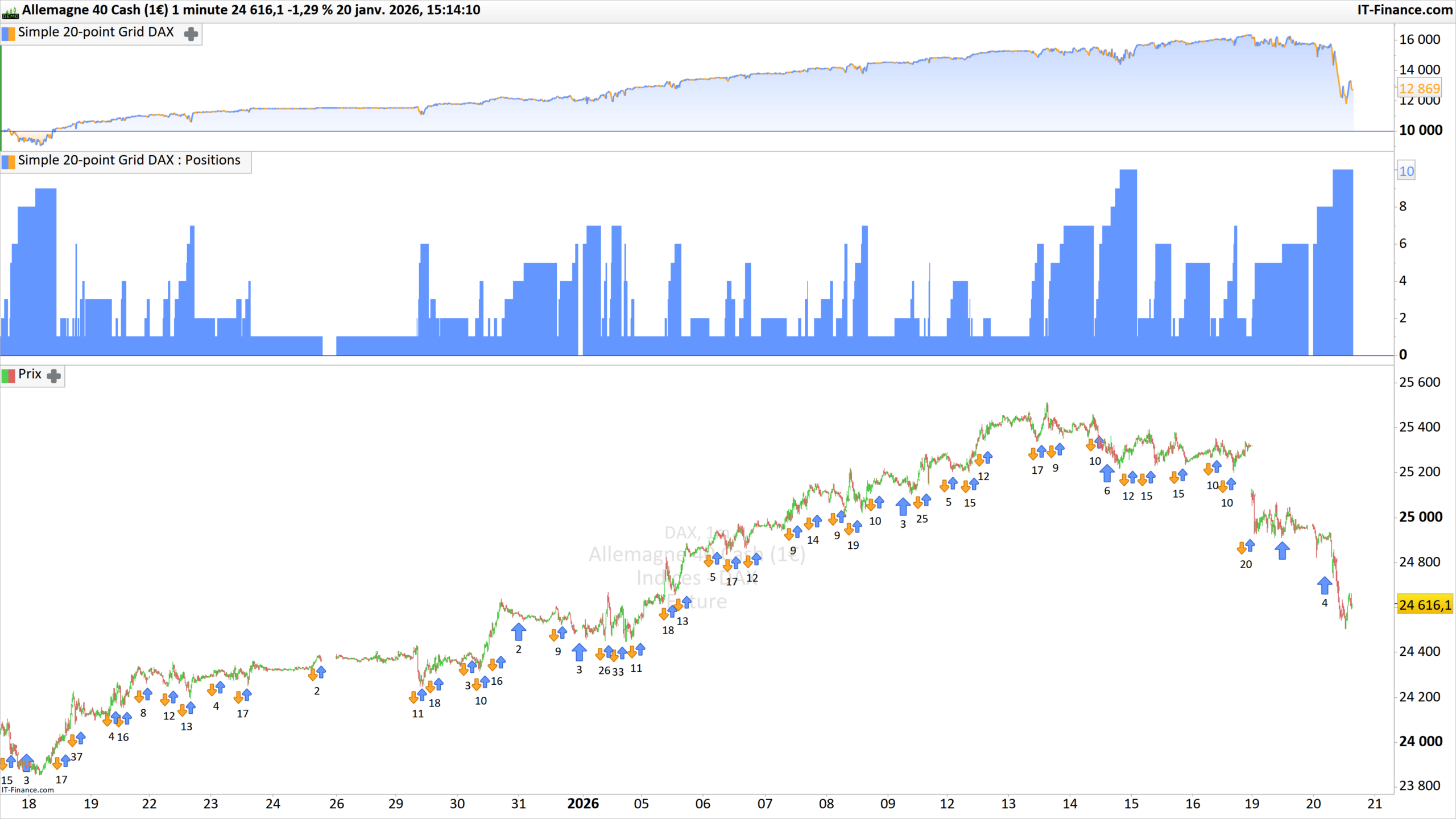

I am sharing a raw grid code I used on the DAX m1 timeframe during the last bullish leg.

The logic is stupidly simple: It buys 1 contract every time price drops by 20 points from the last trade price. It closes everything when the total profit reaches a fixed target (Global Target).

I know grids are dangerous, but if you run this only during US market hours and cut it before the close, it acts as a liquidity provider.

Be careful with the leverage, on the DAX it can go fast. I set the max positions to 10 to avoid blowing the account.

