Hi all, I have just joined this forum in the hope of finding strategies that work for autotrading. I previously backtested hundreds of strategies involving MACDs, EMAs, OBV & more. (Although at the time I didn’t realise I could change the timeframe, I now do it with 200k units). I found quite a few successful backtests, out about 40 bots live on various markets from S&P500 to Oil and FX. I even made a video on it: https://www.youtube.com/watch?v=VPINK8mA0Uc

After about 3 months all had failed.

I understand that generally people don’t want to share algos or they can be bought, but perhaps this thread could be to share just the combinations of indicators etc? Or maybe there is already a post on this?

I’m currently remodelling my strategies from before to include Fibonacci pivots, the momentum indicator and using trailing stops instead of clear cut exits, which seem to be having a positive effect.

Any ideas, much appreciated 😊

I think you’re overcomplicating things. Combining and optimizing numerous indicators rarely improves a strategy. If anything, it’s one indicator that makes logical sense. Find a significant advantage in the market that has persisted for many years and try to leverage and improve upon it. Just as an example… we know that the S&P 500 always has the tendency to rise. That’s the advantage. And you can use it. So, there’s a high probability.

Agree with Phoentzs. One thing you could try to fresh your mind a bit, is to throw all indicators in the bin, and just really play it super simple. Play with breakouts from dclose or dopen. Try to exit EOD (as that also saves your from lots of overnight fees) or with some basic ATR trailing stop you can find on this forum. No optimization needed, just pure simple price action can get your further than you think!

Yep, Phoenz and Snal are on the money.

If your going to use these known calculations keep it simple. My best (long term robust) bots that have run for years have less than 20 lines of code and pass the pub test, meaning they make logistical sense like Phoentz described.

Moreover, this is largely about expectations. If you’re a manual trader that has edge it can be very difficult to find a bot to perform as you may expect. I think few get that far but can be done for sure. But that is not the starting place. Unfortunately, the starting place algorithmically is to find a a 42%ish WR with a gain/loss of 1.3+. This just shows you it is possible and your process has evolved to “I now know something”. Once you find that SIMPLY (not easily) then look around and raise your expectations.

May I suggest running through your known indicators and testing them into oblivion and record that data as your own data base. Maybe this is what you have done I don’t know? Then you will have a short list of calcs you may be able to use to write a set of better than nothing bots. You might even get something decent, but won’t quite be able to live of it.

For me, once I’d done all that it was then possible to completely melt my brain by mostly throwing it all out and start to think outside the black box to where the real creativity comes in.

I’ll go one further and save you years of pain. Forget entries and exits, they come after structure and logic. Any indicator will get you acceptable entries and exits. But what is the Regime? How is the market structured for this trade? I just spent a year of looking to find a 49% D grade edge just needed the appropriate regime classification to take it to 81.5% and PF of 3 occuring twice a week. No joke.

Thanks everyone , really appreciate all your feedback and it’s given me a lot to work with. A few points…

“Unfortunately, the starting place algorithmically is to find a a 42%ish WR with a gain/loss of 1.3+.“ thanks for this, yes I’ve found quite a few over that, although sometimes number of trades is only like 10 or less, so only counting the ones over say 30 trades in the backtest, is this reasonable amount?

Thanks for the simple dclose idea, just did a quick backtest it looks promising. Although the gain/loss ratio hasn’t been great so far. But will keep trying.

“I just spent a year of looking to find a 49% D grade edge just needed the appropriate regime classification to take it to 81.5% and PF of 3 occuring twice a week. “ Apologies @ can you explain this in more basic talk, what’s a d grade edge?

The Regime side is really interesting, thanks , have a lot to learn here.

yeah I’m keeping a reasonable record of systems and going back and trying to improve them. so might publish some one day.

Buy the SP500 blindly on Monday and sell it on a specific day of the week—whichever one is up to you. Then compare the result with one of your existing systems and decide for yourself which is better. That’s the rough draft.

“what’s a d grade edge?”

Sure, an easy way to grade a system is to calculate its expected value. SMBU have a handy calculator and there are others I’m sure.

