Hi trader! I have a problem i can´t solve properly. I would like to set different values for stopploss /profit when going long and use antoher value when im short! And not have same value for both long and short!

I also use trailing stop and breakeven.

I hope if anyone can help and tell me why its not working properly?

Best regards

//Entry en position

//POSITION LONG

IF CONDBUY THEN

buy positionsize contract at market

SET STOP %LOSS 2.6 // i Want different value here for long??

SET STOP PLOSS 102 // i Want different value here for long??

ENDIF

//POSITION SHORT

IF CONDSELL THEN

Sellshort positionsize contract at market

SET STOP %LOSS 0.6 // i Want different value here for short??

SET STOP PLOSS 45 // i Want different value here for short??

ENDIF

SET STOP PLOSS 100 // I dont get same result even if i put same value in both long/short

SET TARGET %PROFIT 2.8 // I dont get same result even if i put same value in both long/short

//--------------------------------------------------------------------------------------------------------------------------------------------------

// Trailingstop

IF Not OnMarket THEN

//

// when NOT OnMarket reset values to default values

//

TrailStart = 15 // 15=85%...62=61% Start trailing profits from this point

BasePerCent = 0.04 // Profit percentage to keep when setting BerakEven

StepSize = 7 // 15/7= 86%win- Pip chunks to increase Percentage

PerCentInc = 0.100 //10.0% PerCent increment after each StepSize chunk

RoundTO = -0.5 //-0.5 rounds always to Lower integer, +0.4 rounds always to Higher integer, 0

Barnumber = 52 // 20

Barpercent = 0 //0.2 // 20%

PriceDistance = 7 * pipsize

y1 = 0

y2 = 0

etc

etc

Simply remove lines 17-18.

Pellejons – Please pay attention to where you post your topics. Your topic has been moved to the correct forum as described in the forum rules.

Post your topic in the correct forum:

_ ProRealTime Platform Support: only platform related issues.

_ ProOrder: only strategy topics.

_ ProBuilder: only indicator topics.

_ ProScreener: only screener topics

_ General Discussion: any other topics.

_ Welcome New Members: for new forum members to introduce themselves.

