Bonjour roberto et toute la communauté

je vous partage une stratégie sur du 30 sec nasdaq 15h30/17h30 je voudrais pouvoir diminuer la perte j’ai essayé d’intégrer votre break even pour limiter la perte mais cela reste moyen je trouve.

Pouvez vous apporter votre savoir sur cette algo je vous remercie.

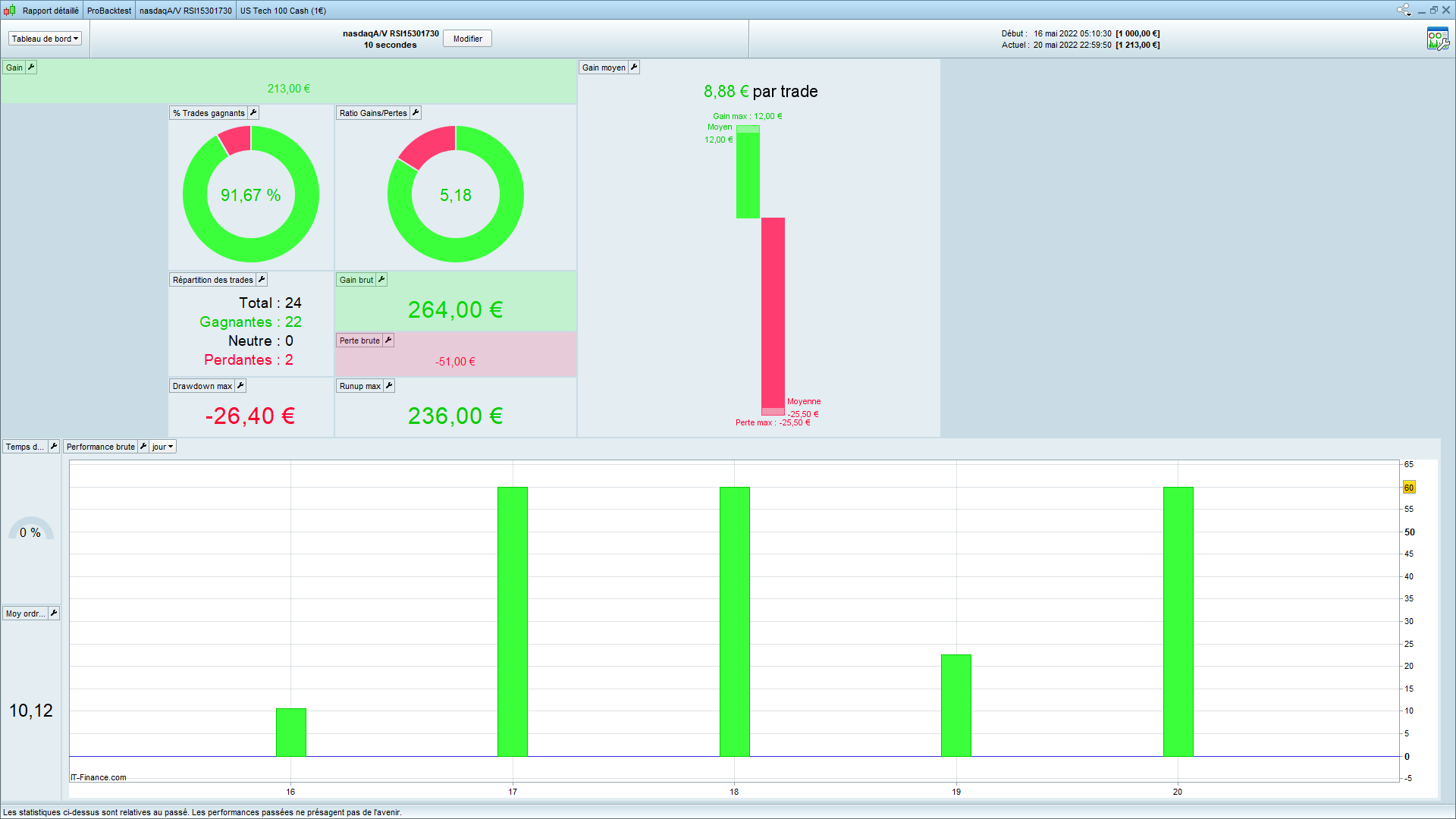

Je m’aperçois que les deux premiers trades sont toujours gagnants mais un mauvais vient gâcher la fête.

