Hi everyone,

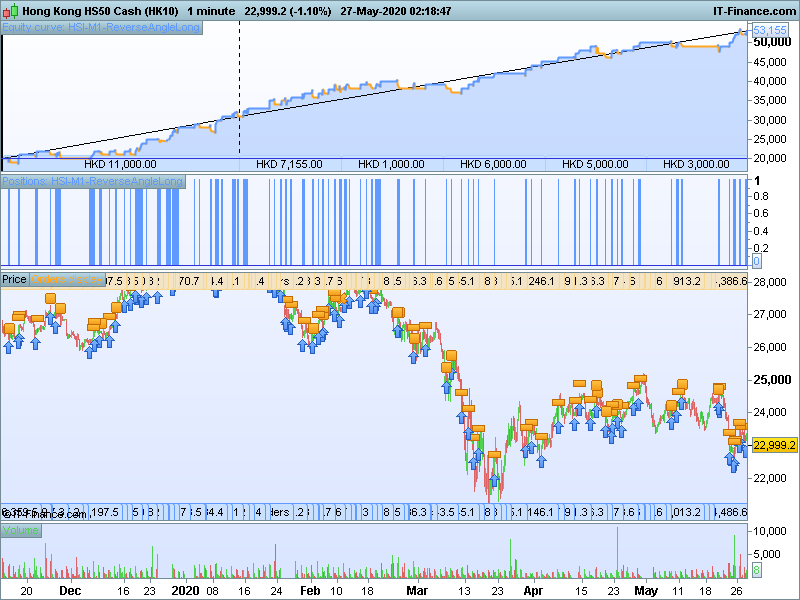

Here is a new strategy on Hang Seng 1 min TF. It measures the angle of the slope and looking for a V-slope. As unit of price and bar is not the same, thus replaced the bar with ATR (with higher period) to have in relative price to price comparison.

Looking forward for your suggestion and ideas of improvement.

DEFPARAM CumulateOrders = false

DEFPARAM PRELOADBARS = 2000

//Money Management

MM = 0 // = 0 for optimization

if MM = 0 then

positionsize = 1

ENDIF

if MM = 1 then

once maxSize = 2

once minSize = 1

once startingsize = 1

once stepsize = 0.5

once resetafterlost = 0

once doublestepdown = 0

once resetafterstrikewin = 2

once positionsize = startingsize

once wincount = 0

if strategyprofit <> strategyprofit[1] then

if positionperf(1)>0 then

if positionsize < maxSize then

positionsize = positionsize + stepsize

endif

wincount = wincount + 1

if wincount >= resetafterstrikewin then

positionsize = startingsize

wincount = 0

endif

else

if resetafterlost then

positionsize = startingsize

elsif doublestepdown then

positionsize = positionsize - stepsize * 2

else

positionsize = positionsize - stepsize

endif

wincount = 0

endif

endif

if positionsize < minSize then

positionsize = minSize

endif

ENDIF

timedaytrade = (time > 093100 + waitmin) AND (time < 120000) OR (time > 130000 + waitmin AND time < 155500)

timeok = timedaytrade

//====== Enter market - start =====

samebarsignal = 0

M1atrAB = AverageTrueRange[periodA + periodB](close)

//Look for V shape

adjacentA = (close - close[periodA]) / M1atrAB

angelA = atan(adjacentA)

adjacentB = (close[periodA] - close[periodA + periodB]) / M1atrAB[periodA]

angelB = atan(adjacentB)

C1 = angelB < longB AND angelA > longA

// LONG side

IF timeok AND Not OnMarket AND C1 AND samebarsignal = 0 THEN

BUY positionsize CONTRACT AT MARKET

SET STOP pLOSS SL

TP = RR * SL

SET TARGET pPROFIT TP

samebarsignal = 1

ENDIF

//====== Enter market - end =====

//====== Exit market - start =====

IF NOT ONMARKET THEN

ENDIF

//====== Exit market - end =====

Hi,

Can you try to backtest this strategy with a breakeven and maybe a filter on M5

With 200k, i get 100%.

