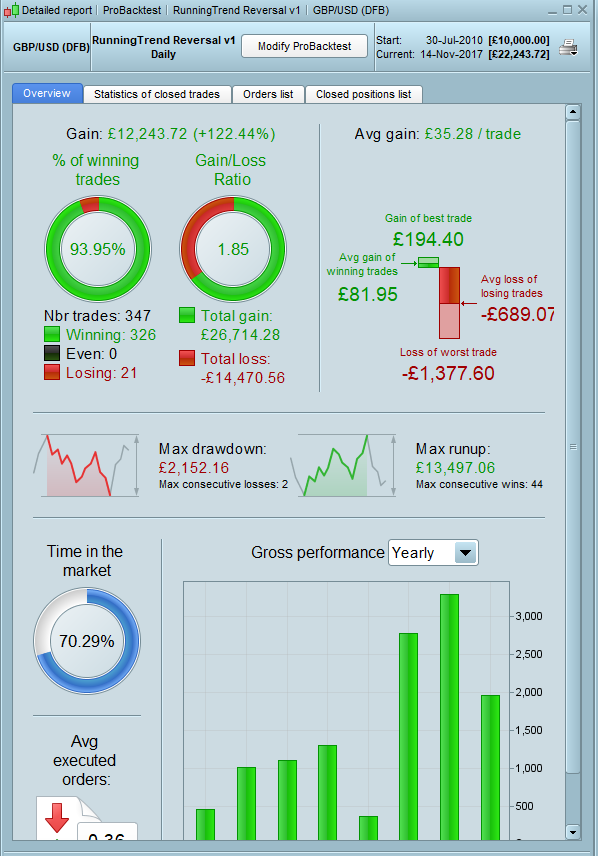

I wrote a simple indicator and then turned it into a strategy that seems to work quite well. I have optimized it on GPDUSD Daily DFB.

