I would like to show you my first attempt to create a system.It is a Scalp system for Timeframe 1 hr Dax ,Take Profit 4 pips and Trailing Stop 12 pips. The System start in 8 30 pm Time Zone GMT+1 and stop 17 00, Spread is 1 point .It has become backtest from 2012 and the results the see above.

Any feedback and any suggestions are welcome!Enjoy it!

//-------------------------------------------------------------------------

// Main code : A Scalper Machine V1 dax

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

// A SCALPER MACHINE V1

//-------------------------------------------------------------------------

// Definition of code parameters

DEFPARAM CumulateOrders = False // Cumulating positions deactivated

REM All positions will be not open before this time

defparam flatbefore = 080000

REM All positions will be closed after this time

defparam flatafter = 165000

// MONEY MANAGMENT

QTY=1

ONCE M=500

BANK=100

ONCE PQTYADJUST=0

QTYADJUST = ROUND(STRATEGYPROFIT /M)

IF QTYADJUST > 0 THEN

QTY=QTY+QTYADJUST

IF QTYADJUST < PQTYADJUST THEN

M=M+BANK

PQTYADJUST=QTYADJUST

ENDIF

IF QTYADJUST > PQTYADJUST THEN

PQTYADJUST=QTYADJUST

ENDIF

ELSE

QTY=1

ENDIF

// VARIABLE.. FOR EASY BACKTESTING ////////

a=55

b=2

n=2

z=7

v=23

q=2

a1=12

b1=1

k=15

w=2

ts1=9

ema = Exponentialaverage[ts1](close)

advance=abs(round(ema-ema[1]))

/////////////////////////////////////////////////////////////////////////////////////////

// TIME AND DAY MANAGMENT

// Prevents the system from placing new orders on specified days of the week

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

// trading window

ONCE startTime = 083000

ONCE endTime = 170000

// trade only in trading window 9-20

IF Time >= startTime AND Time <= endTime THEN

// MAIN SYSTEM //

// Conditions to enter long positions

indicator1 = Average[n](close)

indicator2 = Average[z](close)

c1 = (indicator1 > indicator2)

indicator3 = Stochastic[a,b](close)

indicator4 = Average[v](Stochastic[a,b](close))

c2 = (indicator3 > indicator4)

indicator5 = MACDline[12,26,9](close)

indicator6 = ExponentialAverage[q](MACDline[12,26,9](close))

c3 = (indicator5 > indicator6)

// Conditions to enter short positions

indicator9 = Average[a1](close)

indicator10 = Average[b1](close)

c5 = (indicator9 > indicator10)

indicator11 = Average[k](Stochastic[a,b](close))

indicator12 = Stochastic[a,b](close)

c6 = (indicator11 > indicator12)

indicator13 = ExponentialAverage[w](MACDline[12,26,9](close))

indicator14 = MACDline[12,26,9](close)

c7 = (indicator13 > indicator14)

// LONG

if not longonmarket and c1 AND c2 AND c3 and Momentum[11](close)>0 and RSI[6](close)>65 and not daysForbiddenEntry then

BuyPrice = ema+advance

buy qty contract at BuyPrice limit

endif

// SHORT

if not shortonmarket and c5 AND c6 AND c7 and Momentum[11](close)<0 and RSI[6](close)<35 and not daysForbiddenEntry then

SellPrice = ema-advance

sellshort qty contract at sellprice limit

ENDIF

set stop pTRAILING 12

set target Pprofit 4

endif

Hi Antonios, I moved your post from the library pending queue to the forum.

Unfortunately, you have been trapped into the “0 bar phenomena” which is a well-known and common problem of Probacktest result before the version 10.3 of prorealtime. If the stoploss and takeprofit price levels are met within the same bar, the takeprofit is tested first and your trade is a winning one, but it would not be the case in real time trading.

I see that you have optimized a lot, all indicators periods, which is not good, the result is over-fitted on the past data.

So, I’m sorry but the backtest is not good here. Please don’t be offend, we are all here to help each other 🙂 Your questions are welcome.

Hi there, if I may suggest a good book for everyone interested in automatic strategy: “Building Winning Algorithmic Trading Systems”… This book will explain in details what Nicolas means…

Cheers.