Sur le backtest depuis mi mars que je le suis les semaines sont toujours positves mais ca pourrait être mieux. Quand pensez vous?

Merci pour votre aide

// Définition des paramètres du code

DEFPARAM CumulateOrders = False // Cumul des positions désactivé

// Annule tous les ordres en attente et ferme toutes les positions à l'heure "FLATAFTER"

DEFPARAM FLATAFTER = 173000

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position avant l'heure spécifiée

noEntryBeforeTime = 153000

timeEnterBefore = time >= noEntryBeforeTime

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position après l'heure spécifiée

noEntryAfterTime = 173000

timeEnterAfter = time < noEntryAfterTime

// Empêche le système de placer de nouveaux ordres sur les jours de la semaine spécifiés

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

// Conditions pour ouvrir une position acheteuse

indicator1 = RSI[14](close)

c1 = (indicator1 CROSSES OVER 30)

IF c1 AND timeEnterBefore AND timeEnterAfter AND not daysForbiddenEntry THEN

BUY 1 CONTRACT AT MARKET

ENDIF

// Conditions pour ouvrir une position en vente à découvert

indicator2 = RSI[14](close)

c2 = (indicator2 CROSSES UNDER 70)

IF c2 AND timeEnterBefore AND timeEnterAfter AND not daysForbiddenEntry THEN

SELLSHORT 1 CONTRACT AT MARKET

ENDIF

// Stops et objectifs

SET STOP pTRAILING 31

SET TARGET pPROFIT 11

IF Not OnMarket THEN

//

// when NOT OnMarket reset values to default values

//

TrailStart = 5 //30 Start trailing profits from this point

BasePerCent = 0.000 //20.0% Profit percentage to keep when setting BerakEven

StepSize = 10 //10 Pip chunks to increase Percentage

PerCentInc = 0.100 //10.0% PerCent increment after each StepSize chunk

BarNumber = 10 //10 Add further % so that trades don't keep running too long

BarPerCent = 0.100 //10% Add this additional percentage every BarNumber bars

RoundTO = -0.5 //-0.5 rounds always to Lower integer, +0.4 rounds always to Higher integer, 0 defaults PRT behaviour

PriceDistance = 7 * pipsize //7 minimun distance from current price

y1 = 0 //reset to 0

y2 = 0 //reset to 0

ProfitPerCent = BasePerCent //reset to desired default value

TradeBar = BarIndex

ELSIF LongOnMarket AND close > (TradePrice + (y1 * pipsize)) THEN //LONG positions

//

// compute the value of the Percentage of profits, if any, to lock in for LONG trades

//

x1 = (close - tradeprice) / pipsize //convert price to pips

IF x1 >= TrailStart THEN // go ahead only if N+ pips

Diff1 = abs(TrailStart - x1) //difference from current profit and TrailStart

Chunks1 = max(0,round((Diff1 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks1 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y1 = max(x1 * ProfitPerCent, y1) //y1 = % of max profit

ENDIF

ELSIF ShortOnMarket AND close < (TradePrice - (y2 * pipsize)) THEN //SHORT positions

//

// compute the value of the Percentage of profits, if any, to lock in for SHORT trades

//

x2 = (tradeprice - close) / pipsize //convert price to pips

IF x2 >= TrailStart THEN // go ahead only if N+ pips

Diff2 = abs(TrailStart - x2) //difference from current profit and TrailStart

Chunks2 = max(0,round((Diff2 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks2 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y2 = max(x2 * ProfitPerCent, y2) //y2 = % of max profit

