Bonjour à tous,

Cela fait un moment que je suis parmi vous sur ce forum. Depuis toutes ces années j’ai surtout appris dans l’ombre et aujourd’hui je voudrais rendre un peu de qui a été donné en partageant une stratégie avec la communauté.

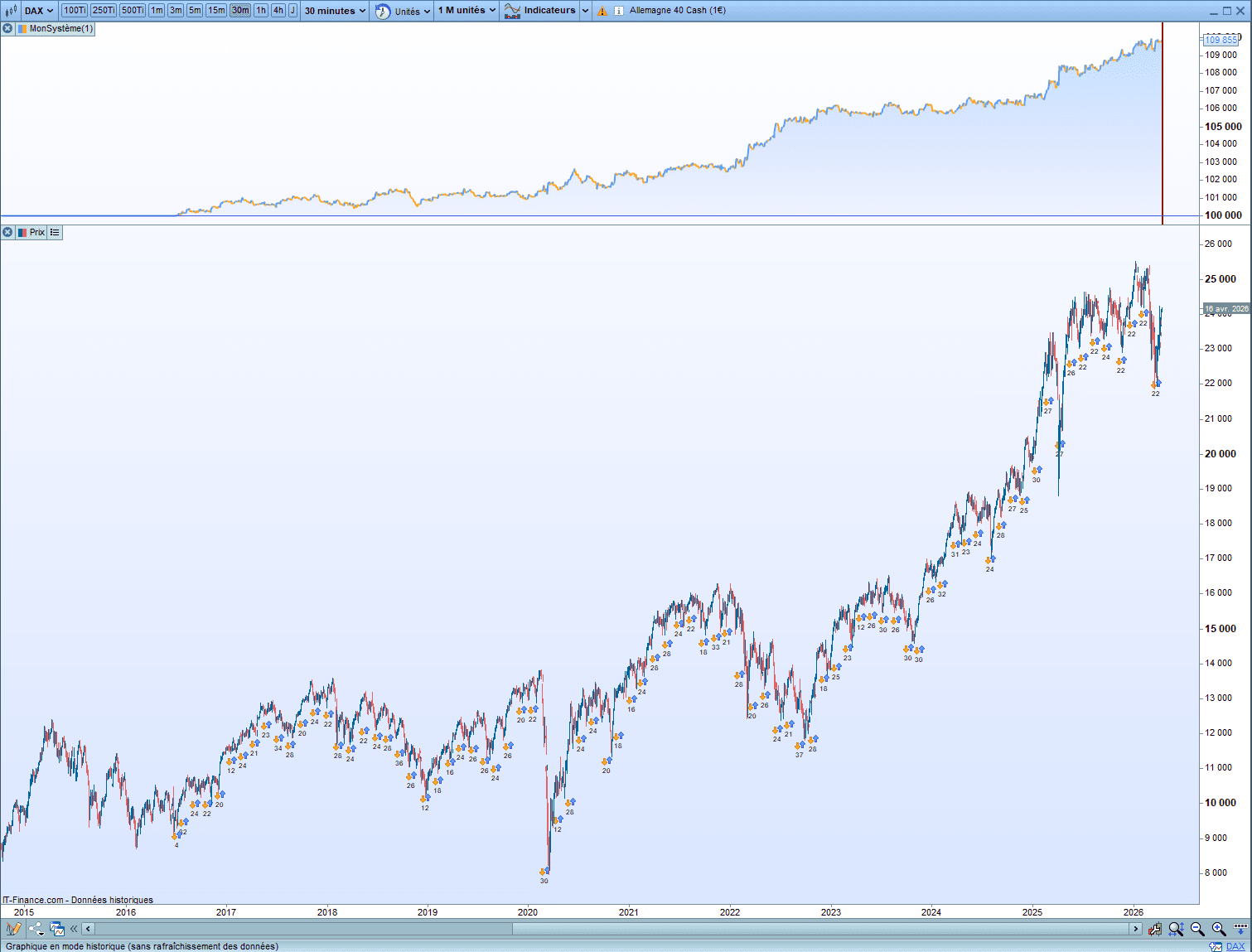

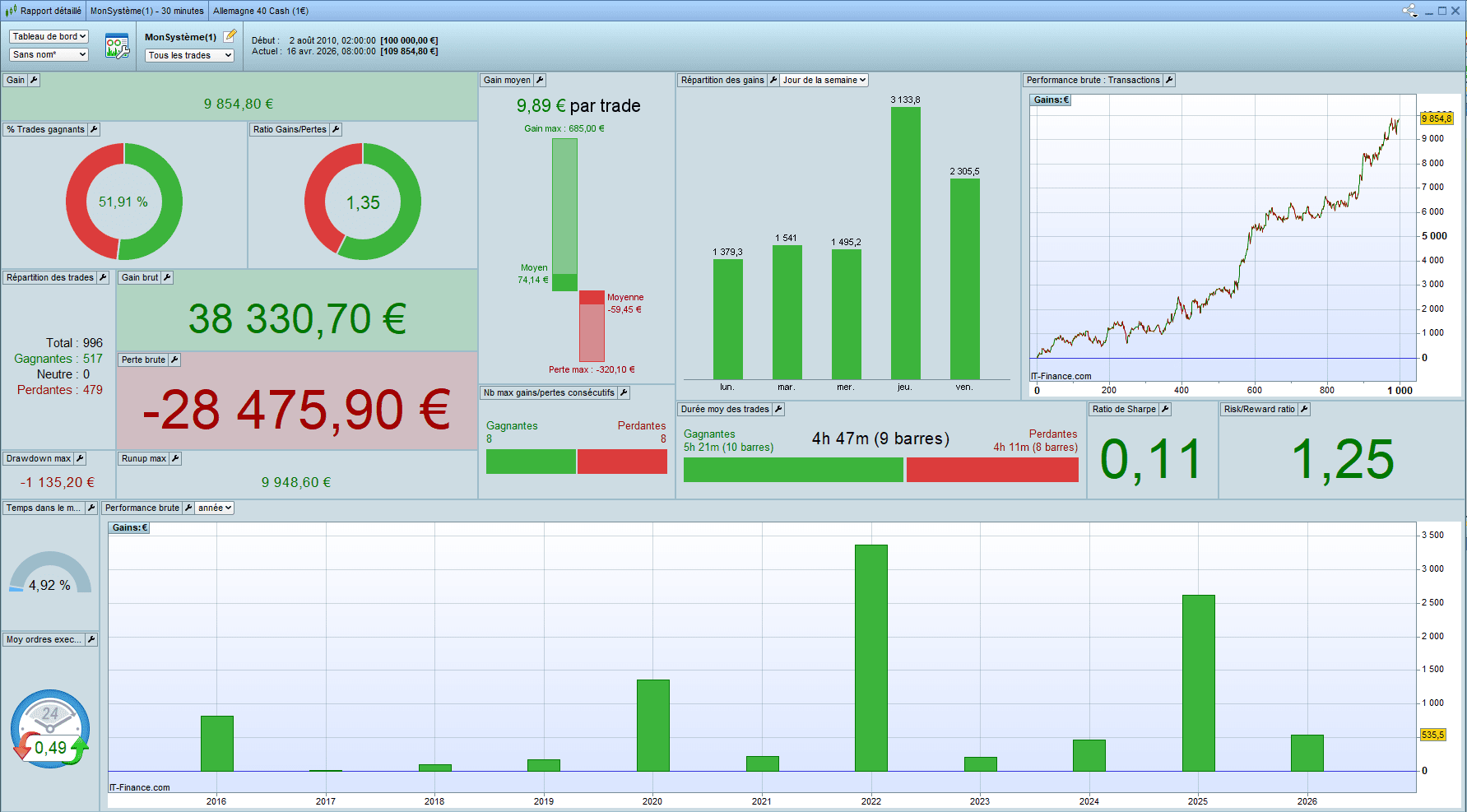

C’est un stratégie très simple qui fonctionne en 30 minutes sur le DAX40 (backtest sur PRT via IG avec 1 million d’unités).

