Bonjour à tous,

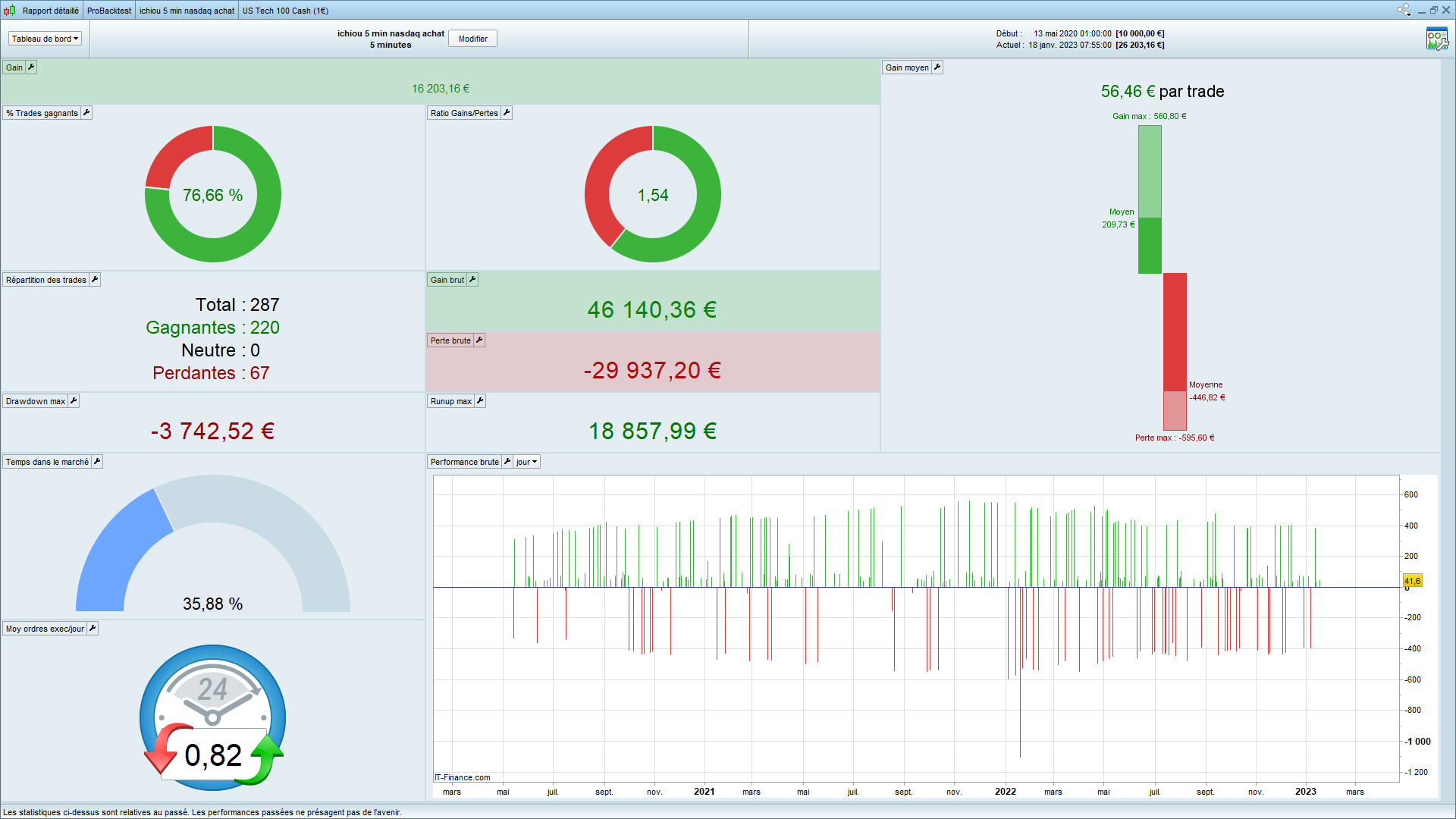

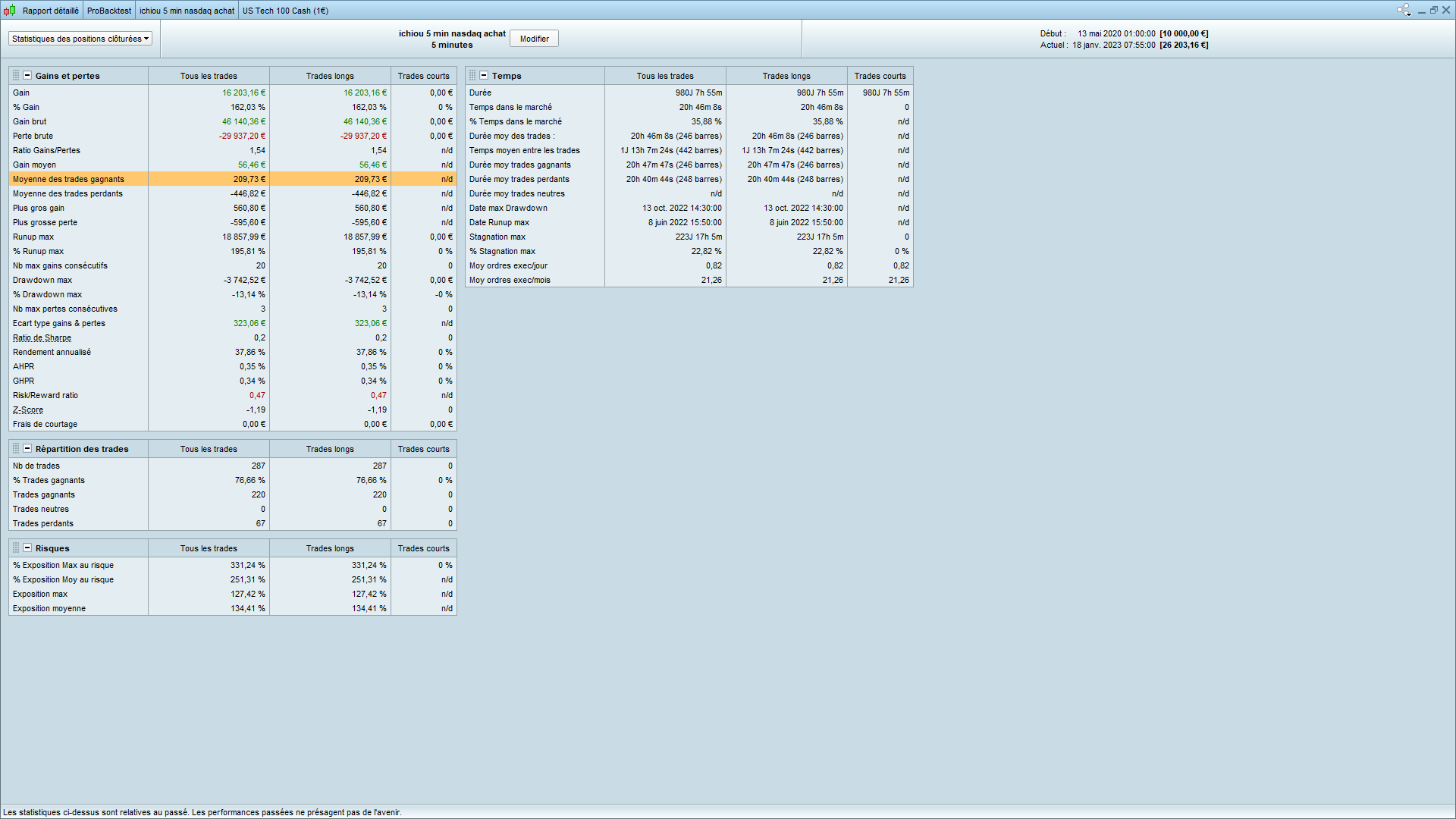