ENDIF

ENDIF

IF y1 THEN //Place pending STOP order when y1 > 0 (LONG positions)

SellPrice = Tradeprice + (y1 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - SellPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close >= SellPrice THEN

SELL AT SellPrice STOP

ELSE

SELL AT SellPrice LIMIT

ENDIF

ELSE

//

//sell AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

SELL AT Market

ENDIF

ENDIF

IF y2 THEN //Place pending STOP order when y2 > 0 (SHORT positions)

ExitPrice = Tradeprice - (y2 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - ExitPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close <= ExitPrice THEN

EXITSHORT AT ExitPrice STOP

ELSE

EXITSHORT AT ExitPrice LIMIT

ENDIF

ELSE

//

//ExitShort AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

EXITSHORT AT Market

ENDIF

ENDIF

Controllo codice maxTrades x day

Avec ce code, vous pouvez limiter les transactions par jour. C’est vraiment très utile.

Bonjour phoentzs merci pour ton retour,

Je recontre un souci, peux tu vérifier si j’ai bien mis les lignes de codes comme il le faut sur ma algo parce que j’ai bien l’impression qu’il continue à prendre plusieurs trades , Si tu peux me corriger je t’en remercie. Et avoir ton avis et les modifications que tu apporterais.

Merci encore

// Définition des paramètres du code

DEFPARAM CumulateOrders = False // Cumul des positions désactivé

// Annule tous les ordres en attente et ferme toutes les positions à l'heure "FLATAFTER"

DEFPARAM FLATAFTER = 173000

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position avant l'heure spécifiée

noEntryBeforeTime = 153000

timeEnterBefore = time >= noEntryBeforeTime

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position après l'heure spécifiée

noEntryAfterTime = 173000

timeEnterAfter = time < noEntryAfterTime

// Empêche le système de placer de nouveaux ordres sur les jours de la semaine spécifiés

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

// Conditions pour ouvrir une position acheteuse

indicator1 = RSI[14](close)

c1 = (indicator1 CROSSES OVER 30)

IF c1 AND timeEnterBefore AND timeEnterAfter AND not daysForbiddenEntry THEN

BUY 1 CONTRACT AT MARKET

ENDIF

once maxTrades = 1 //maxNumberDailyTrades

once tally = 0

if intradayBarIndex = 0 then

tally = 0

endif

newTrades = (onMarket and not onMarket[1]) or (longOnMarket and shortOnMarket[1]) or (longOnMarket[1] and shortOnMarket) or ((not OnMarket and not onMarket[1]) and (strategyProfit <> strategyProfit[1])) or ((tradeIndex(1) = tradeIndex(2)) and (barIndex = tradeIndex(1)) and (barIndex > 0) and (strategyProfit = strategyProfit[1]))

if newTrades then

tally = tally +1

endif

// Conditions pour ouvrir une position en vente à découvert

indicator2 = RSI[14](close)

c2 = (indicator2 CROSSES UNDER 70)

IF c2 AND timeEnterBefore AND timeEnterAfter AND not daysForbiddenEntry THEN

SELLSHORT 1 CONTRACT AT MARKET

ENDIF

once maxTrades = 1 //maxNumberDailyTrades

once tally = 0

if intradayBarIndex = 0 then

tally = 0

endif

newTrades = (onMarket and not onMarket[1]) or (longOnMarket and shortOnMarket[1]) or (longOnMarket[1] and shortOnMarket) or ((not OnMarket and not onMarket[1]) and (strategyProfit <> strategyProfit[1])) or ((tradeIndex(1) = tradeIndex(2)) and (barIndex = tradeIndex(1)) and (barIndex > 0) and (strategyProfit = strategyProfit[1]))

if newTrades then

tally = tally +1

endif

// Stops et objectifs

SET STOP pTRAILING 31

SET TARGET pPROFIT 11

IF Not OnMarket THEN

//

// when NOT OnMarket reset values to default values

//

TrailStart = 5 //30 Start trailing profits from this point

BasePerCent = 0.000 //20.0% Profit percentage to keep when setting BerakEven

StepSize = 10 //10 Pip chunks to increase Percentage

PerCentInc = 0.100 //10.0% PerCent increment after each StepSize chunk

BarNumber = 10 //10 Add further % so that trades don't keep running too long

BarPerCent = 0.100 //10% Add this additional percentage every BarNumber bars

RoundTO = -0.5 //-0.5 rounds always to Lower integer, +0.4 rounds always to Higher integer, 0 defaults PRT behaviour

