Paul

PaulParticipant

Master

to compare

It’s nonetheless daily version from the pure renko topic, including machine learning

@Paul would you mind sharing the .itf to the above strategy? Thanks in advance.

PaulParticipant

Master

unfortunately results are fake, daily using spread & tick by tick, still maybe the code posted above has some interesting parts.

here used;

set stop %loss 0.01

set target %profit 1.1

Thanks Paul. Is it not working with tick by tick because the box size is too small and during 1 day (1 candle) the price will move more than that value up and down? Perhaps it would be best to launch these in shorter timeframe, although maybe not as short as 10s (!)

The main problem with 10s for me is the short backtest period. I only have 200k bars so it becomes a weekly (4 days) backtest.

PaulParticipant

Master

Hi eckaw Yes the boxsize is too small and doesn’t make sense and also if a high crosses over/under boxsize then buy that level on stop doesn’t work reliable either because of minimum distance. So backtesting using on stop on slower timeframe & much data, in demo buying at market on faster timeframe like 10s. A bit like barhunter strategy setup perhaps.

Hello,

I’m very interesting about this file. I’m a poor programmer, but i try to comprise, what the ea make for take an order.

So i compare the 3 EA, who are on this file (Renko; MySystem; 20201218 renko…)

Here a Board with the different filter use in each EA.

So we can better compare each EA. And search the better optimization

Thank you for sharing these EA.

Hi All,

interesting code, but always same errors when ProOrder trying to go on market.

The stop is too short because of the broker.

Despite i have set manual value on stop.

Any ideas?

Thanks,

I went back and checked the “New Renko System” on this forum and I’m now rethinking my renko strategy to try out this idea of @Verdi55 https://www.prorealcode.com/topic/new-renko-system/page/3/#post-66276

I don’t think my pockets are deep enough to launch 99 simultaneous renko systems, but looking into maybe launching 11 of them on one market with -5 to +5 fixed renko boxed settings on EURUSD. I’m also experimenting with replacing the fixed renko box to an ATR renko box. I’m just worried about the drawdown and I’m trying to calculate this via Excel to make sure there isn’t too much drawdown. I think there is a great potential in this approach though, almost assuming all strategies are slightly wrong but all together the will do very well.

@nicolas_macary Yeah, I still have problems with them running on demo forward test. Still haven’t managed to get rid of the various run-time errors but will check it more tonight!

@eckaw That’s very interesting! What time frame are you considering? Renko seems to show nice potential in the shorter ones but perhaps even more so during 10m-1h? What you say is the same idea of ensemble learning within machine learning, specifically neural networks and is a proven strategy to increase the performance of a system. The most important factor when successfully building an ensemble of networks is that every single network can perform the task at hand in some way and be as different from every other network as possible. Having many different systems performing well in their respective markets / trends / whatever and combining the result is the analogue of the machine learning case. Very cool. Maybe what you say is what is needed especially for renko systems to perform well.

@DjungelJarl the renko systems doesn’t actually take time into consideration, so the only reason why them seem to work ‘better’ on short time frames is because the stop loss works differently on this timeframe compared to same code on longer timeframes.