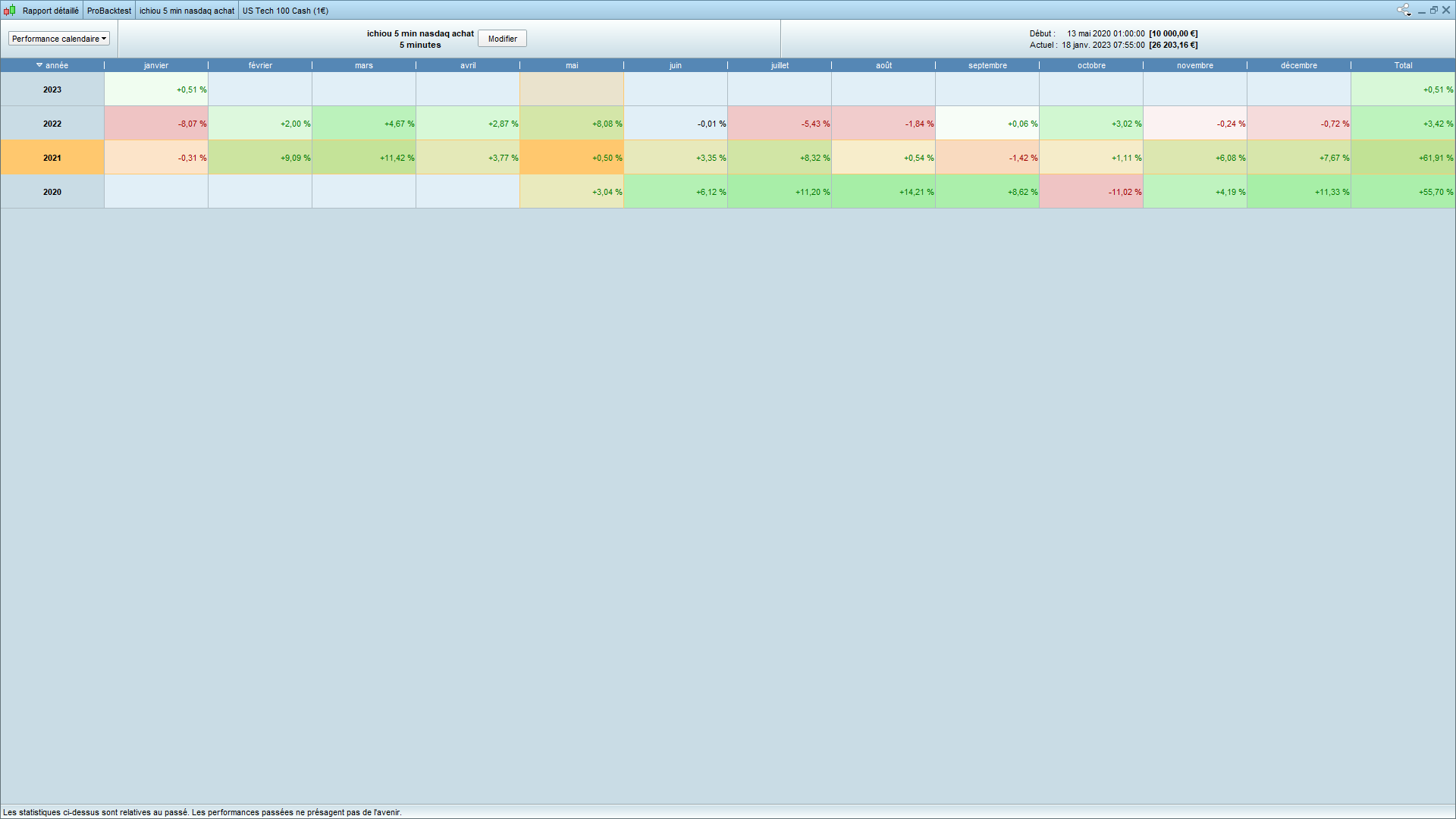

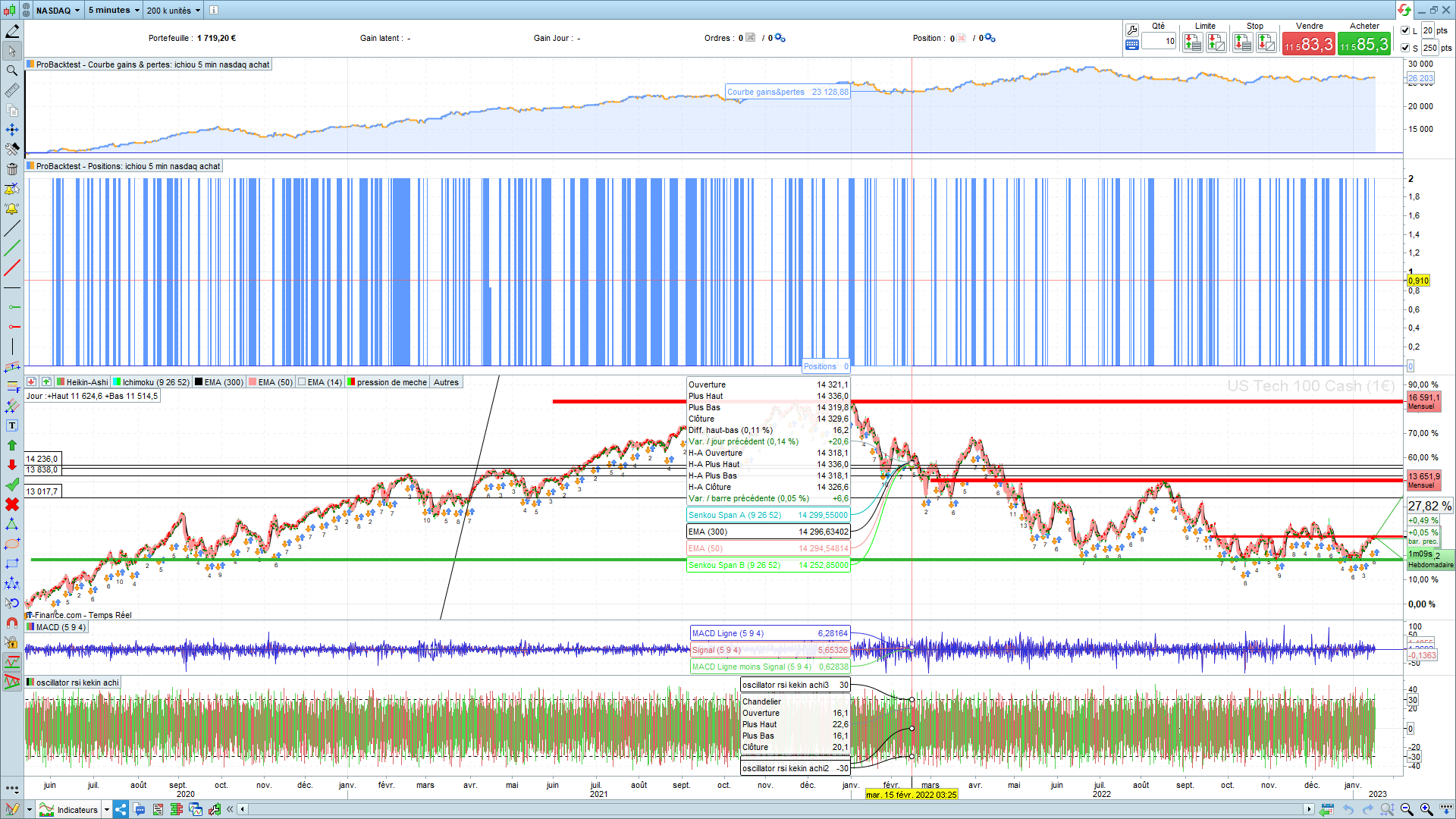

