Expert Services

No recent search

Stratégie multi indices en 10′ (secondes)

- Forums

- Forum ProRealTime Français

- ProOrder : Trading Automatique & Backtests

- Stratégie multi indices en 10′ (secondes)

-

AuthorPosts

-

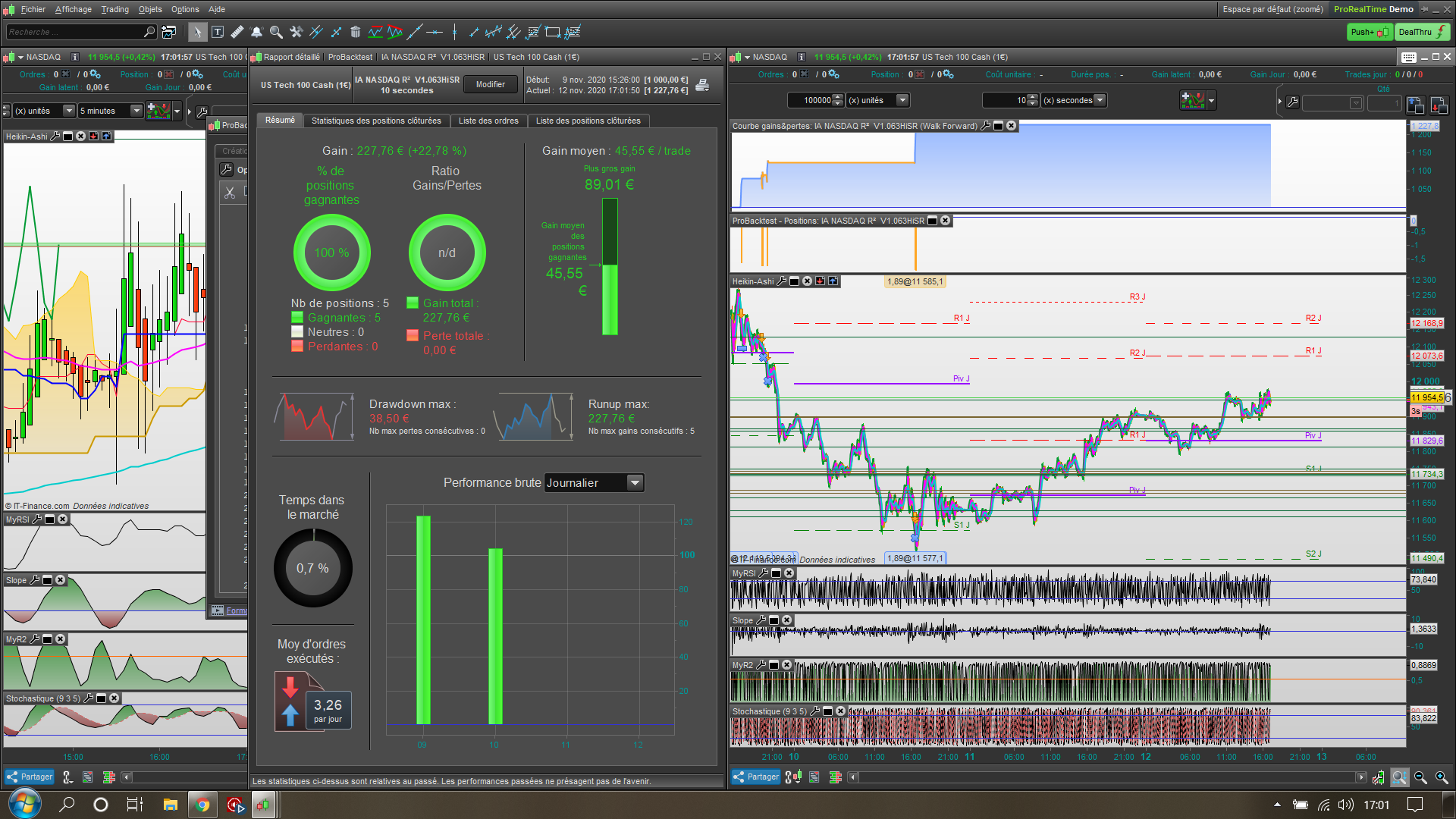

Bonjour la communauté,

je partage aujourd’hui une stratégie qui me donne de bon résultats avec un manque de constance d’une semaine à l’autre.

j’atteint mes limite en programmation…mais je suis convaincu que la base est est bonne et mérite d’être partagée et améliorée.

merci de faire part de vos commentaires, amélioration, correction, …

fonctionne sur plusieurs indices en travaillant sur les variables startingvalue(P,1,2,3,4…)

