Léo

LéoParticipant

Average

Dear All,

I hope I am posting this subject in the correct section of the website.

I have no experience in programming and I think that the best way for me to understand the codes posted on this website is to try to work on my own projects.

Therefore I tried to write the code below, the idea is to take position when prices crosses MM7 and x prior closes are above or under MM7. A lot of it is based on the SL strategies that I found in a thread created by Gianluca and originaly developped by Nicolas and Ale.

I assume there is a lot of mistakes in this code, but I hardly see my mistake myself.

Can you please comment on this ?

Thank you all for your contribution to this website, very much appreciated.

Best regards.

Alex.

//-------------------------------------------------------------------------

// Code principal : Break MM7 H4 Dax

// Stop strategy adapted from Gianluca/Nicolas/Ale https://www.prorealcode.com/topic/trailing-stop-and-breakeven-codes/

//-------------------------------------------------------------------------

// Dax - IG MARKETS// TIME FRAME H4

//idea1 : Buy when Close crosses over MM7 and Close for the X previous periods were below MM7 (X=5 in this first code)

//idea2 : Set initial SL on the lowest of the X previous periods (X=5 in this first code)

//idea3 : Move SL to entry point when profit > 300 pts

//idea4 : Move SL to highest Close when Close crosses under MM7

//idea5 : If SL > 300 pts no trade

DEFPARAM CumulateOrders = false

MM7= Average[7]

C1= Close crosses over MM7 and Close[1]<MM7[1] and Close[2]<MM7[2] and Close[3]<MM7[3] and Close[4]<MM7[4] and Close[5]<MM7[5]

C2= Close crosses under MM7 and close[1]>MM7[1] and Close[2]>MM7[2] and Close[3]>MM7[3] and Close[4]>MM7[4] and Close[5]>MM7[5]

LongSLvalue= high-lowest[5](low)

ShortSLvalue= highest[5](high)-low

if not onmarket then

if C1 and longSLvalue < 300 then

buy 1 contract at (high+1) stop

endif

if C2 and shortSLvalue < 300 then

sell 1 contract at (low-1) stop

endif

endif

// Stop strategy adapted from Gianluca/Nicolas/Ale https://www.prorealcode.com/topic/trailing-stop-and-breakeven-codes/

//1/TRAILING STOP//////////////////////////////////////////////////////

once trailinstop= 1 //1 on - 0 off

trailingstart = 300 //trailing will start @trailinstart points profit

trailingstep = 5 //trailing step to move the "stoploss"

//1 trailing stop function

if trailinstop>0 then

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

// set initial SL

if newSL=0 then

newSL=longSLvalue

endif

//first move (breakeven)

IF newSL>0 AND close-tradeprice(1)>=trailingstart*pipsize THEN

newSL = tradeprice(1)+trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND close crosses under MM7 THEN

newSL = low-1

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//Set initial SL

if newSL=0 then

newSL=shortSLvalue

endif

//first move (breakeven)

IF newSL>0 AND tradeprice(1)-close>=trailingstart*pipsize THEN

newSL = tradeprice(1)-trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND close crosses over MM7 THEN

newSL = high+1

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

endif

///////////////////////////

LéoParticipant

Average

Dear All,

still trying to work on this strategy.

I tried the code below which works well on long position but does not take any short position.

I think I must be missing something very obvious.

Could someone help please ?

Best regards.

Alex.

DEFPARAM CumulateOrders = false

TaillePosition=5

SMA= Average[PeriodeMM]

C1= Close crosses over SMA and Summation[X](Close<SMA)=(X-1)

C2= Close crosses under SMA and Summation[X](Close>SMA)=(X-1)

LongSLvalue= high-lowest[5](low)

ShortSLvalue= highest[5](high)-low

if not longonmarket then

if C1 and longSLvalue < 300 then

buy TaillePosition contract at (high+1) stop

set stop ploss LongSLvalue

endif

endif

if not shortonmarket then

if C2 and shortSLvalue < 300 then

sell TaillePosition contract at (low-1) stop

set stop ploss ShortSLvalue

endif

endif

Change SELL to SELLSHORT in line 22.

BUY opens a long position.

SELL closes a long position

SELLSHORT opens a short position.

EXITSHORT closes a short position.

SMA should be as below, but as Longs have executed then I guess the default (Close) is being assumed by the code?

SMA= Average[PeriodeMM](Close)

Yes GraHal, CLOSE is assumed if that parameter is missing.

But I prefer to always add all parameters without caring about built-in assumptions.