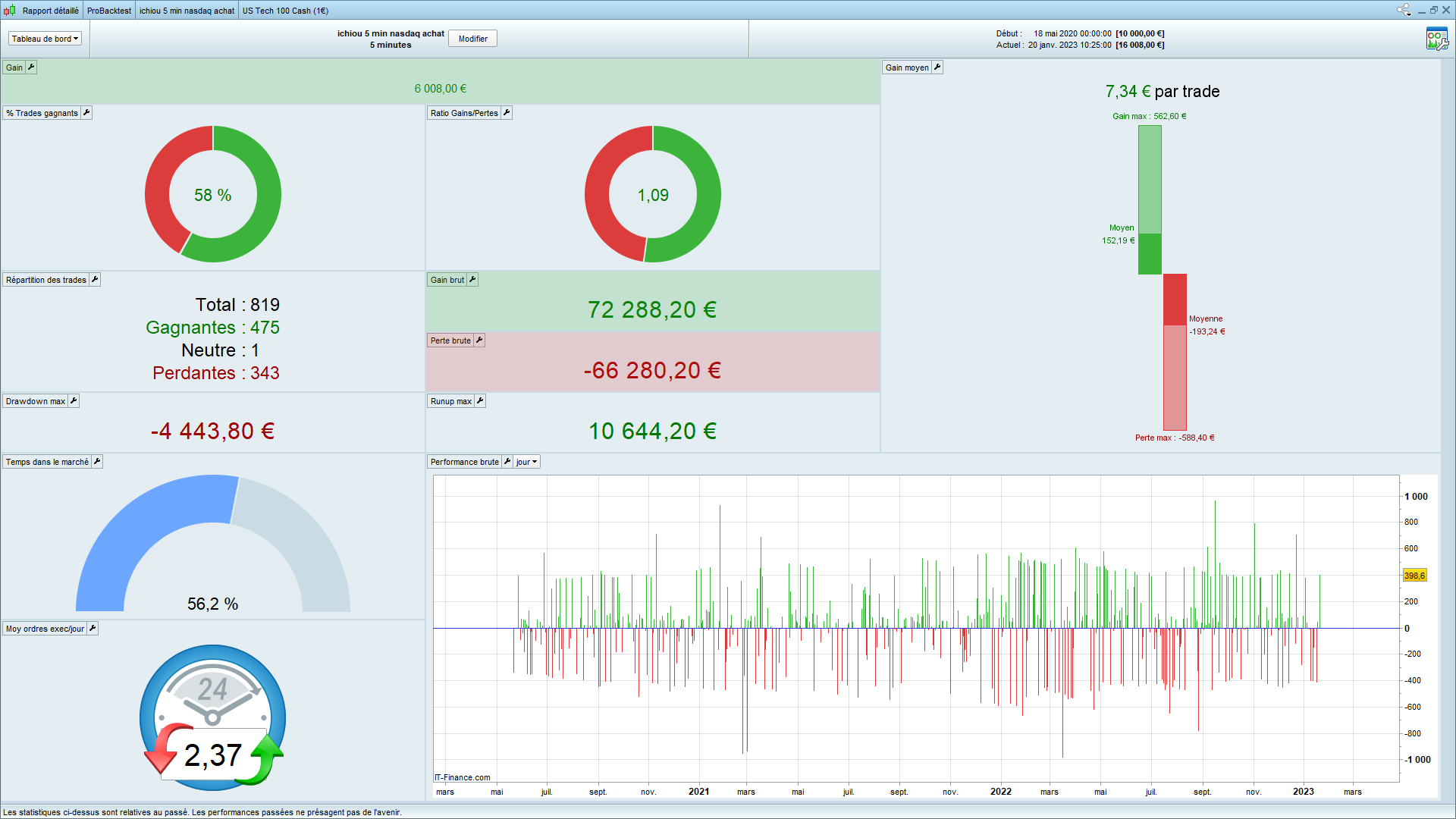

je vous remonte et partage un stratégie sur le nadasq en 5min avec spread à 1 pour capital de 10000 avec 2 contrats, je pense qu’on peut encore améliorer les gains et diminuer les pertes.

