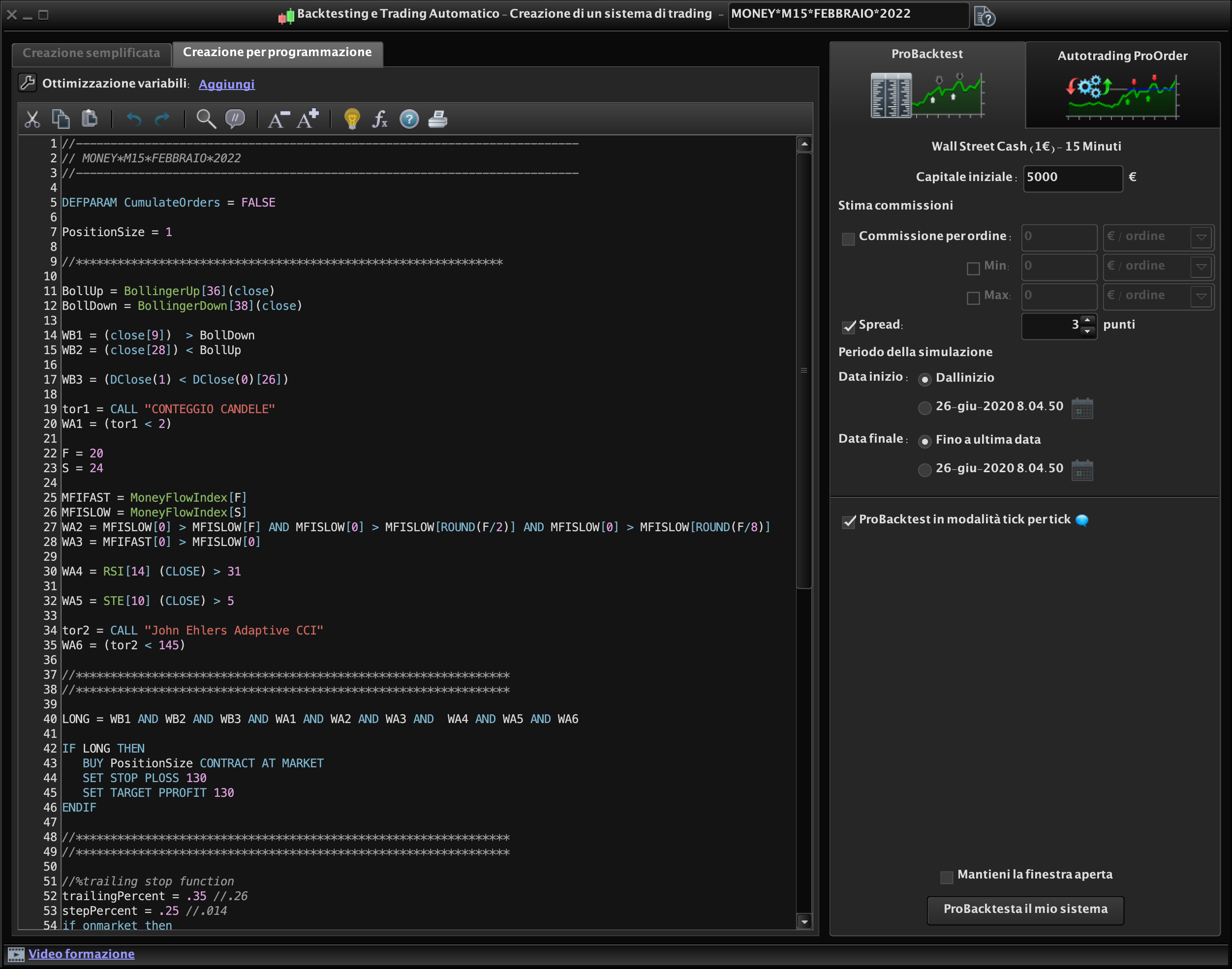

//-------------------------------------------------------------------------

// MONEY*M15*FEBBRAIO*2022

//-------------------------------------------------------------------------

DEFPARAM CumulateOrders = FALSE

PositionSize = 1

//**************************************************************

BollUp = BollingerUp[36](close)