PriceDistance = 7 * pipsize //7 minimun distance from current price

y1 = 0 //reset to 0

y2 = 0 //reset to 0

ProfitPerCent = BasePerCent //reset to desired default value

TradeBar = BarIndex

ELSIF LongOnMarket AND close > (TradePrice + (y1 * pipsize)) THEN //LONG positions

//

// compute the value of the Percentage of profits, if any, to lock in for LONG trades

//

x1 = (close - tradeprice) / pipsize //convert price to pips

IF x1 >= TrailStart THEN // go ahead only if N+ pips

Diff1 = abs(TrailStart - x1) //difference from current profit and TrailStart

Chunks1 = max(0,round((Diff1 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks1 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y1 = max(x1 * ProfitPerCent, y1) //y1 = % of max profit

ENDIF

ELSIF ShortOnMarket AND close < (TradePrice - (y2 * pipsize)) THEN //SHORT positions

//

// compute the value of the Percentage of profits, if any, to lock in for SHORT trades

//

x2 = (tradeprice - close) / pipsize //convert price to pips

IF x2 >= TrailStart THEN // go ahead only if N+ pips

Diff2 = abs(TrailStart - x2) //difference from current profit and TrailStart

Chunks2 = max(0,round((Diff2 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks2 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y2 = max(x2 * ProfitPerCent, y2) //y2 = % of max profit

ENDIF

ENDIF

IF y1 THEN //Place pending STOP order when y1 > 0 (LONG positions)

SellPrice = Tradeprice + (y1 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - SellPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close >= SellPrice THEN

SELL AT SellPrice STOP

ELSE

SELL AT SellPrice LIMIT

ENDIF

ELSE

//

//sell AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

SELL AT Market

ENDIF

ENDIF

IF y2 THEN //Place pending STOP order when y2 > 0 (SHORT positions)

ExitPrice = Tradeprice - (y2 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - ExitPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close <= ExitPrice THEN

EXITSHORT AT ExitPrice STOP

ELSE

EXITSHORT AT ExitPrice LIMIT

ENDIF

ELSE

//

//ExitShort AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

EXITSHORT AT Market

ENDIF

ENDIF

Je te remerci enormement pour ton aide. tu a changer la qualité de mon petit algo scalping. Je l’adopte sur du 10 sec et du 30 sec sur les différents indice. Je n’ai pas encore essayé sur le devises.

Merci encore a bientot et bon dimanche a toi.

Quelle version allez-vous utiliser maintenant ?

J’ai comparé la première et la deuxième. les gains sont meilleurs avec avec le premier de robberto. je vous enverrai ce soir âpres mon travail l’algo avec les paramètres un peu modifié. La seul chose que je regrette c’est que je ne peux faire que un back test sur 90k bougies. Je l’ai effectué sur du graph 10sec et 30 sec sur les indices cac et dax le matin et le nasdaq et dow l’apres midi. Sachez que j’ai effectué cette technique que je suis depuis mi avril mais que je note chaque semaine le vendredi soir les résultats de chaque semaine. Les gains sont tjs supérieurs chaque semaine alors que je n’avais pas cette modification incorporé maintenant. Et les résultats son meilleurs avec 2 ou 5 trades par jours. Pour vous dire cette semaine avec votre aide la semaine était positive alors qu’elle aurait était négative. Si vous pouvez quand vous aurez mes algos pourriez vous voir avec un backtest et 2millions de bouggies me dire si le resultat est concluant. Merci encore .

