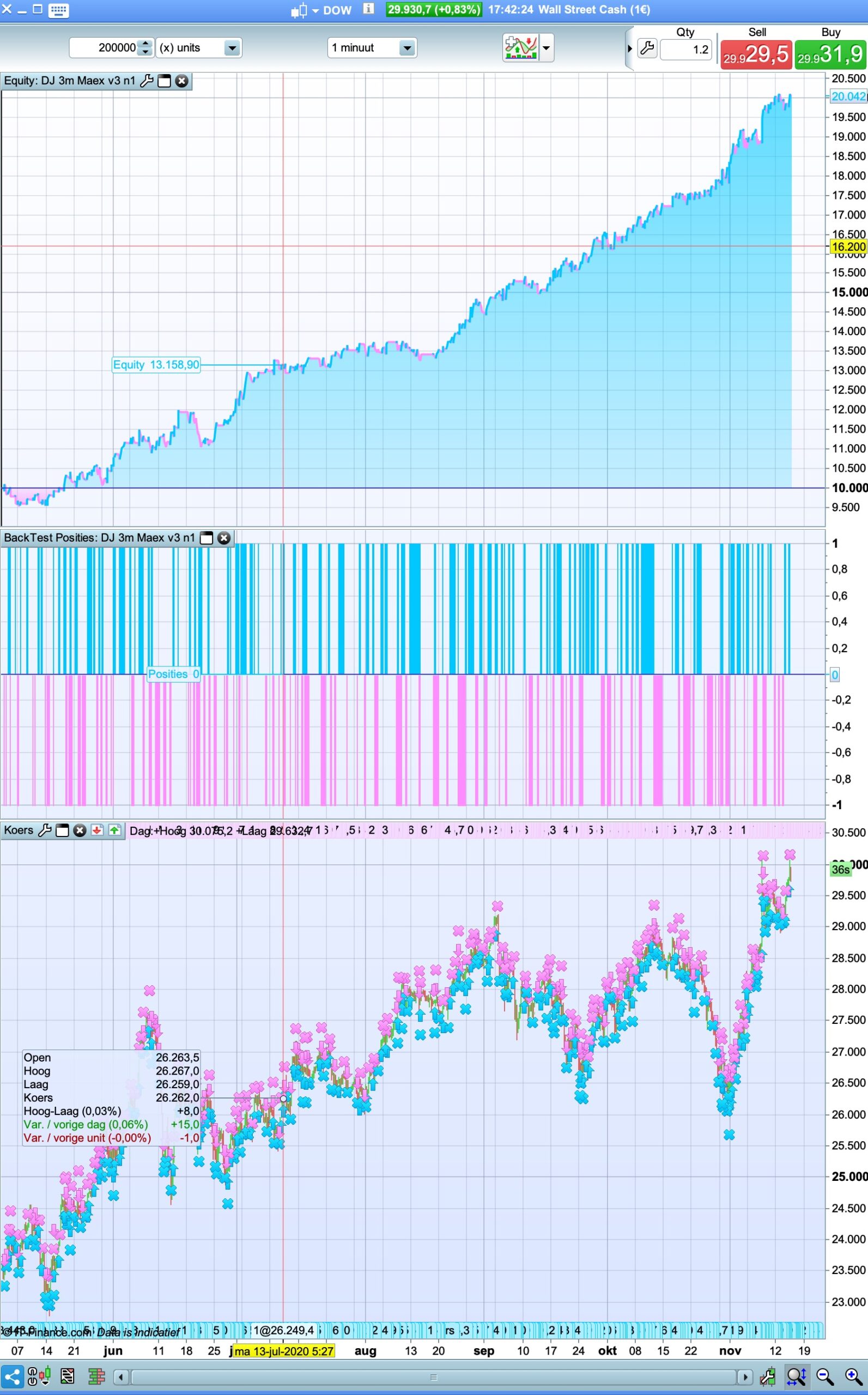

Paul your DJ-3m-Maex-v3.itf gives loads better equity curve on 1 min TF.

Thank You for sharing.

Paul

PaulParticipant

Master

nice work Nonetheless! It’s very difficult to find good oos results. Also I like the size of the stoploss in comparison to the ts atr values used and the way you used the breakeven. It’s rewarding to see in the first day with a positive result!

v3 is not as refined but the intend was to swap indicators in/out and compare the two methods. I will work on it a bit more.