// --------------------------------------------------------

// Strategy: Simple Accumulation Grid (Long Only)

// Asset: DAX / Indices

// Risk: HIGH - No Stop Loss per trade

// --------------------------------------------------------

DEFPARAM CumulateOrders = True // Essential for Grid

// Settings

GridStep = 20 // Distance between buys

TakeProfitPoints = 50 // Target in points (Global)

MaxPositions = 10 // Safety limit

// Entry Logic

IF Not OnMarket THEN

BUY 1 CONTRACT AT MARKET

LastEntryPrice = Close

ENDIF

// Add to Grid (Averaging Down)

IF LongOnMarket AND CountOfPosition < MaxPositions THEN

IF Close <= LastEntryPrice - GridStep THEN

BUY 1 CONTRACT AT MARKET

LastEntryPrice = Close // Update reference price

ENDIF

ENDIF

// Exit Logic (Global Profit Target)

// We calculate the average entry price of the whole stack

AvgPrice = PositionPrice

CurrentProfit = (Close - AvgPrice) * CountOfPosition

IF CurrentProfit >= (TakeProfitPoints * PointValue) THEN

SELL AT MARKET

ENDIF

It’s not too bad that the trend is clear (long only on indices)… Of course, be wary of Trump as soon as the US wakes up!

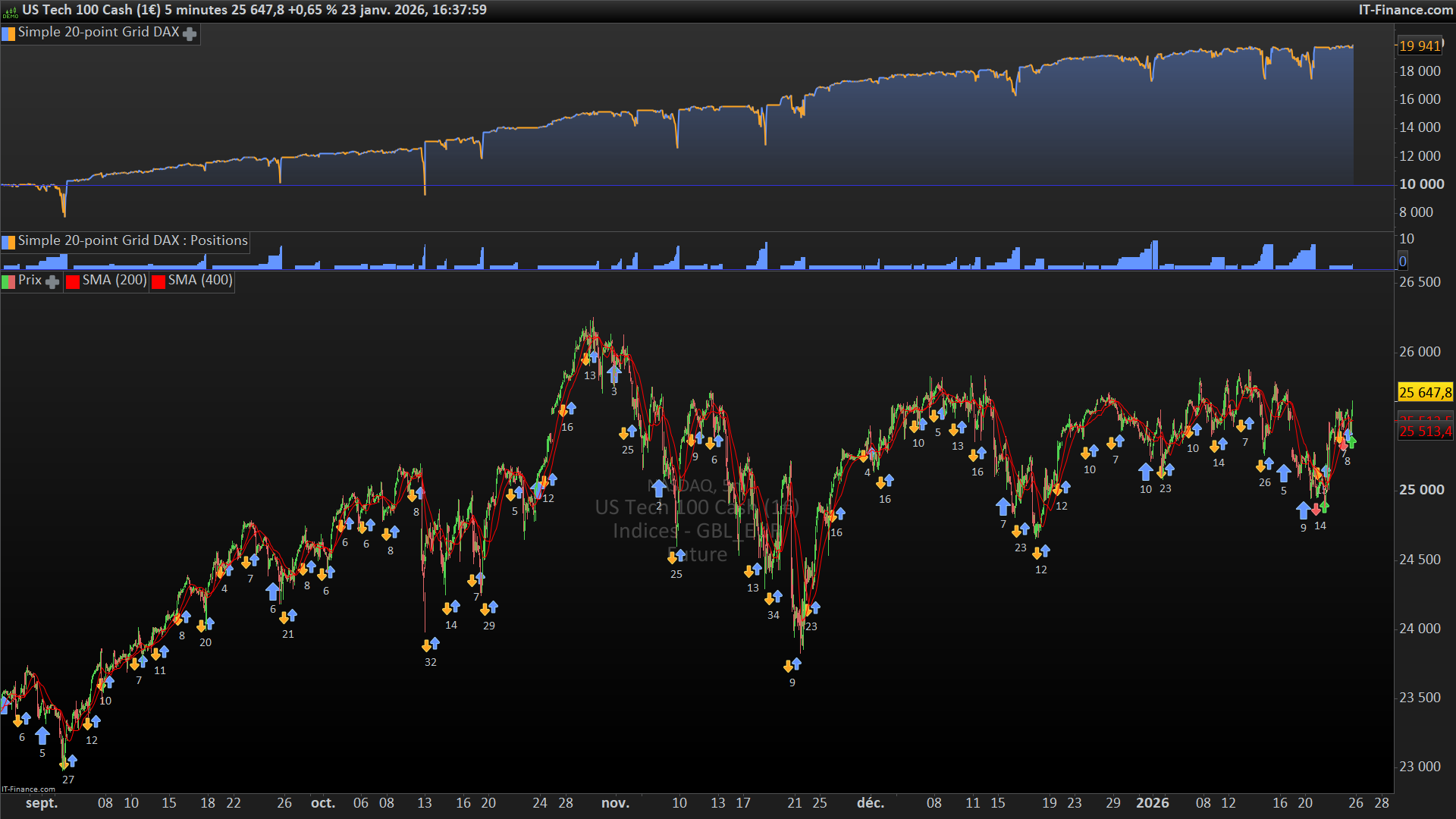

This is below another version, tested for recent NASDAQ data 5-minutes, 0.5 contracts, 1 point spread.