BollDown = BollingerDown[38](close)

WB1 = (close[9]) > BollDown

WB2 = (close[28]) < BollUp

WB3 = (DClose(1) < DClose(0)[26])

tor1 = CALL "CONTEGGIO CANDELE"

WA1 = (tor1 < 2)

F = 20

S = 24

MFIFAST = MoneyFlowIndex[F]

MFISLOW = MoneyFlowIndex[S]

WA2 = MFISLOW[0] > MFISLOW[F] AND MFISLOW[0] > MFISLOW[ROUND(F/2)] AND MFISLOW[0] > MFISLOW[ROUND(F/8)]

WA3 = MFIFAST[0] > MFISLOW[0]

WA4 = RSI[14] (CLOSE) > 31

WA5 = STE[10] (CLOSE) > 5

tor2 = CALL "John Ehlers Adaptive CCI"

WA6 = (tor2 < 145)

//***************************************************************

//***************************************************************

LONG = WB1 AND WB2 AND WB3 AND WA1 AND WA2 AND WA3 AND WA4 AND WA5 AND WA6

IF LONG THEN

BUY PositionSize CONTRACT AT MARKET

SET STOP PLOSS 130

SET TARGET PPROFIT 130

ENDIF

//***************************************************************

//***************************************************************

//%trailing stop function

trailingPercent = .35 //.26

stepPercent = .25 //.014

if onmarket then

trailingstart = tradeprice(1)*(trailingpercent/100) //trailing will start @trailingstart points profit

trailingstep = tradeprice(1)*(stepPercent/100) //% step to move the stoploss

endif

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart THEN

newSL = tradeprice(1)+trailingstep

ENDIF

//next moves

IF newSL>0 AND close-newSL>trailingstep THEN

newSL = newSL+trailingstep

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart THEN

newSL = tradeprice(1)-trailingstep

ENDIF

//next moves

IF newSL>0 AND newSL-close>trailingstep THEN

newSL = newSL-trailingstep

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

Grazie Fabiano, potresti spiegarci come hai sviluppato la strategia? Dovresti anche condividere il codice ITF della strategia per consentire alle persone di ottenere gli indicatori necessari che stai utilizzando con CALL.