LéoParticipant

Average

Dear Grahal, Vonasi and Roberto,

Thank you for your help – much appreciated.

I updated the code accordingly and backtested on Dow Jones in 1H. Results are not great Especially prior to 2015 but not so bad since.

I will try to optimize X and SMA and repost it here if I find good parameters.

Thank you again for your help.

DEFPARAM CumulateOrders = false

TaillePosition=1

SMA= Average[PeriodeMM](close)

C1= Close crosses over SMA and Summation[X](Close<SMA)=(X-1)

C2= Close crosses under SMA and Summation[X](Close>SMA)=(X-1)

LongSLvalue= high-lowest[5](low)

ShortSLvalue= highest[5](high)-low

if not onmarket then

if C1 and longSLvalue < 300 then

buy TaillePosition contract at (high+1) stop

set stop ploss LongSLvalue

endif

else

if C2 and shortSLvalue < 300 then

sellshort TaillePosition contract at (low-1) stop

set stop ploss ShortSLvalue

endif

endif

If onmarket then

if C1 and longSLvalue < 300 then

exitshort TaillePosition contract at (high+1) stop

endif

else

if C2 and shortSLvalue < 300 then

sell TaillePosition contract at (low-1) stop

endif

endif

LéoParticipant

Average

Hi All,

I simplified the code as below and tested different combinations for PMM and X.