I get this result with 10.3 tick by tick. Still look too good to be true.

Nicolas- Is this the same backtest problem that we have in the backtest in Rauls 5 min intraday thread?

A question, what is the point of placing a trailing of 12 points if you put a take profit of 4?

just put it on live , you knows …..

Thank you Antonios for this interesting code.

Ratio is very good and I like when you are few time in market. Let’s have a look if tick by tick backtest and demo mode have same results…

About optimization: backtests are still good when I modify a little bit variables.

Growth of the contracts number if perhaps too much exponantial for me.

Could you just tell us how did you find this strategy?

Thank for all to the feedback in system,I have some problems with backtest in 1hr,I try to solve it and will come back with the upgrading…Raul….Trailing Stop and Take Profit The results of backtesting.

Hi Antonios,

Thank you for the code. Looks very good.

Do you think that you can attach a printscreen for us ?

Cheers,

DJ

i ve put a trailling stop of 5 only and i ve it on live demo ….

Hello Traders!

I would like to forgive me for not so good English but is don’t my native language.

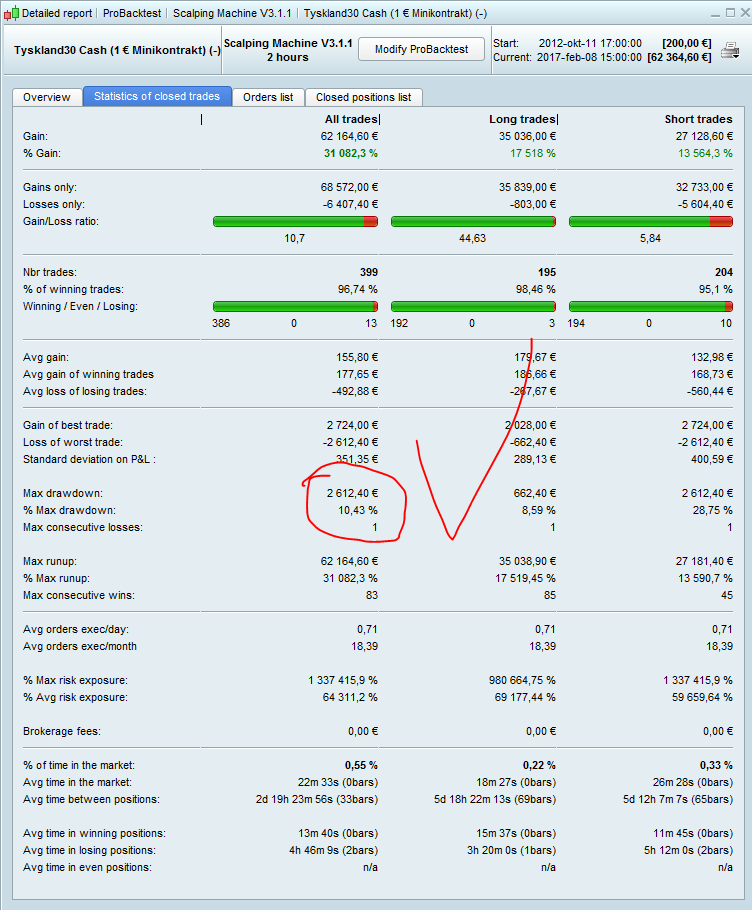

I want once again to thank you all for feedback to my system,and and especially the Alex ,the algorithm gave me the idea for my system.This new version is for 2HR ,1 point spread , trading hours 09:00-19:00 GMT+1,Initial capital is 200 $ ,Risk= 2,and Dax 1Mini.

Trailling Stop 65 and Take Profit 12.The results are from 2012 tick by tick,and he wants is the attention to DD in the Risk=2.

Enjoy that.