PaulParticipant

Master

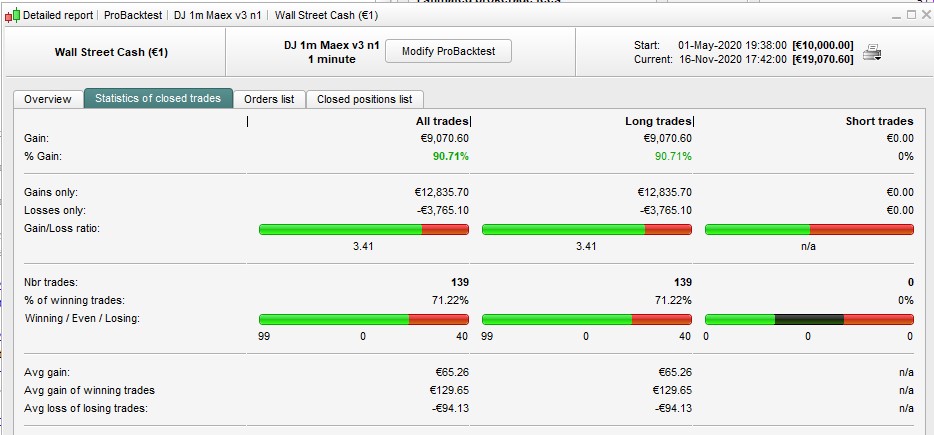

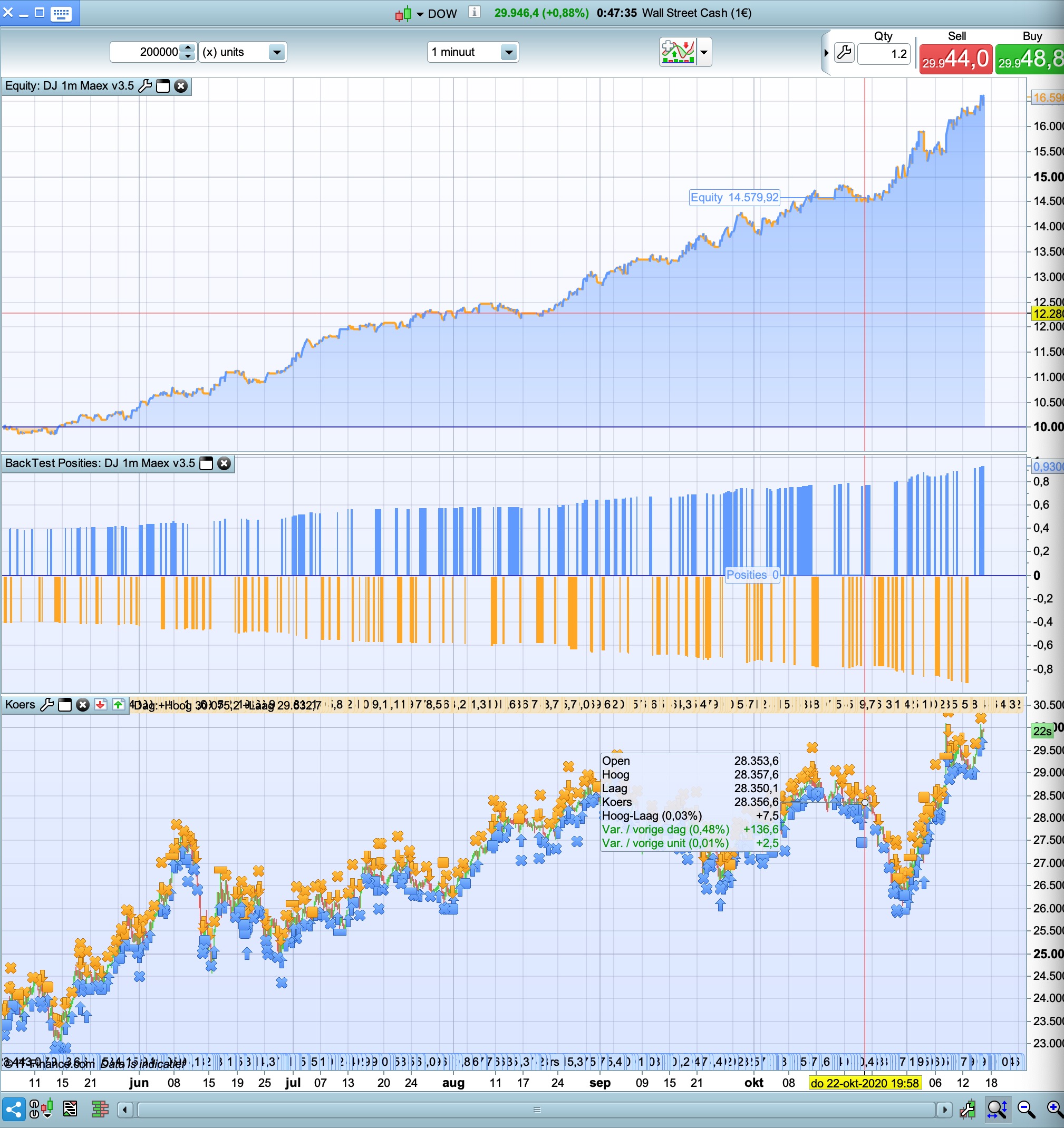

@nonetheless I included your setup in a clean v3 and results are interesting!

Didn’t optimise, it’s also setup for short & long

long & short together have improvement and doesn’t break the strategy which is often the case when optimised for long only!

long only & close on short signal improve equitycurve shape, drawdawn and average losses.