In the example I gave of the 42% WR system, the expected value of this trade is -0.03. Not even D grade. This is before anything goes wrong like slippage or broker anomalies and leaves us with no conviction.

That’s a big problem, so we want quality AND quantity when possible. Why? With 10-30 trades we can know very little and certainly haven’t encountered real problems so we are left learning from the streets of live trading. This can be totally fine with some experience if the trade makes sense. 100+ then there’s is an insight. 1000+ and we have some data to work with.

This is why it can be tricky. Unlike traditional science where samples can be 10’s of millions with quantitative finance we have so little data to work with relatively speaking. So we use what we have and PRT couldn’t handle those numbers anyway. One way is using lower time frames to generate enough signals. But it doesn’t have to be. Signal to noise ratio is through the roof in markets so I find we must be selective to believe what we find.

That’s the challenge.

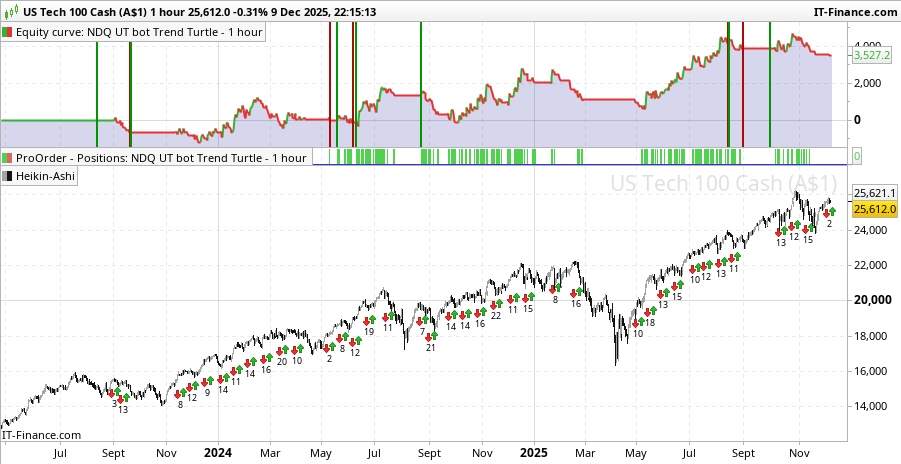

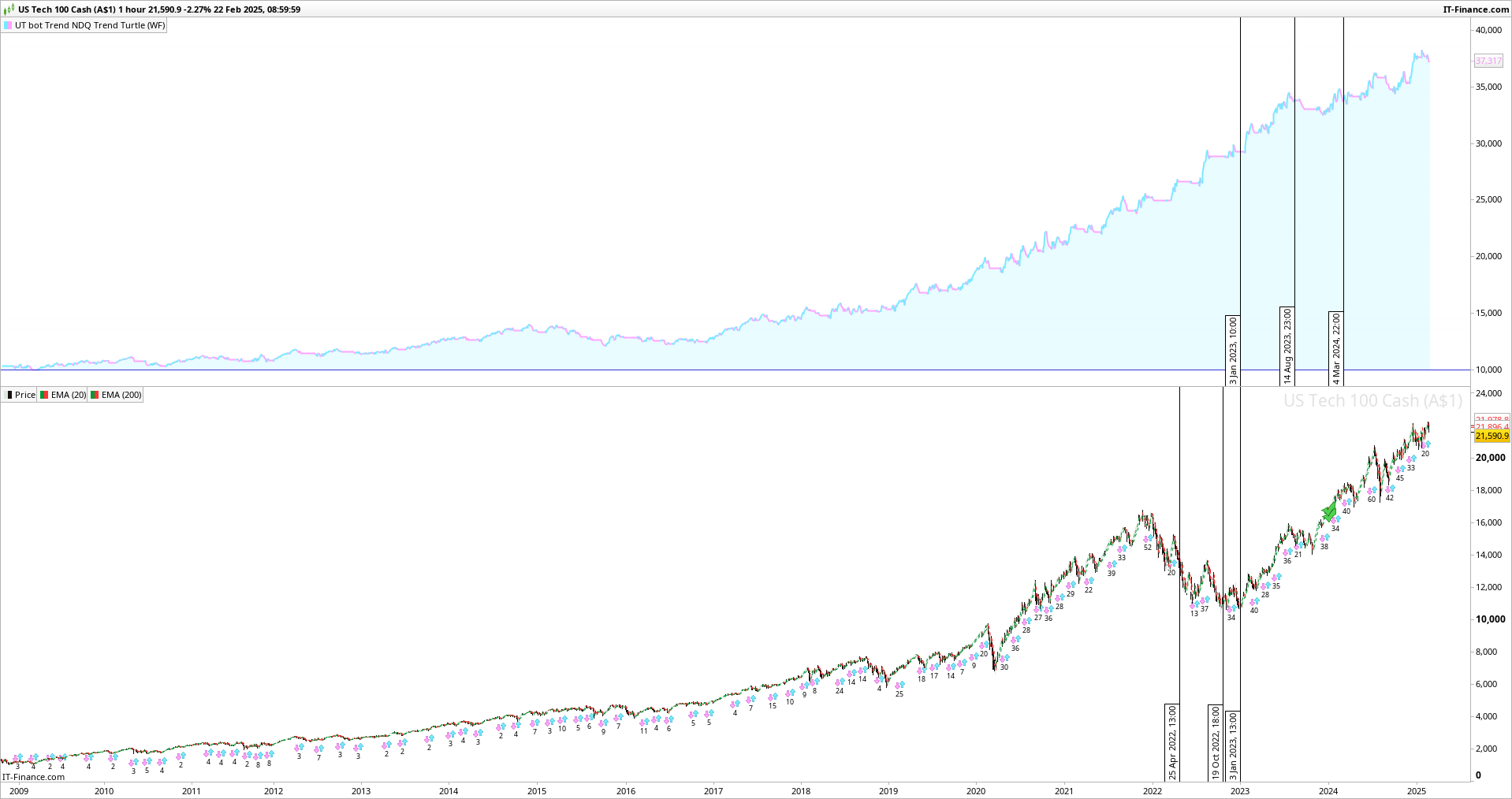

I can show a starter bot as an example to benchmark both live results against the original back test with the incubation period for a D grade edge that is super robust. Full test showed a 42% WR avg (WR is not static). In the 235 live trades I’ve had slippage once that was so great during CPI event that doubled the loss. Once I tried to out trade it and missed $600 before I stopped such nonsense. I marvel at this bot and keep it on due to its reliability and quite a few of these types of edges can make a decent portfolio to start with. As far as I can tell, it was the sample size and process that I applied that avoided curve fitting. It’s not as pretty live as the stair step equity when zoomed out and I fully expect to lose half of what it makes during it’s cycles. It can be rough