//------------------------------------------------------------------------- // Définition des paramètres du code Defparam CumulateOrders = False Defparam Preloadbars = 10000 Defparam FlatBefore = 153000 Defparam FlatAfter = 213000 daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0 //daysForbiddenEntry = OpenDayOfWeek = 1 OR OpenDayOfWeek = 6 OR OpenDayOfWeek = 0 //************************************************************************ // Heuristics Algorithm P Start If (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) Then optimizeP = optimizeP + 1 EnDif StartingValueP = 10 ResetPeriodP = 5 //Specify no of days after which to reset optimization IncrementP = 1 MaxIncrementP = 3 //Limit of no of IncrementPs either up or down RepsP = 3 //Number of trades to use for analysis MaxValueP = 12 //Maximum allowed value MinValueP = 9 //Minimum allowed value once DayinitP = day once MonthinitP = month If (month = MonthinitP and day = (DayinitP + ResetPeriodP)) or (month = (MonthinitP + 1) and ((month - DayinitP) + day = ResetPeriodP)) Then R2LimE = StartingValueP WinCountBP = 0 StratAvgBP = 0 BestAP = 0 BestBP = 0 DayinitP = day MonthinitP = month EndIf once P = StartingValueP once PincPosP = 1 //Positive IncrementP Position once NincPosP = 1 //Neative IncrementP Position once optimizeP = 0 ////Initialize Heuristicks Engine Counter (Must be IncrementPed at Position Start or Exit) once ModeP = 1 //Switches between negative and positive IncrementPs //once WinCountBP = P //Initialize Best Win Count //GRAPH WinCountBP coloured (0,0,0) AS "WinCountBP" //once StratAvgBP = PP5P //Initialize Best Avg Strategy Profit //GRAPH StratAvgBP coloured (0,0,0) AS "StratAvgBP" If optimizeP = RepsP Then WinCountAP = 0 //Initialize current Win Count StratAvgAP = 0 //Initialize current Avg Strategy Profit For iP = 1 to RepsP Do If positionperf(iP) > 0 Then WinCountAP = WinCountAP + 1 //IncrementP Current WinCount EndIf StratAvgAP = StratAvgAP + (((PositionPerf(iP)*countofposition[iP]*close)*-1)*-1) Next StratAvgAP = StratAvgAP/RepsP //Calculate Current Avg Strategy Profit //Graph (PositionPerf(1)*countofposition[1]*close)*-1 as "PosPerf1" //Graph (PositionPerf(2)*countofposition[2]*close)*-1 as "PosPerf2" //Graph StratAvgAP*-1 as "StratAvgAP" //once BestAP = P00 //GRAPH BestAP coloured (0,0,0) AS "BestAP" If StratAvgAP >= StratAvgBP Then StratAvgBP = StratAvgAP //Update Best Strategy Profit BestAP = P EndIf //once BestBP = P00 //GRAPH BestBP coloured (0,0,0) AS "BestBP" If WinCountAP >= WinCountBP Then WinCountBP = WinCountAP //Update Best Win Count BestBP = P EndIf If WinCountAP > WinCountBP and StratAvgAP > StratAvgBP Then ModeP = 0 ElsIf WinCountAP < WinCountBP and StratAvgAP < StratAvgBP and ModeP = 1 Then P = P - (IncrementP*NincPosP) NincPosP = NincPosP + 1 ModeP = 2 ElsIf WinCountAP >= WinCountBP or StratAvgAP >= StratAvgBP and ModeP = 1 Then P = P + (IncrementP*PincPosP) PincPosP = PincPosP + 1 ModeP = 1 ElsIf WinCountAP < WinCountBP and StratAvgAP < StratAvgBP and ModeP = 2 Then P = P + (IncrementP*PincPosP) PincPosP = PincPosP + 1 ModeP = 1 ElsIf WinCountAP >= WinCountBP or StratAvgAP >= StratAvgBP and ModeP = 2 Then P = P - (IncrementP*NincPosP) NincPosP = NincPosP + 1 ModeP = 2 EndIf If NincPosP > MaxIncrementP or PincPosP > MaxIncrementP Then If BestAP = BestBP Then P = BestAP Else If RepsP >= 10 Then WeightedScoreP = 10 Else WeightedScoreP = round((RepsP/100)*100) EndIf P = round(((BestAP*(20-WeightedScoreP)) + (BestBP*WeightedScoreP))/20) //Lower RepsP = Less weight assigned to Win% EndIf NincPosP = 1 PincPosP = 1 ElsIf P > MaxValueP Then P = MaxValueP ElsIf P < MinValueP Then P = MinValueP EndIF optimizeP = 0 Endif // Heuristics Algorithm P End //************************************************************************ // Heuristics Algorithm 1 Start If (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) Then optimize = optimize + 1 EnDif StartingValue = 0.54 ResetPeriod = 5 //Specify no of hour after which to reset optimization Increment = 0.005 MaxIncrement = 40 //Limit of no of increments either up or down Reps = 3 //Number of trades to use for analysis MaxValue = 0.6 //Maximum allowed value MinValue = 0.4 //Minimum allowed value once Dayinit = day once Monthinit = month If (month = Monthinit and day = (Dayinit + ResetPeriod)) or (month = (Monthinit + 1) and ((month - Dayinit) + day = ResetPeriod)) Then R2LimE = StartingValue WinCountB = 0 StratAvgB = 0 BestA = 0 BestB = 0 Dayinit = day Monthinit = month EndIf once R2LimE = StartingValue once PIncPos = 1 //Positive Increment Position once NIncPos = 1 //Neative Increment Position once Optimize = 0 ////Initialize Heuristicks Engine Counter (Must be Incremented at Position Start or Exit) once Mode = 1 //Switches between negative and positive increments //once WinCountB = 3 //Initialize Best Win Count //GRAPH WinCountB coloured (0,0,0) AS "WinCountB" //once StratAvgB = 4353 //Initialize Best Avg Strategy Profit //GRAPH StratAvgB coloured (0,0,0) AS "StratAvgB" If Optimize = Reps Then WinCountA = 0 //Initialize current Win Count StratAvgA = 0 //Initialize current Avg Strategy Profit For i = 1 to Reps Do If positionperf(i) > 0 Then WinCountA = WinCountA + 1 //Increment Current WinCount EndIf StratAvgA = StratAvgA + (((PositionPerf(i)*countofposition[i]*close)*-1)*-1) Next StratAvgA = StratAvgA/Reps //Calculate Current Avg Strategy Profit //Graph (PositionPerf(1)*countofposition[1]*close)*-1 as "PosPerf1" //Graph (PositionPerf(2)*countofposition[2]*close)*-1 as "PosPerf2" //Graph StratAvgA*-1 as "StratAvgA" //once BestA = 300 //GRAPH BestA coloured (0,0,0) AS "BestA" If StratAvgA >= StratAvgB Then StratAvgB = StratAvgA //Update Best Strategy Profit BestA = R2LimE EndIf //once BestB = 300 //GRAPH BestB coloured (0,0,0) AS "BestB" If WinCountA >= WinCountB Then WinCountB = WinCountA //Update Best Win Count BestB = R2LimE EndIf If WinCountA > WinCountB and StratAvgA > StratAvgB Then Mode = 0 ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode = 1 Then R2LimE = R2LimE - (Increment*NIncPos) NIncPos = NIncPos + 1 Mode = 2 ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode = 1 Then R2LimE = R2LimE + (Increment*PIncPos) PIncPos = PIncPos + 1 Mode = 1 ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode = 2 Then R2LimE = R2LimE + (Increment*PIncPos) PIncPos = PIncPos + 1 Mode = 1 ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode = 2 Then R2LimE = R2LimE - (Increment*NIncPos) NIncPos = NIncPos + 1 Mode = 2 EndIf If NIncPos > MaxIncrement or PIncPos > MaxIncrement Then If BestA = BestB Then R2LimE = BestA Else If reps >= 10 Then WeightedScore = 10 Else WeightedScore = round((reps/100)*100) EndIf R2LimE = round(((BestA*(20-WeightedScore)) + (BestB*WeightedScore))/20) //Lower Reps = Less weight assigned to Win% EndIf NIncPos = 1 PIncPos = 1 ElsIf R2LimE > MaxValue Then R2LimE = MaxValue ElsIf R2LimE < MinValue Then R2LimE = MinValue EndIF Optimize = 0 EndIf // Heuristics Algorithm 1 End //************************************************************************ // Heuristics Algorithm 2 Start If (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) Then optimize2 = optimize2 + 1 Endif StartingValue2 = 0.7 ResetPeriod2 = 5 //Specify no of months after which to reset optimization Increment2 = 0.005 MaxIncrement2 = 40 //Limit of no of increments either up or down Reps2 = 3 //Number of trades to use for analysis MaxValue2 = 0.8 //Maximum allowed value MinValue2 = 0.6 //Minimum allowed value once Dayinit2 = day once Monthinit2 = month If (month = Monthinit2 and day = (Dayinit2 + ResetPeriod2)) or (month = (Monthinit2 + 1) and ((month - Dayinit2) + day = ResetPeriod2)) Then R2LimS = StartingValue2 WinCountB2 = 0 StratAvgB2 = 0 BestA2 = 0 BestB2 = 0 Dayinit2 = Hour Monthinit2 = Day EndIf once R2LimS = StartingValue2 once PIncPos2 = 1 //Positive Increment Position once NIncPos2 = 1 //Neative Increment Position once Optimize2 = 0 ////Initialize Heuristicks Engine Counter (Must be Incremented at Position Start or Exit) once Mode2 = 1 //Switches between negative and positive increments //once WinCountB2 = 3 //Initialize Best Win Count //GRAPH WinCountB2 coloured (0,0,0) AS "WinCountB2" //once StratAvgB2 = 4353 //Initialize Best Avg Strategy Profit //GRAPH StratAvgB2 coloured (0,0,0) AS "StratAvgB2" If Optimize2 = Reps2 Then WinCountA2 = 0 //Initialize current Win Count StratAvgA2 = 0 //Initialize current Avg Strategy Profit For i2 = 1 to Reps2 Do If positionperf(i2) > 0 Then WinCountA2 = WinCountA2 + 1 //Increment Current WinCount EndIf StratAvgA2 = StratAvgA2 + (((PositionPerf(i2)*countofposition[i2]*close)*-1)*-1) Next StratAvgA2 = StratAvgA2/Reps2 //Calculate Current Avg Strategy Profit //Graph (PositionPerf(1)*countofposition[1]*close)*-1 as "PosPerf1-2" //Graph (PositionPerf(2)*countofposition[2]*close)*-1 as "PosPerf2-2" //Graph StratAvgA2*-1 as "StratAvgA2" //once BestA2 = 300 //GRAPH BestA2 coloured (0,0,0) AS "BestA2" If StratAvgA2 >= StratAvgB2 Then StratAvgB2 = StratAvgA2 //Update Best Strategy Profit BestA2 = R2LimS EndIf //once BestB2 = 300 //GRAPH BestB2 coloured (0,0,0) AS "BestB2" If WinCountA2 >= WinCountB2 Then WinCountB2 = WinCountA2 //Update Best Win Count BestB2 = R2LimS EndIf If WinCountA2 > WinCountB2 and StratAvgA2 > StratAvgB2 Then Mode2 = 0 ElsIf WinCountA2 < WinCountB2 and StratAvgA2 < StratAvgB2 and Mode2 = 1 Then R2LimS = R2LimS - (Increment2*NIncPos2) NIncPos2 = NIncPos2 + 1 Mode2 = 2 ElsIf WinCountA2 >= WinCountB2 or StratAvgA2 >= StratAvgB2 and Mode2 = 1 Then R2LimS = R2LimS + (Increment2*PIncPos2) PIncPos2 = PIncPos2 + 1 Mode2 = 1 ElsIf WinCountA2 < WinCountB2 and StratAvgA2 < StratAvgB2 and Mode2 = 2 Then R2LimS = R2LimS + (Increment2*PIncPos2) PIncPos2 = PIncPos2 + 1 Mode2 = 1 ElsIf WinCountA2 >= WinCountB2 or StratAvgA2 >= StratAvgB2 and Mode2 = 2 Then R2LimS = R2LimS - (Increment2*NIncPos2) NIncPos2 = NIncPos2 + 1 Mode2 = 2 EndIf If NIncPos2 > MaxIncrement2 or PIncPos2 > MaxIncrement2 Then If BestA2 = BestB2 Then R2LimS = BestA2 Else If reps2 >= 10 Then WeightedScore2 = 10 Else WeightedScore2 = round((reps2/100)*100) EndIf R2LimS = round(((BestA2*(20-WeightedScore2)) + (BestB2*WeightedScore2))/20) //Lower Reps = Less weight assigned to Win% EndIf NIncPos2 = 1 PIncPos2 = 1 ElsIf R2LimS > MaxValue2 Then R2LimS = MaxValue2 ElsIf R2LimS < MinValue2 Then R2LimS = MinValue2 EndIF Optimize2 = 0 EndIf // Heuristics Algorithm 2 End //************************************************************************ // Heuristics Algorithm 3 Start If (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) Then optimize3 = optimize3 + 1 EnDif StartingValue3 = 5.6 ResetPeriod3 = 5 //Specify no of hour after which to reset optimization Increment3 = 0.2 MaxIncrement3 = 15 //Limit of no of Increment3s either up or down Reps3 = 3 //Number of trades to use for analysis MaxValue3 = 7 //Maximum allowed value MinValue3 = 4 //Minimum allowed value once Dayinit3 = day once Monthinit3 = month If (month = Monthinit3 and day = (Dayinit3 + ResetPeriod3)) or (month = (Monthinit3 + 1) and ((month - Dayinit3) + day = ResetPeriod3)) Then TrailingStart = StartingValue3 WinCountB3 = 0 StratAvgB3 = 0 BestA3 = 0 BestB3 = 0 Dayinit3 = day Monthinit3 = month EndIf once TrailingStart = StartingValue3 once PincPos3 = 1 //Positive Increment3 Position once NincPos3 = 1 //Neative Increment3 Position once optimize3 = 0 ////Initialize Heuristicks Engine Counter (Must be Increment3ed at Position Start or Exit) once Mode3 = 1 //Switches between negative and positive Increment3s //once WinCountB3 = 3 //Initialize Best Win Count //GRAPH WinCountB3 coloured (0,0,0) AS "WinCountB3" //once StratAvgB3 = 4353 //Initialize Best Avg Strategy Profit //GRAPH StratAvgB3 coloured (0,0,0) AS "StratAvgB3" If optimize3 = Reps3 Then WinCountA3 = 0 //Initialize current Win Count StratAvgA3 = 0 //Initialize current Avg Strategy Profit For i3 = 1 to Reps3 Do If positionperf(i3) > 0 Then WinCountA3 = WinCountA3 + 1 //Increment3 Current WinCount EndIf StratAvgA3 = StratAvgA3 + (((PositionPerf(i3)*countofposition[i3]*close)*-1)*-1) Next StratAvgA3 = StratAvgA3/Reps3 //Calculate Current Avg Strategy Profit //Graph (PositionPerf(1)*countofposition[1]*close)*-1 as "PosPerf1" //Graph (PositionPerf(2)*countofposition[2]*close)*-1 as "PosPerf2" //Graph StratAvgA3*-1 as "StratAvgA3" //once BestA3 = 300 //GRAPH BestA3 coloured (0,0,0) AS "BestA3" If StratAvgA3 >= StratAvgB3 Then StratAvgB3 = StratAvgA3 //Update Best Strategy Profit BestA3 = TrailingStart EndIf //once BestB3 = 300 //GRAPH BestB3 coloured (0,0,0) AS "BestB3" If WinCountA3 >= WinCountB3 Then WinCountB3 = WinCountA3 //Update Best Win Count BestB3 = TrailingStart EndIf If WinCountA3 > WinCountB3 and StratAvgA3 > StratAvgB3 Then Mode3 = 0 ElsIf WinCountA3 < WinCountB3 and StratAvgA3 < StratAvgB3 and Mode3 = 1 Then TrailingStart = TrailingStart - (Increment3*NincPos3) NincPos3 = NincPos3 + 1 Mode3 = 2 ElsIf WinCountA3 >= WinCountB3 or StratAvgA3 >= StratAvgB3 and Mode3 = 1 Then TrailingStart = TrailingStart + (Increment3*PincPos3) PincPos3 = PincPos3 + 1 Mode3 = 1 ElsIf WinCountA3 < WinCountB3 and StratAvgA3 < StratAvgB3 and Mode3 = 2 Then TrailingStart = TrailingStart + (Increment3*PincPos3) PincPos3 = PincPos3 + 1 Mode3 = 1 ElsIf WinCountA3 >= WinCountB3 or StratAvgA3 >= StratAvgB3 and Mode3 = 2 Then TrailingStart = TrailingStart - (Increment3*NincPos3) NincPos3 = NincPos3 + 1 Mode3 = 2 EndIf If