Added a trend filter (simple couple of long term SMA comparison) plus another exit when in profit / breakeven in grid situation.

There is a whole range of things to explore for this kind of strategies! Lots of maths and headaches, but hey we like this so much! 🙂

// --------------------------------------------------------

// Strategy: Simple Accumulation Grid (Long Only)

// Risk: HIGH - No Stop Loss per trade

// --------------------------------------------------------

DEFPARAM CumulateOrders = True // Essential for Grid

// Settings

GridStep = 20 // Distance between buys

TakeProfitPoints = 50 // Target in points (Global)

MaxPositions = 10 // Safety limit

sma1=average[200]

sma2=average[400]

uptrend = sma1>sma2

// Entry Logic

IF Not OnMarket and uptrend THEN

BUY 1 CONTRACT AT MARKET

LastEntryPrice = Close

ENDIF

// Add to Grid (Averaging Down)

IF LongOnMarket AND CountOfPosition < MaxPositions and not uptrend THEN

IF Close <= LastEntryPrice - GridStep THEN

BUY 0.5 CONTRACT AT MARKET

LastEntryPrice = Close // Update reference price

ENDIF

ENDIF

// Exit Logic (Global Profit Target)

// We calculate the average entry price of the whole stack

AvgPrice = PositionPrice

CurrentProfit = (Close - AvgPrice) * CountOfPosition

IF (CurrentProfit >= (TakeProfitPoints * PointValue)) OR (CurrentProfit>0 and countofposition>1) THEN

SELL AT MARKET

ENDIF

Good job Nicolas, as always!

Actually, I’d like to build an algo that would make 40/50 points per day on the DAX, through one or several trades, every day. Between 9:00 a.m and 5:30 p.m Either long or short.

A consistent algo, with the requirement that it takes winning trades every day and achieves those 40/50 points. Stop loss to be defined.

No grid or martingale. Just 1 lot on each trade.Let’s do it, let’s build this algo together !

@Nicolas

Would it be possible to rewrite this code so that the grid is calculated in percentages instead of pips?

@Lifen, yes! let’s do it! 😉

@phoentzs

Sure, here is below the new version with a grid step in percentage, along with a profit exit in percentage of price also.

Here is what have changed:

- GridStep (fixed pips) is replaced by GridStepPct (percentage). The trigger price for the next grid buy is now computed as LastEntryPrice * (1 – GridStepPct / 100). With a 1% step and a last entry at 100, the next buy triggers at 99, at 200 it triggers at 198, and so on. The grid automatically scales with price level.

- TakeProfitPoints (fixed points multiplied by PointValue) is replaced by TakeProfitPct. The profit is now expressed as (Close – AvgPrice) / AvgPrice * 100, which gives a pure percentage gain relative to the weighted average entry price of the whole stack. The exit fires when that percentage reaches TakeProfitPct.

- CurrentProfit (absolute currency value) is gone entirely. ProfitPct replaces it in both exit conditions, keeping everything consistent in percentage terms.

// --------------------------------------------------------

// Strategy: Simple Accumulation Grid (Long Only)

// Risk: HIGH - No Stop Loss per trade

// Grid and profit target calculated in PERCENTAGES

// --------------------------------------------------------

DEFPARAM CumulateOrders = True // Essential for Grid

// Settings

GridStepPct = 1.0 // Distance between buys in % (e.g. 1.0 = 1%)

TakeProfitPct = 2.5 // Global profit target in % of average entry price

MaxPositions = 10 // Safety limit

sma1 = average[200]

sma2 = average[400]

uptrend = sma1 > sma2

// Entry Logic

IF Not OnMarket AND uptrend THEN

BUY 1 CONTRACT AT MARKET

LastEntryPrice = Close

ENDIF

// Add to Grid (Averaging Down)

// Trigger when price drops GridStepPct% below last entry price

IF LongOnMarket AND CountOfPosition < MaxPositions AND NOT uptrend THEN

GridTriggerPrice = LastEntryPrice * (1 - GridStepPct / 100)