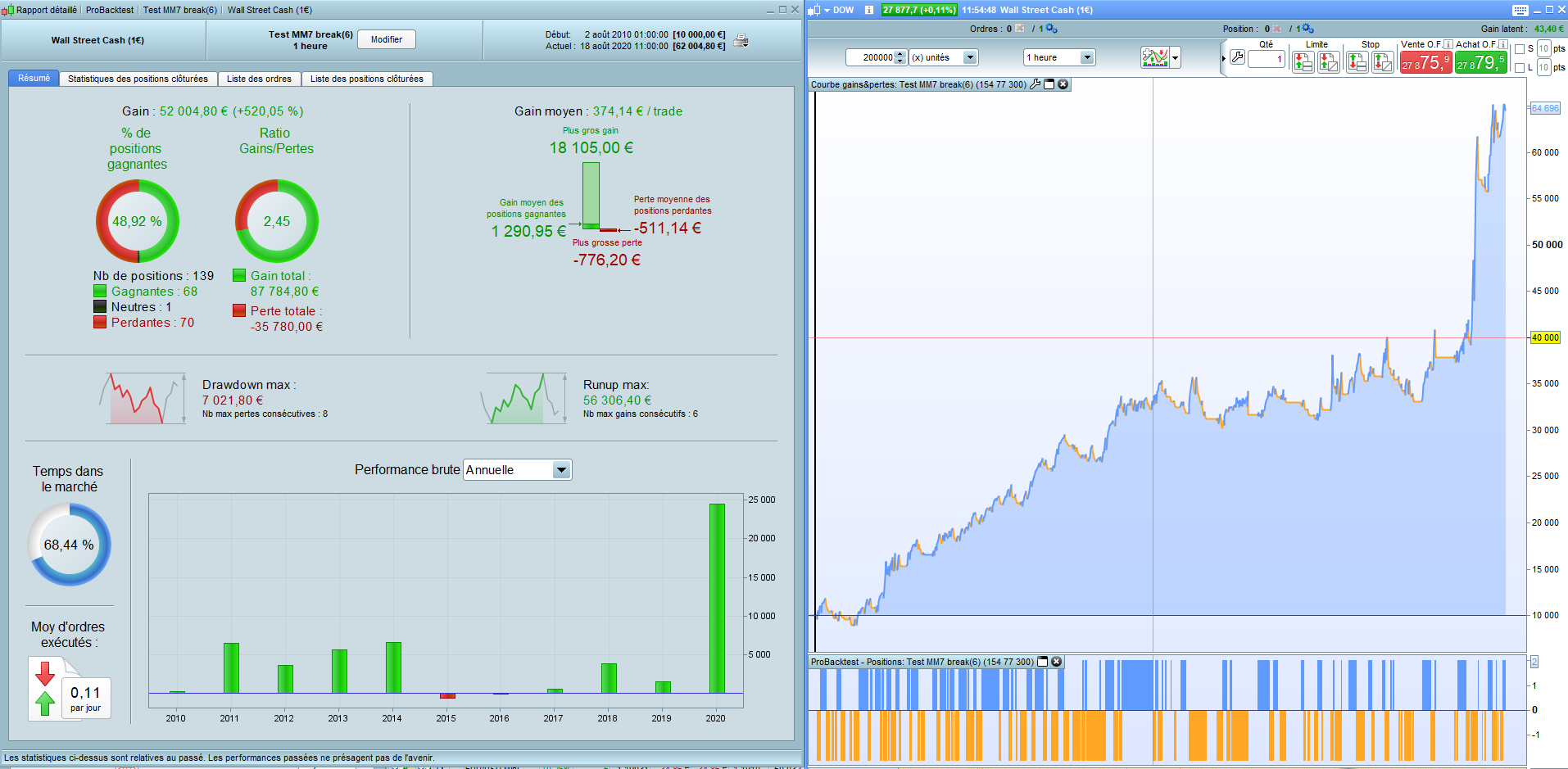

Best results for Dow H1 are with PMM=154 and X=77. (2020 show particularly good results as it was able to capture most of the Feb/March adjustment).

Results are even better with larger SL but I found 300 good for now.

As mentionned this is experimental, but I am happy to hear your comments.

Thanks.

Alex.

DEFPARAM CumulateOrders = false

TaillePosition=2

PeriodeMM = PMM //154

X = XX //77

SLValue = SLV //300

SMA= Average[PeriodeMM](close)

C1= Close crosses over SMA and Summation[X](Close<SMA)=(X-1)

C2= Close crosses under SMA and Summation[X](Close>SMA)=(X-1)

if not longonmarket and C1 then

buy TaillePosition contract at (high+1) stop

set stop ploss SLValue

endif

if not shortonmarket and C2 then

sellshort TaillePosition contract at (low-1) stop

set stop ploss SLValue

endif

if C1 and shortonmarket then

set stop ploss SLValue

endif

if C2 and longonmarket then

set stop ploss SLValue

endif

Beware of over fitting. Divide your optimizing period into at least 1 IS+ 1 OOS periods.

Optimize on 70% of history (In-Sample period) and test the robustness (validation of optimized variables) with the 30% of history (the Out Of Sample period). You can automate this process with the walk forward tool: https://www.prorealcode.com/blog/learning/prorealtime-walk-analysis-tool/

(french videos: Analyse Walk Forward avec ProRealTime et Récapitulatif sur l’utilisation du module Walk Forward sous ProRealTime)

LéoParticipant

Average

Dear Nicolas,

Thank you for this link. I have been through them now and will try backtest + roll forward and post the results here.

Best regards.

LéoParticipant

Average

Dear Nicolas,

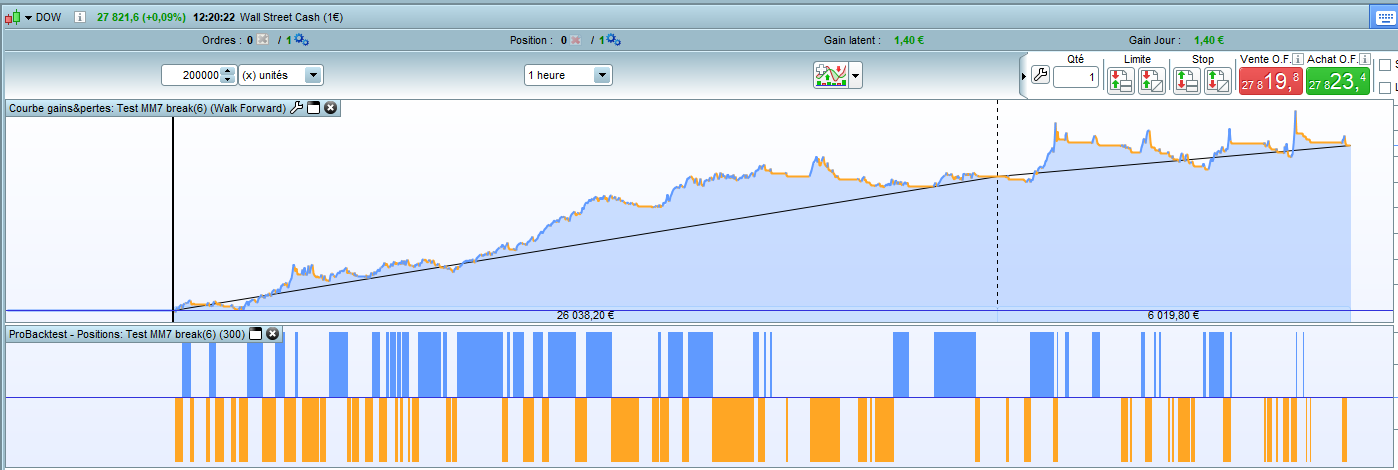

I worked on parameters using one IS / OOS (70/30) period as suggested (Dow 1h, 200’000 bars, Tick by tick mode).