NincPos3 > MaxIncrement3 or PincPos3 > MaxIncrement3 Then If BestA3 = BestB3 Then TrailingStart = BestA3 Else If Reps3 >= 10 Then WeightedScore3 = 10 Else WeightedScore3 = round((Reps3/100)*100) EndIf TrailingStep = round(((BestA3*(20-WeightedScore3)) + (BestB3*WeightedScore3))/20) //Lower Reps3 = Less weight assigned to Win% EndIf NincPos3 = 1 PincPos3 = 1 ElsIf TrailingStart > MaxValue3 Then TrailingStart = MaxValue3 ElsIf TrailingStart < MinValue3 Then TrailingStart = MinValue3 EndIF optimize3 = 0 EndIf // Heuristics Algorithm 3 End //************************************************************************ // Heuristics Algorithm 4 Start If (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) Then optimize4 = optimize4 + 1 EnDif StartingValue4 = 1.9 ResetPeriod4 = 5 //Specify no of days after which to reset optimization Increment4 = 0.1 MaxIncrement4 = 20 //Limit of no of Increment4s either up or down Reps4 = 3 //Number of trades to use for analysis MaxValue4 = 3 //Maximum allowed value MinValue4 = 1 //Minimum allowed value once Dayinit4 = Day once Monthinit4 = Month If (Month = Monthinit4 and Day = (Dayinit4 + ResetPeriod4)) or (Month = (Monthinit4 + 1) and ((month - Dayinit4) + Day = ResetPeriod4)) Then TrailingStep = StartingValue4 WinCountB4 = 0 StratAvgB4 = 0 BestA4 = 0 BestB4 = 0 Dayinit4 = Day Monthinit4 = Month EndIf once TrailingStep = StartingValue4 once PincPos4 = 1 //Positive Increment4 Position once NincPos4 = 1 //Neative Increment4 Position once optimize4 = 0 ////Initialize Heuristicks Engine Counter (Must be Increment4ed at Position Start or Exit) once Mode4 = 1 //Switches between negative and positive Increment4s //once WinCountB4 = 4 //Initialize Best Win Count //GRAPH WinCountB4 coloured (0,0,0) AS "WinCountB4" //once StratAvgB4 = 4454 //Initialize Best Avg Strategy Profit //GRAPH StratAvgB4 coloured (0,0,0) AS "StratAvgB4" If optimize4 = Reps4 Then WinCountA4 = 0 //Initialize current Win Count StratAvgA4 = 0 //Initialize current Avg Strategy Profit For i4 = 1 to Reps4 Do If positionperf(i4) > 0 Then WinCountA4 = WinCountA4 + 1 //Increment4 Current WinCount EndIf StratAvgA4 = StratAvgA4 + (((PositionPerf(i4)*countofposition[i4]*close)*-1)*-1) Next StratAvgA4 = StratAvgA4/Reps4 //Calculate Current Avg Strategy Profit //Graph (PositionPerf(1)*countofposition[1]*close)*-1 as "PosPerf1" //Graph (PositionPerf(2)*countofposition[2]*close)*-1 as "PosPerf2" //Graph StratAvgA4*-1 as "StratAvgA4" //once BestA4 = 400 //GRAPH BestA4 coloured (0,0,0) AS "BestA4" If StratAvgA4 >= StratAvgB4 Then StratAvgB4 = StratAvgA4 //Update Best Strategy Profit BestA4 = TrailingStep EndIf //once BestB4 = 400 //GRAPH BestB4 coloured (0,0,0) AS "BestB4" If WinCountA4 >= WinCountB4 Then WinCountB4 = WinCountA4 //Update Best Win Count BestB4 = TrailingStep EndIf If WinCountA4 > WinCountB4 and StratAvgA4 > StratAvgB4 Then Mode4 = 0 ElsIf WinCountA4 < WinCountB4 and StratAvgA4 < StratAvgB4 and Mode4 = 1 Then TrailingStep = TrailingStep - (Increment4*NincPos4) NincPos4 = NincPos4 + 1 Mode4 = 2 ElsIf WinCountA4 >= WinCountB4 or StratAvgA4 >= StratAvgB4 and Mode4 = 1 Then TrailingStep = TrailingStep + (Increment4*PincPos4) PincPos4 = PincPos4 + 1 Mode4 = 1 ElsIf WinCountA4 < WinCountB4 and StratAvgA4 < StratAvgB4 and Mode4 = 2 Then TrailingStep = TrailingStep + (Increment4*PincPos4) PincPos4 = PincPos4 + 1 Mode4 = 1 ElsIf WinCountA4 >= WinCountB4 or StratAvgA4 >= StratAvgB4 and Mode4 = 2 Then TrailingStep = TrailingStep - (Increment4*NincPos4) NincPos4 = NincPos4 + 1 Mode4 = 2 EndIf If NincPos4 > MaxIncrement4 or PincPos4 > MaxIncrement4 Then If BestA4 = BestB4 Then TrailingStep = BestA4 Else If Reps4 >= 10 Then WeightedScore4 = 10 Else WeightedScore4 = round((Reps4/100)*100) EndIf TrailingStep = round(((BestA4*(20-WeightedScore4)) + (BestB4*WeightedScore4))/20) //Lower Reps4 = Less weight assigned to Win% EndIf NincPos4 = 1 PincPos4 = 1 ElsIf TrailingStep > MaxValue4 Then TrailingStep = MaxValue4 ElsIf TrailingStep < MinValue4 Then TrailingStep = MinValue4 EndIF optimize4 = 0 EndIf // Heuristics Algorithm 4 End //************************************************************************ //Pivot (H + L + C + O)/4 If OpenDayOfWeek = 1 Then Ht = DHigh(2) Bs = DLow(2) C = DClose(2) O = DOpen(0) Endif If OpenDayOfWeek => 2 and dayofweek < 6 Then Ht = DHigh(1) Bs = DLow(1) C = DClose(1) O = DOpen(0) Endif Pivot = (Ht + Bs + C + O)/4 Res4 = Ht + (3*(Pivot - BS)) Res3 = Ht + (2*(Pivot - Bs)) Res2 = Pivot + (Ht - Bs) Res1 = (2*Pivot) - Bs Sup1 = (2*Pivot) - Ht Sup2 = Pivot-(Ht - Bs) Sup3 = Bs - (2*(Ht - Pivot)) Sup4 = Bs - (3*(Ht - Pivot)) //Heikin-Hachi Once UpDown = 0 IF BarIndex = 0 Then xClose = TotalPrice xOpen = Range xHigh = High xLow = Low Else xClose = TotalPrice xOpen = (xOpen[1] + xClose[1])/2 xHigh = Max(max(high, xOpen), xClose) xLow = Min(min(Low, xOpen), xClose) endif If XClose >= XOpen then if UpDown <> 1 then UpDown = 1 endif Else If UpDown <> -1 then UpDown = -1 endif endif HHSize = 0.6 Distance = 8 LookBack = 8640 SRk = 5 SRs = 8 //P = 9 // Slope, R², RSI, Sochastic //R2LimE = 0.52 // Coefficient de correlation R² d'entrée //R2LimS = 0.77 // Coefficient de correlation R² de sortie Q = P // Stochastic R = 3 // Stochastic S = 5 // Stochastic SumBull = 2 // Variable Bull SumBear = 2 // Variable Bear // Timeframe SRLevel timeframe (5 minutes, updateonclose) // --- icihmoku support and resistance kijun = (highest[26](high)+lowest[26](low))/2 SSB = (highest[52](high[26])+lowest[52](low[26]))/2 kijunp = summation[SRk](Kijun=Kijun[1])=SRk ssbp = summation[SRs](SSB=SSB[1])=SRs if kijunp then kijunPrice = kijun endif if ssbp then ssbPrice = SSB endif if kijunprice = ssbprice then SRlevel = kijunprice if SRLevel > Close then ResLevel = SRlevel elsif SRLevel < Close then SupLevel = SRlevel endif endif // Timeframe en UT Supérieur Timeframe (3 minutes, updateonclose) SlopeUTSup = Endpointaverage[P](LinearRegressionSlope[P](Close)) If SlopeUTSup > SlopeUTSup[1] then BullUTSup = 1 BearUTSup = 0 Elsif SlopeUTSup < SlopeUTSup[1] then BullUTSup = 0 BearUTSup = -1 endif MyR2Sup = R2[P](Close) If MyR2Sup > R2LimE then AllowedEntry = 1 Elsif MyR2Sup < R2LimE then AllowedEntry = 0 Endif MyRSIUTSup = TriangularAverage[P](RSI[5](Close)) If MyRSIUTSup > MyRSIUTSup[1] then MyRSIUTSupBull = +1 MyRSIUTSupBear = 0 Elsif MyRSIUTSup < MyRSIUTSup[1] then MyRSIUTSupBull = 0 MyRSIUTSupBear = -1 Endif //************************************************************************ //Timeframe en UT de Trading Timeframe (10 seconds, default) EMA50 = ExponentialAverage[50](Close) EMA200 = ExponentialAverage[200](Close) Slope = EndpointAverage[P](LinearRegressionSlope[P](Close)) If Slope > Slope[1] Then Bull = +1 Bear = 0 