IF Close <= GridTriggerPrice THEN

BUY 0.5 CONTRACT AT MARKET

LastEntryPrice = Close

ENDIF

ENDIF

// Exit Logic (Global Profit Target in %)

// PositionPrice = weighted average entry price of the whole stack

AvgPrice = PositionPrice

ProfitPct = (Close - AvgPrice) / AvgPrice * 100

IF (ProfitPct >= TakeProfitPct) OR (ProfitPct > 0 AND CountOfPosition > 1) THEN

SELL AT MARKET

ENDIF

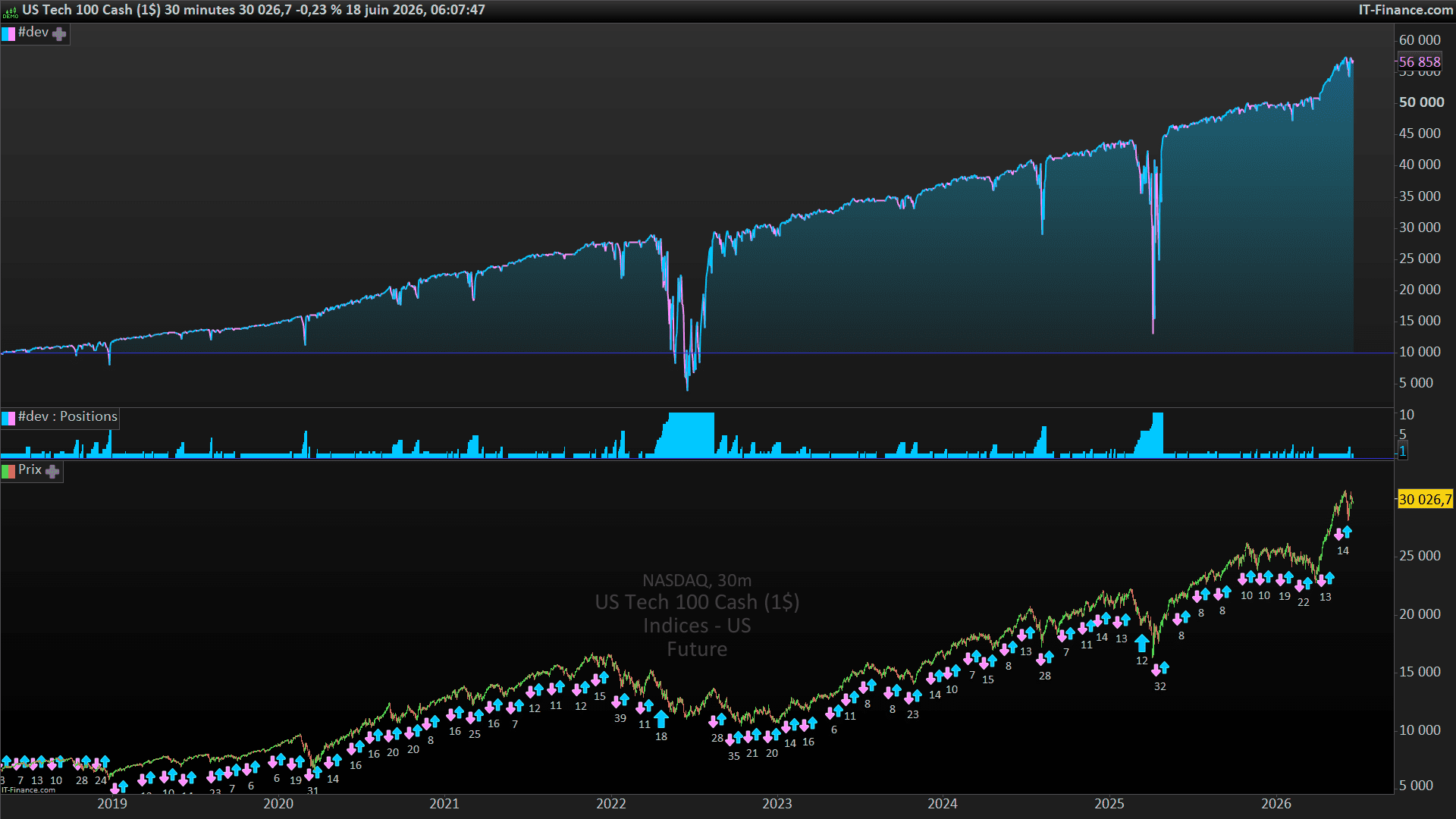

Attached is “performance” of the code for NASDAQ 30min CFD, UTC+0 with weekend data. What a ride! 40k drawdown is ugly though