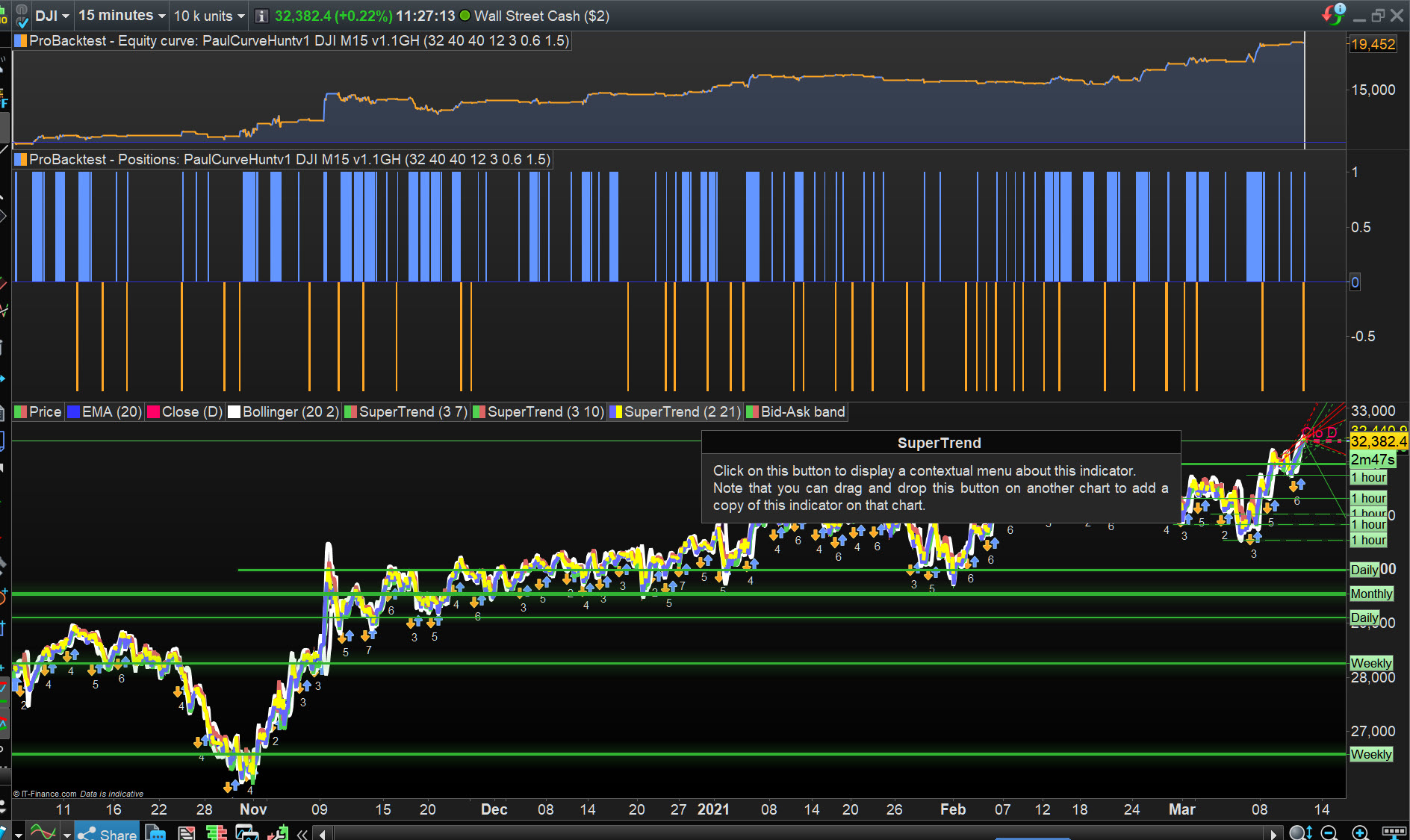

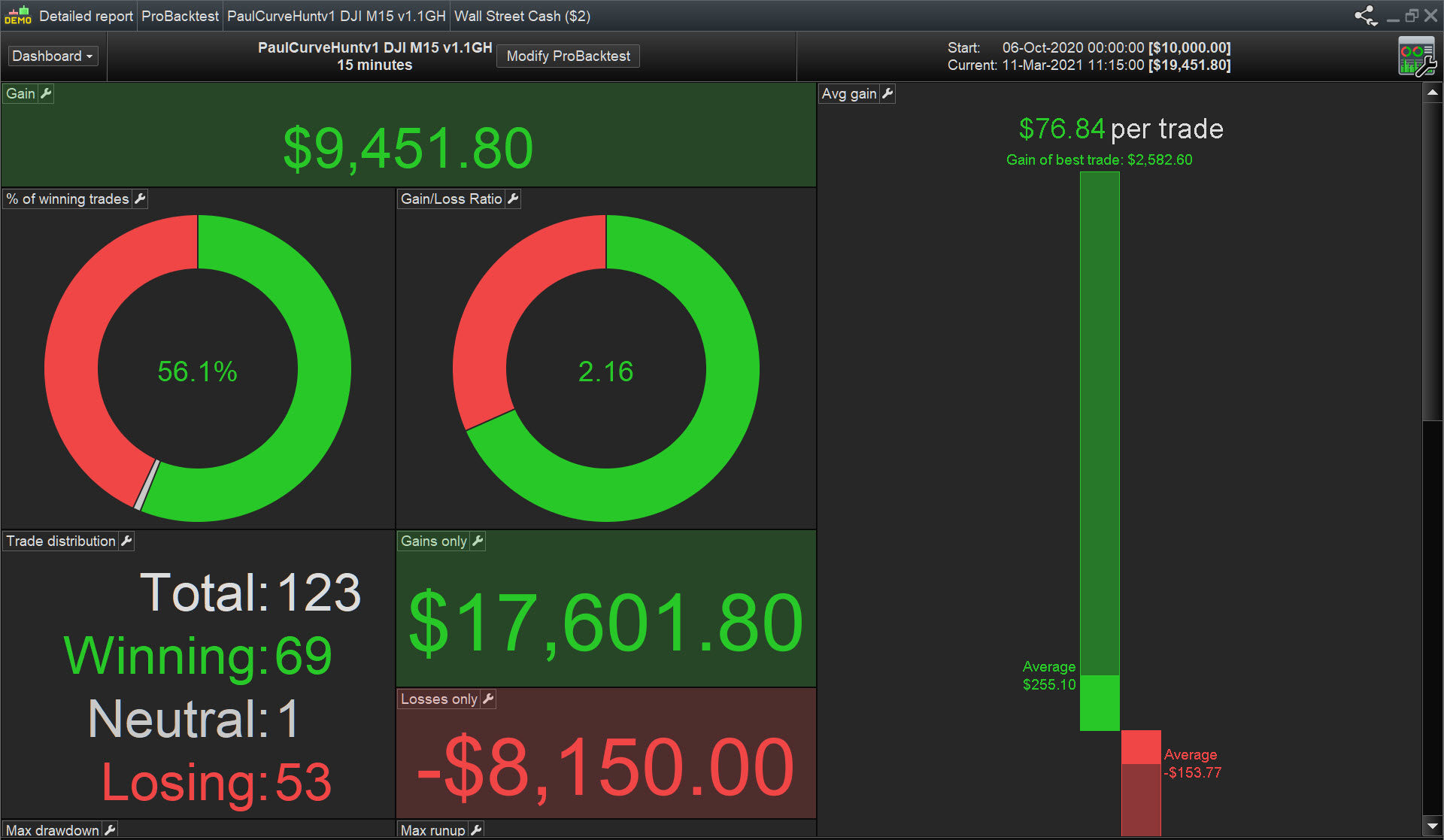

@Paul, do you trust these to let them take orders in real? Only in Demo for now? The drawdown looks a bit high isnt it?