indeed and at other times an absolute saviour for months on end. Its edge is so small it is laughable and yet has netted thousands over time. 12 lines of code and 2 indicators entering on an impulse signal with 100pt TS used but it only really works because of what Phoentzs has told you. The US markets are so bullish we can throw darts and grind out something algorithmically. Leverage takes care of the rest to beat ETF performance but I could never go all in on something this mediocre. That is why we keep looking for better.

So only you know what you’re looking for, but please don’t overlook simple as a first port of call! Hope that helps some.

indicators are an eldorado, yes. yes!! but they are an eldorado for the brokers, for the banks behind the brokers, for the “market gurus” and other part of the crowd in the business of system-selling and traders’ “education” selling. not for the traders. for the traders – let me put it to some extreme – they are dead end. and they are like a swamp, once in – it’s very hard to get out. especially if one is for some reason fascinated by any kind of maths and stats, be it because of personal interest or professional background. so here is my favorit magic combination of indicators: zero out all of them. it forces (or let’s say frees) one’s mind to start thinking differently (from the crowd). about the market, how it works, how it does not work, who and how is operating there, how they make money, how they hedge and how they lose. how big price changes emerge, how long they last and how they end. is it all that happening because of macd-shmackdee behaving in certain way? are institutions and market makers buying or selling something like crazy for hours, days, weeks, months and years (chose your favorit time horizon…) bacause fibonacci had a strong drink last night and dropped 61,8% below the table? or because elliott was surfing on his favorit wave?