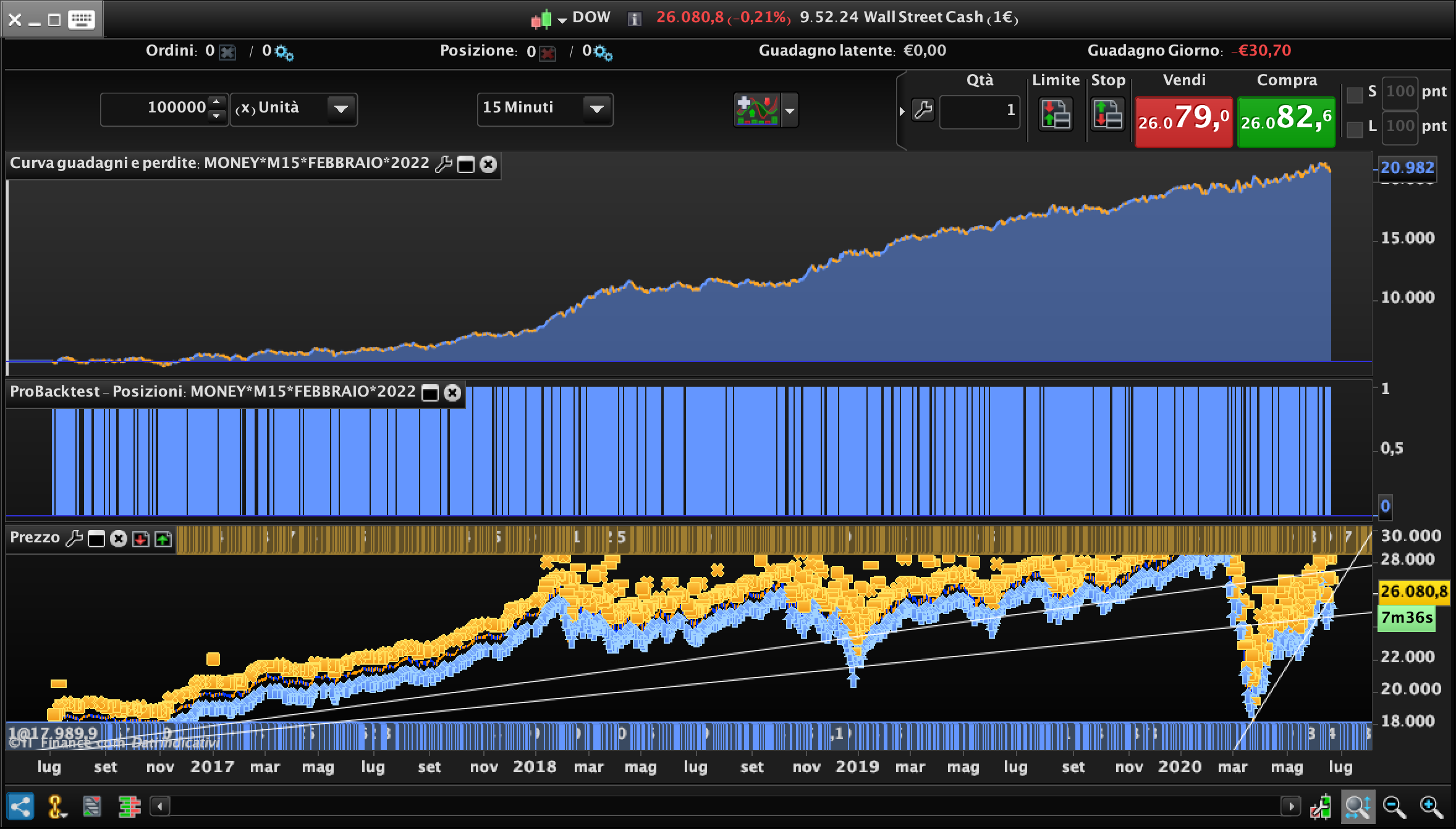

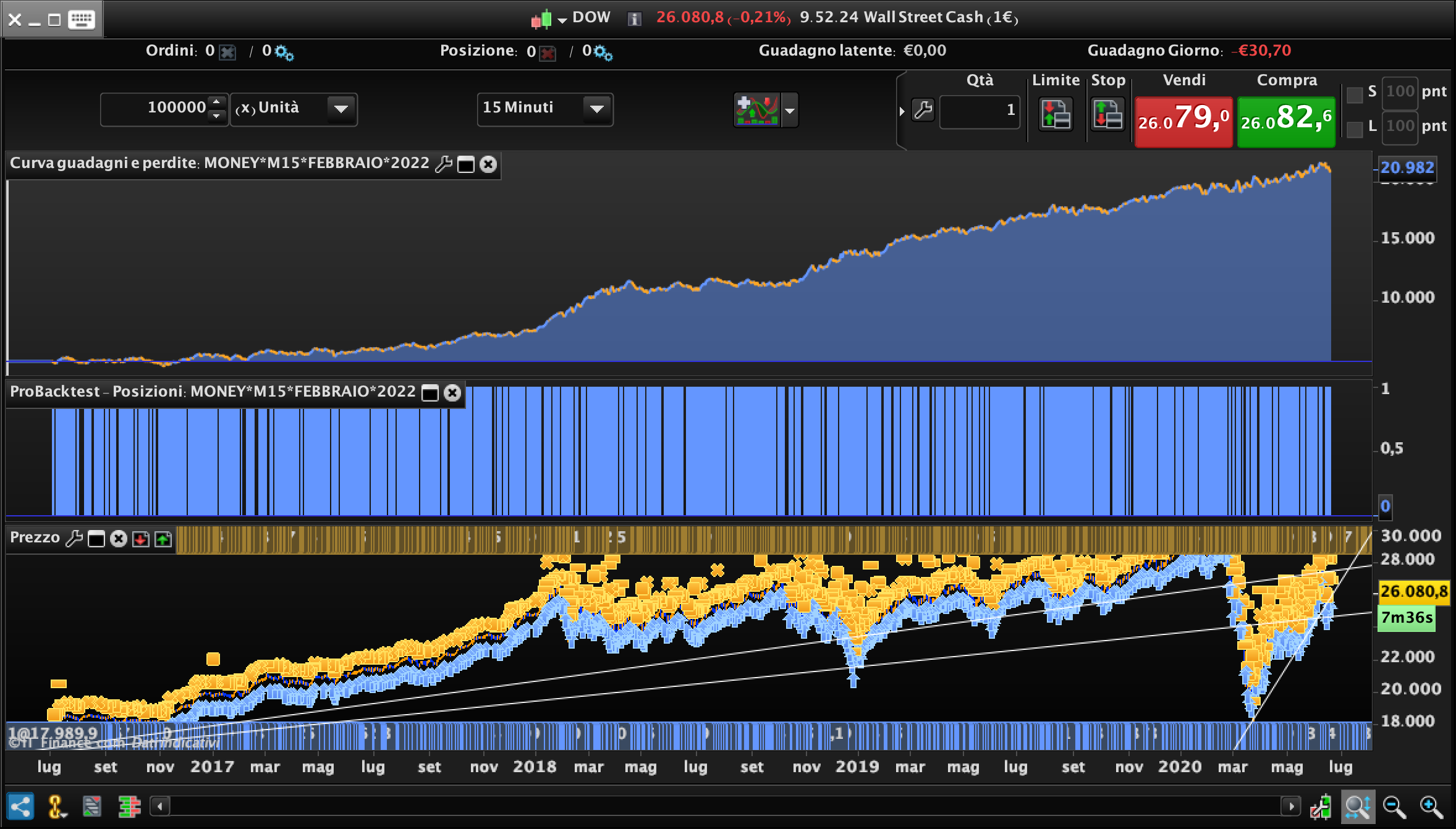

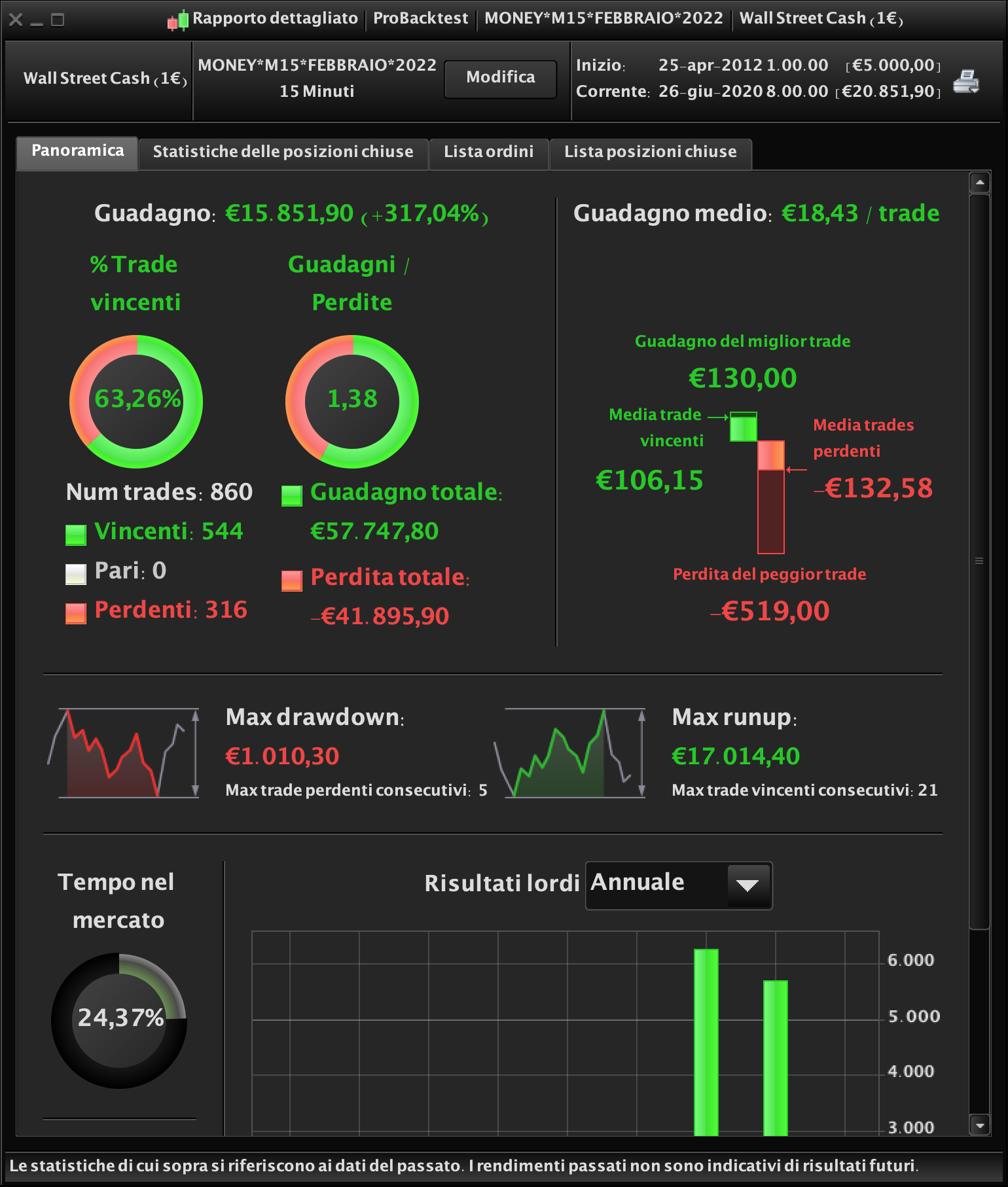

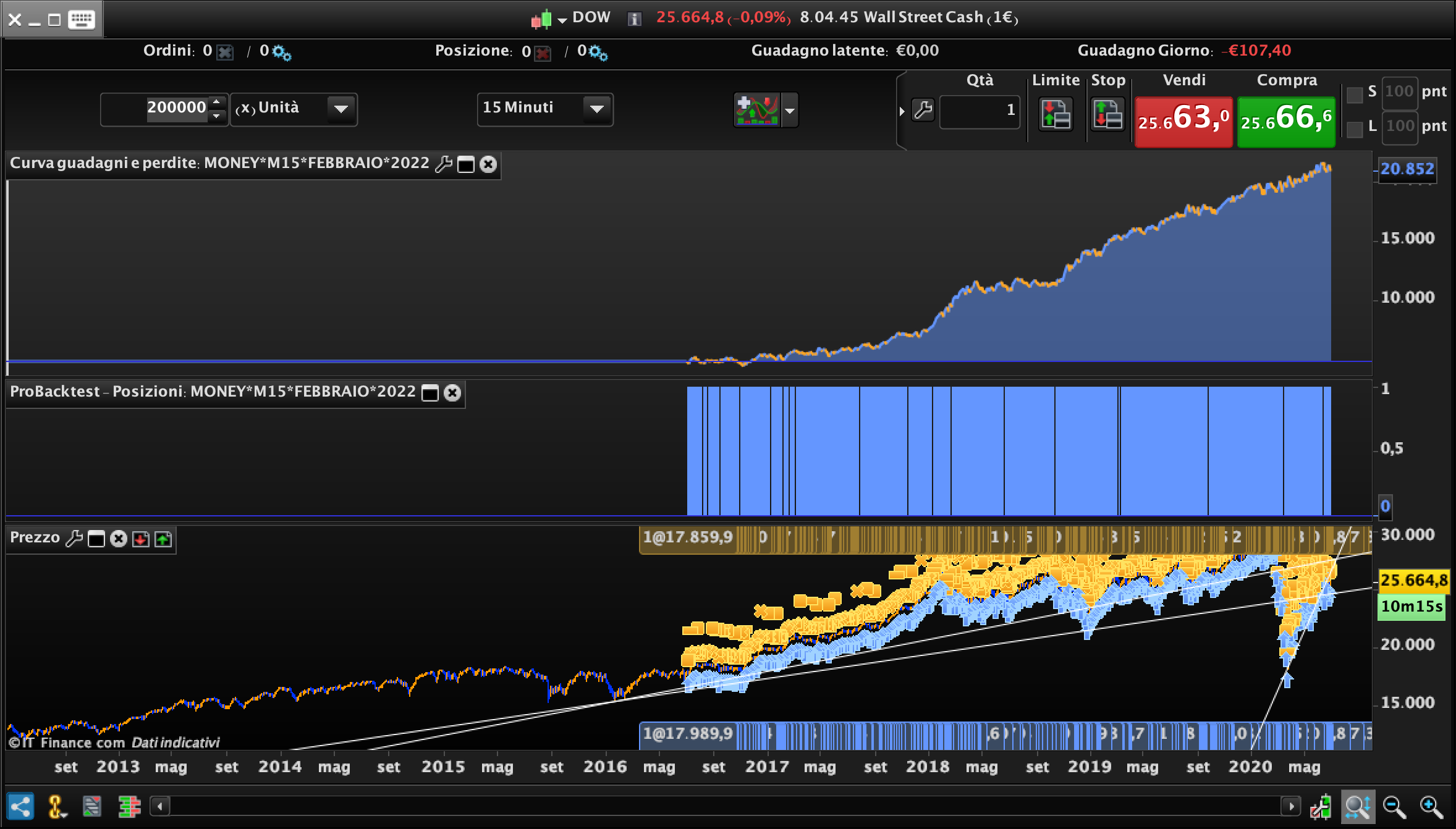

Buongiorno, allego i file .itf delle CALL utilizzate, la strategia è stata pensata per cercare… di prendere una partenza di un trend in long, ho testato tutti i parametri cercando di fare il meglio che mi riesce, con le mie poche conoscenze di programmazione.