Otherwise incredible job 😀

Paul

PaulParticipant

Master

Thnx. Just occasionally I check the how it would’ve performed OOS. I don’t have it in demo or live.

PaulParticipant

Master

here is a modified code & idea from Vonasi, instead of seasonal pattens it hunts for intraday patterns. Which in essence is a bit like barhunter, but now better written and changed to fit the purpose.

Timeframe 15m to 4 hours. There are maybe combinations possible. I post the code so it can be explored.

This code is setup for forex eurusd mini, 1hour tf and optimised on 30k bars without sl/pt/ts or spread.

note stepsize is depended on the market it is applied too.

here is a modified code & idea from Vonasi, instead of seasonal pattens it hunts for intraday patterns

The seasonality bit I’ll take credit for but the intraday patterns is all your own doing. Happy curve hunting!

Thank You Paul for yet another intriguing Strategy!

I’m putting attached on Demo Forward Test.

Spread = 5

@Paul @mods

Hi there,

I keep getting kicked out by IG in LIVE with this strategy without understanding why. Apparently many people have had the same experience;

I tried to increase the SL and the Trailing vs the original figure but it doesn’t work;

Here under the code modified.

once minstop = 15 // minimum trailing stop distance

…

set stop %loss 3

Anybody has manage to launched it live ?

thanks for your help,

Chris

//-------------------------------------------------------------------------

// Code principal : DAX H1 Timehunter v4.5p

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

// hoofd code : Timehunter v4.5p 1h dax

//-------------------------------------------------------------------------

// dax 1 hour timeframe backtest / dax 1 minute live

// spread 4

// optimise entryhour 0 to 23

// optimise entryminute 0 to 59 but set to 0 using 1 hour or higher timeframe

// on timeframe 5 minutes with entryminute interval of 5

// on timeframe 10 minutes with entryminute interval of 10

// on timeframe 15 minutes with entryminute interval of 15

// on timeframe 30 minutes with entryminute interval of 30

defparam cumulateorders = false

defparam preloadbars = 1000

timeframe (default)

once positionsize = 1

once mode = 1 // use [1] for 1 hour timeframe, [0] for 1 minute timeframe

once tds = 3 // off when optimising [trend detection system]

// separate long/short or go both

once longtrading =1

once shorttrading =1

once holiday =1

once closefriday =1

once displaydim =1 // displays the number of days in market (activated graph)

once maxdim =5 // maximum days in market (first day = 0)

// select the number of points above/below the breakvaluelong/short

once entryhour =4

once entryminute=0

// select the number of points above/below the breakvaluelong/short

once breakpointpercentage=4

// breakpoint calculation

breakpoint = ((close/10000)*breakpointpercentage)*pointsize

// reset low timeframe

if intradaybarindex=0 then

tradecounter=0

tradeday=1

endif

// holiday

if holiday then

if (month = 5 and day = 1) or (month = 12 and day >=24) then

tradeday=0

else

tradeday=1

endif

endif

timeframe (1 hour, updateonclose)

// reset high timeframe

if intradaybarindex=0 then

breakvaluelong=99999

breakvalueshort=0

endif

// define break value

if (longtrading and not shorttrading) or (longtrading and shorttrading) then

if hour=entryhour and (minute>=entryminute) then

startbarlong=intradaybarindex

breakvaluelong=high

endif

endif

if (shorttrading and not longtrading) or (longtrading and shorttrading) then

if hour=entryhour and (minute>=entryminute) then

startbarshort=intradaybarindex

breakvalueshort=low

endif

endif

// trend detection system

if tds=0 then

trendup=1

trenddown=1

else

if tds=1 then

trendup=(average[10](close)>average[10](close)[1])

trenddown=(average[10](close)<average[10](close)[1])

else

if tds=2 then

period= 2

inner = 2*weightedaverage[round( period/2)](typicalprice)-weightedaverage[period](typicalprice)