I suppose it is usefull (or maybe even crucial) when designing a trading approach to think also about the “other side” of your trade. you want to make money (I assume…) – and that means, as brutual as it sounds, you need those on the “other side” of your trades losing their cash. nobody is comming to the market with the aim putting their cash on my table. contrary, everybody wants my money, your money. me losing – somebody is earning, and vice versa. so we are in business with ultra-fierce competition. it’s not some cool game of colourful indicators on the screen. it’s billions of usd/eur/etc. on one side fighting every day against billions on the other side in order to take away money from each other, battling on each tick up and down. and we “know” those famous 90% – which is the cliche number for the losing (retail) traders. I think the reality is much worse. I was listening few weeks ago to an interview with an IG manager, quite useless interview for traders I would say, but there he was telling / quoting some study on US market participants / that only around 1% of traders over 5 years time span make money trading intraday. 1% Karl… And more, I belive not only majority of retail folks lose a lot, but also institutions and all the other “big guys” with very deep pockets and fastest computers in the basement, they are not “gods” either.

have fun and cheers

justisan

@ModestInvestor

Ok I got to be honest, I’d not seen your video until now.

You sir, are hilarious.

Look, if your at the start please reflect and name one field, expertise, skill, capability that provides oodles of cash where success comes BEFORE experience. Because this is the very first birthplace of a trader. In every other profession it is known to require years of training and education. A builder/plumber/chef doing a 4 year apprenticeship, a doctorate taking 10yrs of academia and a huge sunken cost. A commercial pilots license costing 130K aud.

But a trader no. Sign up, deposit and you’re away. Very low barrier to entry. Well that’s what is says on the packet..right?

No.

250K of wins and losses is a heavy tuition fee for my first 30K paid out. Maybe it was the ‘Downstairs office’ Uni I went to, it could be less for others and certainly better/faster if full time.

After this you can apply for your license to print money.

Very entertaining vid. Thumbs up from me.

Thanks @coincatcha I’ll be using expected value from now on cheers. Trend Turtle sounds like it could like the famous Turtle trading strategy. But agree in won’t overlook simple , cheers

I really hope that wasn’t $250k of losses, glad things are working out & thanks for the compliments on the video. 😊

@justisan thanks, an interesting point of view. I do largely concur, (Infact I’d given up until my friend started building an A.I bot which gave me more insight) but I also believe that indicators aren’t the lead or even reliable, but can be used to show what is happening/trending and likely to happen. There will be a lot of losses, but I only need that slight edge) The 1% bit is fascinating, I always suspected way over the % the platforms say lose.

I really liked Jim Simons book “the man who solved the markets”, an insanely intelligent bunch of people who failed many times, but eventually found very profitable systems.

I’ve pretty much designed my first bot, S&P 500 with just 2 indicators and a trailing stop, I’ll post it soon.

I really liked Jim Simons book

Some people run crazy low wr/high expectancy systems that either suit them or it’s all they can find, then go all in for the ride. I know that wasn’t so much the case with Jim’s fund but there are plenty of stories going around of 18% 1:6 type trades.

In the end, it just comes down to what we can tolerate and how heavy we use them. Research is defunct at that point and becomes a game of minding our minds.

Go hard, you’ll get it.

hi again,

what brokers operating in EU post as % of losing accounts on their websites/platforms is not something really relevant and might be even giving way too much hope to the readers of that message. if I did not misunderstand, it’s a report for last quarter. so if a broker tells 70% of their accounts are losing, it means 70% of accounts lost money last quarter and so 30% were making money. one can think “wow! I am definetely clever and so it should not be that difficult to be among those 30% making money”. but it is not that “linear”. on one hand even generally successful trader can have easily a drawdown which goes for 3 months or longer. but more on the other hand: even generally losing trader will have sometimes a winning period of 3 months – or longer. so those 30% making money last 3 months are by far not necessary systematically successful traders – they might be very probably among those 70% losing money next quarter, and so on every next quarter. “adding” those winners/losers as probabilities (which they are not), after 4 quarters the number will be like 90% losing (after 8 quarters 97,5%). and those remaining 10% are not necessary systematic winners, not even talking about if those 10% would be able to make living from their trading results. making 10USD last quarter puts one into 30% of “winners” for the quarter.