Je précise que je ne suis pas du tout satisfait de la stratégie. Elle me semble bien trop optimisée et trop fébrile pour être lancé en réel. Cependant cela peut constituer une base de travail intéressante. n’hésitez pas à vous l’appropriez et à l’améliorer.

Je la poste ici afin tout le monde puisse en profiter l’améliorer le cas échéant.

@nicolas @robertogozzi @fbolsa si vous le souhaitez je peux publier cette stratégie dans la libraire. As you wish 😉

// DAX 30MIN

DEFPARAM flatbefore = 090000

DEFPARAM flatafter = 173000

DEFPARAM CumulateOrders = False

//Filtre de tendance

timeframe(4 hours)

filtre= Supertrend[3,10]

if close>filtre then

tendance=1

else

tendance=-1

endif

timeframe(30 minutes)

//Paramètres

atrPeriod = 2

multipleatr=2

riskMult = 0.5

tpMult = 0.5

// Keltner

myATR = AverageTrueRange[atrPeriod](close)

ema20=ExponentialAverage[50](close)

Ksup=ema20+multipleatr*myATR

Kinf=ema20-multipleatr*myATR

//Volume

vol=Volume

smavol=Average[20](vol)

//Condition volatilité

condvol=vol>smavol

//Condition d'entrée en position

condachat=close crosses over Ksup

condvente=close crosses under Kinf

//Prises de positions

IF condachat and condvol and tendance=1 THEN

BUY 1 CONTRACT AT MARKET

ENDIF

IF condvente and condvol and tendance=-1 THEN

SELLSHORT 1 CONTRACT AT MARKET

ENDIF

//Sorties sur rentournement

IF LongOnMarket AND close<ema20 THEN

SELL AT MARKET

ENDIF

IF ShortOnMarket AND close>ema20 THEN

EXITSHORT AT MARKET

ENDIF

// SL et TP initiaux

IF LongOnMarket THEN

SET STOP LOSS (tradeprice - riskMult * myATR)

SET TARGET PROFIT (tradeprice + tpMult * myATR)

ENDIF

IF ShortOnMarket THEN

SET STOP LOSS (tradeprice + riskMult * myATR)

SET TARGET PROFIT (tradeprice - tpMult * myATR)

ENDIF

Je viens de me rendre compte que j’ai testé avec un spread de 1, or nous sommes à 2 aujourd’hui avec IG sur le DAX. Cela change légèrement les résultats mais ça reste sympa visuellement.

Merci turame, en effet pour être au range de “master”, il faut avoir de la bouteille sur le site 🙂 (présent depuis 2017 ! merci pour ta présence).

En analysant ton code, je vois un problème de “taille”, si je peux m’exprimer ainsi, en effet:

// SL et TP initiaux

IF LongOnMarket THEN

SET STOP LOSS (tradeprice - riskMult * myATR)

SET TARGET PROFIT (tradeprice + tpMult * myATR)

ENDIF

IF ShortOnMarket THEN

SET STOP LOSS (tradeprice + riskMult * myATR)

SET TARGET PROFIT (tradeprice - tpMult * myATR)

ENDIF

tu utilises des niveaux de prix, alors que ces instructions attendent des distances, soit une fraction du prix. Il faut plutôt utiliser les instructions SET STOP PRICE et SET TARGET PRICE, comme ceci:

// SL et TP initiaux

IF LongOnMarket THEN

SET STOP PRICE (tradeprice - riskMult * myATR)

SET TARGET PRICE (tradeprice + tpMult * myATR)

ENDIF

IF ShortOnMarket THEN

SET STOP PRICE (tradeprice + riskMult * myATR)

SET TARGET PRICE (tradeprice - tpMult * myATR)

ENDIF

Malheureusement, je pense que cela aura un impact fort sur les résultats, à tester !