WFE is 53,8 % using 150 for PMM and 112 for XX – which I understand is not so bad. I understand it would make sense to have more than one IS/OOS but it is running super slowly.

Alex.

That’s how you have to proceed, well done. If you have put your strategy live at the same moment of the vertical dotted line, then you had made this nice profit (of the OOS period).

LéoParticipant

Average

Thank you Nicolas !

Draw down is important and got worst on the OOS period.

Despite a RR of 2 I am not sure this would be worse to try live !

Alex

Ok, that’s why robustness test is important and should by conducted by anyone creating strategies.

LéoParticipant

Average

Dear Nicolas,

Maybe you can help to understand the issue I have.

I am testing the code below with variables to optimize PMM, XX, SLa and TPa.

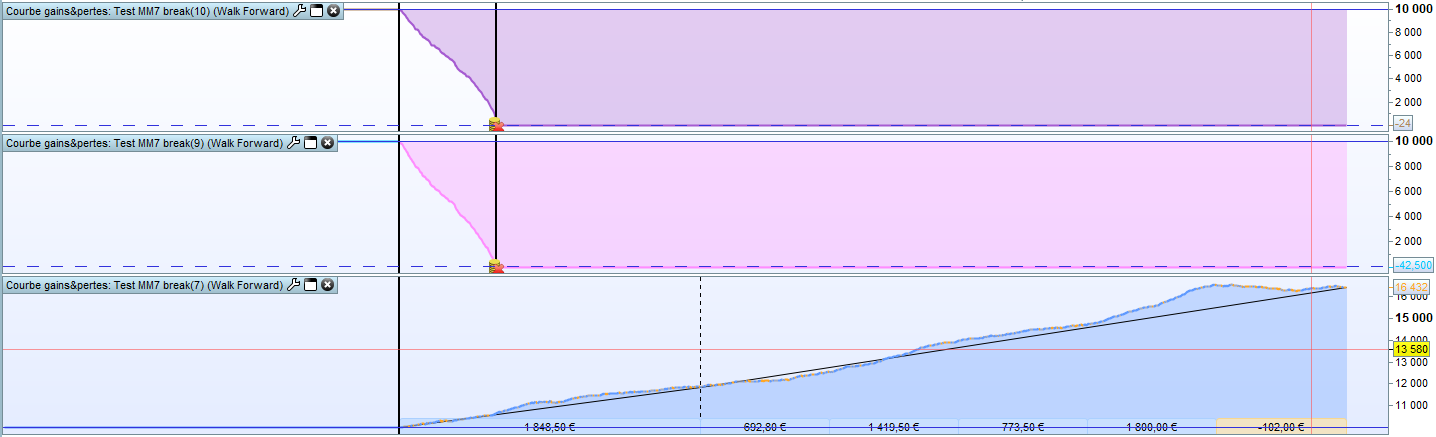

The walk forward analysis below (TEST MM7 Break(7)) shows that the best variables would be PMM = 6 or 7, XX = 5 and SLa and TPa = 5 (200 K bares, Tick by tick, spread = 1 )

When I replace the variables in the code for PMM=6, XX=5 SLa=5 and TPa=5 (Test MM7 Break(9)) or PMM=7, XX=5 SLa=5 and TPa=5 (Test MM7 Break(10)) the stratgey fails after few months (200 K bares, Tick by tick, spread = 1 ).

I would have expected a gain curve more or less in line with the results of the walkforward analysis.

I definetly miss something – Can you please help ?

Thank you !

Alex.

DEFPARAM CumulateOrders = false

TaillePosition=1

PeriodeMM = PMM

X = XX

SL = SLa

TP = TPa

SMA= Average[PeriodeMM](close)

ATR = abs(close - open) > ATR * 2

C1= Close crosses over SMA

C1= C1 and Summation[X](Close<SMA)=(X-1)

C1= C1 and ATR

C2= Close crosses under SMA

C2= C2 and Summation[X](Close>SMA)=(X-1)

C2 = C2 and ATR

if not longonmarket and C1 then

buy TaillePosition contract at (high+1) stop

endif

if not shortonmarket and C2 then

sellshort TaillePosition contract at (low-1) stop

endif

set stop ploss SL

Set target pprofit TP