Elsif Slope < Slope[1] Then Bull = 0 Bear = -1 Endif MyR2 = R2[P](WeightedClose) MyRSI = EndpointAverage[P](RSI[5](Close)) If MyRSI > MyRSI[1] then MyRSIBull = +1 MyRSIBear = 0 Elsif MyRSI < MyRSI[1] then MyRSIBull = 0 MyRSIBear = -1 Endif MyStocK = Stochastic[Q,R](close) MyStocD = WeightedAverage[S](Stochastic[Q,R](close)) If MyStocK > MyStocD Then StocUp = +1 StocDown = 0 Elsif MyStocK < MyStocD Then StocUp = 0 StocDown = -1 Endif //************************************************************************ levier = 2 capital = 500 + (strategyprofit*2/5) z = (capital / (close/20)) * levier //************************************************************************ //Position acheteuse BuyConditionA = (xClose - xOpen)*pipsize => HHSize BuyConditionB = Summation[SumBull](BullUTSup) = SumBull BuyConditionC = Summation[SumBull](AllowedEntry) = Sumbull BuyConditionD = MyRSIUTSup < 76.4 BuyConditionE = summation[SumBull](MyRSIUTSupBull) = SumBull BuyConditionF = EMA50 > EMA200 and EMA50 < Close and EMA200 < Close BuyConditionG = Summation[SumBull](Bull) = SumBull BuyConditionH = MyRSI < 76.4 BuyConditionI = summation[SumBull](MyRSIBull) = SumBull BuyConditionJ = Summation[SumBull](StocUp) = SumBull and MyStocK < 80 BuyConditionK = MyR2 Crosses over R2LimE BuyConditionL = MyR2 > R2LimE if BuyconditionA and BuyConditionB and BuyConditionC and BuyConditionD and BuyConditionE and BuyConditionF and BuyConditionG and BuyConditionH and BuyConditionI and BuyConditionJ and BuyConditionK and not onmarket and not daysForbiddenEntry then allowtrading = 1 for iSRB = 0 to lookback -1 do dist = (Reslevel[iSRB] - Close) < distance*pipsize if dist then allowtrading = 0 //no trading is allowed we are near a SR! break //break the loop, no need to continue, trading is not allowed anymore! endif next if close > pivot then //above Pivot iPivt = 1 while iPivt =< 4 do if iPivt = 1 then Floor = Pivot Ceil = Res1 if close > Floor and close < Ceil then break endif elsif iPivt = 2 then Floor = Res1 Ceil = Res2 if close > Floor and close < Ceil then break endif elsif iPivt = 3 then Floor = Res2 Ceil = Res3 if close > Floor and close < Ceil then break endif elsif iPivt = 4 then Floor = Res3 Ceil = Res4 if close > Floor and close < Ceil then break endif endif iPivt = iPivt + 1 wend elsif close < Pivot then //below Pivot iPivt = 1 while iPivt <= 4 do if iPivt = 1 then Floor = Sup1 Ceil = Pivot if close > Floor and close < Ceil then break endif elsif iPivt = 2 then Floor = Sup2 Ceil = Sup1 if close > Floor and close < Ceil then break endif elsif iPivt = 3 then Floor = Sup3 Ceil = Sup2 if close > Floor and close < Ceil then break endif elsif iPivt = 4 then Floor = Sup4 Ceil = Sup3 if close > Floor and close < Ceil then break endif endif iPivt = iPivt + 1 wend endif For IPivt = 1 to 4 do dist = (Ceil - Close) < distance*pipsize If Dist then allowtrading = 0 Break endif next If BuyConditionL then Entry = Barindex endif if Barindex-Entry <= 2 then if allowtrading then buy z share at market endif endif endif If Longonmarket and MyR2Sup crosses under R2LimS then Sell at Market elsif Longonmarket and MyR2Sup crosses under R2LimE then Sell at Market Endif //Position Vendeuse SellConditionA = (xOpen - xClose)*pipsize => HHSize SellConditionB = Summation[SumBear](BearUTSup) = -SumBear SellConditionC = Summation[SumBull](AllowedEntry) = SumBull SellConditionD = MyRSIUTSup > 23.6 SellConditionE = Summation[SumBear](MyRSIUTSupBear) = -SumBear SellConditionF = EMA50 < EMA200 and EMA50 > Close and EMA200 > Close SellConditionG = Summation[SumBear](Bear) = -SumBear SellConditionH = MyRSI > 23.6 SellConditionI = Summation[SumBear](MyRSIBear) = -SumBear SellConditionJ = Summation[SumBear](StocDown) = -SumBear and MyStocK > 20 SellConditionK = MyR2 Crosses over R2LimE SellConditionL = MyR2 > R2LimE if SellConditionA and SellconditionB and SellConditionC And SellConditionD and SellConditionE and SellConditionF and SellConditionG and SellConditionH and SellConditionI and SellConditionJ and SellConditionK and not onmarket and not daysForbiddenEntry then allowtrading = 1 for iSRV = 0 to lookback -1 do dist = (close-Suplevel[iSRV]) < distance*pipsize if dist then allowtrading = 0 //no trading is allowed we are near a SR! break //break the loop, no need to continue, trading is not allowed anymore! endif next if close > pivot then //above Pivot iPivt = 1 while iPivt =< 4 do if iPivt = 1 then Floor = Pivot Ceil = Res1 if close > Floor and close < Ceil then break endif elsif iPivt = 2 then Floor = Res1 Ceil = Res2 if close > Floor and close < Ceil then break endif elsif iPivt = 3 then Floor = Res2 Ceil = Res3 if close > Floor and close < Ceil then break endif elsif iPivt = 4 then Floor = Res3 Ceil = Res4 if close > Floor and close < Ceil then break endif endif iPivt = iPivt + 1 wend elsif close < Pivot then //below Pivot iPivt = 1 while iPivt <= 4 do if iPivt = 1 then Floor = Sup1 Ceil = Pivot if close > Floor and close < Ceil then break endif elsif iPivt = 2 then Floor = Sup2 Ceil = Sup1 if close > Floor and close < Ceil then break endif elsif iPivt = 3 then Floor = Sup3 Ceil = Sup2 if close > Floor and close < Ceil then break endif elsif iPivt = 4 then Floor = Sup4 Ceil = Sup3 if close > Floor and close < Ceil then break endif endif iPivt = iPivt + 1 wend endif For IPivt = 1 to 4 do dist = (Close - Floor) < distance*pipsize If Dist then allowtrading = 0 Break endif next if SellConditionL then Entry = Barindex endif If Barindex-Entry <= 2 then if allowtrading then sellshort z share at market endif endif endif If Shortonmarket and MyR2Sup crosses under R2LimS then Exitshort at market elsif Shortonmarket and MyR2Sup crosses under R2LimE then Exitshort at market Endif //************************************************************************ //Stop Loss & Trailing function //Set stop $loss capital*levier*4/100 Set Target $Profit capital*levier*3/100 //reset the stoploss value If not onmarket then newSL = 0 Endif //manage long positions If Longonmarket Then If newSL = 0 and xLow-tradeprice(1) > trailingstart*pipsize then newSL = tradeprice(1) + trailingstep*pipsize Endif If newSL <> 0 and xLow-newSL > trailingstep*pipsize then newSL = newSL + trailingstep*pipsize Endif Endif //manage short positions If ShortonMarket then If newSL = 0 and tradeprice(1)-xHigh > trailingstart*pipsize Then newSL = tradeprice(1) - trailingstep*pipsize Endif If newSL <> 0 and newSL-xHigh > trailingstep*pipsize Then newSL = newSL - trailingstep*pipsize Endif Endif //stop order to exit the positions If newSL <> 0 Then Sell at newSL Stop Exitshort at newSL Stop Endif //************************************************************************ma contribution au cercle vertueux…