hull = weightedaverage[round(sqrt(period))](inner)

trendup = hull > hull[1]

trenddown = hull < hull[1]

else

if tds=3 then

period= 2

inner = 2*weightedaverage[round( period/2)](totalprice)-weightedaverage[period](totalprice)

hull = weightedaverage[round(sqrt(period))](inner)

trendup = hull > hull[1]

trenddown = hull < hull[1]

endif

endif

endif

endif

// point pivot [fifi743]

if dayofweek < dayofweek[1] then

weeklyhigh = prevweekhigh

weeklylow = prevweeklow

weeklyclose = prevweekclose

prevweekhigh = high

prevweeklow = low

weeklypivot = (weeklyhigh + weeklylow + weeklyclose) / 3

endif

prevweekhigh = max(prevweekhigh, high)

prevweeklow = min(prevweeklow, low)

prevweekclose = close

if dayofweek = 1 then

dayhigh = dhigh(2)

daylow = dlow(2)

dayclose = dclose(2)

endif

if dayofweek >=2 and dayofweek < 6 then

dayhigh = dhigh(1)

daylow = dlow(1)

dayclose = dclose(1)

endif

pivot = (dayhigh + daylow + dayclose) / 3

ecart=2

ecartwp=3

// conditions

condbuy=intradaybarindex=startbarlong

condbuy=condbuy and trendup

condbuy=condbuy and (close>pivot or (close <pivot and (pivot-close)/pointsize >ecart))

condbuy=condbuy and (close>weeklypivot or (close <weeklypivot and (weeklypivot-close)/pointsize >ecartwp))

condsell=intradaybarindex=startbarshort

condsell=condsell and trenddown

condsell=condsell and (close<pivot or (close>pivot and (close-pivot)/pointsize >ecart))

condsell=condsell and (close<weeklypivot or (close>weeklypivot and (close-weeklypivot)/pointsize >ecartwp))

timeframe (default)

// entry

if mode then // mode[1] backtesting on 1 hour timeframe

if tradeday and tradecounter < 1 then

if (longtrading and not shorttrading) or (longtrading and shorttrading) then

if condbuy then

buy positionsize contract at (breakvaluelong+breakpoint) stop

tradecounter=tradecounter+1

endif

endif

if (shorttrading and not longtrading) or (longtrading and shorttrading) then

if condsell then

sellshort positionsize contract at (breakvalueshort-breakpoint) stop

tradecounter=tradecounter+1

endif

endif

endif

else // mode[0] running demo / live on 1 minute timeframe

if tradeday and tradecounter < 1 then

if (longtrading and not shorttrading) or (longtrading and shorttrading) then

if condbuy then

if high > breakvaluelong+breakpoint then

buy positionsize contract at market

tradecounter=tradecounter+1

endif

endif

endif

if (shorttrading and not longtrading) or (longtrading and shorttrading) then

if condsell then

if low < breakvalueshort-breakpoint then

sellshort positionsize contract at market

tradecounter=tradecounter+1

endif

endif

endif

endif

endif

timeframe (1 hour, updateonclose)

// trailing atr stop on high timeframe

once trailingstoptype = 1 // trailing stop - 0 off, 1 on

once trailingstoplong = 5 // trailing stop atr relative distance

once trailingstopshort = 5 // trailing stop atr relative distance

once atrtrailingperiod = 14 // atr parameter value

once minstop = 15 // minimum trailing stop distance

//----------------------------------------------

atrtrail = averagetruerange[atrtrailingperiod]((close/10)*pipsize)/1000

trailingstartl = round(atrtrail*trailingstoplong)

trailingstarts = round(atrtrail*trailingstopshort)