Now I will review how to speed up the code in calculation.

Sharing works because without sharing I doubt very much if I would ‘ve got such results!

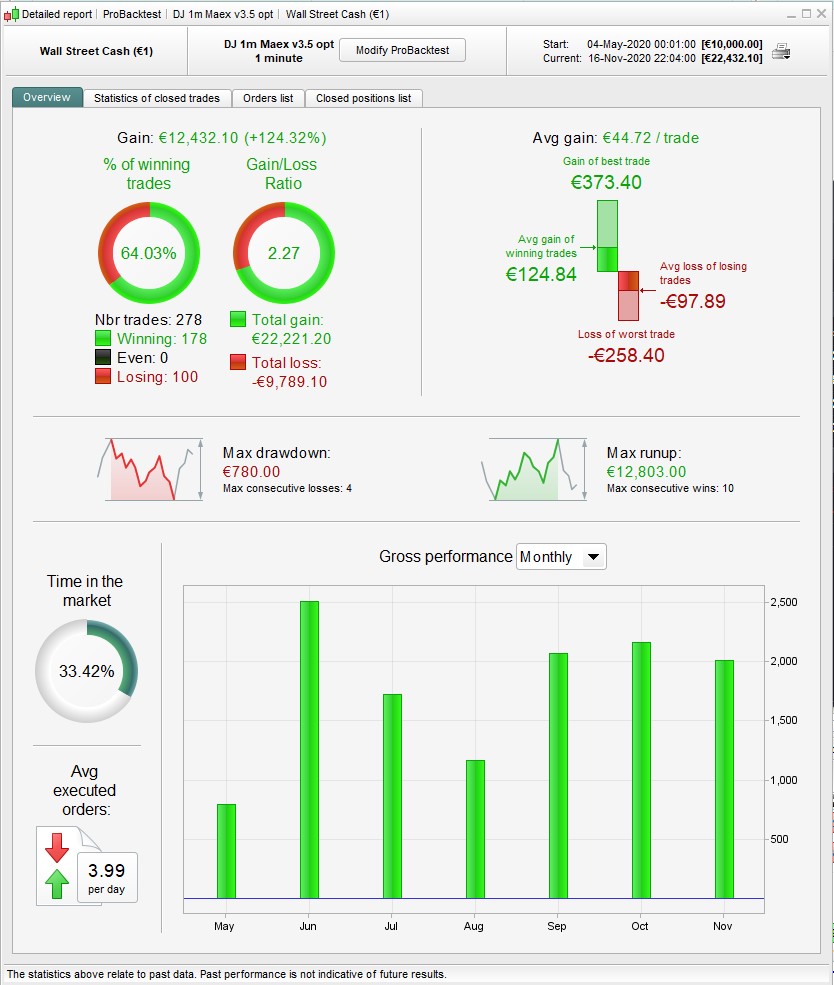

Well yes, it is interesting, partly because in 6 months there is precisely 0 short trades … which can’t be right. (kind of explains why the 2 histograms you posted are almost identical!)

I think it might be the vectorial ??