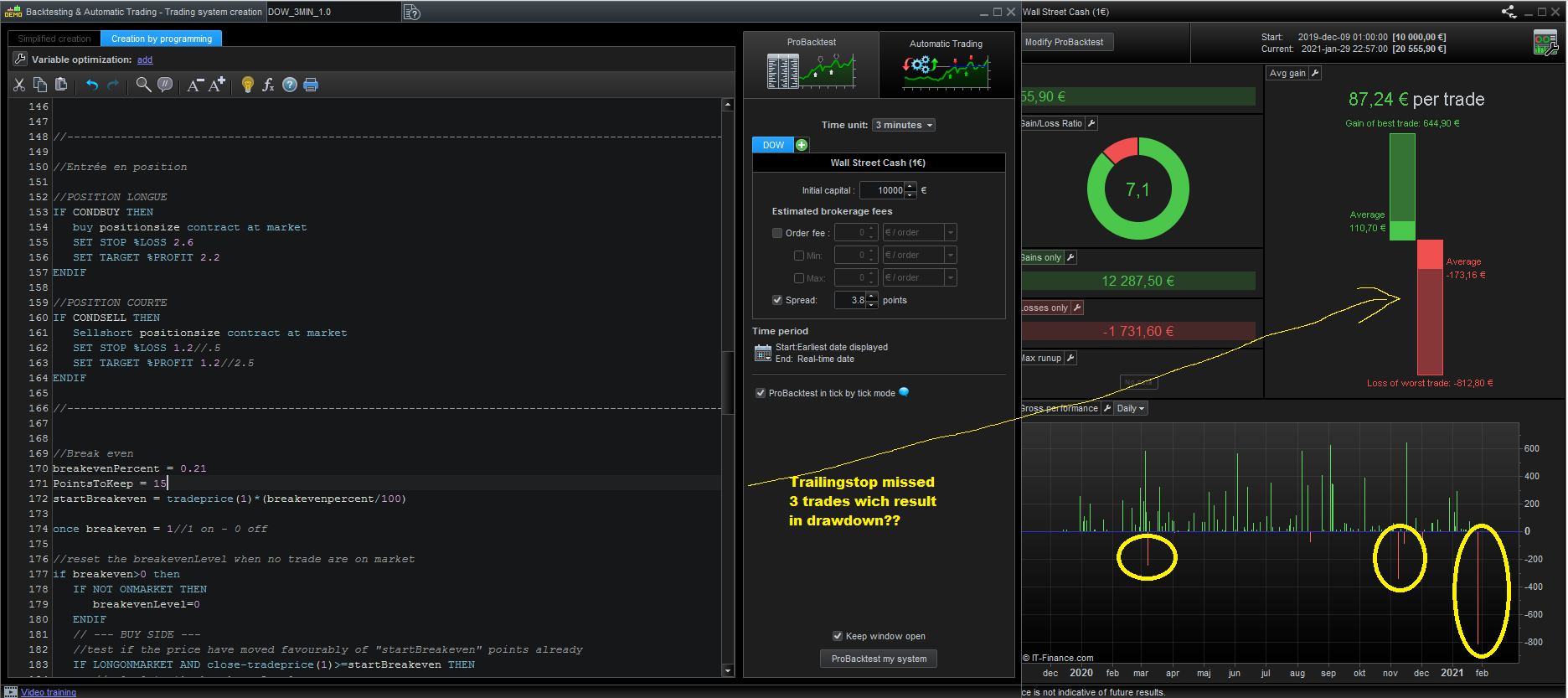

I explain myself bad. I have tested a lot of times now. It seems to be a error in trailingstop code or platform it self that occurs 3 times at 200k bars where it lets through and lets the price go down to set stop %loss.

There will be some maxdraw losses I want to avoid.

The question is whether there is another code that can back up and catch what the trailing top misses? or other way to fix it?

Best regards!

To be able to help you we need to recreate exactly the same trades.

To help us, please:

- post the full working code

- tell us the date & time of entry of the trade(s) that produced unexpected results.

At present we only know you are trading Wall Street Cash (1€) on a 3-minute TF.

DEFPARAM CumulateOrders = false

DEFPARAM Preloadbars = 50000

positionsize=1

Ctime = time >= 140000 and time < 221400//Euro time

ONCE PeriodeA = 4

ONCE nbChandelierA= 30

MMA = Exponentialaverage[PeriodeA](close)

ADJASUROPPO = (MMA-MMA[nbchandelierA]) / nbChandelierA

ANGLE = (ATAN(ADJASUROPPO)) //FONCTION ARC TANGENTE

CB1 = ANGLE >= 34

CS1 = ANGLE <= - 48

//VECTEUR = CALCUL DE LA PENTE ET SA MOYENNE MOBILE

ONCE PeriodeB = 30

ONCE nbChandelierB= 35

lag = 0

MMB = Exponentialaverage[PeriodeB](close)

pente = (MMB-MMB[nbchandelierB]) / nbchandelierB

trigger = Exponentialaverage[PeriodeB+lag](pente)

CB2 = (pente > trigger) AND (pente < 0)

CS2 = (pente CROSSES UNDER trigger) AND (pente > - 0.5)

mx = average[54,0](close)

CB3 = mx > mx[1]

mx2 = average[21,6](close)

CS3 = mx2 < mx2[1]

//------------------------------------------

lengthRSI = 25 //RSI period

lengthStoch = 20 //Stochastic period

smoothK = 12 //Smooth signal of stochastic RSI

smoothD = 2 //Smooth signal of smoothed stochastic RSI

myRSI = RSI[lengthRSI](close)

MinRSI = lowest[lengthStoch](myrsi)

MaxRSI = highest[lengthStoch](myrsi)

StochRSI = (myRSI-MinRSI) / (MaxRSI-MinRSI)

K = average[smoothK](stochrsi)*100

D = average[smoothD](K)

cb4 = K>D

cs4 = K<D

//--------------------------------------------

Tenkan = (highest[9](high)+lowest[9](low))/2

Kijun = (highest[26](high)+lowest[26](low))/2

SSpanA = (tenkan[26]+kijun[26])/2

SSpanB = (highest[52](high[26])+lowest[52](low[26]))/2

If SSpanA>SSpanB then

if open<SSpanA and open>SSpanB or close<SSpanA and close>SSpanB then

CondIchi = 0

Else

CondIchi = 1

endif

endif

If SSpanB>SSpanA then

if open>SSpanA and open<SSpanB or close>SSpanA and close<SSpanB then

CondIchi = 0

Else

CondIchi = 1

endif

endif

CONDBUY = CB1 and CB2 and CB3 and cb4 and CTime and CondIchi

CONDSELL = CS1 and CS2 and CS3 and cs4 and Ctime and CondIchi

VarDistIchiBuy = 6

VarDistIchiSell = 21

If CONDBUY then

DistIchiSSA = Open - SSpanA

DistIchiSSB = Open - SSpanB

CondDistIchi = DistIchiSSA >= VarDistIchiBuy AND DistIchiSSB >= VarDistIchiBuy

Endif

If CONDSELL then

DistIchiSSA = SSpanA - Open

DistIchiSSB = SSpanB - Open

CondDistIchi = DistIchiSSA >= VarDistIchiSell AND DistIchiSSB >= VarDistIchiSell

Endif

CONDBUY = CONDBUY and CondDistIchi

CONDSELL = CONDSELL and CondDistIchi

//--------------------------------------------------------------------------------------------------------------------------------------------------