for example

DEFPARAM CumulateOrders = false

DEFPARAM PRELOADBARS = 2000

//Money Management

MM = 0 // = 0 for optimization

if MM = 0 then

positionsize = 1

ENDIF

if MM = 1 then

once maxSize = 2

once minSize = 1

once startingsize = 1

once stepsize = 0.5

once resetafterlost = 0

once doublestepdown = 0

once resetafterstrikewin = 2

once positionsize = startingsize

once wincount = 0

if strategyprofit <> strategyprofit[1] then

if positionperf(1)>0 then

if positionsize < maxSize then

positionsize = positionsize + stepsize

endif

wincount = wincount + 1

if wincount >= resetafterstrikewin then

positionsize = startingsize

wincount = 0

endif

else

if resetafterlost then

positionsize = startingsize

elsif doublestepdown then

positionsize = positionsize - stepsize * 2

else

positionsize = positionsize - stepsize

endif

wincount = 0

endif

endif

if positionsize < minSize then

positionsize = minSize

endif

ENDIF

timedaytrade = (time > 093100 + waitmin) AND (time < 120000) OR (time > 130000 + waitmin AND time < 155500)

timeok = timedaytrade

timeframe(5minutes,updateonclose)

st = close > supertrend[5,4]

timeframe(default)

//====== Enter market - start =====

samebarsignal = 0

M1atrAB = AverageTrueRange[periodA + periodB](close)

//Look for V shape

adjacentA = (close - close[periodA]) / M1atrAB

angelA = atan(adjacentA)

adjacentB = (close[periodA] - close[periodA + periodB]) / M1atrAB[periodA]

angelB = atan(adjacentB)

C1 = angelB < longB AND angelA > longA

// LONG side

IF timeok AND Not OnMarket AND C1 AND samebarsignal = 0 and st THEN

BUY positionsize CONTRACT AT MARKET

SET STOP pLOSS SL

TP = RR * SL

SET TARGET pPROFIT TP

samebarsignal = 1

ENDIF

//====== Enter market - end =====

//====== Exit market - start =====

IF NOT ONMARKET THEN

ENDIF

//====== Exit market - end =====

// breakeven stop atr

once breakevenstoptype = 1 // breakeven stop - 0 off, 1 on

once breakevenstoplong = 1 // breakeven stop atr relative distance

once breakevenstopshort = 1 // breakeven stop atr relative distance

once pointstokeep = 5 // positive or negative

once atrperiodbreakeven = 14 // atr parameter value

once minstopbreakeven = 36 // minimum breakeven stop distance

//----------------------------------------------

atrbreakeven = averagetruerange[atrperiodbreakeven]((close/10)*pipsize)/1000

//atrbreakeven=averagetruerange[atrperiodbreakeven]((close/1)*pipsize) // (forex)

bestopl = round(atrbreakeven*breakevenstoplong)

bestops = round(atrbreakeven*breakevenstopshort)

if breakevenstoptype = 1 then

//

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

maxpricebe = 0

minpricebe = close

newslbe = 0

endif

//

if longonmarket then

maxpricebe = max(maxpricebe,close)

if maxpricebe-tradeprice(1)>=bestopl*pointsize then

if maxpricebe-tradeprice(1)>=minstopbreakeven then

newslbe=tradeprice(1)+pointstokeep*pipsize

else

newslbe=tradeprice(1)- minstopbreakeven*pointsize

endif

endif

endif

//

if shortonmarket then

minpricebe = min(minpricebe,close)

if tradeprice(1)-minpricebe>=bestops*pointsize then

if tradeprice(1)-minpricebe>=minstopbreakeven then

newslbe = tradeprice(1)-pointstokeep*pipsize

else

newslbe = tradeprice(1) + minstopbreakeven*pointsize

endif

endif

endif

//

if longonmarket then

if newslbe>0 then

sell at newslbe stop

endif

if newslbe>0 then

if low < newslbe then

sell at market

endif

endif

endif

//

if shortonmarket then

if newslbe>0 then

exitshort at newslbe stop

endif

if newslbe>0 then

if high > newslbe then

exitshort at market

endif

endif

endif

endif

Thanks @MAKSIDE for the idea.