////////////SCALPING MACHINE V3.1////////////////////////////////////////////

defparam cumulateorders=false

defparam preloadbars=1000

//defparam flatbefore = 080000

REM All positions will be closed after this time

//defparam flatafter = 203000

////////// MONEY MANAGMENT//////////////////////////////////////////////////

equity = Capital + StrategyProfit

maxrisk = round(equity*(Risk/100))

PositionSize = abs(round((maxrisk/StopLoss)/PointValue)*pipsize)

Capital = 200

Risk = 1.7

StopLoss = round(margin*2)

margin = rangepips*rangepercent

rangepercent =0.1

REM NIGHT MAX

maximo = dhigh(0)

REM NIGHT MIN

minimo = dlow(0)

REM RANGE IN PIPS BETWEEN NIGHT MAX AND MIN

rangepips = round(maximo-minimo)

/////////////////VARIAMBLES/////////////////////////////////////////////////

ts1=9

ema = Exponentialaverage[ts1](close)

once uma=Highest[ts1](high)

once umb=Lowest[ts1](low)

Wave=39*pipsize

a=11

b=13

n=13

z=4

v=12

q=26

a1=9

b1=9

k=1

////////////////////TIME MANAGMENT//////////////////////////////////////////

ONCE startTime = 090000

ONCE endTime = 190000

IF Time >= startTime AND Time <= endTime THEN

////////////////////////////////////////////////////////////////////////

/////////CONDITIONS TO ENTER LONG&SHORT ////////////////////////

///////////////LONG/////////////////////////////////////////////

indicator1 = Average[a](close)

indicator2 = Average[b](close)

c1 = (indicator1 > indicator2)

indicator3 = Stochastic[n,z](close)

indicator4 = Average[a](Stochastic[n,z](close))

c2 = (indicator3 > indicator4)

indicator5 = MACDline[v,q,a1](close)

indicator6 = ExponentialAverage[9](MACDline[v,q,a1](close))

c3 = (indicator5 > indicator6)

////////////SHORT//////////////////////////////////////////////////

indicator9 = Average[b1](close)

indicator10 = Average[k](close)

c5 = (indicator9 > indicator10)

indicator11 = Average[a](Stochastic[n,z](close))

indicator12 = Stochastic[n,z](close)

c6 = (indicator11 > indicator12)

indicator13 = ExponentialAverage[9](MACDline[v,q,a1](close))

indicator14 = MACDline[v,q,a1](close)

c7 = (indicator13 > indicator14)

/////////////////////// CONDITIONS////////////////////////////////

if High > ema and Low < ema then // Touching Ema8

tb = BarIndex

ltp = ema

uma = ema

umb = ema

endif

if low>ema then // New bullish movement

n = BarIndex - tb

uma=Highest[n](high)

umb=ema

endif

if high<ema then // New bearish movement

m = BarIndex - tb

umb=Lowest[m](low)

uma=ema

endif

if (uma-ltp)>Wave and uma>ema then // buy condition

myres=1

endif

if (uma-ltp)<=wave then

myres=0

endif

if (ltp-umb)>wave and umb<ema then // short condition

mysub=-1

endif

if (ltp-umb)<=wave then

mysub=0

endif

advance=abs(round(ema-ema[1]))

//mylot=2

///////////MAIN///////////////////////////////////////////////////////

if not longonmarket and myres=1 and c1 and c2 and c3 and Momentum[11](close)>0 then

BuyPrice = ema+advance

buy positionsize contract at BuyPrice limit

endif

if not shortonmarket and mysub=-1 and c5 and c6 and c7 and Momentum[11](close)<0 then

SellPrice = ema-advance

sellshort positionsize contract at sellprice limit

endif

endif

///////////MONEY MANAGMENT//////////////////////////////////////////////////

//set stop ploss 76

set stop pTRAILING 65

set target pprofit 12

……….Update…..everything is OK after for backtesting , will have to change this variable…….a=7

a=7

b=13

n=13

z=4

v=12

q=26

a1=9

b1=9

k=1

As Nicolas told you, the backtests (even the last one) are not made in “tick by tick” mode. If you rectify, you will see that the system is always loosing.

Hi Antonios. I’m trying to backtest and understand this for myself as you have included many things which are new to me and which I would like to learn. Problem is that I am getting no trades when I run the backtest. I’m in London…all I have changed are the times to:

ONCE startTime = 080000

ONCE endTime = 180000

and I’m looking at the Dax 2H. I have changed a=7.

Please can you let me know if there is anything else that I need to change. Apologies in advance if I’m missing something obvious.