//Entry en position

//POSITION LONG

IF CONDBUY THEN

buy positionsize contract at market

SET STOP %LOSS 2.6

SET TARGET %PROFIT 2.2

ENDIF

//POSITION SHORT

IF CONDSELL THEN

Sellshort positionsize contract at market

SET STOP %LOSS 1.2//.5

SET TARGET %PROFIT 1.2//2.5

ENDIF

//Break even

breakevenPercent = 0.21

PointsToKeep = 5

startBreakeven = tradeprice(1)*(breakevenpercent/100)

once breakeven = 1//1 on - 0 off

//reset the breakevenLevel when no trade are on market

if breakeven>0 then

IF NOT ONMARKET THEN

breakevenLevel=0

ENDIF

// --- BUY SIDE ---

//test if the price have moved favourably of "startBreakeven" points already

IF LONGONMARKET AND close-tradeprice(1)>=startBreakeven THEN

//calculate the breakevenLevel

breakevenLevel = tradeprice(1)+PointsToKeep

ENDIF

//place the new stop orders on market at breakevenLevel

IF breakevenLevel>0 THEN

SELL AT breakevenLevel STOP

ENDIF

// --- end of BUY SIDE ---

IF SHORTONMARKET AND tradeprice(1)-close>startBreakeven THEN

//calculate the breakevenLevel

breakevenLevel = tradeprice(1)-PointsToKeep

ENDIF

//place the new stop orders on market at breakevenLevel

IF breakevenLevel>0 THEN

EXITSHORT AT breakevenLevel STOP

ENDIF

endif

// trailing atr stop

once trailingstoptype = 1 // trailing stop - 0 off, 1 on

once tsincrements = .05 // set to 0 to ignore tsincrements

once tsminatrdist = 7

once tsatrperiod = 18 // ts atr parameter

once tsminstop = 12 // ts minimum stop distance

once tssensitivity = 1 // [0]close;[1]high/low

if trailingstoptype then

if barindex=tradeindex then

trailingstoplong = 3 // ts atr distance

trailingstopshort = 3 // ts atr distance

else

if longonmarket then

if tsnewsl>0 then

if trailingstoplong>tsminatrdist then

if tsnewsl>tsnewsl[1] then

trailingstoplong=trailingstoplong

else

trailingstoplong=trailingstoplong-tsincrements

endif

else

trailingstoplong=tsminatrdist

endif

endif

endif

if shortonmarket then

if tsnewsl>0 then

if trailingstopshort>tsminatrdist then

if tsnewsl<tsnewsl[1] then

trailingstopshort=trailingstopshort

else

trailingstopshort=trailingstopshort-tsincrements

endif

else

trailingstopshort=tsminatrdist

endif

endif

endif

endif

tsatr=averagetruerange[tsatrperiod]((close/8.8))/1000

//tsatr=averagetruerange[tsatrperiod]((close/1)) // (forex)

tgl=round(tsatr*trailingstoplong)

tgs=round(tsatr*trailingstopshort)

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

tsmaxprice=0

tsminprice=close

tsnewsl=0

endif

if tssensitivity then

tssensitivitylong=high

tssensitivityshort=low

else

tssensitivitylong=close

tssensitivityshort=close

endif

if longonmarket then

tsmaxprice=max(tsmaxprice,tssensitivitylong)

if tsmaxprice-tradeprice(1)>=tgl*pointsize then

if tsmaxprice-tradeprice(1)>=tsminstop then

tsnewsl=tsmaxprice-tgl*pointsize

else

tsnewsl=tsmaxprice-tsminstop*pointsize

endif

endif

endif

if shortonmarket then

tsminprice=min(tsminprice,tssensitivityshort)

if tradeprice(1)-tsminprice>=tgs*pointsize then

if tradeprice(1)-tsminprice>=tsminstop then

tsnewsl=tsminprice+tgs*pointsize

else

tsnewsl=tsminprice+tsminstop*pointsize

endif

endif

endif

if longonmarket then

if tsnewsl>0 then

sell at tsnewsl stop

endif

if tsnewsl>0 then

if low crosses under tsnewsl then

sell at market // when stop is rejected

endif

endif

endif

if shortonmarket then

if tsnewsl>0 then

exitshort at tsnewsl stop

endif

if tsnewsl>0 then

if high crosses over tsnewsl then

exitshort at market // when stop is rejected

endif

endif

endif

endif

if onmarket then

if dayofweek=0 and (hour=0 and minute>=57) and abs(dopen(0)-dclose(1))>50 and positionperf(0)>0 then

if shortonmarket and close>dopen(0) then

exitshort at market

endif

if longonmarket and close<dopen(0) then

sell at market

endif

endif

endif

I have tried different trailing script .But it same result it let 3-6 long trades through the trailingscripts and hit at last set stop loss… Thats strange!?

Feb 21 2020

Mar 17 2020

Jun 19 2020

I think its more! But those 3 are obvious..