Je vous ferais une comparaison et vous enverrai en image avant et âpres intégration de votre aide. merci

Malheureusement, je n’ai qu’un maximum de 1 semaine comme période de backtest dans ces unités de temps. À titre d’idée : peut-être que le système est plus viable si vous attribuez une tendance de haute qualité avec MTF ? Juste comme une idée.

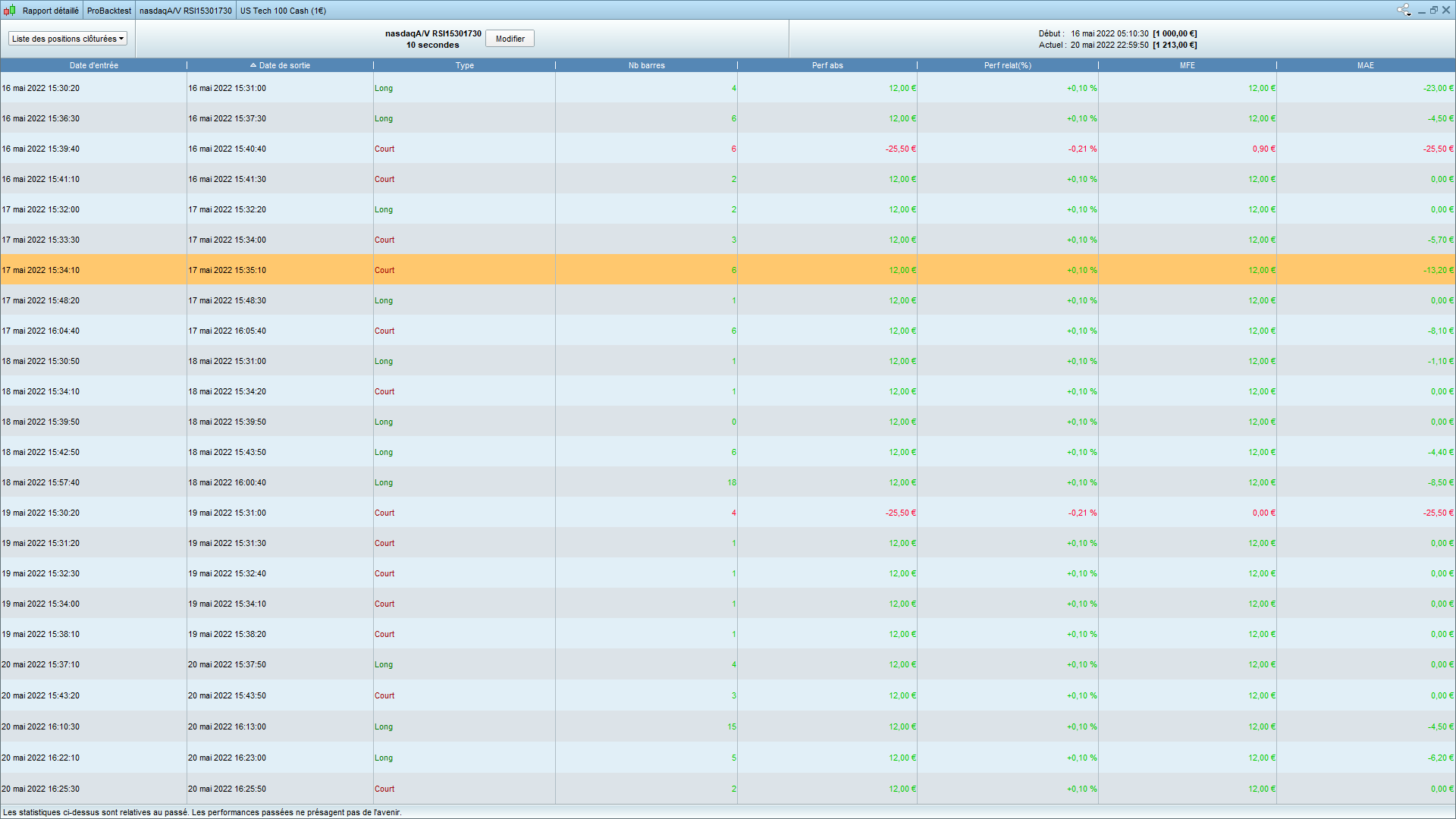

Voici le backtest réglé sur 5 trades en 10 sec avec tp 12 et stop a 28 sur nadasq