//

if trailingstoptype then

tgl =trailingstartl

tgs=trailingstarts

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

maxprice = 0

minprice = close

newsl = 0

endif

if longonmarket then

maxprice = max(maxprice,close)

if maxprice-tradeprice(1)>=tgl*pointsize then

if maxprice-tradeprice(1)>=minstop then

newsl = maxprice-tgl*pointsize

else

newsl = maxprice - minstop*pointsize

endif

endif

endif

if shortonmarket then

minprice = min(minprice,close)

if tradeprice(1)-minprice>=tgs*pointsize then

if tradeprice(1)-minprice>=minstop then

newsl = minprice+tgs*pointsize

else

newsl = minprice + minstop*pointsize

endif

endif

endif

endif

timeframe (default)

// trailing atr stop exits on low timeframe

if trailingstoptype then

if longonmarket then

if newsl>0 then

sell at newsl stop

endif

endif

if shortonmarket then

if newsl>0 then

exitshort at newsl stop

endif

endif

endif

// close to reduce risk in the weekend

if closefriday then

if onmarket then

if (dayofweek=5 and hour=22) then

sell at market

exitshort at market

endif

endif

endif

// stoploss & profit target

set target %profit 2

set stop %loss 3

// display days in market

if displaydim then

if (not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket))) then

dim=0

endif

if not ( dayofweek=1 and hour <= 1) then

if onmarket then

if openday <> openday[1] then

dim = dim + 1

endif

endif

endif

if onmarket and dayofweek=1 and hour=1 then

//dim=-1 // shows when position is active on monday first hour

endif

if onmarket and dim>=maxdim then

sell at market

exitshort at market

endif

endif

//graph dim // display days in market

//graphonprice newsl coloured(0,0,255,255) as "trailingstop atr"

//graphonprice breakvaluelong+breakpoint coloured(121,141,35,255) as "breakpoint"

//graphonprice breakvalueshort-breakpoint coloured(121,141,35,255) as "breakpoint"

//graphonprice breakvaluelong coloured(255,0,0,255) as "breakvaluelong"

//graphonprice breakvalueshort coloured(255,0,0,255) as "breakvalueshort"

//graph barindex-tradeindex

//graph intradaybarindex

without understanding why

What Rejection message do you see? Check the Cancelled / Rejected tab on the Orders List?

hi @Grahal,

It says “the level of order is to close from the market level. The minimum is 10 points”;

I thought it was the SL; but apparently not.

I am on IG Live.

Did you launch it live?

@Meta Signals Pro

It’s a pending stop order that’s too close ?

the level of order is to close from the market level. The minimum is 10 points”;

So does it run in Live for a while (over several bars) but then gets Rejected when it tries to exeute an Order / Trade?

If Yes, then it’s, as fifi says, a pending Buy or SellShort Order as below …

buy positionsize contract at (breakvaluelong+breakpoint) stop

sellshort positionsize contract at (breakvalueshort-breakpoint) stop

The breakpoint must be greater than 10 points

replace with the code below

minidistance=10

buy positionsize contract at (breakvaluelong+max(breakpoint,minidistance)) stop

sellshort positionsize contract at (breakvalueshort-max(breakpoint,minidistance)) stop

You can also, when starting a prepared instance of the system, choose to check the “Re-adjustable stops” checkbox which will allow ProRealTime to adjust the stoploss level based on the current minimum stop distance.

Above only works if the coded pending order is > 10 so best bet is fifi code + enable the adjustabe stop box.

Thanks Guys ^^

Here is the modified code for the followers!

//-------------------------------------------------------------------------

// hoofd code : Timehunter v4.5p 1h dax

//-------------------------------------------------------------------------

// dax 1 hour timeframe backtest / dax 1 minute live

// spread 4

// optimise entryhour 0 to 23

// optimise entryminute 0 to 59 but set to 0 using 1 hour or higher timeframe

// on timeframe 5 minutes with entryminute interval of 5

// on timeframe 10 minutes with entryminute interval of 10

// on timeframe 15 minutes with entryminute interval of 15

// on timeframe 30 minutes with entryminute interval of 30

defparam cumulateorders = false

defparam preloadbars = 1000

timeframe (default)

once positionsize = 1

once mode = 1 // use [1] for 1 hour timeframe, [0] for 1 minute timeframe

once tds = 3 // off when optimising [trend detection system]