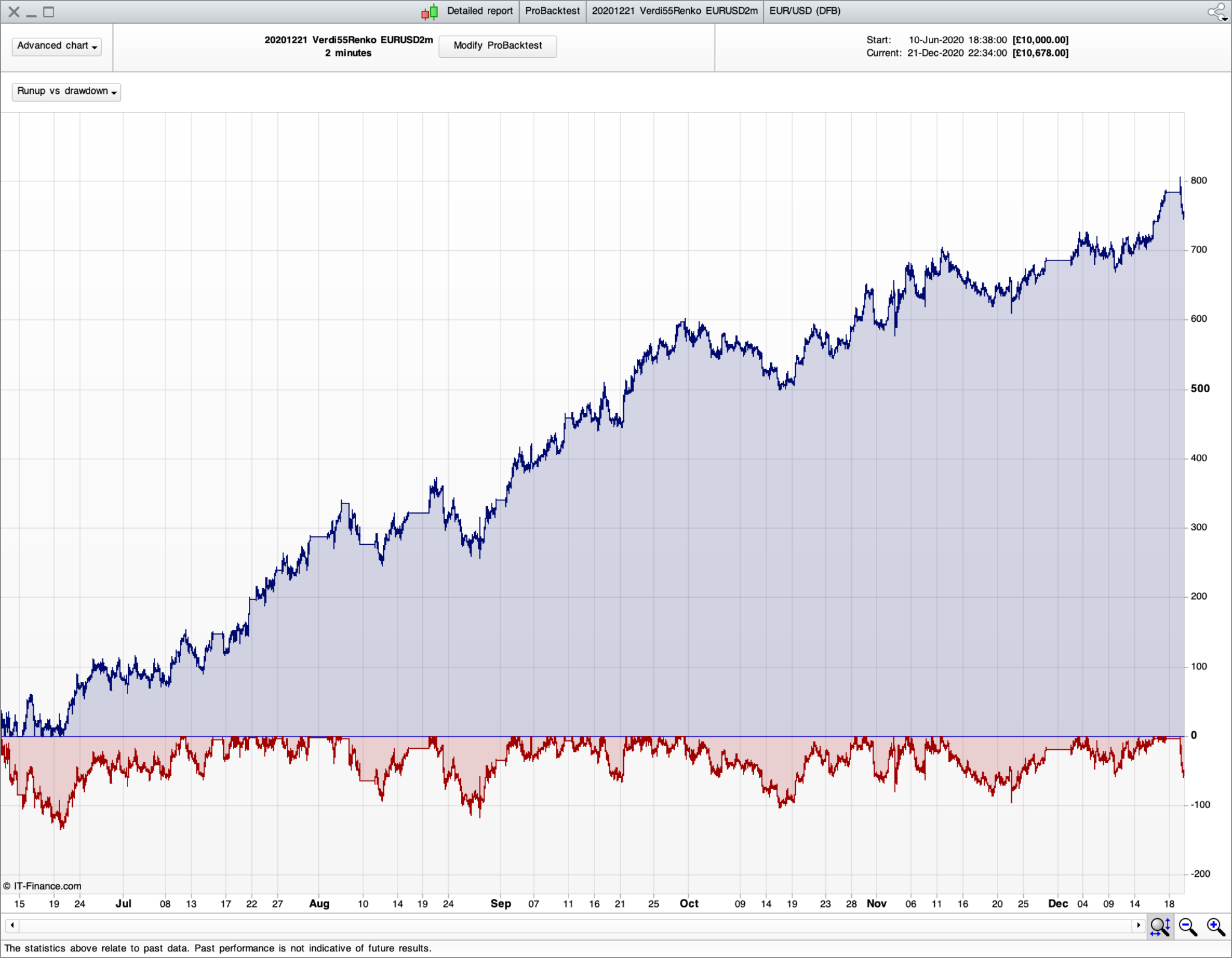

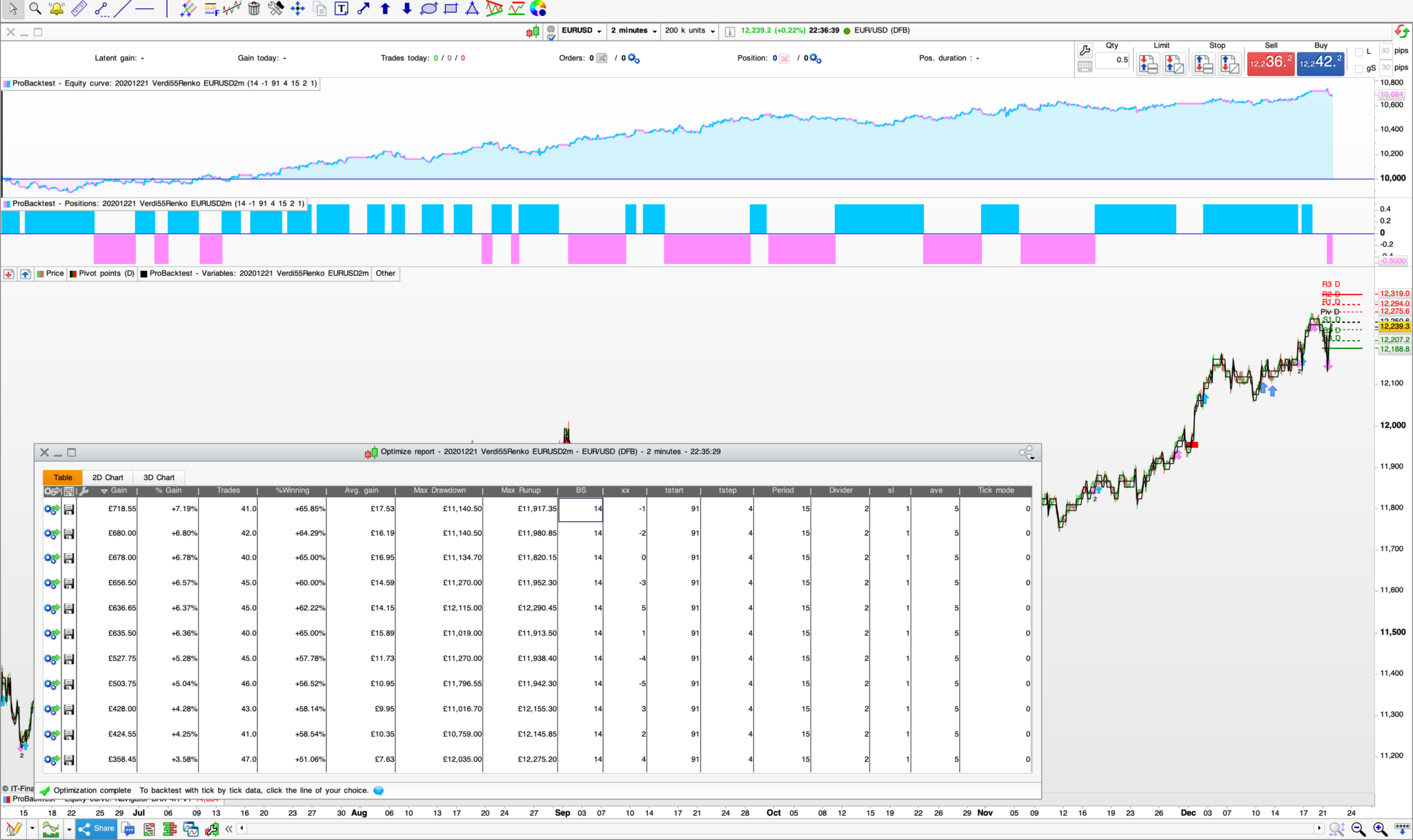

Here’s an example I’m experimenting with now (not tested)

It’s 2min on EURUSD, spread 0.8

The idea would be to launch 11 of these systems simultaneously, with different ‘xx’ settings. In this backtest these 11 systems would have profited £6,247.75 accumulated during the time period 10th June – today.

Sorry there’s something wrong with how I calculated that renko box setting in that .itf, as now it acts simply as a fixed renko box (setting: 14). I’ve got this working before so will update tomorrow.

Thanks for the update, I think this approach is promising to say the least. Will also do my own tests and get back

changing

once boxsize = ATRperiod

to

once boxsize = converted

seems to fix that issue I mentioned. I’m not sure it is the correct way to use ATR Renko but it seems to give similar results with a dynamic box size which might (or might not) work better longterm.