Nicolas thanked this postMerci Fantasio, pourrais-tu nous en dire un peu plus sur la stratégie ? Le code étant très long et complexe, ce serait déjà une bonne base pour les suggestions d’améliorations ! Merci encore 😉

Slt Nicolas, oui en effet, le code est long mais il ne doit pas faire peur…! tout d’abord, je dois dire que j’ai découvert prorealcode pendant le dernier confinement, je ne suis pas programmeur, j’apprend sur le tas en lisant le forum et en décryptant vos codes à tous; beaucoup dans mon code sont des morceaux qui viennent d’un peu partout, j’ai peut être des incohérences ce qui expliquerait que je me retrouve certaines semaines avec des résultats neutre, d’autres semaines c’est très bon. c’est une stratégie disont “intrascalp” qui prend en compte plusieurs timeframe, car c’est le seul moyen fiable que j’ai trouvé pour confirmer la tendance à court terme. c’est une stratégie en 10 secondes ce qui ne me permet pas de backtester au delà de 4 jours, peut être certain d’entre vous pouront faire plus avec la V11 la première partie du code sont une succession de 5 algorithmes que j’ai emprunté à Juan. ils servent à l’optimisation des variables:- StartingValueP = période pour:

- Slope ==> pente de régression linéaire

- R² ==> coefficient de corrélation de Scope

- moyenne mobile d’un RSI[5]

- période du Stochastique

- StartingValue = variable d’ajustement pour la valeur d’entrée en position en fonction du R² ( supérieur à 0,4) 0.54

- StartingValue2 = variable d’ajustement du R² de sortie

- StartingValue3 = il s’agit de l’optimisation de la variable d’un trailingstart (basée sur Heikin Ashi)

- StartingValue4 = il s’agit de l’optimisation de la variable d’un trailingstep (basée sur Heikin Ashi)

- Timeframe (5 minutes, updateonclose)

j’utilise Ichimoku dans ce timeframe pour definir des supports et résistance en fonction des plats Kijun et SSB, j’utilise également le point pivot pour définir les résistance et support du pivot, si je suis trop proche de ces zones je ne dois pas trader!

- Timeframe (3 minutes, updateonclose) ça change en fonction de l’actif, car ce time frame est important pour l’indice trader, 2, 3, 4….4 étant un maximum

- dans ce time frame intervient plusieurs indicateurs:

- une pente de régression linéaire (Slope)

- un R²

- un RSI

- dans ce time frame intervient plusieurs indicateurs:

Slope me donne la tendance, elle monte je suis à l’achat, elle descend je suis à la vente. le RSI doit être inférieur à 76.4 en achat et supérieur à 23.8 en vente (référence à un palier de fibo…;)); le R² me sert pour déterminer un point d’entrée, en fonction de Slope, il me confirme la tendance lorsqu’il est supérieur à 0,x “0.54 dans le cas présent sur le Nasdaq). c’est tout pour ce time frame.

j’ai créer des valeurs booléenne pour l’interprétation de comment le code doit fonctionner (si des questions je suis à votre disposition)

- Timeframe (10 seconds, default)

- c’est le timeframe de trading, si les conditions définies dans le timeframe supérieur (3 minutes) sont remplie, et que je trouve un point d’entrée en 10 sec alors j’entre.