Je m’aperçois que je n’ai que des trades longs je ne comprends pas pourquoi les courts ne fonctionne pas.

merci au passage à nicolas et robertto .

// Définition des paramètres du code

DEFPARAM CumulateOrders = false // pas de cumul de positions

DEFPARAM Preloadbars = 1000000

capital= 50000

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position avant l'heure spécifiée

noEntryBeforeTime = 150000

timeEnterBefore = time >= noEntryBeforeTime

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position après l'heure spécifiée

noEntryAfterTime = 223000

timeEnterAfter = time < noEntryAfterTime

// Empêche le système de placer de nouveaux ordres sur les jours de la semaine spécifiés

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

// Conditions pour ouvrir une position acheteuse

indicator1 = SenkouSpanA[9,26,52]

c1 = (close CROSSES OVER indicator1)

indicator2 = SenkouSpanB[9,26,52]

c2 = (close CROSSES OVER indicator2)

c3 = (close > DOpen(0)[1])

IF (c1 AND c2 ) AND timeEnterBefore AND timeEnterAfter AND not daysForbiddenEntry THEN

BUY 2 CONTRACT AT MARKET

partial=0

ENDIF

// sortie partielle

if longonmarket and positionperf>1.71/100 and partial=0 then

sell countofposition/1.7 contract at market

partial = 1

endif

if summation[1680](longonmarket)=1680 then

sell at market

endif

if summation[1000](shortonmarket)=1000 then

exitshort at market

endif

// Stops et objectifs

set stop %loss 1.8

set target %profit 1.73

IF Not OnMarket THEN

//

// when NOT OnMarket reset values to default values

//

TrailStart = 65 //30 Start trailing profits from this point

BasePerCent = 0.000 //20.0% Profit percentage to keep when setting BerakEven

StepSize = 1 //10 Pip chunks to increase Percentage

PerCentInc = 0.000 //10.0% PerCent increment after each StepSize chunk

BarNumber = 10 //10 Add further % so that trades don't keep running too long

BarPerCent = 0.235 //10% Add this additional percentage every BarNumber bars

RoundTO = -0.5 //-0.5 rounds always to Lower integer, +0.4 rounds always to Higher integer, 0 defaults PRT behaviour

PriceDistance = 9 * pipsize //7 minimun distance from current price

y1 = 0 //reset to 0

y2 = 0 //reset to 0

ProfitPerCent = BasePerCent //reset to desired default value

TradeBar = BarIndex

ELSIF LongOnMarket AND close > (TradePrice + (y1 * pipsize)) THEN //LONG positions

//

// compute the value of the Percentage of profits, if any, to lock in for LONG trades

//

x1 = (close - tradeprice) / pipsize //convert price to pips

IF x1 >= TrailStart THEN // go ahead only if N+ pips

Diff1 = abs(TrailStart - x1) //difference from current profit and TrailStart

Chunks1 = max(0,round((Diff1 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks1 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y1 = max(x1 * ProfitPerCent, y1) //y1 = % of max profit

ENDIF

ELSIF ShortOnMarket AND close < (TradePrice - (y2 * pipsize)) THEN //SHORT positions

//

// compute the value of the Percentage of profits, if any, to lock in for SHORT trades

//

x2 = (tradeprice - close) / pipsize //convert price to pips

IF x2 >= TrailStart THEN // go ahead only if N+ pips

Diff2 = abs(TrailStart - x2) //difference from current profit and TrailStart

Chunks2 = max(0,round((Diff2 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks2 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y2 = max(x2 * ProfitPerCent, y2) //y2 = % of max profit