// separate long/short or go both

once longtrading =1

once shorttrading =1

once holiday =1

once closefriday =1

once displaydim =1 // displays the number of days in market (activated graph)

once maxdim =5 // maximum days in market (first day = 0)

// select the number of points above/below the breakvaluelong/short

once entryhour =4

once entryminute=0

// select the number of points above/below the breakvaluelong/short

once breakpointpercentage=4

// breakpoint calculation

breakpoint = ((close/10000)*breakpointpercentage)*pointsize

// reset low timeframe

if intradaybarindex=0 then

tradecounter=0

tradeday=1

endif

// holiday

if holiday then

if (month = 5 and day = 1) or (month = 12 and day >=24) then

tradeday=0

else

tradeday=1

endif

endif

timeframe (1 hour, updateonclose)

// reset high timeframe

if intradaybarindex=0 then

breakvaluelong=99999

breakvalueshort=0

endif

// define break value

if (longtrading and not shorttrading) or (longtrading and shorttrading) then

if hour=entryhour and (minute>=entryminute) then

startbarlong=intradaybarindex

breakvaluelong=high

endif

endif

if (shorttrading and not longtrading) or (longtrading and shorttrading) then

if hour=entryhour and (minute>=entryminute) then

startbarshort=intradaybarindex

breakvalueshort=low

endif

endif

// trend detection system

if tds=0 then

trendup=1

trenddown=1

else

if tds=1 then

trendup=(average[10](close)>average[10](close)[1])

trenddown=(average[10](close)<average[10](close)[1])

else

if tds=2 then

period= 2

inner = 2*weightedaverage[round( period/2)](typicalprice)-weightedaverage[period](typicalprice)

hull = weightedaverage[round(sqrt(period))](inner)

trendup = hull > hull[1]

trenddown = hull < hull[1]

else

if tds=3 then

period= 2

inner = 2*weightedaverage[round( period/2)](totalprice)-weightedaverage[period](totalprice)

hull = weightedaverage[round(sqrt(period))](inner)

trendup = hull > hull[1]

trenddown = hull < hull[1]

endif

endif

endif

endif

// point pivot [fifi743]

if dayofweek < dayofweek[1] then

weeklyhigh = prevweekhigh

weeklylow = prevweeklow

weeklyclose = prevweekclose

prevweekhigh = high

prevweeklow = low

weeklypivot = (weeklyhigh + weeklylow + weeklyclose) / 3

endif

prevweekhigh = max(prevweekhigh, high)

prevweeklow = min(prevweeklow, low)

prevweekclose = close

if dayofweek = 1 then

dayhigh = dhigh(2)

daylow = dlow(2)

dayclose = dclose(2)

endif

if dayofweek >=2 and dayofweek < 6 then

dayhigh = dhigh(1)

daylow = dlow(1)

dayclose = dclose(1)

endif

pivot = (dayhigh + daylow + dayclose) / 3

ecart=2

ecartwp=3

// conditions

condbuy=intradaybarindex=startbarlong

condbuy=condbuy and trendup

condbuy=condbuy and (close>pivot or (close <pivot and (pivot-close)/pointsize >ecart))

condbuy=condbuy and (close>weeklypivot or (close <weeklypivot and (weeklypivot-close)/pointsize >ecartwp))

condsell=intradaybarindex=startbarshort

condsell=condsell and trenddown

condsell=condsell and (close<pivot or (close>pivot and (close-pivot)/pointsize >ecart))

condsell=condsell and (close<weeklypivot or (close>weeklypivot and (close-weeklypivot)/pointsize >ecartwp))

timeframe (default)