// Définition des paramètres du code

DEFPARAM CumulateOrders = False // Cumul des positions désactivé

// Annule tous les ordres en attente et ferme toutes les positions à l'heure "FLATAFTER"

DEFPARAM FLATAFTER = 173000

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position avant l'heure spécifiée

noEntryBeforeTime = 153000

timeEnterBefore = time >= noEntryBeforeTime

// Empêche le système de placer des ordres pour entrer sur le marché ou augmenter la taille d'une position après l'heure spécifiée

noEntryAfterTime = 173000

timeEnterAfter = time < noEntryAfterTime

// Empêche le système de placer de nouveaux ordres sur les jours de la semaine spécifiés

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

// Conditions pour ouvrir une position acheteuse

indicator1 = RSI[13](close)

c1 = (indicator1 CROSSES OVER 30)

IF c1 AND timeEnterBefore AND timeEnterAfter AND not daysForbiddenEntry and tally < maxTrades THEN

BUY 1 CONTRACT AT MARKET

ENDIF

//---------------------------------------------------------------------------------------------------------------

once maxTrades = 5 //maxNumberDailyTrades

once tally = 0

if intradayBarIndex = 0 then

tally = 0

endif

newTrades = (onMarket and not onMarket[1]) or ((not onMarket and not onMarket[1]) and (strategyProfit <> strategyProfit[1])) or (longOnMarket and ShortOnMarket[1]) or (longOnMarket[1] and shortOnMarket) or ((tradeIndex(1) = tradeIndex(2)) and (barIndex = tradeIndex(1)) and (barIndex > 0) and (strategyProfit = strategyProfit[1]))

if newTrades then

tally = tally +1

endif

//------------------------------------------------------------------------------------------------------------------------

// Conditions pour ouvrir une position en vente à découvert

indicator2 = RSI[13](close)

c2 = (indicator2 CROSSES UNDER 70)

IF c2 AND timeEnterBefore AND timeEnterAfter AND not daysForbiddenEntry and tally < maxTrades THEN

SELLSHORT 1 CONTRACT AT MARKET

ENDIF

//---------------------------------------------------------------------------------------------------------------

//Max-Orders per Day

once maxOrdersL = 1 //long

once maxOrdersS = 1 //short

if intradayBarIndex = 0 then //reset orders count

ordersCountL = 0

ordersCountS = 0

endif

if longTriggered then //check if an order has opened in the current bar

ordersCountL = ordersCountL + 1

endif

if shortTriggered then //check if an order has opened in the current bar

ordersCountS = ordersCountS + 1

endif

//------------------------------------------------------------------------------------------------------------------------

//Stops et objectifs

SET STOP pTRAILING 28

SET TARGET pPROFIT 12

IF Not OnMarket THEN

//

// when NOT OnMarket reset values to default values

//

TrailStart = 6 //30 Start trailing profits from this point

BasePerCent = 0.000 //20.0% Profit percentage to keep when setting BerakEven

StepSize = 10 //10 Pip chunks to increase Percentage

PerCentInc = 0.100 //10.0% PerCent increment after each StepSize chunk

BarNumber = 10 //10 Add further % so that trades don't keep running too long

BarPerCent = 0.100 //10% Add this additional percentage every BarNumber bars

RoundTO = -0.5 //-0.5 rounds always to Lower integer, +0.4 rounds always to Higher integer, 0 defaults PRT behaviour