Spero si possa implementare e sia utile…anche se vedo zero interesse per la strategia.

Grazie a TE Nicolas e a tutti quelli che aiutano in questo forum, Francesco, Grahal, Vonasi, Roberto Gozzi, Fifi, ecc….

Ciao Fabiano,

Grazie per aver condiviso la strategia, mi sembra ben fatta anche se esistono i rischi di solo due anni di statistica.

Potresti inserire un orario di trading iniziale e uno finale tipo questo.

timel = time >= 090000 and time <= 200000

Hai giustamente usato un trailing stop in percentuale, forse sarebbe meglio usare anche uno stop in percentuale per meglio adattarsi al valore del DOW J.

Per il target io userei un sistema che si adatta alla volatilità del momento tipo questo.

5* averagetruerange[10](close)

A volte uso anche un numero massimo di barre dove essere a mercato.

ONCE maxCandlesLongWithProfit = 185

ONCE maxCandlesLongWithoutProfit = 185

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

numberCandles = (BarIndex - TradeIndex)

m1 = posProfit > 0 AND numberCandles >= maxCandlesLongWithProfit

m3 = posProfit < 0 AND numberCandles >= maxCandlesLongWithoutProfit

IF LONGONMARKET AND (m1 OR m3) THEN

SELL AT MARKET

ENDIF

Fai delle prove e vedi come va……ma ricordati di metterlo prima in demo per un po di mesi per vedere se non è troppo ottimizato.

Ciao buona giornata.