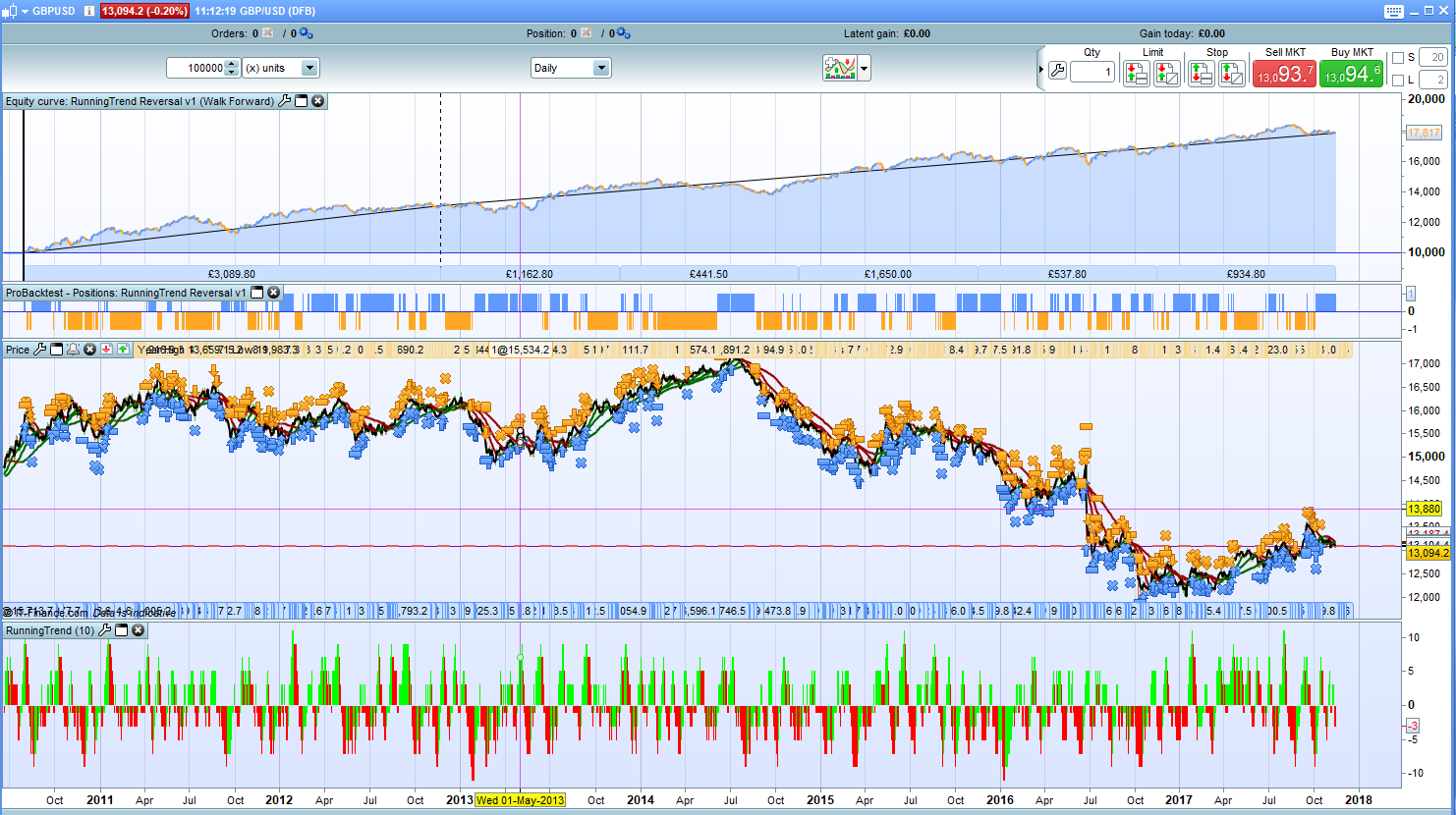

The indicator ‘RunningTrend’ simply counts movement up or down of TypivalPrice over a lookback period and presents it as a histogram.

The strategy enters long or short if not already on the market at changes or direction of the indicator. It exits positions if a candle closes in profit or a take profit level is hit. The amount of profit required to close increases the more days that pass. (this condition can be easily removed if you prefer as alternative code is included). This is an attempt to cover overnight costs/rollover costs for positions held for a long time.

Positions are closed after a certain number of days have passed without achieving profit.

A very loose stop loss is used which may not be to everyone’s risk/reward ratio tastes but is necessary to let positions run and to protect against black swan moments!

Re-investment can be turned on or off.

Any thoughts or ideas on the strategy or indicator will be much appreciated.

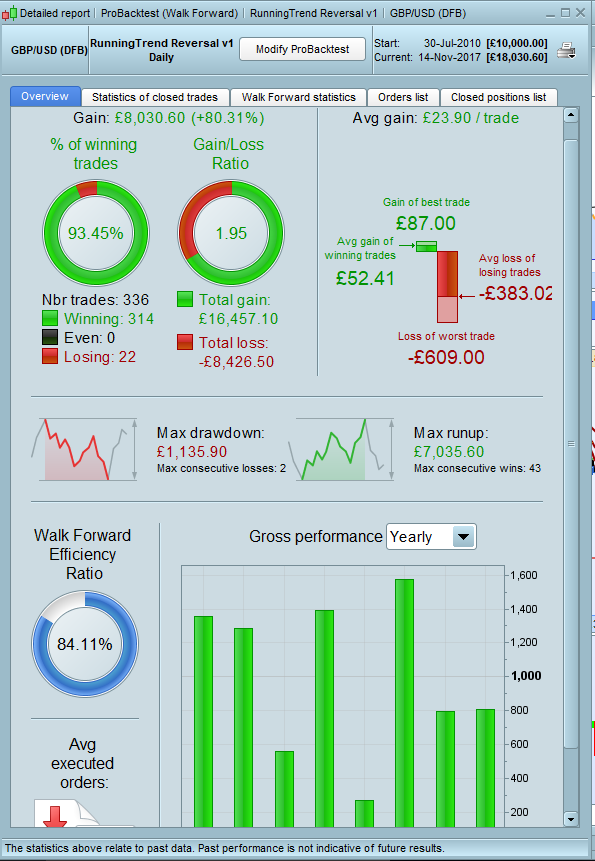

I have not tested this either live or in demo but walk forward testing seems promising.

Walk forward screen shots….