PriceDistance = 7 * pipsize //7 minimun distance from current price

y1 = 0 //reset to 0

y2 = 0 //reset to 0

ProfitPerCent = BasePerCent //reset to desired default value

TradeBar = BarIndex

ELSIF LongOnMarket AND close > (TradePrice + (y1 * pipsize)) THEN //LONG positions

//

// compute the value of the Percentage of profits, if any, to lock in for LONG trades

//

x1 = (close - tradeprice) / pipsize //convert price to pips

IF x1 >= TrailStart THEN // go ahead only if N+ pips

Diff1 = abs(TrailStart - x1) //difference from current profit and TrailStart

Chunks1 = max(0,round((Diff1 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks1 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y1 = max(x1 * ProfitPerCent, y1) //y1 = % of max profit

ENDIF

ELSIF ShortOnMarket AND close < (TradePrice - (y2 * pipsize)) THEN //SHORT positions

//

// compute the value of the Percentage of profits, if any, to lock in for SHORT trades

//

x2 = (tradeprice - close) / pipsize //convert price to pips

IF x2 >= TrailStart THEN // go ahead only if N+ pips

Diff2 = abs(TrailStart - x2) //difference from current profit and TrailStart

Chunks2 = max(0,round((Diff2 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks2 * PerCentInc)) //compute new size of ProfitPerCent

// compute number of bars elapsed and add an additionl percentage

// (this percentage is different from PerCentInc, since it's a direct percentage, not a Percentage of BasePerCent)

// (if BasePerCent is 20% and this is 10%, the whole percentage will be 30%, not 22%)

BarCount = BarIndex - TradeBar

IF BarCount MOD BarNumber = 0 THEN

ProfitPerCent = ProfitPerCent + BarPerCent

ENDIF

//

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y2 = max(x2 * ProfitPerCent, y2) //y2 = % of max profit

ENDIF

ENDIF

IF y1 THEN //Place pending STOP order when y1 > 0 (LONG positions)

SellPrice = Tradeprice + (y1 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - SellPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close >= SellPrice THEN

SELL AT SellPrice STOP

ELSE

SELL AT SellPrice LIMIT

ENDIF

ELSE

//

//sell AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

SELL AT Market

ENDIF

ENDIF

IF y2 THEN //Place pending STOP order when y2 > 0 (SHORT positions)

ExitPrice = Tradeprice - (y2 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - ExitPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close <= ExitPrice THEN