minidistance=10

// entry

if mode then // mode[1] backtesting on 1 hour timeframe

if tradeday and tradecounter < 1 then

if (longtrading and not shorttrading) or (longtrading and shorttrading) then

if condbuy then

buy positionsize contract at (breakvaluelong+max(breakpoint,minidistance)) stop

tradecounter=tradecounter+1

endif

endif

if (shorttrading and not longtrading) or (longtrading and shorttrading) then

if condsell then

sellshort positionsize contract at (breakvalueshort-max(breakpoint,minidistance)) stop

tradecounter=tradecounter+1

endif

endif

endif

else // mode[0] running demo / live on 1 minute timeframe

if tradeday and tradecounter < 1 then

if (longtrading and not shorttrading) or (longtrading and shorttrading) then

if condbuy then

if high > breakvaluelong+breakpoint then

buy positionsize contract at market

tradecounter=tradecounter+1

endif

endif

endif

if (shorttrading and not longtrading) or (longtrading and shorttrading) then

if condsell then

if low < breakvalueshort-breakpoint then

sellshort positionsize contract at market

tradecounter=tradecounter+1

endif

endif

endif

endif

endif

timeframe (1 hour, updateonclose)

// trailing atr stop on high timeframe

once trailingstoptype = 1 // trailing stop - 0 off, 1 on

once trailingstoplong = 5 // trailing stop atr relative distance

once trailingstopshort = 5 // trailing stop atr relative distance

once atrtrailingperiod = 14 // atr parameter value

once minstop = 15 // minimum trailing stop distance

//----------------------------------------------

atrtrail = averagetruerange[atrtrailingperiod]((close/10)*pipsize)/1000

trailingstartl = round(atrtrail*trailingstoplong)

trailingstarts = round(atrtrail*trailingstopshort)

//

if trailingstoptype then

tgl =trailingstartl

tgs=trailingstarts

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

maxprice = 0

minprice = close

newsl = 0

endif

if longonmarket then

maxprice = max(maxprice,close)

if maxprice-tradeprice(1)>=tgl*pointsize then

if maxprice-tradeprice(1)>=minstop then

newsl = maxprice-tgl*pointsize

else

newsl = maxprice - minstop*pointsize

endif

endif

endif

if shortonmarket then

minprice = min(minprice,close)

if tradeprice(1)-minprice>=tgs*pointsize then

if tradeprice(1)-minprice>=minstop then

newsl = minprice+tgs*pointsize

else

newsl = minprice + minstop*pointsize

endif

endif

endif

endif

timeframe (default)

// trailing atr stop exits on low timeframe

if trailingstoptype then

if longonmarket then

if newsl>0 then

sell at newsl stop

endif

endif

if shortonmarket then

if newsl>0 then

exitshort at newsl stop

endif

endif

endif

// close to reduce risk in the weekend

if closefriday then

if onmarket then

if (dayofweek=5 and hour=22) then

sell at market

exitshort at market

endif

endif

endif

// stoploss & profit target

set target %profit 2

set stop %loss 3

// display days in market

if displaydim then

if (not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket))) then

dim=0

endif

if not ( dayofweek=1 and hour <= 1) then

if onmarket then

if openday <> openday[1] then

dim = dim + 1

endif

endif

endif

if onmarket and dayofweek=1 and hour=1 then

//dim=-1 // shows when position is active on monday first hour

endif

if onmarket and dim>=maxdim then

sell at market

exitshort at market

endif

endif

//graph dim // display days in market

//graphonprice newsl coloured(0,0,255,255) as "trailingstop atr"

//graphonprice breakvaluelong+breakpoint coloured(121,141,35,255) as "breakpoint"

//graphonprice breakvalueshort-breakpoint coloured(121,141,35,255) as "breakpoint"

//graphonprice breakvaluelong coloured(255,0,0,255) as "breakvaluelong"

//graphonprice breakvalueshort coloured(255,0,0,255) as "breakvalueshort"

//graph barindex-tradeindex

//graph intradaybarindex