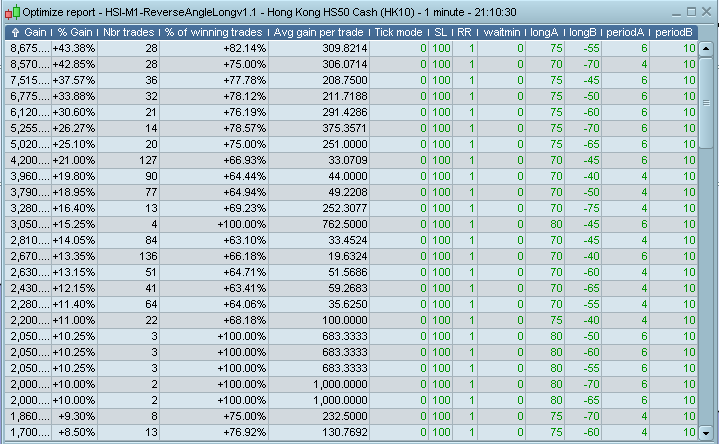

For the 100% result, I guess you mean win rate? Not sure why, but I don’t get the same result with the parameters I set in the .itf.

If re-optimize the parameters, I have some combination giving 100% win rate, but the trade number is way too low <5. Do you observe the same?

If possible, can you please share the .itf?

Thanks. It seems the trades are too little. I’m not expert, but personally, I felt the number of trade is too little to justify the consistency thus I will not have confident. But just me…

hello how did you define x and y to make the code work?