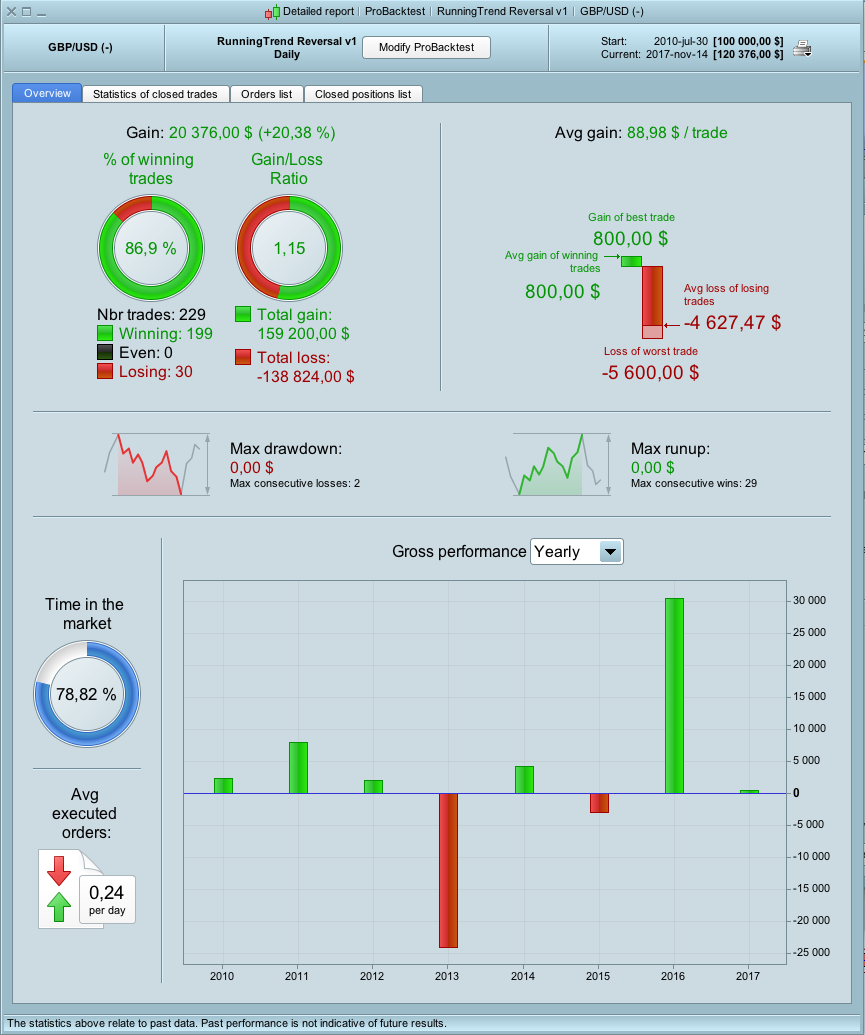

Hmm not getting same results.. Testresults from the same period (2010) gives me 86% winrate and 1.13 gain/loss

but drawdown is near 4K and total loss = 15K$ (GBPUSD mini)

Since im not getting same results i guess its pointless to say but tested on the 200K bar it looks really bad. But then again im getting wrong numbers on the 2010 -> 2017 testing so 🙂

My initial observation is that the strategy is sometimes keeping positions open for many days (3 times for 51 days) so unless you have factored in the daily interest on the open positions it is impossible to say what the real numbers are, or even whether it is profitable or not.

Jebus89 – I don’t know why you are getting different results. Wrong market or wrong timeframe possibly?

Autostrategist. Yes it is a longer term hold and hope strategy that gives up a position after 50 days if it has not won or hit the stoploss. It is not a strategy for those who want to get rich in an hour! From my experience of overnight costs on Forex DFB’s the overnight costs are not so extreme and I have attempted to offset some of this within the strategy. Not many bets run for the full 50 day term most close out within a few days. Whether it is profitable in the real world is an unanswered question that only real money can find out due to the poor quality of backtest data and the hopeless Demo account testing – but that is the same for all strategies. It would be nice if PRT could take into account overnight fees because without this backtest are fantasy.

I read somewhere that surveys of spread betting accounts have shown that those who win are most likely to be those who place few bets and hold for longer so we should not give up on long term strategies just yet.

Any suggestions on improvement or adapting to shorter time frame would be interesting…..

Probably right about longer term holding, I have a mix of strategies, mostly intraday but also some multiday. I seem to recall a strategy on here that attempted to factor in the overnight fees but I don’t think it will ever show in the backtest results probably it was graphing a variable. You could take a stab at working out the average fee per trade and putting that into the Estimated Brokerage Fees section of the BackTest window. Having said that I haven’t been doing this for my own overnight strategies so I’m going to look into that. Don’t know about demo account issues as I only use Live, not recommending it as I have come unstuck a few times, does focus your mind on getting a strategy right before committing to live trading though!

It is not a strategy for those who want to get rich

Alright for some, looks like you already have the yacht 🙂

I don’t think it will be too difficult to calculate in fairly approximate overnight costs as I have done this on another index based strategy – but forex overnight fees are based on the tom-next rate. Does anybody know where I can find a current list of tom-next rates as a quick Google search has failed me so far? I trade with IG and their fees calculation is shown here

https://www.ig.com/uk/learn-to-trade/overnight-funding

They confirmed that fees are only charged if you hold the position at exactly 2200.

A common mistake is to assume that everyone on a yacht is rich. Our yacht is very small and we lack other little comforts in my life such as a house, a car, nights out etc so that we can afford it. A ‘get rich’ strategy would be very handy!

I can’t reproduce your results neither. Attached what I get for the same time period.

Despair – I am on IG GBP/USD (DFB). I notice that your test results show GBP/USD(-). Are we on the same thing? Quite often it seems that the contract/shares/perpoint thing can cause issues. IG seem very tolerant where others are not? Your results are in $ I also notice?