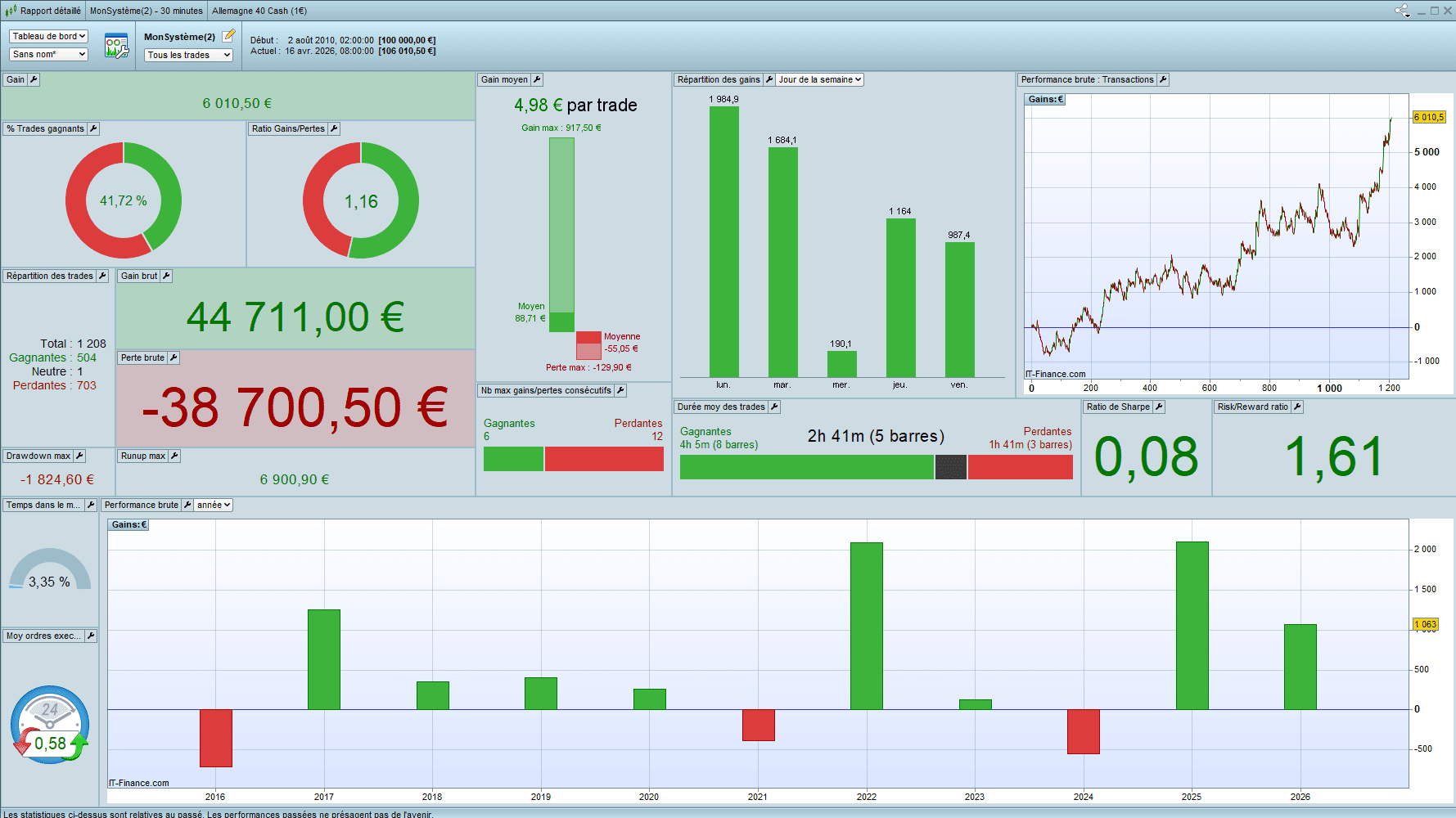

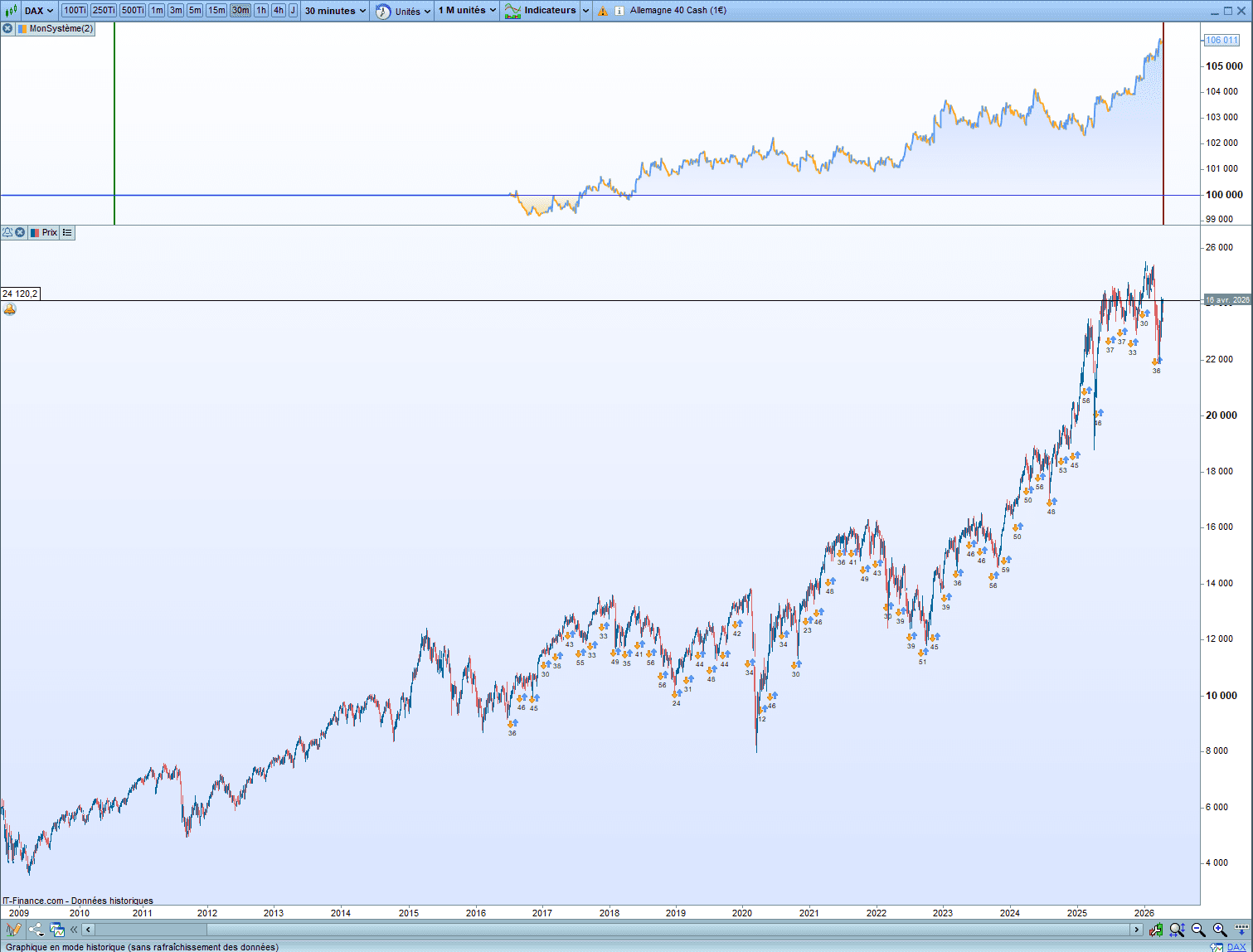

Bien vu @nicolas ! Mais je n’ai pas dis mon dernier mot. J’ai une autre version. les conditions d’entrées sont les mêmes, seul le money management change. Je l’ai fais très vite, il y a probablement des erreurs. Voici la version et les résultats :