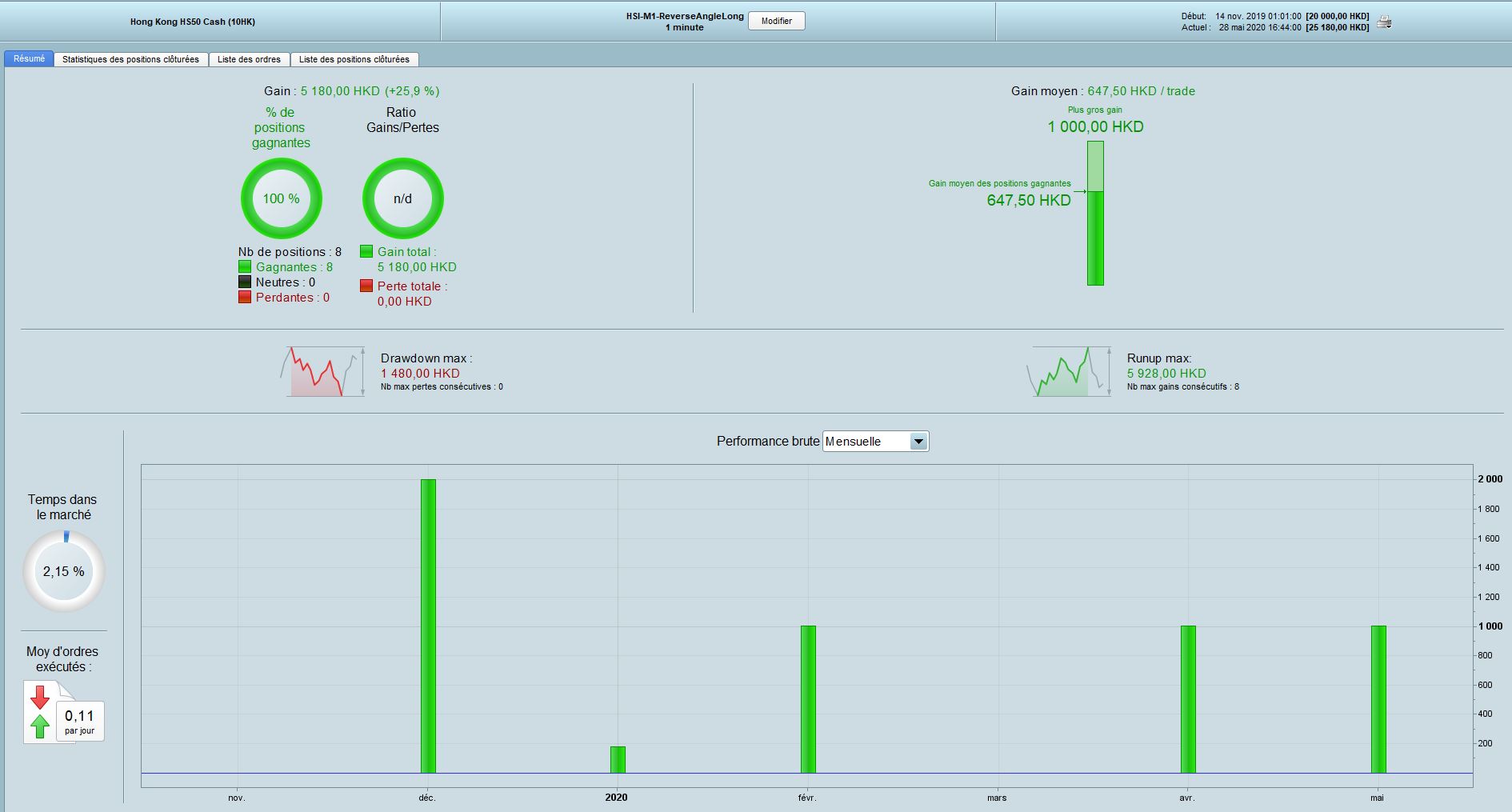

I don’t see an optimization report to help with the decision ..? Thank you Best regards.

Hi DowJones

Thanks for your work

Something I dn’t understand is the ATR instead of a number of bars ?

adjacentB = (close[periodA] - close[periodA + periodB]) / M1atrAB[periodA]

angelB = atan(adjacentB)

Because to calculate Arctangente you need the opposite side : (close[periodA] – close[periodA + periodB] Thant’s ok

But M1atrAB[periodA] is not the adajacent side ?

I understand your explannations but don’t think it will be the same

Cheers

And I don’t understand this part of your code

if resetafterlost then

positionsize = startingsize

elsif doublestepdown then

positionsize = positionsize - stepsize * 2

else

positionsize = positionsize - stepsize

endif

wincount = 0

endif

Because I think you decrement position size when position perf is negative but resetafterlost is always at 0 and doublestepdown too.

Does something mis as a count on loss trades ?

Thanks

I understand your explannations but don’t think it will be the same

Hi @zilliq, indeed. I understand your concern. Using ATR is just taking the reference where x bar in average moved by y point (range). Rather than taking directly the bar, because the bar unit is totally not relevant with point unit. For sure both analogy is still not the same like measuring with ruler with centimeter, but at least using bar vs point are less relevant, e.g. from 5 bars, it moves from 21000 to 21150, so taking arctan of 5 and 150 vs from 5 bars, ATR is 50, it moves from 21000 to 21150, so taking arctan of 50 and 150

but resetafterlost is always at 0 and doublestepdown too

From GRAPH, right? Because I never activate it (line 5) 🙂 I left it like a template and forget to remove it.

MM = 0 // = 0 for optimization

Thanks for you answer Dowjones. I understand for ATR, it’s a different point of view

For the second part, sorry for my bad explanations

I said that resetafterlost is always at 0 so the condition is always at ON (instead to be at 0 some times and if positionsperf(1)<0 to be at 1 for example) and same for doublestepdown. So how can the code understand wich choice to use ?

Hope to be clear

So how can the code understand wich choice to use ?

Ah, sorry for misunderstanding. These are actually configuration parameter, to be chosen accordingly which is preferred.

once maxSize = 2

once minSize = 1

once startingsize = 1

once stepsize = 0.5

once resetafterlost = 0

once doublestepdown = 0

once resetafterstrikewin = 2

Whether you prefer to reset the lot back to startingsize once hit a single loss trade, or you prefer to doublestepdown. It is choice need to be made.

So if you choose resetafterlost, then doublestepdown will not be applicable even if you set it to 1. By default, all are set to 0, so once there is a loss trade, the lot size will be reduced by sizestep

Understand, Thanks

I thought it depends of the configuration of the code

have a nice evening