your statement “I only need that slight edge” sounds like a humble target. there are guys here with target to develop a system(s) which doubles account every week (not joking, you can find those statements and similar here in forum). well, it’s probably easy to agree that is not humble, it’s a dream and really bad one. then there are other – “humble” – folks telling: I only want/need to make 10 points/pips every day, then I am more than happy. what? 10 points a day sounds like peanuts, it has to be possible – equity indices are moving hundreds of points each day… it’s much harder to see that this target/wish is everything but not humble at all as well, if fact it is exactly same like “doubling account every week”. it is unfortunately again a wish for an ATM/money printing license…

trading is really unusual business. as an employee or as an usual company one can provide mediocre or even rather poor work/product and still receive salary, survive for quite long or even make profit as a company. there is a demand for poor/mediocre work/product, it is just not payed that well as high quality work/product. in trading it is kind of extreme I would say: either one has an approach with the edge, or not. there is nothing like “poor” or “mediocre” edge. it’s either 1 or 0. even “slight” edge one can exploit massively. and on the other hand even a system with “big” edge one can crash against the wall – for example by trading it with too big size, or shutting it down in the middle of a painful drawdow – by “chance” just before next trade would carry the equity to the new highs, but instead of that after painful drawdawn comes even worse drawdown. and really ugly it is that in trading one kind of never knows if one really has an edge: I argue that nobody can prove having a system with an edge. even if one has a “successful” backtest and some history of profitable live trading, it’s not a prove for having a system with an edge. yep, if in live trading a system is making several dozens or better several hundreds of trades per year and it is making money for a year or two, it might be a system with an edge – but is it a prove?…

I do not want to demotivate by telling all above. I want to motivate to look at trading extremely, damned serious.

wishing good luck in discovering an edge

justisan

and btw, it was me that idiot 😀 who was shutting down one system manually after waking up at around 04:00 (not on purpose) and seeing dax moving down fast. I am testing that system with rather small size live since one month, it had an open long position for few days already and accumulated 3k of profits until yesterday evening. watching dax dropping this early morning I thought ok, I am out, I will review in more details how this system behaves around FED interest rate announcement days. F****! the move down would not have stopped me out according system’s logic – dax fully recovered and makes new highs now above yesterday’s high and a high for this month, and who knows how much profit I will be missing in the end. (ok, I will see it after trade is closed in the backtest). ok, it’s “only” a test system, and small size. and still I “hate” myself…

I can tell you. Something like 1500 at the moment. That would be including the loss I had too. Automated loss.

Ask me again in an hour.

It can well be that you never heard me telling that I never-ever killed a system because of whatever reason. Losing is part of the job. It is also part of the learning.

Some say we have Demo for that. 😉

Peter, more than an hour later: what’s the status!?

yep, shutting down an automated system manually when trade is live is really nasty stuff. luckily it is for very long already not a regular “habit” of mine any more. I have done that 4 times this year, I remember it well, because it is in the top of my “not-to-do” list. for like 9 system live and like 600 trades performed during the year, stopping 4 trades manually did not a lot of damage luckily. in some cases it was reducing the losses, in some cases it was reducing the profits. does not matter what the outcome was – these were simply stupid, realy bad decisions in the end. as they say, you should follow your system “religiously”. and yes, one can review this and test that – but not shut down system in the middle of the trade… I was not even losing on that mentioned trade today in the early morning – it made around 1k profit after exiting manually. am I happy with that profit of 1k EUR? it’s like 40% of net monthly avarage salary in Austria… but I am totally upset – because it was ugly decision. losses are not only trades which which reduce one’s capital. “losses” are as well those missed profits, and ruined discipline – even for that short moment – is one of the worst things of all in trading.

demo account – is it not a swear word? 😀

similar like you Peter, who never stopped system manually, I was never “doing” a single trade on demo account in my life. either you trade, or you play around. of course many get ultra rich – on demo account. same as many have seen UFO/aliens – on youtube of course.

have a nice evening

justisan