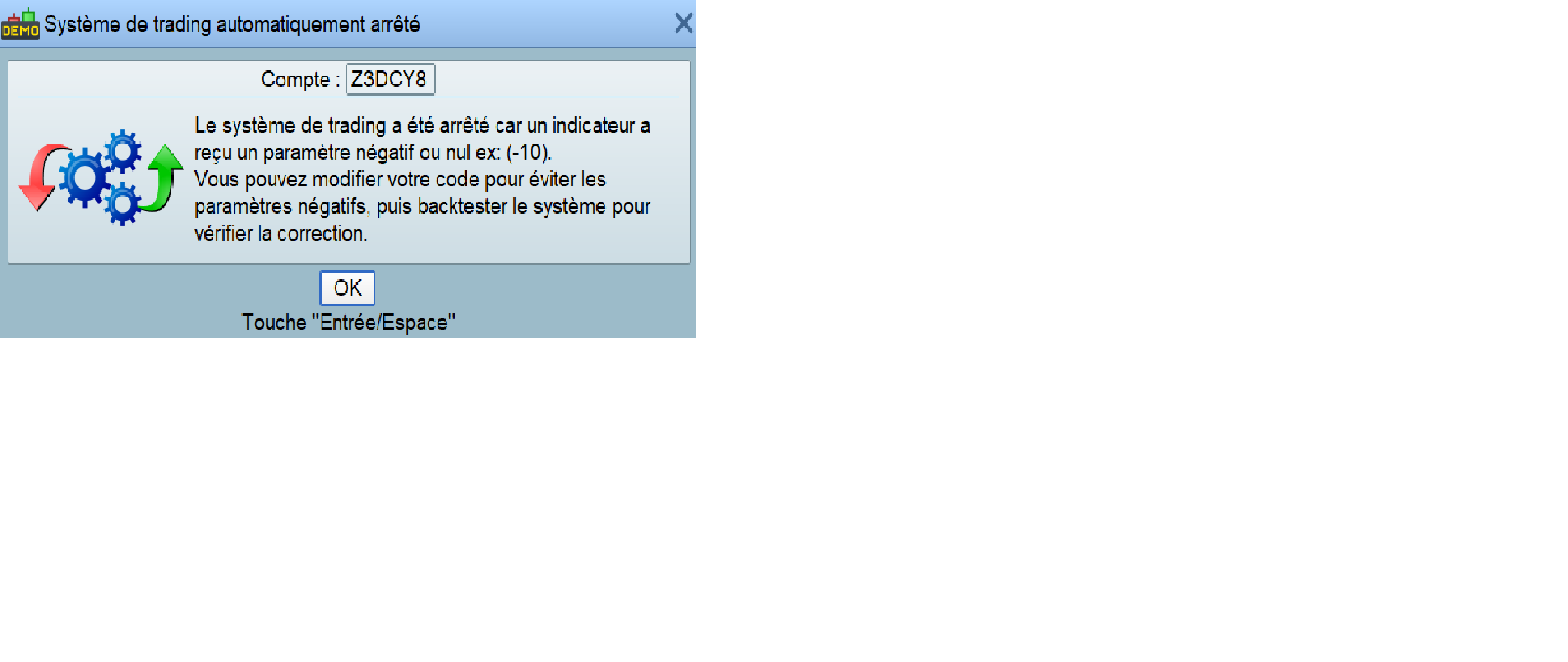

I tested your code, i copy it in @Nonetheless ea.

The EA take an position, and after 1 minute, he closed the position and give an error (the system received a negative parameter or nul )

Here are the itf

I have the same error with DJ1m Maex v4.5 atr

Have a nice day

PaulParticipant

Master

Thnx for testing cgassfr67. There was never had a proper solution for this problem and likely it’s something which just isn’t fixable.

So we can’t use this strategy…?

PaulParticipant

Master

too early to tell, but I tried something new and it’s working so far!… I will post more later.

PaulParticipant

Master

Still no problems in both strategies. If the error occurs ONLY while in position, then don’t calculate the questionable indicators while in position. This means you can’t reverse on opposite signal, but for long/short only it should work which is fine for me.