// DAX 30MIN

DEFPARAM flatbefore = 090000

DEFPARAM flatafter = 173000

DEFPARAM CumulateOrders = False

//Filtre de tendance

timeframe(4 hours)

filtre= Supertrend[3,10]

if close>filtre then

tendance=1

else

tendance=-1

endif

timeframe(30 minutes)

//Money Management

capitalinitial=10000

risque=0.5

exitstrategy=1

profitfactor=6

stopfactor=1.5

partialprofit=1

partialprofitfactor=3

ratchetfactor=7

//Paramètres

atrPeriod = 2

multipleatr=2

riskMult = 0.5

tpMult = 0.5

// Keltner

myATR = AverageTrueRange[atrPeriod](close)

ema20=ExponentialAverage[50](close)

Ksup=ema20+multipleatr*myATR

Kinf=ema20-multipleatr*myATR

//Volume

vol=Volume

smavol=Average[20](vol)

//Condition volatilité

condvol=vol>smavol

//Condition d'entrée en position

condachat=close crosses over Ksup

condvente=close crosses under Kinf

//Positions achats

IF condachat and condvol and tendance=1 THEN

positionsize=round(((capitalinitial+STRATEGYPROFIT)*(risque/100))/(stopfactor*averagetruerange[20]))

buy positionsize shares at market

set stop loss stopfactor*averagetruerange[20]

if exitstrategy=0 THEN

set target profit profitfactor*averagetruerange[20]

ENDIF

flag=0

ENDIF

if LONGONMARKET and close>Ksup+partialprofitfactor*averagetruerange[20] and flag=0 and partialprofit=1 THEN

sell round(positionsize/2) shares at market

flag=1

ENDIF

if LONGONMARKET and exitstrategy=1 and close<lowest[30](highest[55](high)-ratchetfactor*averagetruerange[20]) THEN

sell at market

ENDIF

//Positions ventes

IF condvente and condvol and tendance=-1 THEN

positionsize=round(((capitalinitial+STRATEGYPROFIT)*(risque/100))/(stopfactor*averagetruerange[20]))

sellshort positionsize shares at market

set stop loss stopfactor*averagetruerange[20]

if exitstrategy=0 THEN

set target profit profitfactor*averagetruerange[20]

ENDIF

flag=0

ENDIF

if SHORTONMARKET and close<Kinf-partialprofitfactor*averagetruerange[20] and flag=0 and partialprofit=1 THEN

exitshort round(positionsize/2) shares at market

flag=1

ENDIF

if SHORTONMARKET and exitstrategy=1 and close>highest[30](lowest[55](low)+ratchetfactor*averagetruerange[20]) THEN

exitshort at market

ENDIF

Si tu utilises le timeframe 4-heures pour ton supertrend comme ceci :

timeframe(4 hours)

tu utilises la valeur du supertrend à chaque évaluation du timeframe le plus petit du code, soit le 30-minutes, puisque tu as:

timeframe(30 minutes)

à la ligne 16.

Donc la valeur du Supertrend sera celle non clôturée, par exemple à 14h30, 15h00, 15h30, 16h00, 16h30, 17h00, 17h30 .. au lieu d’utiliser celle fixé par la bougie de 14h00 ! Je ne sais pas si c’est volontaire, toutefois pour utiliser la valeur fixe, faire plutôt:

timeframe(4 hours, updateonclose)

Oui c’est volontaire. Lorsque je backtest une stratégie, je test toujours avec les 2 possibilités (avec et sans updateonclose). Parfois cela permet d’améliorer considérablement les résultats.

Ce n’est pas une stratégie en or loin de là, mais je suis persuadé que des personnes arriverons à en faire quelque chose de bien.