ENDIF

ENDIF

IF y1 THEN //Place pending STOP order when y1 > 0 (LONG positions)

SellPrice = Tradeprice + (y1 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - SellPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close >= SellPrice THEN

SELL AT SellPrice STOP

ELSE

SELL AT SellPrice LIMIT

ENDIF

ELSE

//

//sell AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

SELL AT Market

ENDIF

ENDIF

IF y2 THEN //Place pending STOP order when y2 > 0 (SHORT positions)

ExitPrice = Tradeprice - (y2 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - ExitPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close <= ExitPrice THEN

EXITSHORT AT ExitPrice STOP

ELSE

EXITSHORT AT ExitPrice LIMIT

ENDIF

ELSE

//

//ExitShort AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

EXITSHORT AT Market

ENDIF

Bjr,

Vite fait avant de démarrer la séance, à moins d’une erreur de copier-coller qui oublie un bout de code, ou que je fasse l’erreur fatale de mal lire le code avant mon café, je ne vois pas d’entrée sellshort dans ce code, juste des achats longs, des sorties partielles ou totales, et des exitshort sans entrée sellshort préalable…

SELLSHORT

bonjour jc bryan ,

j’ai fait ce code juste pour des achats et mes sorties sont faites par le break even ou sur une duree de bougies,

Novice encore pour la programmation pourrais tu me dire comment tu mettrais ton sell short

Tu es déjà moins novice que ce que tu penses, ou tu as oublié avoir déjà utilisé cette instruction sellshort, voici ton post #197547 qui ressemble beaucoup au code ci-dessus, dans lequel tu avais déjà utilisé sellshort à la ligne22 avec les conditions c1 et c2 en “cross under” cette fois-là (par rapport au cross over pour la version buy actuelle)

Merci Nicolas pour le partage. C’est très apprécié, et ça signifie que le partage et la collaboration fonctionne toujours dans notre communauté 😉

bonjour JC_Bywan,

J’ai essayé le sellshort peux tu me dire si tu l’aurais positionné avec les conditions C1 et C2 ou si tu l’aurais utliser avec d’autres conditons.

Le résultat est moins bon si j’ai bien compris intégré le sellshort

// Définition des paramètres du code

DEFPARAM CumulateOrders = false // pas de cumul de positions

DEFPARAM Preloadbars = 1000000

capital= 50000

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position avant l'heure spécifiée

noEntryBeforeTime = 150000

timeEnterBefore = time >= noEntryBeforeTime

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position après l'heure spécifiée

noEntryAfterTime = 223000

timeEnterAfter = time < noEntryAfterTime

// Empêche le système de placer de nouveaux ordres sur les jours de la semaine spécifiés

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

// Conditions pour ouvrir une position acheteuse

indicator1 = SenkouSpanA[9,26,52]

c1 = (close CROSSES OVER indicator1)

indicator2 = SenkouSpanB[9,26,52]

c2 = (close CROSSES OVER indicator2)

c3 = (close > DOpen(0)[1])

IF (c1 AND c2 ) AND timeEnterBefore AND timeEnterAfter AND not daysForbiddenEntry THEN

BUY 2 CONTRACT AT MARKET

partial=0

ENDIF

IF NOT ShortOnMarket AND c1 and c2 THEN

SELLSHORT 2 SHARES AT MARKET

ENDIF

// Condition pour ouvrir une position vendeuse

// sortie partielle

if longonmarket and positionperf>1.71/100 and partial=0 then

sell countofposition/1.7 contract at market

partial = 1

endif

if summation[1680](longonmarket)=1680 then

sell at market

endif

if summation[1000](shortonmarket)=1000 then

exitshort at market

endif

// Stops et objectifs

set stop %loss 1.8

set target %profit 1.73

IF Not OnMarket THEN

//

// when NOT OnMarket reset values to default values

//

TrailStart = 65 //30 Start trailing profits from this point

BasePerCent = 0.000 //20.0% Profit percentage to keep when setting BerakEven

StepSize = 1 //10 Pip chunks to increase Percentage

PerCentInc = 0.000 //10.0% PerCent increment after each StepSize chunk

BarNumber = 10 //10 Add further % so that trades don't keep running too long

BarPerCent = 0.235 //10% Add this additional percentage every BarNumber bars

RoundTO = -0.5 //-0.5 rounds always to Lower integer, +0.4 rounds always to Higher integer, 0 defaults PRT behaviour