- je remarque malgré tout que souvent après etre entré en position le marché se retourne, il s’agit de la seule raison qui me fait perdre une position (j’en arrive à la conclusion que je suis chaque fois en retard sur l’entrée)

Dans ce timeframe j’utilise également:

-

- deux moyennes mobile 50 et 200 (filtre pour entrer en position, sous les moyenne ==> vente ; au dessus des moyenne ==> Achat)

- une pente de régression linéaire

- une R²

- un RSI et un Stochastique

pour entrer en position, le RSI doit remplir les même condition qu’en UT supérieur, idem Slope et R² et le stochastique > 20 en vente et <80 à l’achat.

-

- que ce soit à la vente ou à l’achat, la différence entre l’ouverture et la fermeture de la bougie précédente ne doit pas être inférieur à 0.6*pipsize

- voir les conditions

- soit le stop suivre se déclenche et la position est gagnée quoi qu’il arrive

- soit le stop suiveur ne se déclenche pas et le marché se retourne et alors c’est le croisement à la baisse du R² en ut supérieur qui sert de stoploss

- R2limS qui correspond à une valeur élevée du R² (0.7 par défaut)

- R2LimE qui correspond à la valeur de corrélation limite

En effet c’est beaucoup plus clair, merci pour ce résumé 🙂 AMHA, il y a trop de conditions liées à des calculs d’indicateurs dans ton timeframe 10-sec. Si tu connais ta tendance dans les timeframes supérieurs, tu devrais attendre un retour à la moyenne dans ceux-ci, et trouver une action simple du prix dans la plus petite des unités de temps pour lancer ta position.Slt Nicolas, je vais essayé de pondre un truc… j’ai tellement passé de temps sur ce put….. de code que j’avoue avoir envie de prendre un peu de distance quelques jours. merci pour ton retour en tout cas. à titre personnel, vu que tu es le nez dans le code plus que moi, que pense tu de la stratégie?En effet c’est beaucoup plus clair, merci pour ce résumé 🙂 AMHA, il y a trop de conditions liées à des calculs d’indicateurs dans ton timeframe 10-sec. Si tu connais ta tendance dans les timeframes supérieurs, tu devrais attendre un retour à la moyenne dans ceux-ci, et trouver une action simple du prix dans la plus petite des unités de temps pour lancer ta position.

Slt Nicolas, j’ai tenté de réduire les conditions en UT 10′ sans réel amélioration. j’ai ajusté et filtré mon code actuel ce qui améliore la stratégie, mais je suis convaincu qu’il y a moyen d’obtenir mieux… le code actuel fonctionne bien sur le nasdaq….sur les autres indices c’estplus compliqué.Dernière mise à jour: [edit modérateur: merci de poster la stratégie en fichier texte attaché, trop de codes à afficher] …Merci Fantasio, mais j’ai dut supprimer le dernier code, ça faisait planter l’affichage du site 🙄 Aurais-tu la gentillesse d’attacher le code dans un fichier texte la prochaine fois ? (on un ficher itf bien entendu). Merci encore pour le partage.Merci Fantasio, mais j’ai dut supprimer le dernier code, ça faisait planter l’affichage du site 🙄 Aurais-tu la gentillesse d’attacher le code dans un fichier texte la prochaine fois ? (on un ficher itf bien entendu). Merci encore pour le partage.

Disons que j’espère aussi profiter des amélioration que d’autre pourrons apporter. jusque là j’ai beaucoup sollicité la communauté, à mon tour de proposer quelque chose. si la stratégie s’avère pas trop mal je pourrais l’ajouter à la base de donnée des stratégies déjà existantes.Petite erreur sur les conditions de sortie de short:

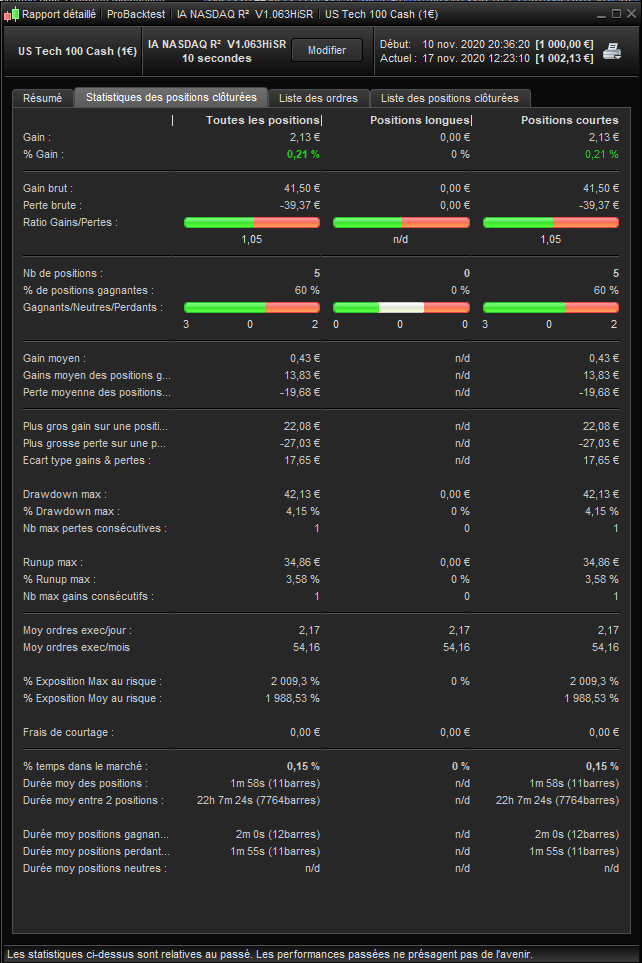

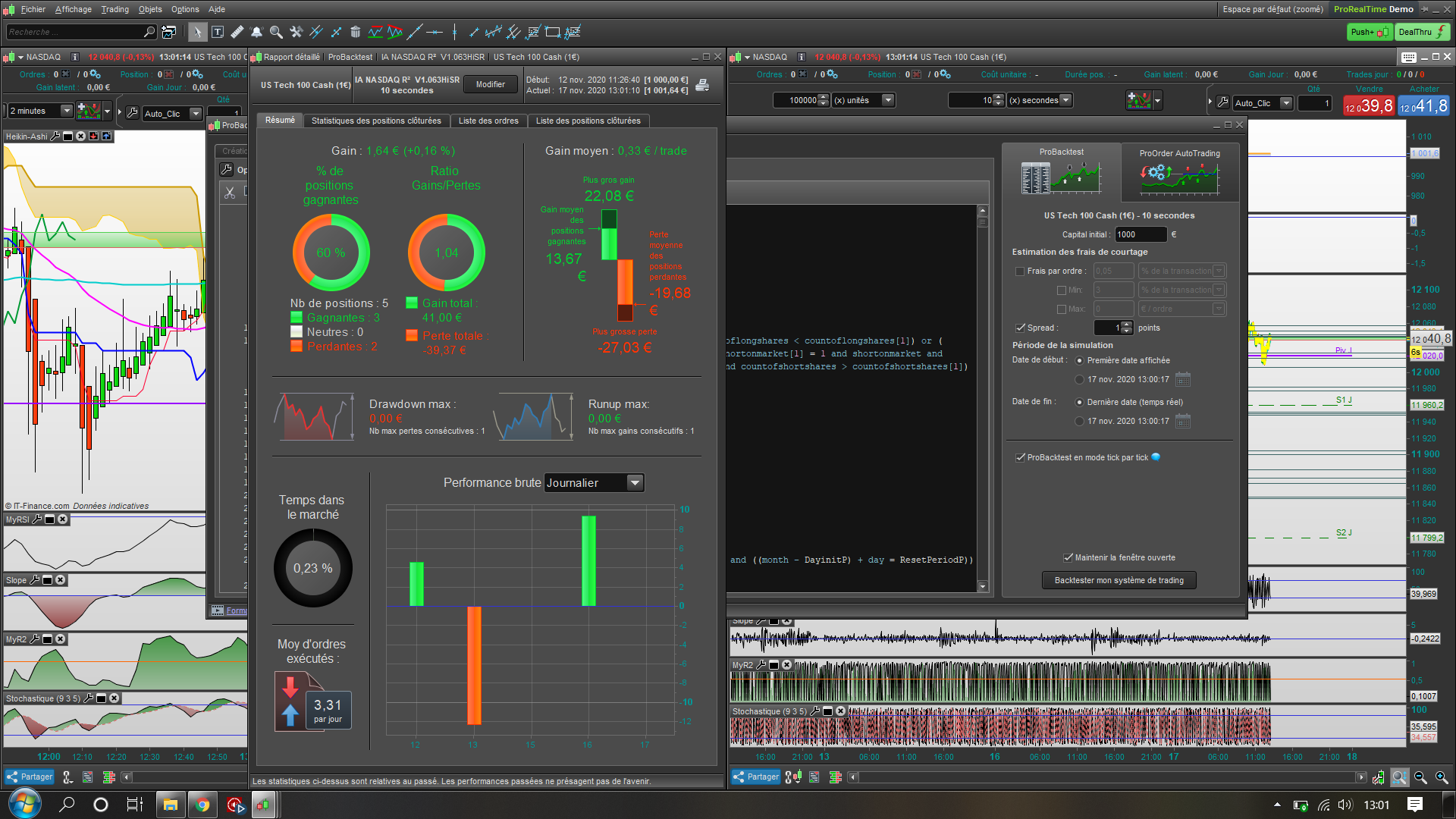

erreur de copié collé.If Shortonmarket and EMA13 crosses over EMA50 then Exitshort at Market elsif shortonmarket and MyR2Sup crosses under R2LimS then Exitshort at Market elsif shortonmarket and MyR2Sup crosses under R2LimE then Exitshort at Market EndifBonjour Fantasio, Merci d’avoir partagé ton travail. Je ne suis pas Expert, mais ton code m’intéresse beaucoup car vue la volatilité actuelle, il vaut mieux profiter de micro oscillations que de faire du Trend Following. Il suffit d’un Tweet de X ou Y personnalité pour que le compte parte en fumée 🙂 J’ai repris ton fichier (IA-NASDAQ-R²-V1.063HiSR.itf) et j’ai mis à jour les conditions de sortie comme indiqué dans ton post (11/12/2020 at 6:44 PM#150327). Malheureusement, j’arrive à un résultat largement inférieur à ton screen shot tant sur le Win Rate (60%) que sur le Profit Factor (x1.05). Aussi, l’Algo n’a pris que des ordres Short. As-tu fais les tests en mode tick by tick? Le Spread de 1 ne correspond pas à ce qu’il y a sur le site de IG. Sur des allers-retours fréquents avec petits gains, cela peut avoir un gros impact sur le résultat final. Je serais intéressé de savoir si tu obtiens les mêmes résultats.

Si tu postes la dernière version, je peux faire des tests sur SP500 et DAX si cela t’intéresse./// SPREAD NQ ////// IF time>=133000 AND time>200000 then spread = 1/2 ELSIF time>=200000 AND time>220000 then spread = 5/2 ELSIF time>=220000 AND time>133000 then spread = 2/2 ENDIFSlt Khaled, oui j’obtiens plus ou moins les mêmes résultats. les les backtest sont toujours effectués en tick/tick Je constat néanmoins des divergences entre back test et réel…. souvent en réel les résultats sont moins bon. La stratégie tourne pour le moment en demo, et j’observe… quand je détecte des position perdante j’essaie de compenser en ajoutant un filtre, c’est la raison pour laquelle le code s’allonge de semaine en semaine… et j’atteins les limites avec le code ci-joint; raison pour laquelle j’ai partagé…afin que la communauté puisse apporter sa contribution. La stratégie est bonne, je l’utilise quotidiennement en manuel avec de bon résultats ( 4 à 5%/jours avec une bonne discipline) le problème, c’est que c’est très difficile de demander à une statégie automatique de remplacer l’œil humain. Par contre l’histoire du spread, j’ai déjà effectué beaucoup de test sur différentes plages de trading, mais en dehors des plages horaires des marchés US ou EUR, je n’ai pas de bon résultats, car ils se comportent différemment en dehors des ouvertures de marché respective. Bien que les plages d’IG soient différentes et côtent H24, je ne conseil pas de trader les marchés US et dehors des ouvertures de WS (15H30 – 22H00 heures Europe) idem pour le CAC ou le DAX qui se trade entre 9h et 17h30 au plus tard; avec cette stratégie.Fantasio, je suis d’accord sur les horaires de trading sur IG, après la clôture des marchés US, ça devient du rodéo… ça doit être des Algos… Est ce que tu sais pourquoi ton Algo ne sort que des Trade Short ? même après la correction de SELL en SELLSHORT?ça doit être un concours de circonstance, car sur des backtest des précédentes semaine j’ai eu des long…. j’ai également eu un long il y a une quinzaine de minute sur un autre indice - StartingValueP = période pour:

-

AuthorPosts

- You must be logged in to reply to this topic.

Stratégie multi indices en 10′ (secondes)

ProOrder : Trading Automatique & Backtests

Author

Summary

This topic contains 21 replies,

has 4 voices, and was last updated by ![]() Meta Signals Pro

Meta Signals Pro

2 years, 6 months ago.

Topic Details

| Forum: | ProOrder : Trading Automatique & Backtests |

| Language: | French |

| Started: | 11/09/2020 |

| Status: | Active |

| Attachments: | 10 files |

About personal data collected

The information collected on this form is stored in a computer file by ProRealCode to create and access your ProRealCode profile. This data is kept in a secure database for the duration of the member's membership. They will be kept as long as you use our services and will be automatically deleted after 3 years of inactivity. Your personal data is used to create your private profile on ProRealCode. This data is maintained by SAS ProRealCode, 407 rue Freycinet, 59151 Arleux, France. If you subscribe to our newsletters, your email address is provided to our service provider "MailChimp" located in the United States, with whom we have signed a confidentiality agreement. This company is also compliant with the EU/Swiss Privacy Shield, and the GDPR. For any request for correction or deletion concerning your data, you can directly contact the ProRealCode team by email at privacy@prorealcode.com If you would like to lodge a complaint regarding the use of your personal data, you can contact your data protection supervisory authority.