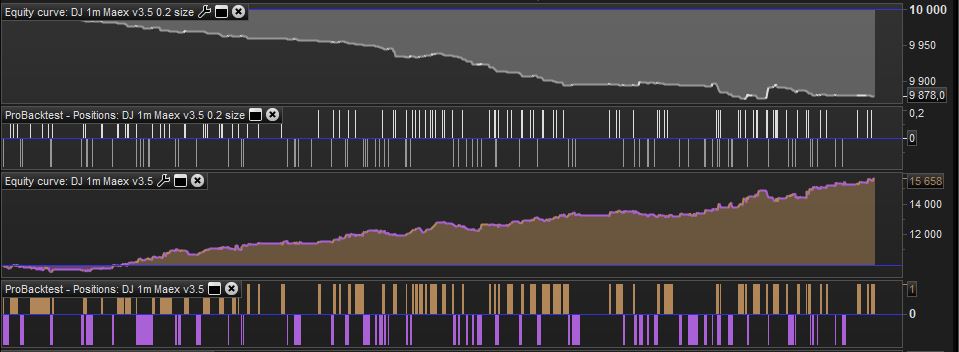

when i change positionsize to 0.2, results sucks, why?

when i change positionsize to 0.2

seems ok to me. which version are you running?

PaulParticipant

Master

nonetheless, tradetype is set to 2 for long only?

closeonreversal is to close a long position if a short signal for entry appears, to close only but not to enter short.

There are a few other things, forgot to include mm, change the name to 1m etc.

0.2 seems fine with me too, on a 1m chart.

tradetype is set to 2 for long only?

Yes – sorry! my bad, didn’t notice you had added a long/short selector 🙄

Pauls version DJ-3m-Maex-v3-n1, changes from 70% hitrate and 3 G/L to 30% hitrate and 0.3 G/L ratio

here’s a refurb of the v3 Long/Short – looking good, at least for those 6 months! (2 oos)

Thanks for your great work on this, Paul.

One problem though is that it doesn’t seem to work with MM – not with my code or with another that I tried – completely peculiar results with either. Obviously some conflict but I can’t see what it is. Any idea?

changes from 70% hitrate and 3 G/L to 30% hitrate and 0.3 G/L ratio

check the CTime setting, you’re prob running on UK time

no, all i do is change positionssize in line 15 to 0.2, tested with both ct time settings. Both works good with 1 contract as size, but 0.2 makes the system lose. You versions works when changing positionsize, but not pauls…

same with your latest version as well nonetheless. All i changed in these two is line 6, from 1 to 0.2

same with your latest version as well

ok, now I’m getting that as well, only just noticed. Probably connected to why the MM won’t work. I’ll have another look at it tomorrow…

PaulParticipant

Master

Obviously some conflict but I can’t see what it is. Any idea?

Yes, countpos is not compatible with mm. Delete the part what defines the stoploss & profittarget and the row countpos=..

then replace the entrylines with this. (it only adds the set orders after each buy/sellshort command)

// entry

if ctime then

if tradetype=1 or tradetype=2 then

if condbuy and (not longonmarket or shortonmarket) then

buy positionsize contract at market

set stop %loss sll

set target %profit ptl

endif

if condbuy and longonmarket then

if reenter=1 then

positionperformance=0

elsif reenter=2 then

positionperformance=1

elsif reenter=3 then

positionperformance=positionperf(0)<0

elsif reenter=4 then

positionperformance=positionperf(0)>0

endif

if positionperformance then

buy positionsize contract at market

set stop %loss sll

set target %profit ptl

endif

endif

endif

if closeonreversal and tradetype=2 and condsell then

sell at market

endif

if tradetype=1 or tradetype=3 then

if condsell and (not shortonmarket or longonmarket) then

sellshort positionsize contract at market

set stop %loss sls

set target %profit pts

endif

if condsell and shortonmarket then

if reenter=1 then

positionperformance=0

elsif reenter=2 then

positionperformance=1

elsif reenter=3 then

positionperformance=positionperf(0)<0

elsif reenter=4 then

positionperformance=positionperf(0)>0

endif

if positionperformance then

sellshort positionsize contract at market

set stop %loss sls

set target %profit pts

endif

endif

if closeonreversal and tradetype=3 and condbuy then

exitshort at market

endif

endif

else

if condbuy then

//exitshort at market

endif

if condsell then

//sell at market

endif

endif