Like this below, or include all condbuy/condsell conditions. But with mtf it could be a bitmore tricky. Actually I think it’s perhaps not programmed right below. But it’s also in the test. Anyway this is the idea.

//-------------------------------------------------------------------------

// Hoofd code : test div0

//-------------------------------------------------------------------------

defparam cumulateorders = false

defparam preloadbars = 2000

once sll = 0.2 // stoploss long

once sls = 0.2 // stoploss short

once ptl = 0.5 // profit target long

once pts = 0.5 // profit target short

TIMEFRAME(15 minutes)

indicator1 = SuperTrend[2,6]

indicator1a = SAR[0.005,0.005,0.01]

cnd1 = (close > indicator1) or (close > indicator1a)

cnd2 = (close < indicator1) or (close < indicator1a)

TIMEFRAME(5 minutes)

//Stochastic RSI | indicator

lengthRSIa = 10 //RSI period

lengthStocha = 10 //Stochastic period

smoothKa = 4 //Smooth signal of stochastic RSI

smoothDa = 2 //Smooth signal of smoothed stochastic RSI

myRSIa = RSI[lengthRSIa](close)

MinRSIa = lowest[lengthStocha](myrsia)

MaxRSIa = highest[lengthStocha](myrsia)

if (MaxRSIa-MinRSIa)<>0 then

StochRSIa = (myRSIa-MinRSIa) / (MaxRSIa-MinRSIa)

else

StochRSIa=StochRSIa[1]

endif

K2a = average[smoothKa](stochrsia)*100

D2a = average[smoothDa](K2a)

cnd3 = K2a>D2a

cnd4 = K2a<D2a

TIMEFRAME(default)

// mfe & mae

if not onmarket then

n = 4

nn= 1

maerec=0

mferec=0

for i=1 to n

maerec=maerec+(high[i]-open[i])

mferec=mferec+(open[i]-low[i])

next

for j=1 to nn

maerec=maerec+(open[j]-low[j])

mferec=mferec+(high[j]-open[j])

next

averecentmael=close-(maerec/nn)

averecentmfel=close+(mferec/nn)

averecentmaes=close+(maerec/n)

averecentmfes=close-(mferec/n)

avgl=(averecentmael+averecentmfel)/2

avgs=(averecentmaes+averecentmfes)/2

avgmfemaes=average[25](avgs)

avgmfemael=average[25](avgl)

periodea = 8

nbchandeliera = 3

mma = average[periodea,1](totalprice)

adjasuroppo = (mma-mma[nbchandeliera]*pipsize) / nbchandeliera

angle = (atan(adjasuroppo))

cb1 = angle < 0

cs1 = angle > 0

else

cb1=0

cs1=0

endif

cb2=close>totalprice

cs2=close<totalprice

// conditions

condbuy = avgmfemael crosses over avgmfemaes

condbuy = condbuy and cb1 and cnd1 and cnd3

condbuy = condbuy and ((high>high[1] or close>open or low>low[1]))

condbuy=condbuy and cb2 and cb2>cb2[1]

condsell = avgmfemael crosses under avgmfemaes

condsell = condsell and cs1 and cnd2 and cnd4

condsell = condsell and ((high<high[1] or close<open or low<low[1]))

condsell = condsell and cs2 and cs2>cs2[1]

// entry

if condbuy then

buy 1 contract at market

set stop %loss sll

set target %profit ptl

endif

if condsell then

sellshort 1 contract at market

set stop %loss sls

set target %profit pts

endif

I had the stripped down version on test for a while and it worked fine, but as soon as I added the MM and the trail then I kept getting the zero parameter error. That was on 1m.

Have you been testing the above at 10sec?

If so then the upper TFs could probably be brought down to maybe 1m and 5m, but would need re-optimizing. I’ll try it later if i get the time.

Hello guys!

Have you thought about changing the Money Management? Maybe the problem comes from this…!

Could you try something like:

ONCE factor = 8 // factor of 10 means margin will increase/decrease @ 10% of strategy profit; factor 20 = 5% etc

@Paul, could you upload your two .itf?