PriceDistance = 9 * pipsize //7 minimun distance from current price

y1 = 0 //reset to 0

y2 = 0 //reset to 0

ProfitPerCent = BasePerCent //reset to desired default value

TradeBar = BarIndex

ELSIF LongOnMarket AND close > (TradePrice + (y1 * pipsize)) THEN //LONG positions

//

// compute the value of the Percentage of profits, if any, to lock in for LONG trades

//

x1 = (close - tradeprice) / pipsize //convert price to pips

IF x1 >= TrailStart THEN // go ahead only if N+ pips

Diff1 = abs(TrailStart - x1) //difference from current profit and TrailStart

Chunks1 = max(0,round((Diff1 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks1 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y1 = max(x1 * ProfitPerCent, y1) //y1 = % of max profit

ENDIF

ELSIF ShortOnMarket AND close < (TradePrice - (y2 * pipsize)) THEN //SHORT positions

//

// compute the value of the Percentage of profits, if any, to lock in for SHORT trades

//

x2 = (tradeprice - close) / pipsize //convert price to pips

IF x2 >= TrailStart THEN // go ahead only if N+ pips

Diff2 = abs(TrailStart - x2) //difference from current profit and TrailStart

Chunks2 = max(0,round((Diff2 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks2 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y2 = max(x2 * ProfitPerCent, y2) //y2 = % of max profit

ENDIF

ENDIF

IF y1 THEN //Place pending STOP order when y1 > 0 (LONG positions)

SellPrice = Tradeprice + (y1 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - SellPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close >= SellPrice THEN

SELL AT SellPrice STOP

ELSE

SELL AT SellPrice LIMIT

ENDIF

ELSE

//

//sell AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

SELL AT Market

ENDIF

ENDIF

IF y2 THEN //Place pending STOP order when y2 > 0 (SHORT positions)

ExitPrice = Tradeprice - (y2 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - ExitPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close <= ExitPrice THEN

EXITSHORT AT ExitPrice STOP

ELSE

EXITSHORT AT ExitPrice LIMIT

ENDIF

ELSE

//

//ExitShort AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

EXITSHORT AT Market

ENDIF

ENDIF

Je reviens vers toi, concernant mon partage avec l’algo eur/usd 3 minutes.

Je voudrais créer un autre algo en prenant en compte mon algo eur/usd 3minutes , c’est a dire quand mon Trade est lancé je m’aperçois quand il part dans le négatif je voudrais pouvoir paramétrer le fibonnacci afin par exemple quand il retrace vers le dernier plus haut du timeframe 1h ou 4 h ou 15 minutes pouvoir lancé un autre algo qui lui dit retracement des 50% de fibo pas rapport au retracement du time frame 1heure ou 4 heures tu te met à la vente et je voudrais paramétrer le take profit sur le niveau d’ouverture ou même le paramétrer sur le take profit de mon algo 3 minutes et mon stop loss toujours paramétrer sur 0.58%.

Je parle de ca parce que je me suis entrainer en démo quand mon reel prenait le trade j’ai surveillé quand il partait dans le sens contraire j’attendais une bougie de retournement comme un pendu ou harami sur des times frame de différents ou un overblock en time frame 15 minutes et je validé mes trades . Donc je me demande si je ne pourrais pas le paramétrer mais la je ne sais pas faire la technique est plus complexe.

Je sais pas si j’ai été clair pour vous?

Oderblock pardon faute de frappe