EXITSHORT AT ExitPrice STOP

ELSE

EXITSHORT AT ExitPrice LIMIT

ENDIF

ELSE

//

//ExitShort AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

EXITSHORT AT Market

ENDIF

ENDIF

Voici un aperçu du résultat

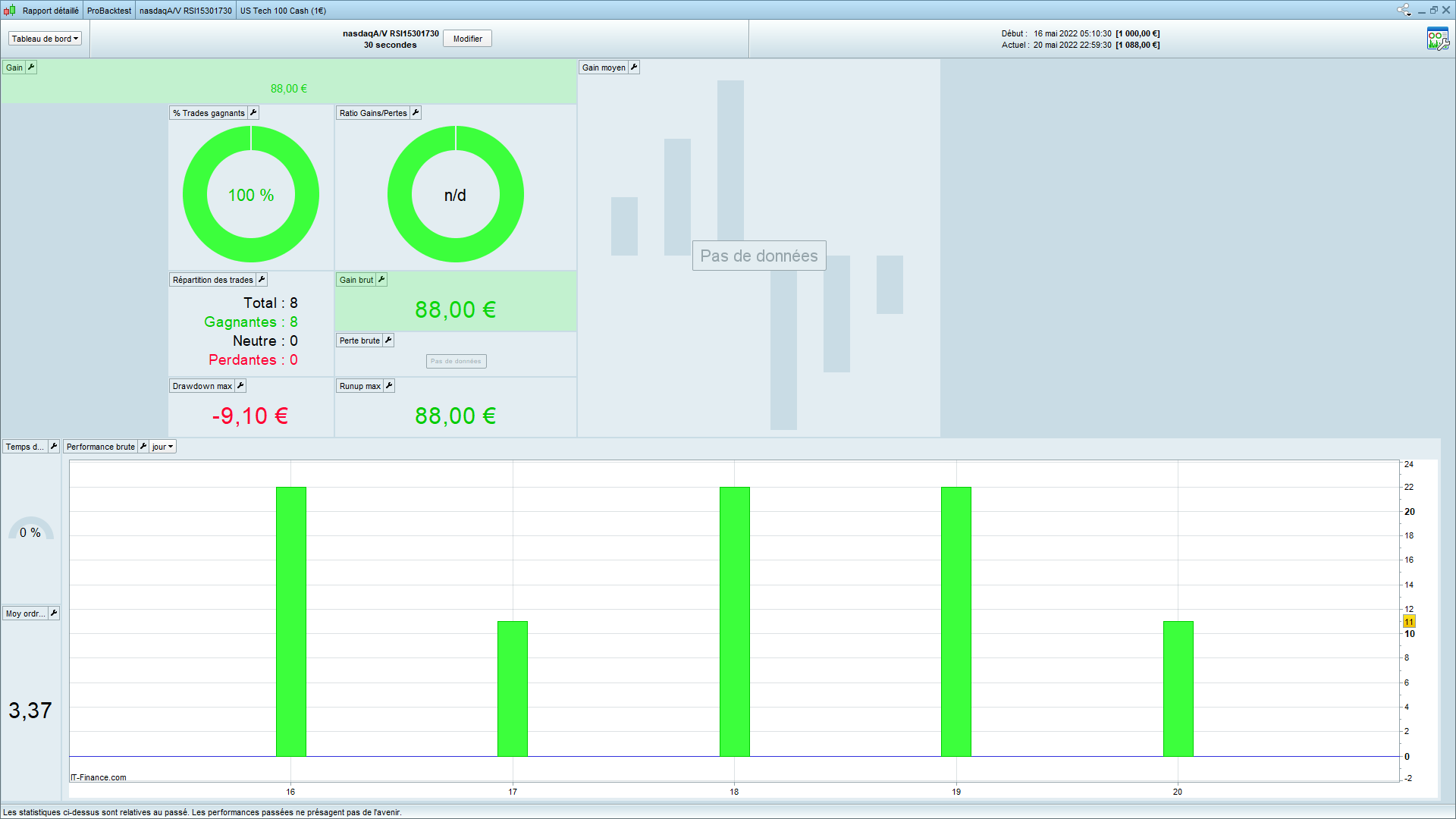

Pour le 30 sec j’ai du utiliser la partie 2 les résultat était meilleurs avec juste 2 trades tp 11 et st 28

Il sera intéressant de voir comment les choses évoluent en une semaine.

Oui bien sûr . Je vous tiens au courant . Après peut être qu’avec un compte pro ils ont la possibilité de le tester sur du plus long terme .

Bonjour,

Je vous dérange 5 minutes, ce matin sur le dax 30 il m’a pris qu’un trade alors que le backtest en signal 3 . Quelel est la raison ? Pouvez vous m’expliquer la raison?

Parce que la température a fortement chuté je dirai 😆

En fait, personne ne peut le savoir, il faudrait vérifier l’entrée et la sortie du trade qui est identique déjà, si celui-ci a durée plus longtemps, alors il a offusqué l’ouverture des autres ?

Fais tu des backtests en tick par tick ? Avec une taille de spread adéquate renseigné dans la case correspondante ?

Bonjour nicolas,

je me douté bien que cela venait de la température lol.

Non je ne fais pas tick par tick mais je vais essayer. Oui j’ai réglé mon spread a 1.4 pour le dax.

Dis moi par rapport au tick par tick il va falloir que je baisse mon tkp ? et mon stop est ce que je le change?